From Alexander Weis and Gerd Kommer

You can demonstrate the superiority of passive investing - i.e. buy-and-hold investments with index funds - over traditional active investing in different ways: By a book Writes about “active versus passive” by publishing a scientific study on aspects of the topic [1] or – particularly entertaining – by betting with active investors. The great Warren Buffett did the latter in 2007, shortly before the start of the financial crisis. At that time he made a bet with a certain Ted Seides. Seides was at the New York financial boutique Protégé Partners employed investment advisor. The bet was about whether an expert like Seides could select a group of particularly good hedge funds that would, over the long term, outperform a simple, broadly diversified, low-cost, buy-and-hold index fund. Buffett said no, the hedge fund expert said yes.

In order to ensure that the special conditions of a single year would not distort the result, the two opponents agreed on a sufficiently long betting period, namely the ten years from January 1st, 2008 to December 31st, 2017. The loser of the bet would have to pay the winner a million dollars. The winner committed to donating the prize money to a charitable organization of their choice.

Buffett relied on the “Vanguard 500 Index Fund” (US-WKN: VFINX), an index fund that tracks the S&P 500 stock index, i.e. the 500 largest listed companies in the USA. [2] Seides selected five funds of hedge funds. [3] The simple average of these five funds should represent the hedge fund return relevant to the bet, according to wagering requirements.

Overall, the bet was designed in such a way that (a) it did not look at returns over a perhaps unrepresentative short-term period; (b) the performance of a rare positive or negative “outlier hedge fund” should not be the determining factor; and (c) not the “mere average” of all around 10,000 hedge funds worldwide, i.e. a broad hedge fund index, was used. Rather, hedge funds should bet in a limited number in the long-term future best Hedge funds are represented. These funds should be selected by a hedge fund professional. In the words of Warren Buffett: “This assemblage [the fund of hedge funds] was an elite crew, loaded with brains, adrenaline and confidence.” (In German: The collection of an elite with brains, adrenaline (i.e. ambition, energy) and self-confidence.) [4]

Ultimately, the initial situation at the start of the bet was comparable to that of many institutional and private investors in hedge funds before they decide to invest in the supposed “precious segment”: They know the best hedge funds in the past, use this past data as the primary selection criterion, but do not know how their selection will perform in the future. Because investors sense this uncertainty, they typically do not put all their eggs in one basket, but rather invest in several funds at the same time.

In retrospect, the ten-year period covered by the bet was a roller coaster, the intensity of which is only likely to be achieved in a minority of all future decades. The following happened in the ten years: the most severe global economic and financial crisis in 80 years, the malaise in the Eurozone that has been ongoing since 2008 with record levels of government and private household debt in most EU countries, the now forgotten "flash crash" of 2010, the dramatic collapse in oil prices from 2015 onwards, negative nominal yields on government bonds for the first time from 2016, one (not yet completed) European refugee crisis, a further intensification of Islamic fundamentalism, the Brexit vote in Great Britain (2016), the election of Donald Trump as US President (2017), the Syrian war in the Middle East and the North Korean conflict - to name just the most important events. The events described were naturally accompanied by dramatic price falls and gains, such as: B. a maximum price loss of the global stock market of 57% in real terms in February 2009 or a breathtaking price rally of +78% in real terms in the 24 months thereafter (all data in euros).

So one thing is clear: this ten-year period is not fair-weather data. There were more than enough opportunities for the “Kings of Wall Street” to outperform a simple buy-and-hold strategy in the form of an S&P 500 index fund investment. In other words: When not then, when?

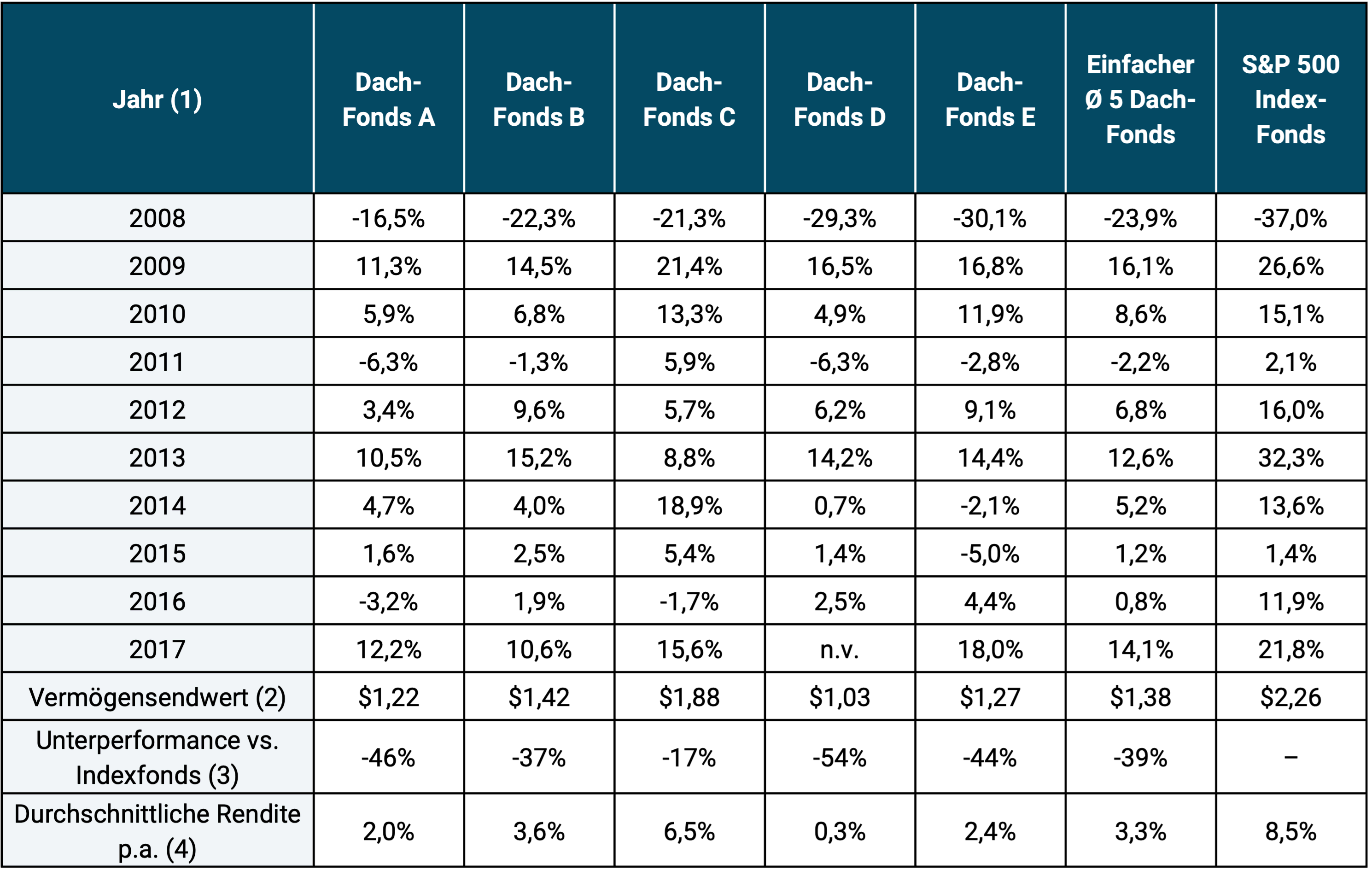

But let's look at the raw numbers in the table below. They are so clear and unambiguous that commenting is almost unnecessary.

Table: Nominal returns of the fund of hedge funds and the index fund in the ten-year bet between Warren Buffett and Ted Seides (in USD)

► Source: Berkshire Hathaway, Annual Report 2017. ► Returns after costs and before taxes, nominal in US dollars. ► The names of the funds of hedge funds have not been published in accordance with official betting conditions. ► (1) Returns for all individual years from January 1st. until 31.12. ► (2) Final value of an initial dollar invested after 10 years. ► (3) Relative final asset value compared to the Vanguard index fund. ► (4) Geometric return per annum (Compound Annual Growth Rate).

What can you say about the numbers in the table? First of all, the failure of the elite funds is so blatant that even we - outright skeptics of active investing - were astonished:

- Not a single one of the five funds of hedge funds was able to beat the S&P 500 index fund over the ten-year period. (However, only the average of the five funds of funds was decisive for the bet).

- The best of the five funds of funds underperformed the S&P 500 by 17%, the worst by a shocking 54%.

- One dollar initially invested became $2.26 in the Vanguard index fund. On average, this dollar only grew to a little more than half (1.38 dollars) across the five hedge funds.

In recent years, however, hedge funds have not only shown themselves to be a bad soap opera in the Buffet-Seides bet. The entire global hedge fund sector (measured by the HFRX Hedge Fund Index) has underperformed the global stock market (MSCI-ACWI index) in 14 out of 15 calendar years since 2003. The cumulative underperformance of the hedge fund sector over these 15 years is so dramatic that one might actually feel sorry for the “rainmakers” were it not for the fantastic salaries with which they are paid for this underperformance. This kind of thing is otherwise only available at Deutsche Bank.

Ted Seides, Buffet's betting partner, even turned out to be a bad loser in the end. At the end of 2017 (shortly before the already foreseeable defeat), he pointed out in an interview that the S&P 500 had suffered a cumulative loss of around 50% in 2007/2008, i.e. in the first 14 months of the bet, while his hedge fund portfolio had only fallen half as much, at around -25%. According to his argument, many S&P 500 investors "dropped out" in 2008 and did not participate in the subsequent market recovery, while hedge fund investors were much more likely to "stay tuned."

It's just unfortunate that this claim firstly had nothing to do with the betting conditions and secondly, Seides couldn't substantiate it for the specific Vanguard index fund. Nevertheless, the Seides objection should give us all something to think about: Only those who are actually continuously invested in the market and who are willing to endure this volatility will probably benefit from the very volatile but high long-term stock market returns. “Getting out” now and then largely leads to long-term under-returns. Actually, that should be clear. Returns are risk premiums. If you don't want to take any risk, you can't have any return - except through luck, and this luck is mirrored by just as much bad luck.

Another, although not new, insight that comes indirectly from the bet: the additional costs of investing play a central role in long-term investment success. These additional costs were probably twenty times higher for the hedge funds than for the Vanguard index fund. The usual cost range for hedge funds is 2% management fees plus performance fees. The latter has an annual impact of around another percentage point in the long term, provided the fund achieves a medium or high return (which, of course, was not the case for the fund of hedge funds selected by Seides in most years).

The stake, which was parked as security in American government bonds during the bet, was already agreed between the parties in November 2012 in shares in Warren Buffett's investment holding company Berkshire Hathaway converted to maximize the amount that should be donated to charity when the bet matures. At the beginning of 2018, $2.2 million went to Girls Incorporated of Omaha, a charitable organization that supports disadvantaged girls in the US state of Nebraska.

Conclusion

The bet between Warren Buffett and Ted Seides showed once again that conventional, i.e. “active” investing typically leads to poor investment results; even if you hire the “best of the best” for it. Because this is the case, Warren Buffet - possibly the most successful active investor of the past six decades - has stipulated in his will that the portion of his assets that goes to his wife should be invested almost entirely in the Vanguard 500 Index Fund. Of course, the clever Buffett knew that he would win the bet, because it ultimately only replicated what science had previously proven many times: over a sufficiently long period of time, between 70% and 100% of all active investors underperform a correctly chosen passive benchmark and the small minority of active “winners” cannot be reliably predicted.

Endnotes

[1] There are probably more than 2,000 of these that have been published since around 1960. The vast majority of these studies say: (a) Overall, active investing – in its countless variations – has produced “negative alpha” in the past (i.e. collectively led to investor damage). (b) There is a lack of convincing evidence why things should be different in the future.

[2] This is also the world's first index fund for private investors. It was released in the USA on August 31, 1976. His investment volume in March 2018 was a gigantic USD 410 billion - almost as much as all of the 300 funds of the largest German fund company DWS combined.

[3] A fund of funds is a fund that invests in funds rather than in individual securities. The underlying idea is that the fund of funds manager is able to select the best “individual fund managers” over time. The best-known (conventional) fund of funds house in Germany is the Sauren Financial Group.

[4] The exact wording of the bet can be found in the annual report of Berkshire Hathaway (Buffet's investment holding company) (for the link see “Literature” below).

literature

Berkshire Hathaway Inc.: “Annual Report (2017)”; Internet reference: here (last accessed on March 23, 2018)