<<< This blog post is also available as a YouTube video. >>>

From Alexander Weis and Selina Gschichtmann

This blog post is a brief introduction to passive investing. We would like to help those who would like to get a compact overview of investing with ETFs before they buy one Deep dive with a more comprehensive one Book by Dr. Gerd Kommer dare.

This article assumes moderate prior knowledge of the stock market. This means that you should know roughly what a share, a bond and an ETF are and at least be able to understand concepts such as return and risk in principle. (If you would like to refresh your knowledge on this, you could do so by taking a look at our glossary in which we explain the most important technical terms in the field of investment.)

In a first step, we provide an overview of the most important forms of investment; in a second step, we examine their returns and risks. We then address the crucial question of investing (“Do I want to be an active or passive investor?”) and show why passive investing is the superior alternative to active approaches. Finally, we present a “recipe” for a passive portfolio consisting of just two ETFs – it couldn’t be simpler.

If you are already familiar with the basics of passive investing, we recommend our more advanced blog post “Factor investing – the basics“.

Are you convinced of passive investing and want to implement it easily and conveniently? We have Gerd Kommer's 1 ETF solution: The L&G Gerd Kommer Multifactor Equity UCITS ETF. Find out more >

Let's get started!

Asset classes – an overview

So that there are no misunderstandings, a classification in advance: In this article we deal exclusively with liquid assets, i.e. h. Types of assets like Human capitalWe leave out investments, company investments or pension insurance claims. There are two reasons for this: firstly, the active-passive debate is irrelevant for most types of illiquid assets because they can ultimately only be managed actively, and secondly, that would go beyond the scope of our short introduction.

What are asset classes? Asset classes are logical groupings of assets that are relatively similar in terms of return, risk and liquidity.

Here is an overview of the most important asset classes:

- Stocks: equity investments in listed companies

- Bonds: Exchange-traded loans to governments or companies

- Real estate: residential and commercial properties

- Raw materials: Natural resources such as oil, base metals or agricultural raw materials

- Precious metals: Subgroup of raw materials (such as gold, silver or platinum)

- Collectibles: art, luxury cars, luxury watches, fine wines, etc.

- Cryptocurrencies: Bitcoin, Ethereum, Tether, etc.

These are the asset classes in which private investors can invest with acceptable effort and at reasonable costs.

Contrary to popular belief, a bank deposit is not an asset class, but rather an unsecured loan from the depositor to a financial institution (more on this in our blog post “The underestimated risk of bank deposits“).

Financial products such as capital-forming ones Insurance, open real estate funds, Private equity, Hedge funds, actively managed investment funds and ETFs are also not their own asset classes, but merely “packaging” for real asset classes. Such “shells” are not bad per se and differ primarily in their material thickness, with hedge funds (thick and expensive) at one extreme and ETFs (light and cheap) at the other extreme of the spectrum. In the case of many financial products, the packaging leads, in addition to costs and loss of transparency, to additional risks that the asset class within the financial product itself does not have.

Let's carry on!

Return and risk – which asset classes are the best?

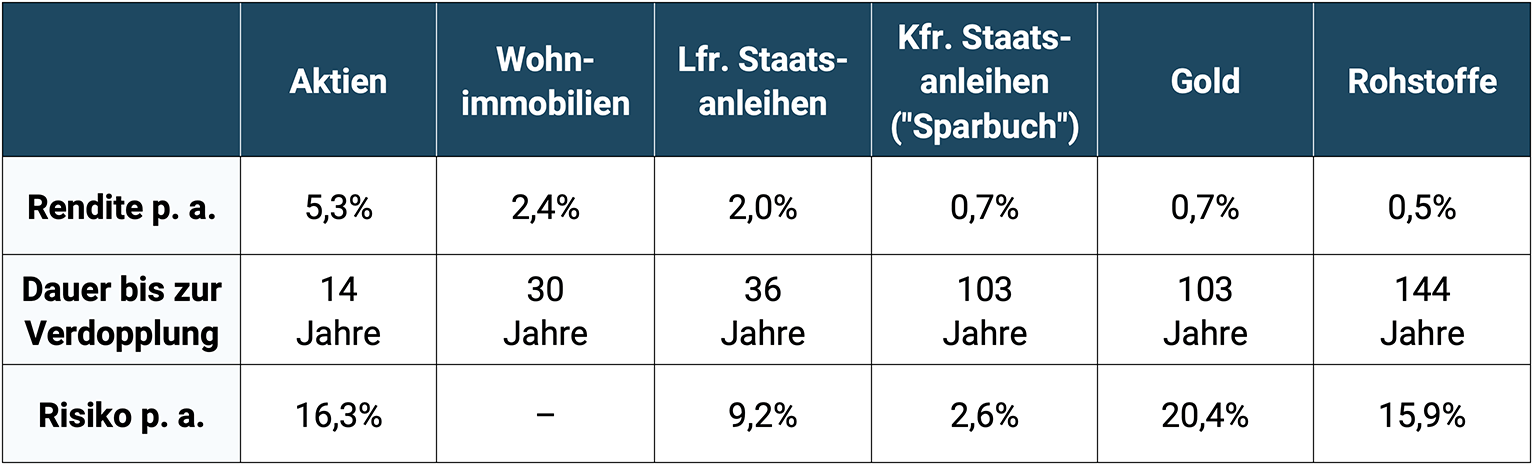

In order to find an answer for yourself as to which asset class you should invest in, you first have to be clear about what goal you are actually pursuing by investing. As a rule, the answer will be: “Achieve the highest possible return with the lowest possible risk”. Therefore, in Table 1 we take a look at the return and risk of our main asset classes (cryptocurrencies are not included in the table due to their too short data history; collector markets are missing due to lack of data availability):

Table: 1: Inflation-adjusted long-term returns of the most important asset classes (in USD) from 1900 to 2021 (122 years)

► Data: Dimson, Marsh, Staunton (2022); Morningstar; David S. Jacks (Gold, Commodities) ► Excluding costs and taxes (maintenance costs for real estate included) ► All returns in US dollars (excluding residential real estate - see below) and total returns (sum of current income + appreciation) and adjusted for inflation ► Residential real estate returns: Different period from 1900 to 2017 and population-weighted average of the returns of nine western countries in local currency (Reason: lack of data availability) excluding return-reducing transaction costs when buying and selling ► "Duration until doubling": Number of years until an initial one-off investment would have doubled at the given average return (excluding costs and taxes) ► "Risk": Standard deviation of the calendar year returns (volatility) from 1975 to 2021. No value is given for real estate because it is real, "honest" and fair with the other asset classes There is no comparable data available (see our blog post). “The risk of investing in real estate”).

What can be seen from the table? The first thing you notice is that the numbers are probably significantly lower than most of us would assume. One reason for this is that these are real returns, i.e. returns after deducting inflation. Another reason is that the media, the Internet and advice books in general have given us an exaggerated idea of realistic returns. The bare numbers in the table are what the capital markets have provided over the last 120 years, without any illusionary fantasy performance. You will have to come to terms with this reality for better or for worse - whether you want to or not, but more on that below.

Secondly, it is clear that stocks have by far the highest returns of all asset classes: twice as high as real estate, two and a half times as high as long-term government bonds and six times as high as gold and savings accounts. 👊🏻

Thirdly, it shows that short-term government bonds are the lowest risk asset class of all asset classes – again by a wide margin.

What do we learn from this? If you want to get the most return from your money, there is no way around stocks. However, since most investors cannot or do not want to live with the strong fluctuations of stocks, a stock investment should be supplemented with a less volatile component. Due to their low fluctuation intensity, short-term high-quality bonds or an interest-bearing bank deposit (as long as the amount is within the state deposit insurance) are best suited for this purpose.

So much for the preliminary banter - now it's time to get down to business!

Active vs. passive investing – the crucial question

Anyone who wants to invest their money on the stock market in securities such as stocks or bonds will sooner or later be confronted with the question of whether an active or passive investment approach makes more sense. But what is active and passive investing all about? (In order to keep the matter as simple as possible, we will limit ourselves below to stocks and leave out the bond market.)

To put it simply, a passive investor simply buys the “market” (in our case, the stock market). At the end of the day, he receives the market return (minus the costs of investing) and is therefore fully exposed to market fluctuations. (“Buying the market” is done by purchasing one or more ETFs.) As we saw above, a good 5% return per year can be achieved in the stock market after deducting inflation, but before deducting taxes and costs.

An active investor, on the other hand, is not satisfied with the market return and believes that it is possible to beat the market systematically. You can do that attempt, either by buying the stocks that you believe will outperform the market (“stock picking”) or by “entering” the market whenever it is at the bottom and “getting out” again just before the next suspected crash (“market timing”). Active investing is inevitably always a form of stock picking, market timing or a mixture of both. You can actively invest as a do-it-yourself (“DIY”) investor or by using an advisor (such as a bank or asset manager).

If you believe in active investing and don't want to be a DIY investor, you can outsource it to a fund manager, an asset manager or a bank for relatively high open and hidden (difficult to detect) fees. We have a separate blog post about how well this works in the case of well-known actively managed funds entitled “The misery of flagship fund investors(Spoiler: Title says it all).

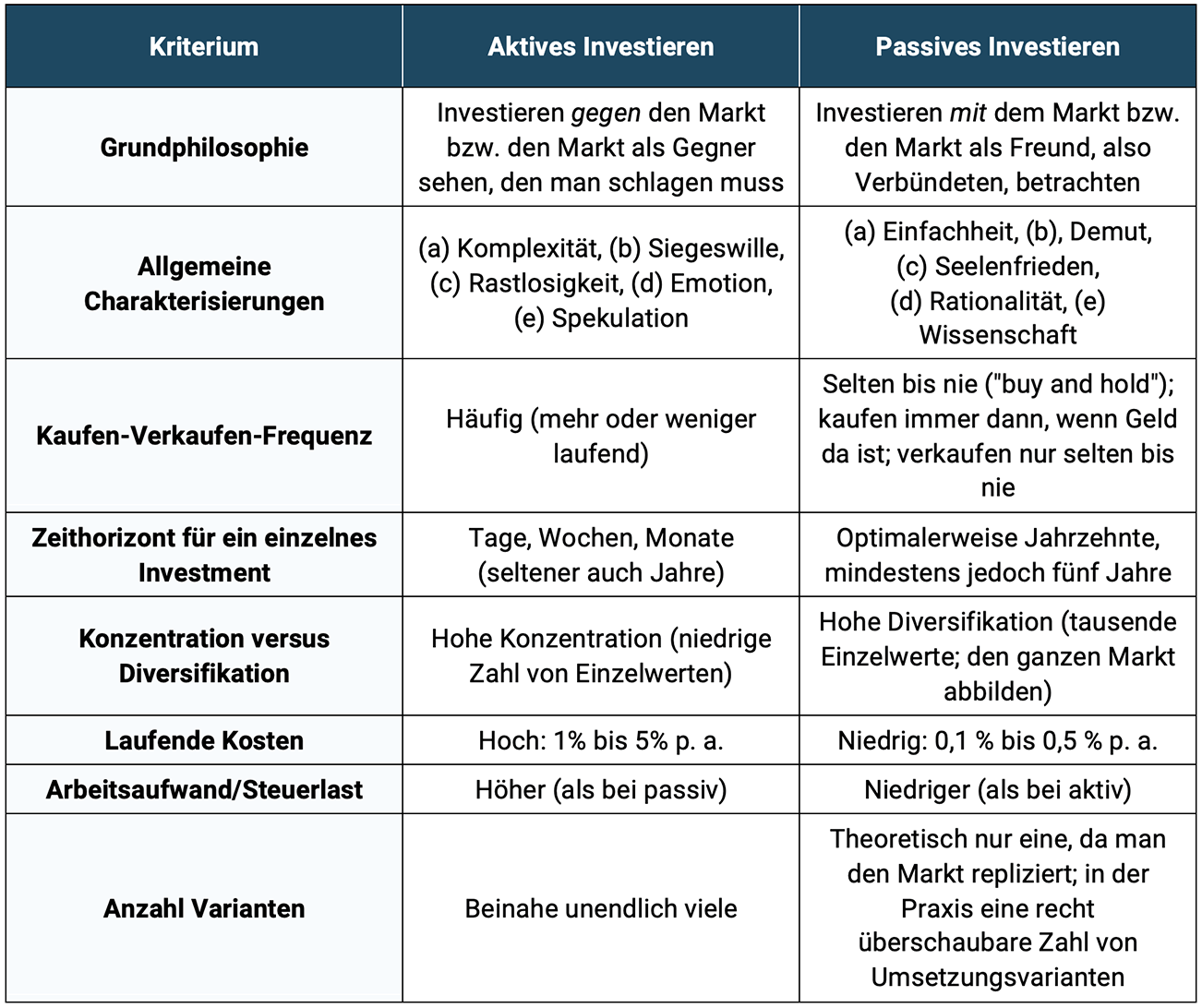

For all those who have lost their way with all the metaphors, we have conjured up Table 2, which explains the differences between active and passive investing in a somewhat drier and more concise form:

Table 2: The biggest differences between active and passive investing

► Source: The easy entry into the world of ETFs by Gerd Kommer

So why invest passively?

The short answer is: Because it is more profitable.

This statement does not come from us, but from science. Over the past 60 years or so, literally thousands of studies have been published demonstrating the statistical superiority of passive investing.

However, since from a financial service provider's perspective you can earn significantly more money with active investing than with passive investing, the established financial industry - science or not - almost exclusively offers active investing.

Active investing is also more profitable for traditional media and the Internet because you can achieve higher circulation and a higher click rate with stories about active investing and speculation - let's not even get started on the advertising revenue from providers of actively managed financial products.

In any case, the scientific evidence that passive investing is superior to active investing is literally overwhelming. But in order not to leave it at guesswork, we base our line of argument on one theoretical and empirical argument from science and then let the numbers speak for themselves.

Theory: The arithmetic of active investing

The arithmetic of active investing says that all investors must collectively generate the market return because, by definition, they together make up the market. This in turn means that 50% of all invested amounts of money must generate a return below and the other 50% must generate a return above market returns. It is important to emphasize that this is a mathematical necessity that cannot be argued away. No further assumptions about costs, taxes and the composition or behavior of market participants are necessary.

Back to the argument: That means that – before Costs (!) – 50% of all active investors beat the market and, conversely, 50% underperform the market must. If we further assume that active investing has higher costs than passive investing – see “Ongoing costs” in Table 2 – the proportion of active investors who beat the market must be between 0% and 50%. This means that the purely statistical probability of outperforming the market is strictly less than 50% and is therefore lower than the probability of winning a coin toss duel. In order to find out how high this proportion is in practical reality, we build a bridge and take a look at our empirical argument.

Empirical: Outperformers are as reliable as a zero in roulette

The practical part of our argument is based on a study by S&P Dow Jones Indices, one of the larger index providers in the world, which has the somewhat cumbersome title “Standard & Poor's Index Versus Active“, or “SPIVA” for short. In the study, the performance of actively managed funds is compared to a fair passive benchmark, which allows conclusions to be drawn about the success of active investing over different time periods and geographical regions. (There are a number of comparable studies that come to similar results, but we chose the SPIVA study because it is one of the most thorough of its kind, has been updated every six months for 20 years, and is publicly available free of charge.)

Two primary conclusions can be drawn from the SPIVA study:

- Outperformers are in the minority: The proportion of actively managed funds that beat their passive benchmark was on average around 40% across all regions (industrialized and developing countries) in the last three years from 2019 to 2021 and only around 10% over the last 20 years from 2002 to 2021 (the extent and number of underperformers increases with the length of the observation period). The obvious question is why not simply invest in this minority, which brings us to the second conclusion.

- Outperformers rarely remain outperformers: the composition of funds that manage to beat their benchmark changes more or less randomly from period to period. Of the top 25% of the equity funds examined in 2017, only 62% managed to land back among the top 25% in the following year, 2018; In 2019 it was 37%; In 2020 it was only 28% and in 2021 it was 1.7%, which was barely noticeable even with a magnifying glass. (For bond funds, the proportion fell to 0 in the third year of 2020). The popular method of only investing in funds that have performed particularly well historically is doomed to failure.

We will simply leave these, in our eyes, powerful findings as they are and thus conclude our argument against active and for passive investing. If you are not yet completely convinced of the advantages of passive investing and/or would like to read further arguments against active and for passive investing, we would like to provide you with our blog post “Ten reasons why active investing works poorly“ to the heart.

If we have already convinced you, then we are pleased and as a thank you we have brought a very special treat for you at the end: a simple recipe for a delicious, juicy passive portfolio consisting of just two ETFs.

How does passive investing work?

Passive investing has been easy in principle since the invention of index funds in the early 1970s and ETFs as a variant of index funds in the early 1990s. Basically you just have to do two things:

Firstly, determine the percentage division of your portfolio between the risky and low-risk parts of the portfolio (e.g. 60/40) and secondly, fill the two parts of the portfolio with specific ETFs.

This static asset allocation is implemented on a strict buy-and-hold basis. Buy-and-hold is part of passive investing, as is broad global diversification through the use of index funds and ETFs.

This is the scientifically derived world portfolio concept of Dr. Gerd Kommer. In the simplest case, one ETF product for the risky part of the portfolio and one for the low-risk part of the portfolio are sufficient. We have illustrated this in the following graphic.

Graphic: Schematic representation of the world portfolio

► Source: The easy entry into the world of ETFs by Gerd Kommer. ► (*) Daily money only if the amount is within the state deposit insurance of a country with a credit rating of at least AA.

The risky part of the portfolio (“RBT”) acts as a “return engine” responsible for generating the portfolio return, while the low-risk (“risk-free”) part of the portfolio (“RFT”) serves as a “security anchor”. We call this dichotomy the Level 1 asset allocation. Basically, all allocations from 100% RBT/0% RFT (“100/0 portfolio”) to 0% RBT/100% RFT (“0/100 portfolio”) are conceivable, but the music usually falls somewhere in between, as few investors will prefer the marginal allocations.

Where specifically a given investor household falls on the RBT-RFT spectrum depends primarily on four variables: return expectations, risk-bearing capacity, liquidity requirements and investment horizon. The stronger the expression of these variables (with the exception of liquidity requirements), the more risky (“aggressive”) the division of a portfolio can be determined. Conversely, if the variables are less pronounced, one should start with a lower-risk (“more conservative”) Level 1 asset allocation.

If the variables differ in their characteristics, it is advisable to focus on the most conservative one at least initially and then make further gradual adjustments in the following years as personal experience with the portfolio has been gained. (If you would like to find out more about historical stock market crashes over the last 120 years, you can here do.)

Once you've settled on a Level 1 allocation, you need to choose specific ETFs - we call them the Level 2 asset allocation. In the simplest form, this can be implemented with one ETF for the RBT or RFT. The RBT ETF should reflect the global stock market as completely as possible, while the RFT ETF only includes bonds i). short remaining term, ii) with a high credit rating and iii) in the Investor's home currency should be included in order to fulfill its risk-reducing function.

In its simplest form, such a portfolio could look like this:

- Risky portfolio part (“RBT”): Vanguard FTSE All-World UCITS ETF (ISIN: IE00BK5BQT80) [as of September 2022] or L&G Gerd Kommer Multifactor Equity UCITS ETF (WKN: WELT0A)

- Low-risk portfolio portion (“RFT”): Lyxor EuroMTS Highest Rated Macro-Weighted Govt Bond 1-3Y (DR) UCITS ETF (ISIN: LU1829219556) [As of September 2022]

Alternatively, the low-risk part of the portfolio could also be represented via a current or fixed-term deposit account at a bank, provided that the investment amount is within the state deposit insurance of 100,000 euros per customer-bank combination.

Please note that this is explicitly not an investment recommendation, but rather just an illustration of how easy it is to implement a passive investment approach. The world portfolio can be further refined as desired (e.g. by adding so-called Factor premiums; However, explaining the theory and practice behind so-called factor investing would go beyond the scope of this article). If you are interested in this and want to take care of your investments yourself, take a look at them Advice books by Dr. Gerd Kommer.

Once the portfolio has been defined and the ETFs purchased, you should ensure at regular intervals that the current level 1 asset allocation does not deviate too much from the desired target allocation, even over longer periods of time. The background to this are market fluctuations to which a portfolio (especially the RBT) is exposed every day. The manual return to the target allocation is called rebalancing and we have already written a detailed blog post about this with the title “Rebalancing: advantages, methods, principles" published.

Conclusion

In this article we looked at what asset classes there are and which of them you should definitely have in your portfolio. For the vast majority of private investors, a mixture of stocks as a “return engine” and bonds as a “security anchor” in the portfolio is likely to be suitable. We then looked at the active-passive investing debate and looked at the differences between active and passive investing, then used theoretical and practical arguments to demonstrate why passive investing is the superior alternative to active investing. Last but not least, we discussed the practical implementation of a passive portfolio (this is often referred to as Dr. Gerd Kommer's world portfolio concept) and also pointed out the importance of the rebalancing principle.

Investing in a global portfolio means making capital available to the global economy. With the help of this capital, over 10,000 listed companies worldwide can produce goods and services that almost eight billion people on our beautiful planet Earth need every day to ensure their very survival and to improve their standard of living compared to their parents' generation. For the provision of risk capital in the form of stocks and bonds, the global portfolio investor is compensated with a return commensurate with the risk.

literature

Dimson, Elroy; Marsh, Paul; Staunton, Mike (2019): “Credit Suisse Global Investment Returns Yearbook 2018”; long version; Credit Suisse Research Institute; 256 pages

Kommer, Gerd (2018): “Invest confidently with index funds and ETFs. How private investors win the game against the financial industry”; Campus Verlag, 5th edition, 2018 (first edition 2002); 415 pages

Kommer, Gerd (2022): “The easy entry into the world of ETFs: Uncomplicated provision – a starter book for financial beginners”; FinanzBuch Verlag, 1st edition, 2022; 180 pages

Kommer, Gerd; Großmann, Felix (2020): “The Corona Crash: What to do?”; blog post; March 2020; Link: https://gerd-kommer.de/blog/corona-crash/

Kommer, Gerd; Großmann, Felix (2022): “Open-ended real estate funds – illusion and reality”; blog post; January 2022; Link: https://gerd-kommer.de/blog/offene-immobilienfonds/

Kommer, Gerd; Riemensperger, Jakob (2021): “The misery of flagship fund investors”; blog post; November 2021; Link: https://gerd-kommer.de/blog/flaggschiff-fonds-elend/

Kommer, Gerd; Schweizer, Jonas (2018): “The risk of investing in real estate”; blog post; August 2018; Link: https://gerd-kommer.de/blog/das-risk-von-direktinvestments-in-immobilien-besser-verstanden/

Kommer, Gerd; Schweizer, Jonas (2019): “The underestimated risk of bank deposits”; blog post; August 2019; Link: https://gerd-kommer.de/blog/risk-von-bankguthaben/

Kommer, Gerd; Schweizer, Jonas (2020): “Capital-forming life insurance – a German wrong turn”; blog post; March 2020; Link: https://gerd-kommer.de/blog/hauptbildende-lebensversicherung/

Kommer, Gerd; Schweizer, Jonas (2021): “Rebalancing: Advantages, Methods, Principles”; blog post; December 2021; Link: https://gerd-kommer.de/blog/rebalancing/

Kommer, Gerd; Weis, Alexander (2018): “Currency hedging: when does it make sense and when does it not?”; blog post; January 2018; Link: https://gerd-kommer.de/blog/wann-ist-waehrungsabsicherung-sinnvoll/

Kommer, Gerd; Weis, Alexander (2018): “Warren Buffett’s Hedge Fund Bet”; blog post; March 2018; Link: https://gerd-kommer.de/blog/warren-buffetts-hedge-fonds-wette/

Kommer, Gerd; Weis, Alexander (2019): “Factor Investing – the Basics”; blog post; May 2019; Link: https://gerd-kommer.de/blog/factor-investing-die-basics/

Kommer, Gerd; Weis, Alexander (2020): “Ten reasons why active investing works poorly”; blog post; February 2020; Link: https://gerd-kommer.de/blog/warum-aktives-investieren-bad-funktioniert/

Kommer, Gerd; Weis, Alexander (2020): “The Pains of Factor Investing”; blog post; May 2020; Link: https://www.gerd-kommer-invest.de/pains-of-factor-investing/

Kommer, Gerd; Weis, Alexander (2021): “Private Equity – Desire and Reality”; blog post; April 2021; Link: https://gerd-kommer.de/blog/private-equity-wunsch-und-realkeit/

Kommer, Gerd; Weis, Alexander (2022): “Bonds and interest rate changes – a case study”; blog post; June 2022; Link: https://gerd-kommer.de/blog/anleihen-und-zinsaenderungen/

S&P Dow Jones Indices LLC (2021): “Standard & Poor’s Index Versus Active”; As of December 2021; Link: https://www.spglobal.com/spdji/en/research-insights/spiva/