From Daniel Chancellor and Jakob Riemensperger

What exactly is a “world portfolio”? Anyone in German-speaking countries passive investing busy, sooner or later you will come across the term “world portfolio”, which Dr. Gerd Kommer introduced it a good 20 years ago. But what does that actually mean? What does a global portfolio actually look like? And do you need one too? You can find answers to these questions here in this blog post.

Before we get started, let's first talk about terminology: The world portfolio is not a single, specific portfolio made up of specific ETFs or indices, but rather a portfolio concept with which every investor can build an individual world portfolio tailored to their personal needs and preferences.

In this blog post you will find out what the most important construction principles are and how to implement them in practice.

(1) The four scientific pioneers behind the world portfolio concept

The key scientific findings from which the world portfolio concept is derived come from four American economists, all of whom won the Nobel Prize in Economics for their groundbreaking contributions to financial economics or macroeconomics (at different times):

- James Tobin (1918-2002). He formulated the “Tobin separation theorem”. It states that “optimal portfolios” are made up of only two basic components, a “risk-free” (low-risk) part and a risky portfolio part.

- Harry Markowitz (1927 – 2023). He showed for the first time how to construct an “optimal portfolio” of individual assets that represents the mathematically best possible combination of return and risk.

- William Sharpe (born 1934). His research results in the distinction between “systematic” and “unsystematic” (or “idiosyncratic”) risks. Idiosyncratic risks can be “diversified away” and are therefore not statistically compensated by the capital market with additional returns. Only systematic risks cannot be diversified away. That's why, as an investor, you can only statistically expect return compensation from the market for systematic risks and that's why you should only have these risks in your portfolio.

- Eugene Fama (born 1939): The market efficiency hypothesis, which states that in the stock market and certain other financial markets, because of their "information efficiency," it is probably impossible to provide a passive benchmark of cost and risk using publicly available information alone systematically (not just by chance). Fama was also a pioneer of factor investing (see Section 9 below).

In order to benefit from the findings of these four economic superstars and other top researchers as a private investor, you do not have to understand the mathematically and statistically complex elements of the so-called modern portfolio theory in detail. It is enough to know the central conceptual conclusions. This blog post aims to help with that.

(2) The world portfolio of Dr. Gerd Kommer – a short definition

The World Portfolio is the implementation of the above and other research results into a “complete”, “fully integrated” investment concept that

- completely normal private investors (as opposed to institutional investors)

- in do-it-yourself mode

- with investment products available in the retail market

- at low cost

- with investment amounts of any size, small or large

- with little time expenditure

- for the purposes of long-term wealth creation or the preservation of existing assets

can practice.

This sketchy summary already shows that the world portfolio concept can be implemented realistically and permanently (for a lifetime) for normal private investor households. To be a global portfolio investor, you don't have to be a stock market freak who spends ten or more hours on financial topics every week.

The portfolio should be integrated and adapted holistically, as science recommends, to the income and asset situation of a private investor household - throughout an entire adult life with all its changes and also during existential life crises.

Kommer first named and described the world portfolio concept in 2001 in his book “Investing worldwide with funds. A year later, in 2002, the first edition of his later bestseller “Invest confidently with index funds and ETFs”. The book initially sat on bookstore shelves like bricks. However, with the onset of the Great Financial Crisis in mid-2007, sales of the book began to increase. In 2016, the book won the German Financial Book Prize from Deutsche Börse AG and Citibank.

To date, around 300,000 copies have been sold Invest confidently and simplified, shorter versions of it are sold. In the editions of the book, which are revised approximately every four years, as well as in the monthly blog that has existed since 2017, Kommer has continually updated the world portfolio concept in an evolutionary manner and has addressed special aspects. A completely revised seventh edition of the book Invest confidently with index funds and ETFs will be published in January 2025.

In Invest confidently The world portfolio concept is derived and described from science. Here we have summarized a short world portfolio definition with the most important key aspects:

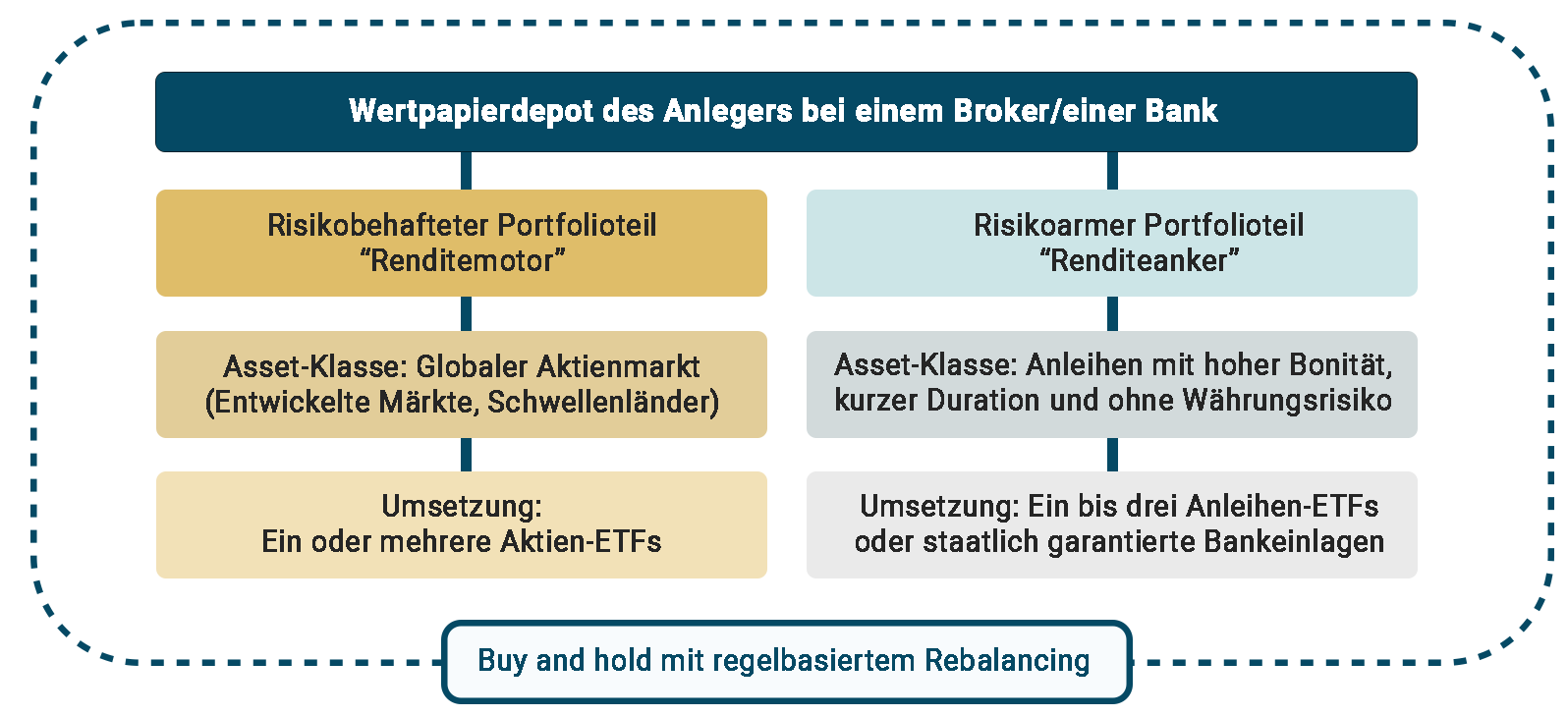

The term global portfolio stands for an investor portfolio that consists of two main conceptual components: a “risky” portfolio part, which is responsible for generating returns in the overall portfolio (the “return engine”), and a “low-risk” portfolio part, which primarily serves as a stability and security anchor in the overall portfolio. Both parts of the portfolio are highly liquid. Other core aspects and features include: (a) maximum global diversification and elimination of all individual asset and default risks, (b) disciplined, consistent buy-and-hold, supplemented by rules-based rebalancing to reduce return damage and opportunity costs (lost profits) from timing as well as the effective tax burden, (c) reducing costs through the use of low-cost index funds and ETFs and (d) reducing counterparty risks through e.g. B. banks, other financial service providers and financial product manufacturers to a level that can no longer be reduced.

The definition components (a) and (b) implicitly contain the important avoidance of active, forecast-based investing, as this produces unattractive return-risk combinations from a scientific perspective. Active investing in capital market investments takes place through security selection or market timing or a mixture of both. Active investing in its infinite number of individual forms “is what everyone does.” It has a global market share of over 95%.

In the remainder of this blog post, we will address the requirements for a real world portfolio according to Gerd Kommer and use specific products and solutions to show what such a portfolio could look like in its simplest form.

(3) The division into a risky and a low-risk part of the portfolio (“Level 1 asset allocation”)

From a bird's eye view, the world portfolio can be divided into a risky ("RBT") and a "risk-free" (low-risk) portfolio part ("RFT"). The RBT is as Profit engine responsible for generating the portfolio return; the RFT serves as a “security or stability anchor” in the portfolio. We call this dichotomy Level 1 asset allocation.

As far as the split between RBT and RFT is concerned, all combinations from 100% RBT/0% RFT (“100/0 portfolio”) to 0% RBT/100% RFT (“0/100 portfolio”) are conceivable. A 100/0 world portfolio has the highest expected return, but will also fluctuate significantly (be volatile) over time. A 0/100 portfolio, on the other hand, has the lowest expected return, but on the other hand it hardly fluctuates over time. In practice, for the vast majority of retail investors, the music is somewhere in between, as few will prefer the rand allocations.

In a simple version of the world portfolio, the RBT consists of one or more index funds/ETFs that track the global stock market. The investment class (asset class) stocks is the asset class with the highest long-term return, higher than the corresponding average returns of real estate, bonds, raw materials, precious metals or collector's items or financial products derived from or related to these asset classes, such as. B. interest-bearing bank deposits, capital-forming life insurance or hedge funds. (Private equity investments have statistically similar returns to stocks, but are riskier and more illiquid - see here and here.)

The RFT is not expected to contribute a significant long-term average return after costs, taxes and inflation, as such an expectation would be at the expense of the core function Stability anchor would go. In the past, and in the future, significant positive real returns after costs and taxes can only be achieved in the long term by bearing risk.

The RFT consists of highly liquid government and corporate bonds with (a) short remaining maturity (and therefore little interest rate risk), (b) low credit risk (and therefore default risk that can hardly be reduced) and (c) no exchange rate risk. (If you would like to read more about interest rate risk, see our blog posts “Bonds and interest rate changes – a case study" and "The interest rate risk on bonds“referred.)

For RFT investment volumes of up to 100,000 euros, you could also use a daily deposit at a bank, as this amount per bank-customer combination in the EU is within the statutory (state) deposit insurance.

(4) Freedom of forecasting and maximum global diversification

An essential advantage of the world portfolio concept is that - unlike active investment strategies or actively managed financial products - it does not require any forecasts, i.e. no forecasts of security prices, economic variables (e.g. interest rates, inflation, economic growth) or other developments in society, politics and the economy that influence the stock market.

We know from science that making economically exploitable forecasts on the capital market is generally not successful. The harm from following the majority of incorrect forecasts outweighs the benefit from following the minority of correct forecasts.

Investing predictions are ultimately bets on one or more of the following investment aspects:

- individual stocks (stock picking);

- individual countries, industries or topics;

- individual fund managers or “gurus”;

- individual time periods (market timing);

- economic or interest rate developments; or

- the monetary policy of central banks

If you would like to find out more about why such bets usually don't work out, you can do so in our blog post "Ten reasons why active investing works poorly“ read up.

In short: Such bets represent bad risks because they are avoidable (“diversifiable away”) and are not worth taking due to the lack of expected compensation (in the form of an expected return). Conversely, it is advisable to avoid any kind of forecast, especially when it comes to important things such as retirement planning. This can be done by clicking on the entire market economy, i.e. maximally globally diversified and buy-and-hold. This can be easily implemented with regard to stocks by purchasing a suitable index fund/ETF that tracks the global stock market.

(5) Buy and Hold & Rebalancing

Buy-and-hold (B&H) is just as important a basic principle in the world portfolio concept as freedom of forecasts and global diversification. B&H (a) reduces labor and costs (particularly by minimizing the costs of buying and selling), (b) reduces the effective tax burden in a tax system such as the German one (see here) and (c) eliminates the potential return damage from poor, emotion-driven timing decisions. These are particularly likely among private investors, as behavioral finance research (behavioral economics) and empirical financial market research have often shown.

In the world portfolio concept, B&H is linked to rebalancing. Rebalancing is the rule-based restoration of the desired percentage weightings (target or target weightings) of all positions in a portfolio over time after they have “developed away” from the previously consciously chosen target structure due to market effects. In practice, this “development” will inevitably occur sooner or later and does not contradict the buy-and-hold idea. The reason for this is that without rebalancing, the composition and the associated risk-return combination of a portfolio would change over time due to market fluctuations and move away from the actual investor preferences. Rebalancing is also a special form of countercyclical (“contrarian”) investing based on the sell-high/buy-low principle. If you would like to learn more about rebalancing, check out our blog post “Rebalancing: advantages, methods, principles“referred to.

(6) Reduction of costs

All other things being equal, costs reduce the net return on an investment, i.e. the return that really matters. Costs act like a negative compound interest effect.

Here is a calculation example: With a starting capital of 5,000 euros, an average annual return of 10% and costs of 0.5% per year, the final asset value after 30 years is a good 76,000 euros. However, if the annual costs had been 1.0%, the final asset value would only be around 66,000 euros - 10,000 euros or almost 15% less.

Because costs are one of the few influencing factors when investing about which you can have a high degree of certainty and If you have control, it is particularly worthwhile to actually exercise this control.

Furthermore, the old general rule “higher quality also costs more” does not apply when investing. Rather, the opposite is the case: some of the most expensive investments, such as hedge funds, closed funds or capital-forming life insurance, are also the lowest-yielding.

(7) Elimination of procedural and financial product-related counterparty risks

A sometimes overlooked part of the world portfolio concept is the consistent avoidance of procedural and financial product-related counterparty risks that accompany most forms of active investing. What do we mean by that?

Many financial products, e.g. Some investments, such as endowment life insurance, private pension insurance, certificates, many private equity investments, hedge fund investments, investments in closed-end funds, investments on some crypto exchanges and investments in P-to-P loans, are associated with (typically overlooked) counterparty risks. In other words, if the relevant counterparty runs into economic difficulties or even goes bankrupt, then some or all of the investor's money may be lost. This also applies to bank balances above the state deposit protection limit of 100,000 euros per bank-customer combination.

With the world portfolio concept, such counterparty risks generally do not exist because (a) index funds/ETFs - unlike the financial products mentioned above - are legally so-called Special assets and (b) the bank only acts as a depositary in the case of a bank deposit, not as a debtor as in the case of a bank deposit.

(8) A simple graphical representation of the world portfolio concept

The following overview shows a simple graphical illustration of the general basic structure of a world portfolio.

(9) Optional: The world portfolio in the factor investing variant

As an optional add-on worth considering, so-called factor premiums can be taken into account when constructing a world portfolio. Factor premiums are characteristics of securities that can be used to increase the expected return (i.e. the statistical average return) of a portfolio compared to the overall market. Over the last 100 years or so, factor investing (using two or more factor premiums) would have generated a return that was significantly more than one percentage point annually higher than that of the “normal” stock market (the overall market) - with a similar risk in terms of volatility (return fluctuations).

The best known factor premiums are:

- the small size premium: Small companies, based on their market capitalization, tend to make better returns than large ones.

- the value premium: Cheaply valued companies (e.g. measured by key figures such as the P/E ratio) tend to return better than highly valued (“expensive”) companies.

- the quality bonus: Companies with low debt and high profitability (e.g. operating profit margin) perform better on average over the long term than companies at the other end of the spectrum (low quality companies).

- the momentum premium: Stocks that have had significantly above-average returns over the last twelve months will tend to continue to do so for another three to six months before falling back to average or below.

- the low investment premium (also called low asset growth premium): Companies that have had below-average (“frugal”) total assets growth in the recent past tend to generate higher stock returns than companies with high total assets growth (“wasteful” companies).

Factor premiums become more apparent the longer the observation period or the investment period. To illustrate: Over a super-short observation period of one day, the stock market statistically has a return above zero in 53% of all cases (days). If the observation period is extended to ten years, the “proportion of returns above zero” indicator increases to 93%. A similar rule also applies to the excess returns from factor premiums.

You can read more about factor investing in this blog post.

(10) Possible world portfolio solutions

(a) For investors who want to invest on their own initiative (in do-it-yourself mode):

In the simplest case, a global portfolio can be implemented with an ETF for the risky part of the portfolio and one for the low-risk part of the portfolio. For an investor who wants a 100/0 Level 1 asset allocation or wants to use overnight funds within the government deposit insurance for the RFT, an ETF alone is even possible.

In its simplest form, such a portfolio could look like this (as of July 2023):

- RBT – stocks global: L&G Gerd Kommer Multifactor Equity UCITS ETF (WKN: WELT0A) or SPDR MSCI ACWI IMI UCITS ETF (WKN: A1JJTD)

- RFT – short-term bonds with a high credit rating without exchange rate risk: L&G Corporate Bond ex-Banks Higher Ratings 0-2Y ETF (WKN: A40E7Q) and/or Xtrackers II Germany Government Bond 0-1 UCITS ETF 1C WKN: DBX0T8). As mentioned above, the low-risk part of the portfolio can alternatively be represented via a current account at a bank, as long as the corresponding daily investment amount is within the state deposit insurance of 100,000 euros per customer-bank combination.

| Important disclaimer: These are expressly not investment recommendations, but simply an illustration of how to easily implement the world portfolio concept could. The RFT is not “risk-free” in the literal sense. Please do your own research and read all product documentation before making an investment decision. |

(b) For investors who do not want to invest on their own but would like to receive support:

— From an initial minimum investment amount of 20 euros with internet-based advice: The Robo advisor strategy by Gerd Kommer. Here you are taken by the hand: You don't have to choose individual ETFs, the Robo suggests the Level 1 asset allocation based on the customer's information and determines the Level 2 asset allocation (the product implementation of the Level 1 asset allocation) for you, takes care of opening the portfolio, buying (and if necessary selling) ETFs, rebalancing and reporting, including the annual creation of a tax certificate. Savings plans and withdrawal plans as well as subsequent investments and withdrawals can be triggered at the push of a button. There is an app for smartphones. Customer support is available as a contact person. The Robo Advisor strategy invests according to the world portfolio concept.

— From a minimum investment amount of one million euros: The Gerd Kommer Invest (“GKI”): Holistic initial and ongoing financial advice and asset management for wealthy private households. Asset protection concepts and succession planning via foundation solutions are also part of the scope of services.

Conclusion

The world portfolio is a scientifically derived, fully integrated investment approach with which private investors can make capital market-based, long-term investments for the purposes of wealth creation and wealth preservation.

The world portfolio concept can be implemented on your own or through delegated investing. Gerd Kommer's advice books, his monthly blog, which has existed since 2017, his YouTube channel and other publications of his, which are linked in Gerd Kommer's monthly newsletter, help with this.

For those who cannot or do not want to implement the world portfolio concept on their own, we have shown some alternatives in this blog post.

Further information on the world portfolio concept

Guide books:

Kommer, Gerd (2024): “Invest confidently with index funds and ETFs. How private investors win the game against the financial industry”; Campus Verlag, 7th edition, 2024 (first edition 2002); 552 pages - a completely revised new edition will appear in January 2024.

Kommer, Gerd (2025): “The easy entry into the world of ETFs: A starter book for financial beginners that is easy to prepare”; financial book publisher; 2nd edition 2022, 176 pages - a very simple beginner's book (does not require any prior knowledge of the stock market)

Kommer, Gerd (2024): “Investing confidently for beginners: How you can build wealth with ETFs”; Campus Verlag, 3rd edition, 2018; 272 pages - a beginner's book for readers who already have basic knowledge of the stock market

Kommer, Gerd (2021). “Buy or Rent – How to make the right decision for yourself”; Campus Verlag, 3rd edition, 2021; 280 pages

Blog posts:

Kommer, Gerd; Schweizer, Jonas (2021): “Rebalancing: Advantages, Methods, Principles”; blog post; December 2021; Link: https://gerd-kommer.de/blog/rebalancing/

Kommer, Gerd; Schweizer, Jonas (2021): “Saving taxes through buy-and-hold”; blog post; October 2021; Link: https://gerd-kommer.de/blog/steuer-sparen-buy-and-hold/

Kommer, Gerd; Weis, Alexander (2019): “The interest rate risk in bonds”; blog post; December 2019; Link: https://gerd-kommer.de/blog/zinsaenderungsrisk/

Kommer, Gerd; Weis, Alexander (2019): “Factor Investing – the Basics”; blog post; May 2019; Link: https://gerd-kommer.de/blog/factor-investing-die-basics/

Kommer, Gerd; Weis, Alexander (2020): “The Pains of Factor Investing”; blog post; May 2020; Link: https://www.gerd-kommer.de/blog/pains-of-factor-investing/

Kommer, Gerd; Weis, Alexander (2020): “Ten reasons why active investing works poorly”; blog post; February 2020; Link: https://gerd-kommer.de/blog/warum-aktives-investieren-bad-funktioniert/

Weis, Alexander; Gschichtmann, Selina (2022): “Passive investing – the basics”; blog post; September 2022; Link: https://gerd-kommer.de/blog/passiv-investieren-die-basics/

Weis, Alexander; Kanzler, Daniel (2022): “Bonds and interest rate changes – a case study”; blog post; June 2022; Link: https://gerd-kommer.de/blog/anleihen-und-zinsaenderungen/

Weis, Alexander; Kommer, Gerd (2019): “Timing the market entry – does it work?”; blog post; March 2019; Link: https://gerd-kommer.de/blog/timing-des-markteinstiegs/

Kommer, Gerd; Kanzler, Daniel (2022): “Leveraging stock investments with credit – does it work?”; Nov 2022; Link: https://gerd-kommer.de/blog/leverage-effekt/