The L&G Gerd Kommer Multifactor Equity UCITS ETF is unique: a All Cap- and All Market-ETF with innovative regional weighting and integrated Factor investing. Translated, this means: an ETF on the “World AG“, which is at the Country weighting both those Market capitalization as well as that economic performance (GDP) taken into account, Factor premiums overweight and one ultra-wide Diversification with over 4,000 stocks.

The Gerd Kommer ETF is as accumulating variant (WKN: WELT0A) and distributing variant (WKN: WELT0B) Available at all major banks and brokers - many of which also offer it as a free savings plan to. Learn more

If you want to know more about the underlying Gerd Kommer Multifactor Equity Index If you would like to find out more, we recommend our blog post „The Gerd Kommer ETF”. If you want to understand all the technical details, we recommend the Index methodology or the Quarterly Index Summary.

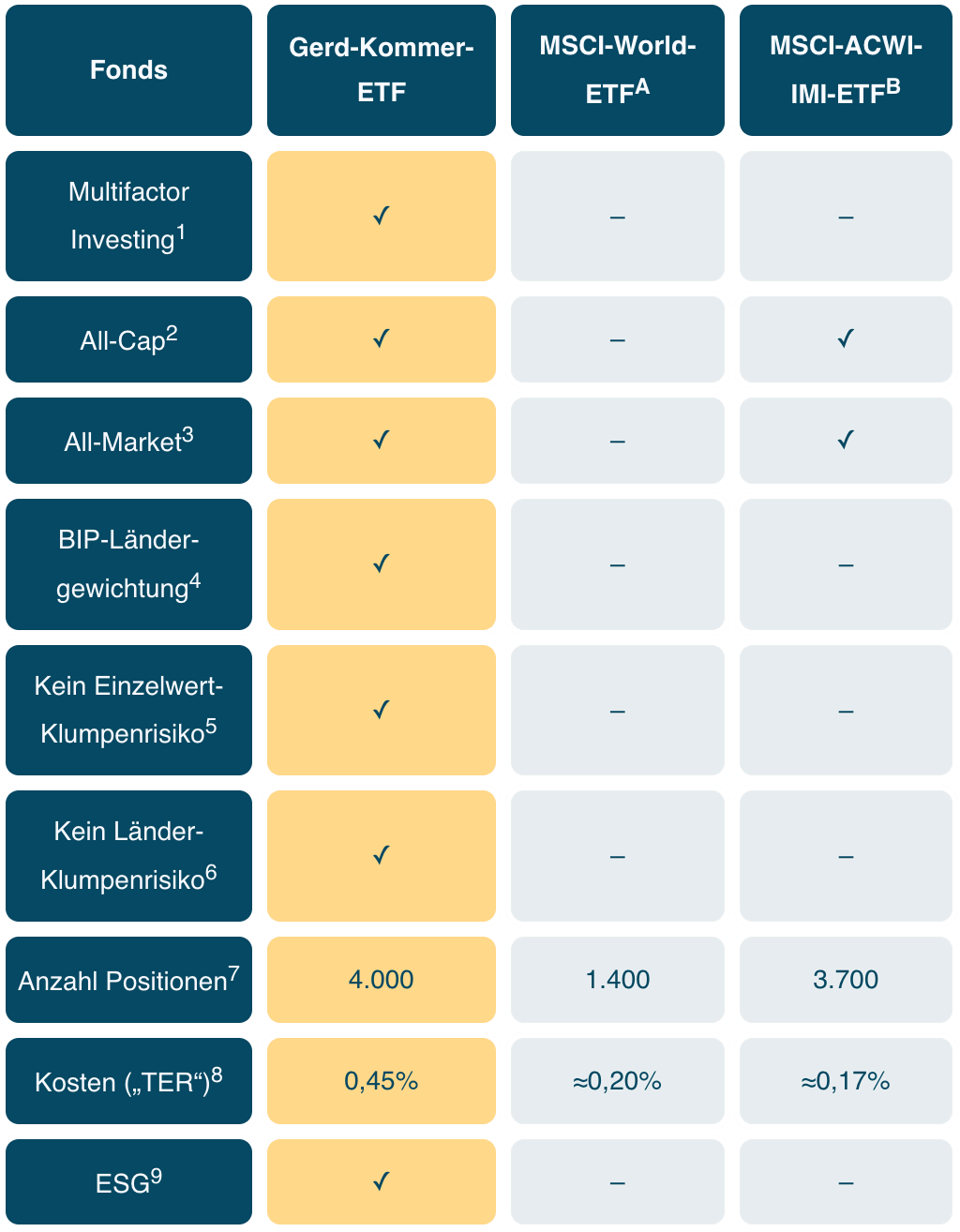

The L&G Gerd Kommer Multifactor Equity UCITS ETF is the 1-ETF solution for the risky equity part of Gerd Kommer's world portfolio concept. This puts it in direct competition with other ETFs on “Welt-AG”, i.e. a highly diversified equity investment in the listed part of the global economy, such as B. is possible by purchasing an ETF on an MSCI World, MSCI ACWI or FTSE All-World index.

When constructing the Gerd Kommer Index, we took up the weaknesses of the existing alternatives and addressed them. In the Gerd Kommer ETF, which replicates the Gerd Kommer index, both emerging markets (missing from the MSCI World, for example) and small caps (missing from the FTSE All-World, for example) are taken into account. Furthermore, when weighting countries, the Gerd Kommer ETF takes into account not only the market capitalization of each country but also its economic performance (measured by GDP), which effectively reduces cluster risks at country level (e.g. around 70% USA in the MSCI World).

In the following table we have compared the Gerd Kommer ETF with the best-known standard world stock market ETFs, i.e. ETFs on the MSCI World, the MSCI ACWI IMI and the FTSE All-World. We have selected what we believe to be the most important criteria for global equity ETFs:

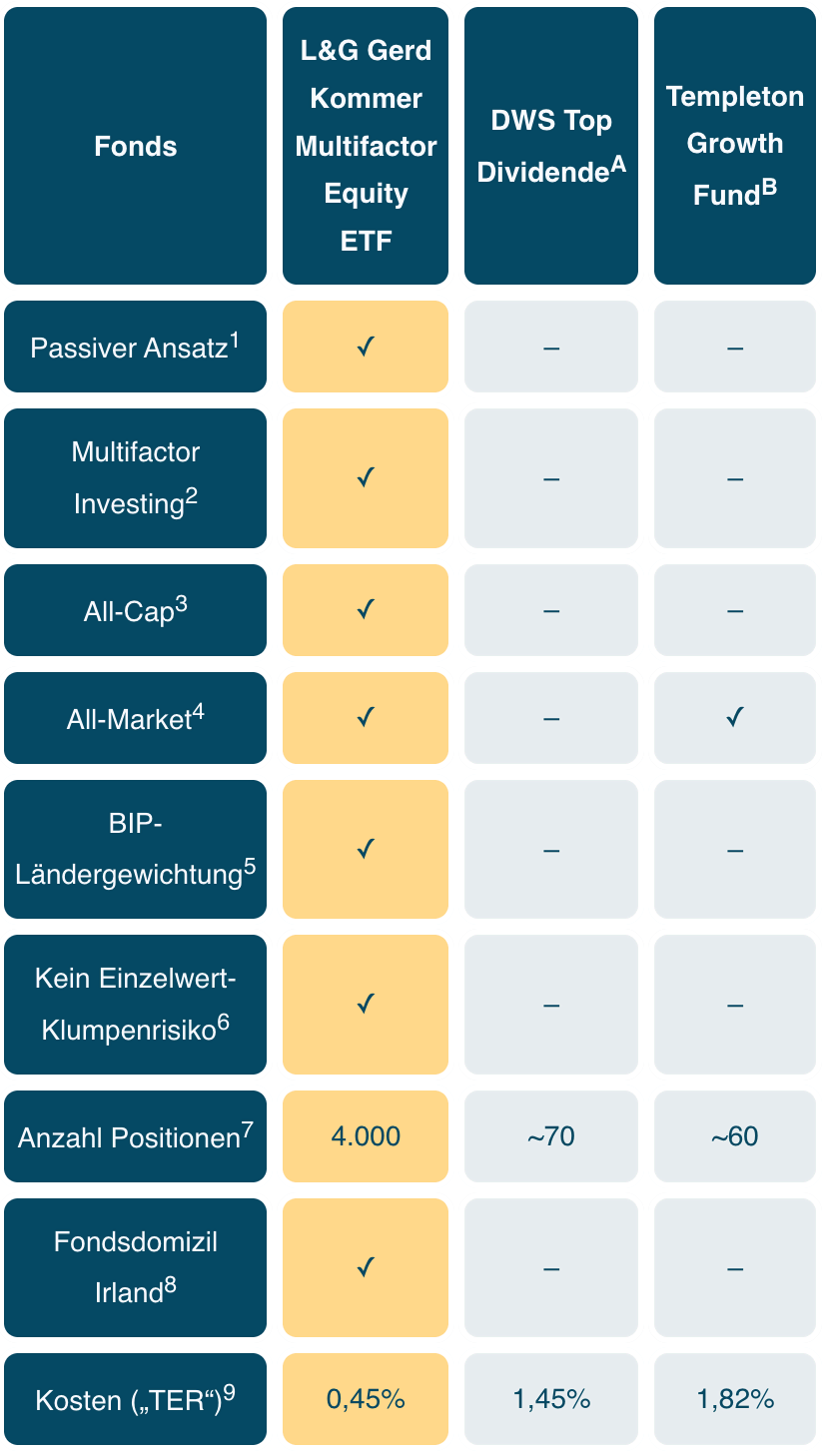

The L&G Gerd Kommer Multifactor Equity UCITS ETF follows an integrated multifactor approach and takes into account the following factor premiums: Size, Value, Quality, Investment and Momentum. One of the motivations for developing the Gerd Kommer ETF was that most other multifactor ETFs on the market suffer from different “diseases” and deficiencies, such as a low level of diversification, which can lead to concentration risks, or the incomplete representation of factor premiums (e.g. not taking small caps into account).

When constructing our index, we made sure to eliminate these deficiencies as much as possible and pursued the goal of an “integrated multifactor approach 2.0” with the Gerd Kommer ETF. In addition to built-in ultra-diversification for concentrated risk-free investing, the ETF also offers coverage of the entire market (“all-cap” and “all-market”) and a rules-based, passive investment approach.

In the following table we have compared the Gerd Kommer ETF and, in our opinion, the multifactor ETFs on the German market that are most comparable to it. This ETF comparison highlights the differences in detail:

The L&G Gerd Kommer Multifactor Equity UCITS ETF pursues a so-called passive Investment approach because a large number of scientific studies have proven for decades that active investing does not work reliably. Stock selection in the Gerd Kommer ETF is therefore carried out exclusively on the basis of mechanical, scientifically derived rules that were carefully defined as part of the index construction. An important ETF fund comparison is therefore with actively managed funds.

In contrast to passive index funds, active investment funds attempt to outperform the market through targeted selection of securities - but this often involves higher fees and is rarely successful. If you would like to find out more about the possible disadvantages of active investing, we recommend our blog post “Ten reasons why active investing works poorly”.

Since we do not shy away from comparison with our competitors on the active side of investing, in the following table we have compared some of the key figures of the Gerd Kommer ETF with those of the largest and, in our opinion, best-known active funds in Germany, which are often sold through a bank.

The Gerd Kommer ETF is suitable for investors who global risky portfolio share want to cover with a single, scientifically structured ETF.

He is for both return-oriented investors with a 100% equity allocation as well as for Investors with more conservative allocationswho want to specifically supplement the share share with low-risk components such as bond ETFs or overnight money. This means that the ETF can be flexibly integrated into different investment strategies.

Passive ETFs often perform well over the long term better results as active funds because they are significantly lower costs cause and no forecast errors through active management. Active funds (like DWS Top Dividende or Templeton Growth) often have ongoing costs (TER) of 1.45% to 2.00%, while the Gerd Kommer ETF is 0.45%.

In addition, numerous scientific studies show that active stock picking based on costs rarely beats the market in the long term. A rule-based, A passive approach is therefore the more efficient solution for most investors.

The Gerd Kommer ETF offers a clear broader diversification than classic world ETFs. He invests as All-cap and all-market ETF in industrialized and emerging countries and covers around 99% of the global stock market away.

In addition, he uses several scientifically proven ones Return factors and limited Cluster risks through a 1% capping of individual stocks as well as a combined weighting Market capitalization and gross domestic product. In particular, this reduces the strong overweighting of individual countries and mega-caps.

In the Gerd Kommer ETF, overweightings of individual heavyweight stocks are achieved through a consistent approach 1 percent cap avoided. The weight of each individual share is limited to a maximum of 1% of the index. In classic world ETFs, however, individual large companies often achieve weights of 3-4% or more.

Compliance with this upper limit is ensured by a Rules-based, quarterly rebalancing ensured. If the weight of a share rises above the 1 percent limit as a result of price gains, it is reduced again as part of the index adjustment. In this way, the portfolio remains broadly diversified over the long term, cluster risks are systematically limited and true ultra-diversification is achieved.