From Gerd Kommer and Maximilian Bartosch

In this blog post we look at a specific old wives' tale about the financial attractiveness of owner-occupied residential properties, which has been re-proclaimed "twice a year" by most media in Germany and by the real estate industry for decades with headlines such as the following:

- „Property owners have significantly more money in old age than tenants“ – Headline of an article in the news magazine Spiegel from January 13th, 2025

- „Pensioners who own their own home are particularly wealthy“ – Headline of an article on the news portal t-online.de from December 17th, 2025

- „Homeowners accumulate more wealth than renters“ –Press release from the Association of Private Building Societies in 2025.

However, the statement “own-occupied home leads to higher wealth in old age than renting” is not far from the truth. The statement is a picture-perfect case of “lying with statistics.” [1]

Lying by concealing essential information

As we know, you can lie in many ways. One of them is that person A (the liar) formulates a statement B correctly, but deliberately omits essential information in order to cause a false understanding or error on the part of addressee C. So A lures C into a comprehension trap by omitting crucial information from statement B. That is the lie. Children can already master this method. In English it has a nice compact name Context Dropping used.

Context dropping – lying by deliberately omitting, i.e. suppressing crucial additional information – happens when the statement “Pensioner with his own home [2] are statistically wealthier than pensioners who rent.”

Below we show how this deception actually works. The claim that home ownership is among older households causal for a higher net worth (as conveyed in the exemplary publications cited at the beginning through manipulative context dropping), we will henceforth call “the real estate lie”. [3]

At first glance - without the correct context - the real estate lie in question appears to be true: homeowners actually have a statistically higher net worth in old age than renter households. This is shown by the relevant data and no one doubts its formal correctness.

But the crux of the matter: the statistical wealth advantage of homeowner households (EHBs) over renter households has nothing to do with owning their own home. It is entirely due to other causes. So here correlation is confused or swapped with causation. Yes, EHB households are generally wealthier as they get older than renter households, but they Caused This asset advantage is not the home.

Here is an illustration of the manipulative swapping of cause and effect Real estate lie: The wealth of the average Ferrari-owning household in Germany (around 14,500 households) naturally exceeds that of the average non-Ferrari-owning household (around 41 million). Now the question: Was the Ferrari the cause of this wealth advantage? Of course not. The Ferrari has statistically reduced this wealth advantage - without it, the wealth advantage of the Ferrari households would be even greater. Either way, Ferrari ownership was the result of the income and wealth advantage, not its cause. It's the same with home ownership. It is the consequence, not the cause, of a number of actual causal factors.

The real causes of homeowners' wealth advantage

The “real estate propagandists” are betting that their recipients will fall for the manipulated statement and misunderstand correlation as causality.

However, as scientific research shows quite clearly, the actual causes of the wealth advantage of EHB households are as follows: [4]

1) EHB households have a higher lifetime income, i.e. h. the sum of their net income over the entire period of earning capacity is statistically higher than for renter households. The proportion of households with two incomes is higher among EHB households than among renter households.

2) EHB households have a higher percentage propensity to save. A higher percentage of their net income, which is already higher in absolute terms (see number 1), goes into wealth creation than is the case with renter households. This higher propensity to save is also expressed in the willingness to submit to a “positive compulsory savings contract” that is linked to the loan-financed purchase of a home. More on that below.

3) EHBs are more risk-averse in their investment behavior and therefore achieve statistically higher long-term returns in their wealth creation away from their own home. This increased willingness to take risks is also reflected in the higher entrepreneurial rate among EHB households than among renter households (starting a business and entrepreneurship are very risky). The higher risk affinity is probably due, among other things, to the proven higher average financial literacy of EHB households.

4) EHBs receive more frequent, larger and earlier wealth transfers from their parents and grandparents through gifts and inheritances. This often happens by “subsidizing” the equity share when the EHB household first purchases property when it is young.

5) EHB households have lower divorce rates than renter households. Divorces often cause serious financial losses for those involved. We show why and how these asset losses happen here.

6) If a home investment fails individually - for example due to a combination of unemployment and excessive debt - the affected households often lose their home through seizure or forced sale and become renter households again. Paradoxically, particularly poor home investments contribute to the “home ownership lie” analyzed here.

Note that in the list and description of the six main causes of the higher wealth of EHB households, we did not say anything about Why These households have higher incomes, higher savings rates, greater willingness to take risks, higher financial literacy or lower divorce rates. Quite obviously, a large part of these wealth-promoting factors lies in the socialization of the people concerned; a small part could also be genetically determined.

Would you compare tenant groups with EHB groups where the six causes listed above no If there were a difference, it would be shown that renters statistically achieve higher or similar levels of wealth in retirement. [5]

Why higher wealth? Quite simply because renting in conjunction with other forms of wealth creation - above all with a simple, broadly diversified stock portfolio on a buy-and-hold basis - leads to a higher net final wealth than an owner-occupied property in the majority of time frames if the financial-mathematically correct comparison is made. Furthermore: The relative final asset advantage of the “rent + capital market investment” constellation will tend to be greater, the higher the loan share (“leverage”) is in the comparison EHB. We at GKI have shown this for Germany and others for other countries - see here and here.

We probably don't need to explain in detail at this point why the real estate lie has been spread again and again by real estate agents, property developers, real estate influencers and banks for decades. These parties earn directly or indirectly from real estate purchases or their financing.

The “compulsory savings contract” for real estate

In connection with the correlation phenomenon of the higher net wealth of EHB households in old age relative to renters, it is often even said that not People with conflicts of interest, i.e. “people without a real estate agenda”, argue that the higher net assets of EHB households are based to a large extent on the phenomenon of the “positive compulsory savings contract”. This means that an EHB household that, for example, has taken out a loan for 80% of the acquisition costs is obliged to pay the corresponding expenses (loan installments, property tax, insurance, maintenance) month after month until it has been completely repaid - typically after 25 years or more. Otherwise there is a risk that the property will be seized by the bank. Above all, the repayment element in debt service contributes directly to wealth creation: with every euro of repayment, the percentage of equity in the property increases.

A tenant household is not under a comparable pressure to save, according to the theory of the positive compulsory savings contract. As a result, tenant households will often save less overall or temporarily interrupt their savings over a 25-year period for consumption purposes.

Here too, the confusion/swapping of correlation and causality probably plays a role. People with a naturally high tendency to save are represented more frequently among EHB households than among renter households. This is probably because their pre-existing strong willingness/inclination to save makes it easier for them to accept the long-term reduction in consumption that comes with the “compulsory home savings contract”. These EHB households would not have been able to purchase their own home for certain reasons [6] or if they had viewed a home as a comparatively unattractive investment, the majority of them would have been just as disciplined and saved for the long term in other asset classes. So if you look behind the façade of formalities, you can't even speak of "compulsion" for most people or households who submit to the supposed "compulsory" savings contract, because they would save even without real estate.

What does the development of the “homeownership ratio” tell us?

If you realize that in almost all countries in the world and especially in Germany, wealth creation through owner-occupied residential real estate is financially supported by the state more strongly through taxation and transfer payments (cash benefits) than any other form of private wealth creation, and if you assume for a moment - incorrectly - that owner-occupied real estate systematically produces high returns on equity, then the homeownership ratio (HOR) in most countries would have to continue to rise over time. [7]

But that is not the case. In the USA, the HOR is now at 65%, the same level as 30 years ago, although every American president during this time announced during the election campaign that his administration would increase the HOR. The HOR average of the 38 OECD countries has essentially moved sideways over the last 20 years. [8] There has also been stagnation in Germany over the last decade (current level 47%). Before that, the HOR had risen moderately - probably due to the special and one-off effect of reunification in conjunction with significantly falling interest rates at the time - since in the eastern federal states the HOR was only 24% before reunification (today around 33%).

Wealthy Switzerland is probably the only economically developed country in which, compared to other forms of private wealth creation, home ownership has not yet been systematically favored or subsidized by the state - neither through taxes nor in any other way. [9] The HOR there is only around 40% - probably the lowest value globally. This is a strong indicator that the “natural” HOR in a rich country with a functioning, deep, liquid rental market and a high level of tenant protection (as is common in Western Europe) is in the 40% to 60% range, but certainly not 80% or higher - where politicians and the real estate industry would like the HOR to be.

In this context, many politicians and of course the entire real estate industry have been claiming for decades that a high HOR is a sign of national prosperity. This is also the view of most citizens. Nevertheless, this idea is probably wrong. Empirically, poor countries have higher HORs than rich countries, with rare exceptions. Romania and Bulgaria are among the poorest states in the EU, but have HORs of 86% and 95%, well above the level of the other, richer European states. In general, poor developing countries worldwide are more likely to have higher HORs than rich industrialized countries. One of the richest countries in the world, Switzerland, has – as mentioned – the lowest HOR globally. [10]

Trying to increase the HOR through state measures “with all financial force” is therefore likely to be – as in most countries over the last 25 years – a waste of taxpayers’ money, which is also economically detrimental to tenant households, and is therefore socially regressive and tends to increase wealth inequality.

The future development of residential property prices in Germany

How will residential property prices develop in the future?

In order to answer this question, one should first look at their development in the long-term past. In the 55 years from 1970 to the end of 2024, residential property prices in Germany rose by a paltry 0.1% p.a., adjusted for inflation. Yes, in the eleven and a half years from mid-2010 to the beginning of 2022, prices had risen sharply, but in the approximately 40 years before that and in the three and a half years since March/April 2022, the increases in value, adjusted for inflation, looked poor - even in the largest cities of Berlin, Hamburg, Munich and Cologne. Since spring 2022, residential property prices in Germany, adjusted for inflation, have fallen from their peak at the time by 26% (Greix index) by September 2025 and by 17% (Europe index) by December 2025 - the most recent figures available. [11] (We show the long-term historical price development in Germany and twelve other western countries since 1970 here.)

We already know with great certainty that the population in Germany will begin to shrink from around 2030. Slowly at the beginning, then faster and faster. This means that a demographic headwind that will continue to affect the development of residential property prices for decades will continue. This demographic “price suppression effect” is further intensified by the fact that those who leave the real estate market due to death occupy particularly large areas per person at this time due to their age and wealth. So we will not only have a decline in population and a resulting dampening effect on demand, but - in addition to the net new construction - an indirect increase in the supply of space, since the owners and tenants who leave the real estate market occupy far larger areas per person than the young people who enter the real estate market after moving out of their parents' house. This increases the supply of space relative to demand.

It is possible that real estate prices in Germany, which have fallen since 2022, are already the front end of this demographic supply and demand effect. Asset markets generally already price in the developments expected for the future in the present.

Another long-term effect on increasing the supply of living space, although its strength is difficult to estimate, could result from the conversion of vacant office space into residential space. (It is also conceivable that in the next few years an AI-related loss of administrative jobs will lead to a second wave of reductions in the need for office space after Corona.)

Government actions to combat climate change will also tend to have a detrimental impact on housing prices and returns in the future. At least that's what Allianz writes in Allianz Global Wealth Report 2024. [12] We consider this assessment to be plausible.

Conclusion

There are many over-optimistic myths circulating about the financial attractiveness of residential real estate as an investment class that do not stand up to a rational comparison with reality - e.g. B. Research results from independent scientists and empirical value increase data from the last 30 to 50 years.

One of these myths is “property owners have more wealth than renters when they get older.” Anyone who formulates this statement “without context” in such a way that the recipient of the statement will probably conclude that real estate ownership has produced this wealth advantage is lying.

Although EHB households are wealthier on average than renter households, the reasons for this wealth advantage are other than the property: (a) higher long-term incomes, (b) higher propensity to save, (c) more risk-taking investments, (d) more wealth inflows via gifts/inheritances (e) fewer divorces.

If the EHB households in question had not invested in an owner-occupied property, but would have remained renters and - without spending a cent more (but not less) on housing and building wealth - they would have invested in more profitable forms of investment such as. For example, if global equity ETFs were invested, they would be invested on a fixed date, e.g. B. the age of 60, was even wealthier.

How beautiful the world would be if everyone who professionally deals with investments for others pursued the goal of spreading as little disinformation as possible in their communication and marketing, including no disinformation through context dropping.

Endnotes

[1] There are numerous books about how this works in general. One of them is “How to lie with statistics” by Prof. Walter Krämer (Amazon link here).

[2] In this blog post, “home” means any type of owner-occupied residential property, including both houses and apartments.

[3] Net worth = Gross worth (total of all assets) minus liabilities.

[4] At the end of this blog post we mention some of these academic studies.

[5] Such studies that neutralize all six causal factors in the study design may not yet exist. They would be very complex and expensive.

[6] For example, because for professional reasons they (have to) live in a place where they do not want to live permanently.

[7] At the end of this blog post in the appendix we show in Table 1 the tax preference for wealth creation through home ownership relative to wealth creation through e.g. B. Shares by the German state.

[8] The OECD is a supranational organization of which, by and large, the 38 wealthiest countries in the world are members. The main task of the OECD is to reach agreement on national tax and economic policies between member states.

[9] The abolition of the so-called Imputed rental value taxation In Switzerland from probably 2028 onwards, this will also lead to state subsidies for wealth creation through one's own home in relation to other forms of wealth creation. For information on imputed rental value taxation, see the keyword “imputed rental value” in the German-language Wikipedia.

[10] Of course, almost all Swiss residential properties still belong to Swiss citizens or Swiss companies (which in turn belong to Swiss citizens), but around 60% do not belong to the households that live there.

[11] It is normal that different property price indices sometimes differ greatly from one another over short periods of time.

[12] "The long-term impact of climate change on housing prices comes mainly through transition risk i.e. the energy consumption of buildings, particularly for heating. Projections of the House Price Index (HPI) in the UK under different climate scenarios up to 2050 show declines between -9.3% and -13.1%. For Germany, cumulative HPI declines could be as high as -24.5%. This would imply per capita losses of EUR32,380. Applied to all markets under consideration, homeowners could face losses of up to EUR30 trillion.” (Allianz Global Wealth Report 2024, p. 5).

appendix

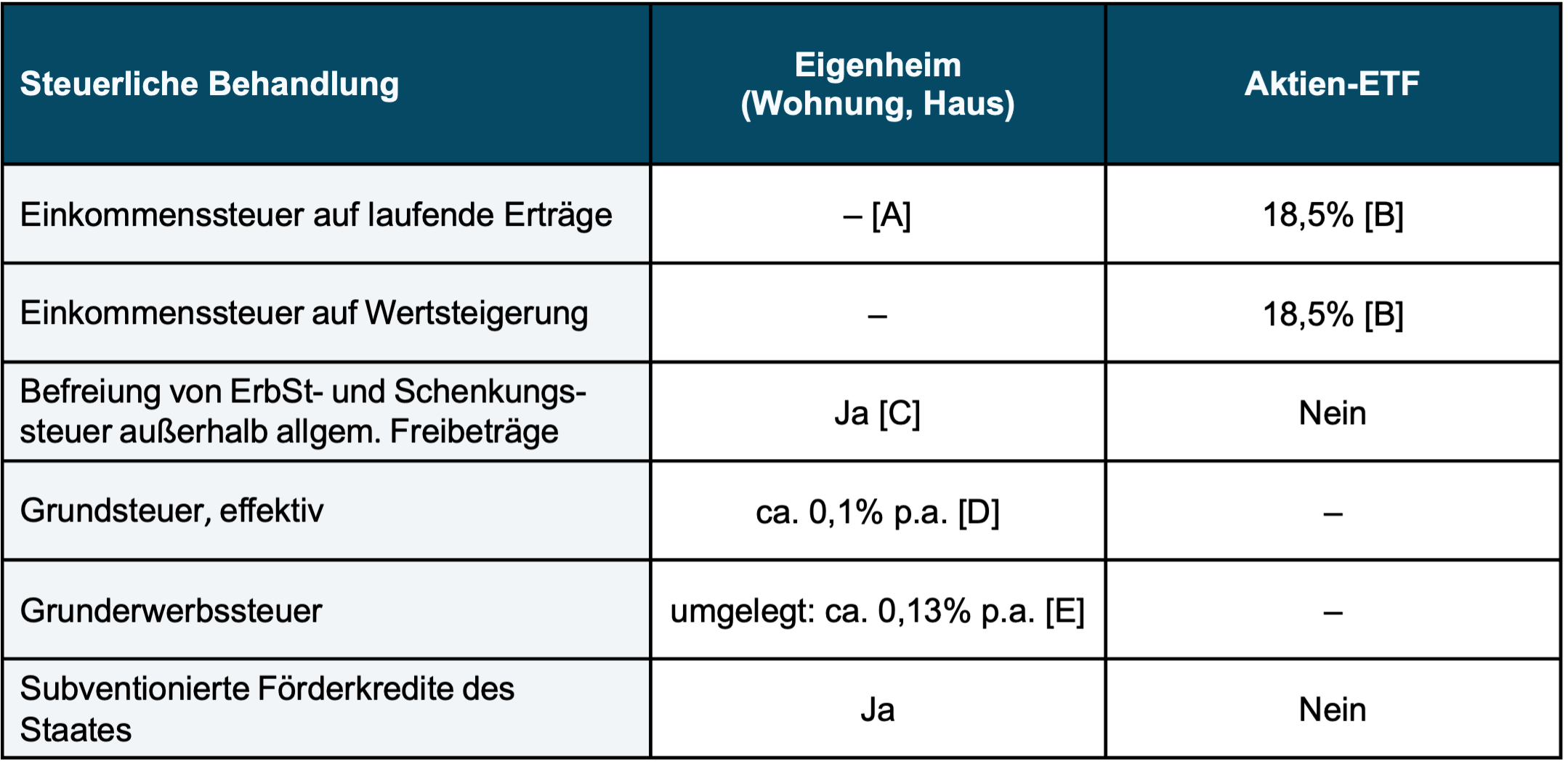

Table 1: The drastic tax incentives for homeownership in Germany compared to Building wealth with capital market investments

► Assumption: Stock ETF is part of private tax assets. ► [A] The current income from a home is the rent saved for the owner. In various countries, this “fictitious” income must be taxed by the owner. ► [B] Stock ETF: 18.5% with 30% partial exemption (70% × 26.375%). ► [C] Inheritance and gift tax exemption for the home. If children or grandchildren are the recipients, then the exemption limit is 200 sqm, for spouses there is no sqm limit. ► [D] Property tax: The effective taxation is property-specific. A rough approximation is given here as a percentage of the current value of the property. ► [E] The stated value results from a property transfer tax of e.g. B. 5% and a holding period of 40 years: 5% ÷ 40 = 0.13% p.a. ► Saver's flat rate of 1,000 euros per person per year for capital market investments is ignored here for the sake of simplicity. It also ignores overall low state subsidies for Riester savings and capital-forming benefits (VL) and the retirement provision portfolio that will exist from 2027.

Literature references

Allianz (without author): Allianz Global Wealth Report 2024; Allianz Insurance Group; Allianz Research; Internet reference here

Birkjaer, Michael et al. (2019): The GoodHome Report 2019 - What makes a happy home?"; Kingfisher plc and the Happiness Research Institute; June 4, 2019; Internet reference here

Bracke, Philippe et al. (2014): “Homeownership and Entrepreneurship: The Role of Mortgage Debt and Commitment”; Working Paper No. 5048; Ifo Institute; Internet reference here

Braun, Rainer (2024): “You build tomorrow’s empty property today”; Interview with Rainer Braun from Emprica in Der Spiegel from July 5th, 2024; Internet reference here

Dräger, Jascha et al. (2024): “The Keys to the House – How Wealth Transfers Stratify Homeownership Opportunities”; German Institute for Economic Research/DIW; October 12, 2024; Internet reference here

Fagundes, Dave (2017): “Buying Happiness”; In: William & Mary Law Review; 58, 2017; Internet reference here

Krämer, Walter (2015): “How to lie with statistics: About the risks and side effects of non-statistics”; Campus Verlag 2015 (book)

Goetzman, William/Matthew Spiegel (2000): “Policy implications of portfolio choice in underserved mortgage markets”; SSRN; 02 Nov 2000; Internet reference here

Moussouni, Oualid et al. (2023): “Does Owning a Home Build More Wealth?” Canada Housing and Mortgage Corporation/CHMC; Internet reference here

Shlay, Anne: (2006): “Low-Income Homeownership: American Dream or Delusion?” In: Urban Studies 43, No. 3, pp. 511-531; Internet reference here

Wong Bucchianeri, Grace (2011): "The American Dream or the American Delusion? The Private and External Benefits of Homeownership for Women"; July 3, 2011; SSRN; Internet reference here