From Gerd Kommer and Tobias Jerschensky

Of the 41 million households in Germany, 43% = 17.6 million own the property in which they live. 57% (23.4 million) are renters. Two thirds of renter households aim to purchase a home (an apartment or a house) in the future. If you ask homeowners aspirants about their motives for purchasing a property, financial motives are mentioned much more often than lifestyle motives, e.g. B. “good retirement provision”, “living rent-free in old age”, “good returns”, “concrete gold”, “material value”, “safe investment” and “inflation protection”.

In Gerd Kommer's book published in 2021 "Buy or rent? How to make the right decision for yourself" The financial and non-financial arguments in a buy-or-rent decision in Germany were compiled and analyzed. The purely economic part of the analysis therein is based on historical data from 1970 to 2020 (51 years). Since then, more than four years have passed, during which a lot has happened in real estate prices, interest rates, rents and capital market returns. Time to bring the financial buy-or-rent comparison in the book up to date with updated figures by the end of 2024.

Due to space limitations, we will not go into this blog post non-financial Arguments, i.e. emotional and lifestyle considerations, which - depending on the argument - speak for either buying or renting. The non-financial arguments are comprehensively covered in the book mentioned above.

Which comparison method leads to truly reliable findings?

Do you want for one? specific Purchase object and one specific Rental situation - i.e. an individual case - to carry out a buy or rent calculation looking into the future, there are numerous useful buy or rent calculators on the Internet. We list links to ten free online calculators at the end of this blog post under point 1 in the appendix. However, such a prognostic case-by-case calculation cannot be used to draw any generalizable conclusions for the purchase or rent consideration.

If you want to formulate generalizable statements about the fundamental economic attractiveness of buying versus renting combined with a simple capital market investment (an ETF portfolio on a buy-and-hold basis) beyond non-representative individual cases, individual case calculations will not help. Structural conclusions can only be reached by calculating with representative statistical data and over sufficiently long, representative periods of time.

If you do that, another basic methodological question immediately arises: Do you want to carry out the comparison on the basis of historical data or on the basis of forward-looking forecasts? Prognostic calculations are inevitably based on subjective assumptions about the future development of home prices, interest rates, rents, capital market returns and taxes. Although forward-looking assumptions for time frames beyond a few months are uncertain and will later turn out to be mostly wrong, the media and real estate finfluencers still predominantly use forecast calculations for their general buy-or-rent analyses. Here are three examples:

- “Buying is cheaper than renting in these seven cities” – Wirtschaftswoche, March 18, 2024, print article

- "Rent or buy? Which strategy is worthwhile in your region" – Handelsblatt, July 5, 2018, print article

- “Is real estate worth it in 2025?” – Finanztip, August 27, 2025, video

The use of forecasts to answer the generalThe question, which is not specific to an individual household, as to whether buying or renting + an ETF portfolio is more financially attractive seems strange when you think about it more closely. To assess the economic attractiveness of Financial market investments - stocks, interest-bearing investments, raw materials, precious metals and cryptocurrencies as well as the financial products derived from them - are practically without exception historical Data series used. So no forecasts, which are based on uncertain, subjective assumptions and will probably not come true as formulated.

Therefore, we base our buy-or-rent analysis in this blog post on this Best practices science and do not calculate on the basis of predictions and assumptions, but on the basis of historical market data. Because we use historical data, because we go back 55 years to 1970, and because we compare our results with academic studies for other countries, our calculated numbers allow fundamental, structural conclusions to be drawn.

What should you consider when making a correct buy or rent comparison?

Here are three basic principles that a reliable comparison of buying and renting + capital market investment must meet:

- Buyers and tenants + ETF investors live in an identical property.

- Buyers and tenants have identical “cash outflows” initially and every month, i.e. they invest the same amount in their wealth creation, i.e. they forgo consumption for wealth building purposes are the same. What exactly is meant by “identical cash outflows” becomes clear in Table 1 below. There, the cash outflows in lines 1 and 2 for the homeowner (EHB) and the tenant/ETF investor amount to the same amount. This equality is achieved by the tenant investing the difference between his monthly rent and the EHB's total expenses in an ETF savings plan.

- The observation period (the analysis period) must be sufficiently long, typically longer than 15 years. Shorter time periods are too distorted by random, temporary market conditions. In addition, most real estate financing takes over 20 years to be completely paid off.

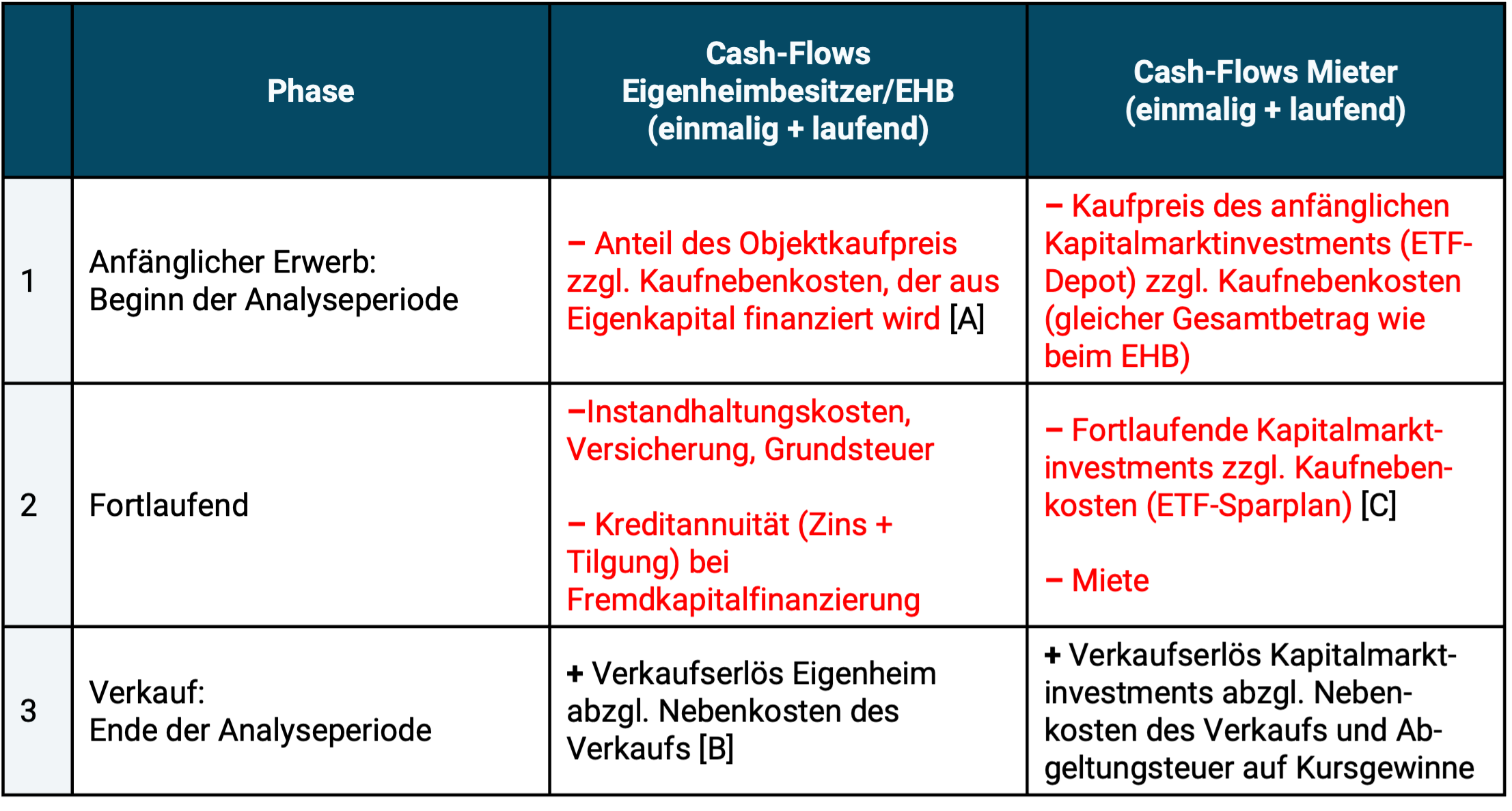

Table: Comparison of cash flows between homeowners (EHB) and tenants in an objective rent-or-buy comparison

Reading note: Cash outflows (from the perspective of the EHB or the tenant) are shown in the table in red and with a minus sign, while cash inflows are shown in black with a plus sign.

► [A] Additional purchasing costs for real estate: real estate transfer tax, broker fees, notary fees, land registry fees. ► [B] If the observation period is shorter than the time until the loan is fully repaid, the existing remaining loan debt is deducted from the sales price of the property to arrive at the net final assets. ► [C] It is assumed that all current income (e.g. dividends) minus taxes are immediately reinvested (investment).

If you design an economic buy-or-rent comparison like in the table, then the party with the higher net assets at the end of the observation period (final assets) has the “investment race”. EHB against tenants won.

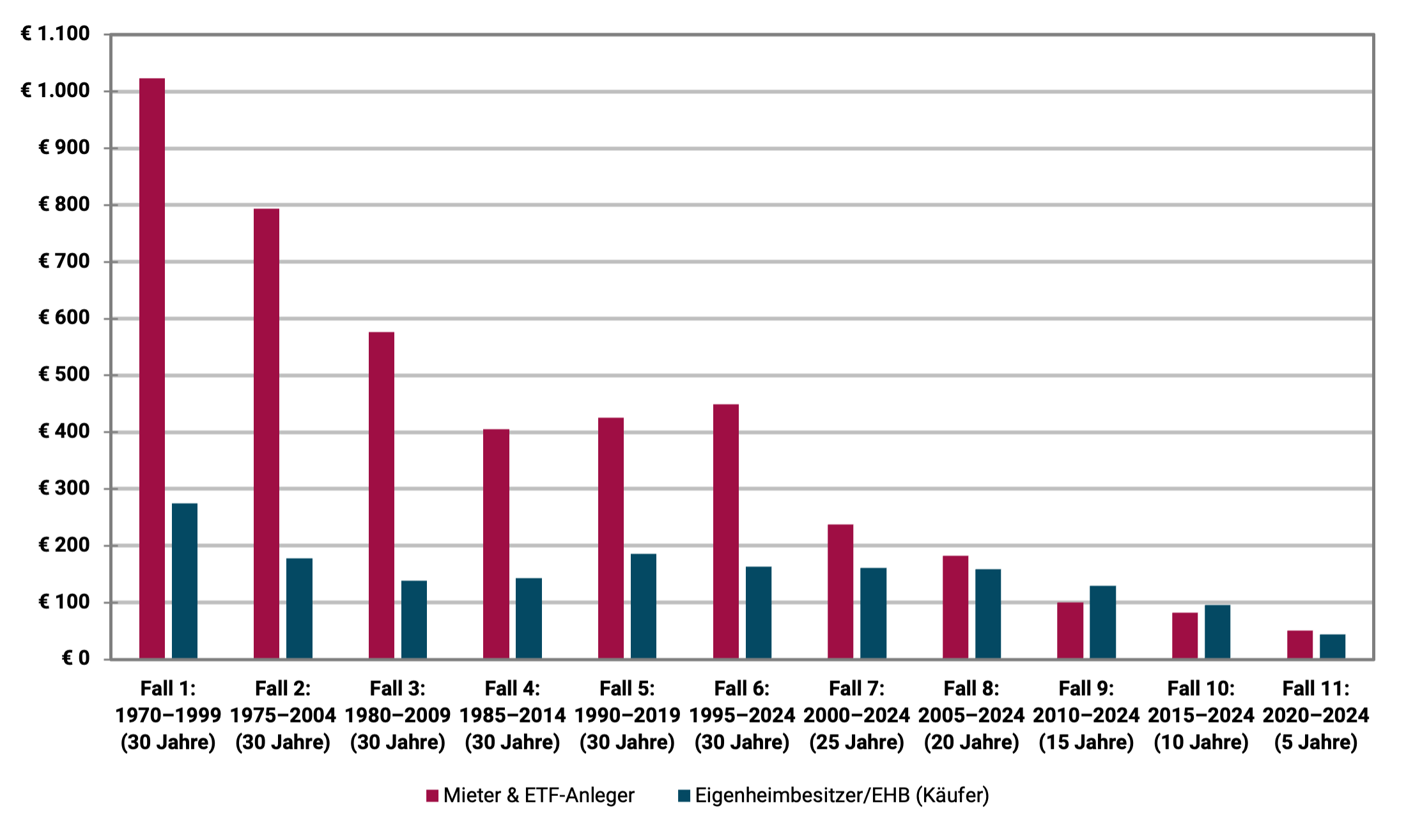

We summarize the results of such a calculation over the entire period from 1970 to 2024 (55 years) in Germany in the following figure. The tenant's capital market investment consists of a simple ETF portfolio on the MSCI World stock index on a buy-and-hold basis. [1] The real estate investment for homeowners is the average residential property in Germany. We accept initial 70% credit financing from the EHB.

We look at eleven different time windows, each lasting a maximum of 30 years, since a typical 70% real estate financing is fully repaid after around 28 years on average. We describe the further assumptions and inputs in the calculation at the end of this blog post in the appendix under point 2 for those readers who want to know exactly how we calculated. Readers primarily interested in the results may ignore the additional explanations in Appendix 2.

Figure: Comparison of the final wealth of homeowners/buyers versus renters/ETF investors in 11 different time windows between 1970 and 2024 (55 years)

► Final assets in EUR thousand.

The interpretation of the results in the figure: Why is the tenant in the lead in the majority?

In nine out of eleven cases, the tenant/ETF investor achieved a higher final net worth at the end of the second period under consideration. Only in the two cases 9 and 10 is it the other way around. However, the EHB advantage in absolute monetary units is small in these two cases: only 19 and 14 thousand euros, respectively.

In general, cases 10 and 11 have to be classified as less important for our conclusions compared to cases 1 to 9. Firstly because they only represent relatively short periods of time and secondly because of the rather insignificant absolute differences in final wealth between EHB and tenant. One could therefore speak of “draws” in “yield races” 10 and 11. A clearer result in one direction or the other would probably only emerge after another five to ten years.

The main reason why the tenant + ETF investor wins our buy or rent race nine out of eleven comparisons is that the equity global asset class produces noticeably higher total returns in the long term than the residential real estate asset class. This applies to German residential properties and it also applies to other countries for which corresponding total return data for residential properties is available. Nevertheless, it must be noted that residential property returns in Germany have been particularly low compared to other countries since 1970 to the present day.

But why is the tenant's final asset advantage in cases 1 to 6 so spectacularly high? (In case 1, for example, 748 thousand euros in favor of the tenant.) There are four reasons for this.

Cause #1: Cases 1 to 6 last the full 30 years, cases 7 to 11 do not. Due to the compound interest effect, differences in returns between two investments A and B have a greater impact on the final assets, the longer the observation period is.

Cause No. 2: German residential real estate recorded disastrously low increases in value in the 44 years from 1970 to 2013. At the end of these four and a half decades, the average German residential property, adjusted for inflation, was worth 16% less than at the beginning - the worst value among around 20 western countries for which such data is available.

Cause No. 3: From 1970 to 2013, real estate loan interest rates were significantly higher at an average of 7.4% p.a. than from 2014 to today at 2.2% p.a.

Cause No. 4: Rents and rent increases in Germany were comparatively low from 1970 to around 2015. During this time, this also favored the tenant/ETF investor side (as did causes 1 to 3).

What influence does the amount of the loan share, the “credit leverage” have?

In our calculation for the illustration, we assumed an initial loan financing of 70% for the EHB. If 100% equity financing had been used (i.e. zero credit), nine of the eleven time window cases would still have been in favor of the tenant, although the distribution of winners and losers and the absolute final asset values would have shifted.

A higher credit percentage than 70%, e.g. B. 85% would also have coincidentally resulted in a 9-to-2 overall result in favor of the tenant as shown in the figure, while this modification would in turn have changed the specific winner-loser distribution across the eleven cases.

In general, it can be concluded that it is popular in the real estate fan community Credit leverage [2] On balance, the EHB was rather detrimental to returns. The lack of financial benefit of the credit leverage effect on the final assets and return on equity of real estate investments contradicts the prevailing opinion in the real estate fan community and among those who make money from selling and financing real estate, i.e. brokers, banks and real estate coaches. In our separate blog post “The credit leverage myth in real estate” we show that and why loan financing (leverage) in commercial real estate financing - where there is better data regarding the effect of debt financing - is statistically detrimental to returns.

What impact would variable loan interest rates have had?

In many Western countries, private real estate loans mostly have variable interest rates, while in Germany long-term fixed interest rates of ten years or more dominate. Would variable interest rates have significantly changed the results in the figure? The short answer: Only marginally and more in the tenant's favor. He would have won the final wealth race in the case of variable interest rates in ten out of the eleven cases. Reason: The interest rates, which have risen sharply since the beginning of 2022, had a less favorable effect on the EHB.

Why does the media regularly report that homeowners are, on average, richer than renters in old age?

How do our results fit in with the statement that has been made repeatedly by the real estate industry, journalists and real estate influencers for decades, that pensioner households that own their own home have, on average, higher wealth than corresponding renter households? On the surface, the statement in question is true, but it is still a case of “lying with statistics”. For these households, home ownership is not the cause of their higher wealth, but rather the consequence - more precisely, the consequence of higher income, typically over decades, combined with a permanently higher propensity to save. [3] In addition, there is a statistically larger and/or earlier increase in assets through donations or inheritances for EHB households relative to tenant households.

Here is an illustration of the real estate industry's manipulative swapping of cause and effect in the situation just described: The average wealth of all Ferrari-owning households in Germany naturally exceeds that of non-Ferrari owners. Now the question: Was the Ferrari the cause of this wealth advantage? Of course not. If anything, the Ferrari did damage. Either way, the Ferrari ownership was the result of the wealth advantage. It's the same with home ownership. He is the one Consequence the above-mentioned causes (primarily higher income, higher propensity to save and therefore higher wealth). If one were to compare renters with homeowners who had the same long-term income and the same propensity to save, and if inheritance effects were taken into account, it would be shown that renters statistically achieve higher final wealth in retirement. However, such empirical studies do not exist for Germany.

What about the home ownership advantage of the “positive compulsory savings contract”?

Earlier we mentioned the higher propensity to save among home-owning households. A higher propensity to save can have two causes: (a) A higher income. It falls e.g. B. It is easier to save 20% of 10,000 euros of net income per month than 20% of 2,000 euros. Furthermore, the absolute savings amount in the former case is 2,000 euros and in the latter case only 400. (b) A purely psychologically caused higher “savings affinity”, i.e. if two households A and B have an identical net income, but household A saves 30% of it and household B only 5%, then household A has a purely psychologically caused higher propensity to save. In plain English: Household A is more economical and cuts down on consumption more.

If a home is financed with debt with a debt ratio of around 60% or higher, then this household will have to incur higher real estate-related expenses per month from loan annuity and other real estate expenses (average maintenance, insurance, property tax) than a comparable renter household. This difference exists until the annuity loan is fully repaid, usually 25+ years. Now the crux of the matter: Such an EHB household has no choice in making these expenses month after month until the loan has been fully repaid, otherwise it would lose the property to the bank through a seizure and would also perceive this loss as a social stigma. The comparable tenant household, however, is not under such pressure and risk with its ETF savings plan. He can stop saving every month and instead consume more without any short-term negative consequences. The tenant therefore needs a good deal of self-discipline in order to spend the same amount every month on financial training as the EHB for 25+ years. The latter, on the other hand, “is forced to do so by the circumstances” and is subject to a “positive compulsory savings contract” because of his real estate loan.

This effect - which is nothing other than the statistically higher propensity to save among owner-occupier households mentioned above - contributes to the fact that EHB households are actually statistically wealthier in old age than renters. But again: the statistical asset advantage of EHBs has nothing to do with the high profitability of the property. If anything, it can be said that this asset advantage despite of the home, not because of it. If a renter household has the same saving discipline as a home-owning household, the renter household will statistically have achieved a higher and often significantly higher final wealth by the age of 50, 60 or 70.

What if you don't use a 100/0 stock portfolio for the tenant, but rather a 60/40 stock-bond portfolio?

We based our rent-versus-buy comparison with a tenant on a 100% equity portfolio (an MSCI World ETF) because we believe that a globally diversified equity ETF on a buy-and-hold basis is less risky than a debt-financed investment in a single property. [4] (The fact that it is easier to observe and measure the ongoing fluctuations in the value of an ETF portfolio than the ongoing fluctuations in the value of the equity position in an individual property does not change this basic fact.)

If the tenant were to be based on a 60/40 portfolio consisting of an MSCI World ETF and a bond ETF (medium-term high-quality bonds), the final asset race in the eleven cases would no longer be 9 to 2 for the tenant, but only 7 to 4. The change in the result illustrates what we all ultimately know: stocks produce far higher returns in the long term than interest-bearing investments.

Two biases in favor of homeownership in our calculations

In two ways, our buy-or-rent calculation is biased in favor of buying.

Aspect 1: The calculation assumes that only one property purchase takes place during the observation periods. Although there is no data on the average holding period (median holding period) of a home in Germany, it is likely to be less than 30 years. Such figures are available for the USA. There, the median holding period for a home is around twelve years. In Germany it will be longer, but probably shorter than 30 years. Due to the very high transaction costs (additional costs of buying and selling) in real estate, the return on a home decreases as the holding period decreases. In addition, if a loan-financed home is sold “early,” there may be an expensive prepayment penalty on the loan.

Aspect 2: When taxing the tenant's stock ETF portfolio, the tax advantage that buy-and-hold has under the German withholding tax was not taken into account. We quantified this tax advantage in a separate blog post (“Save taxes through buy-and-hold”).

The academic literature on buying versus renting

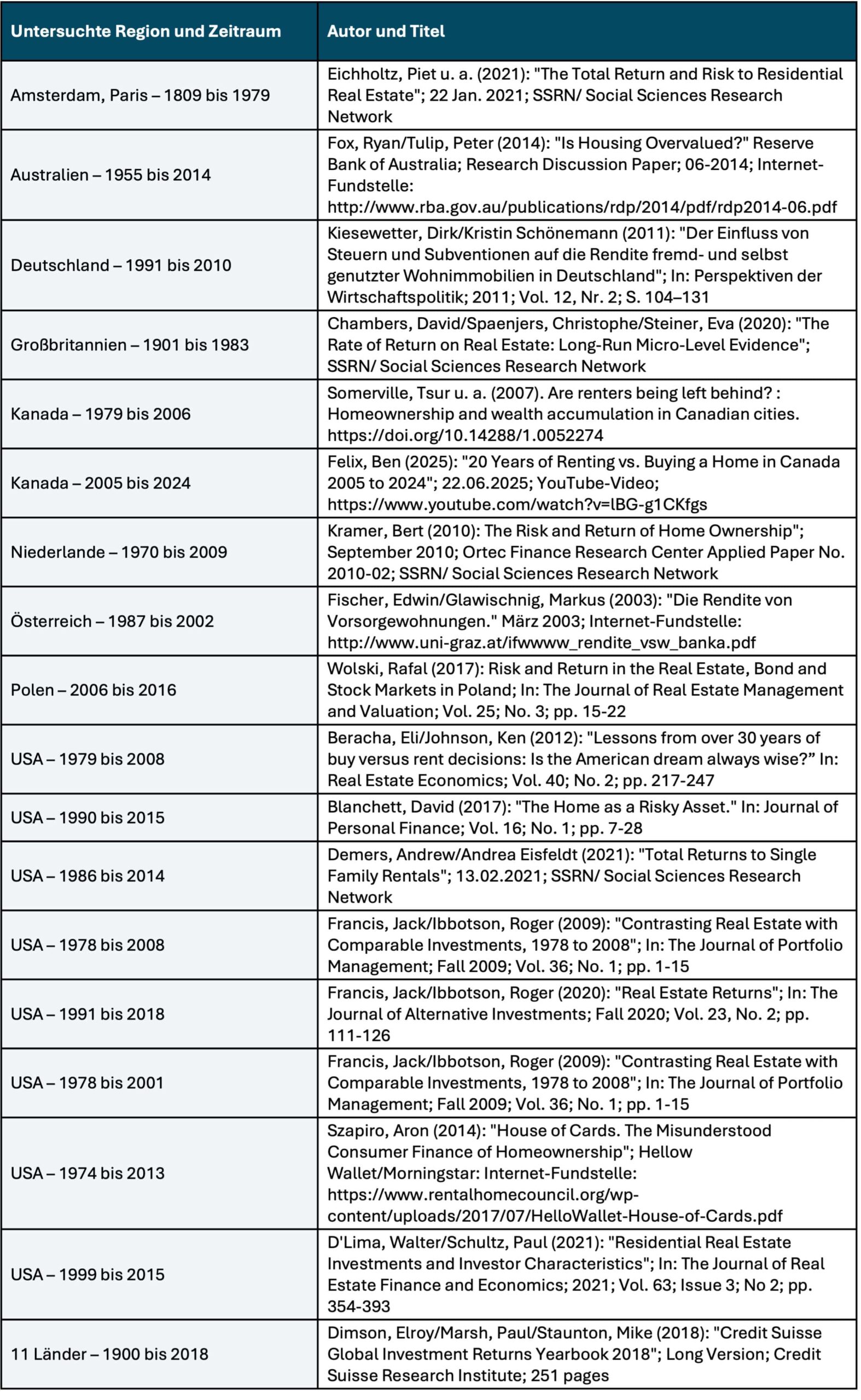

Our buy-or-rent results for Germany presented here are consistent with the basic trend from a number of similar historical buy-or-rent studies or general real estate yield studies for other countries and time periods. At the end of this blog post we list 18 such academic studies in the appendix under point 3.

Conclusion

In the 55 years from 1970 to 2024, renting combined with a simple, broadly diversified stock investment on a buy-and-hold basis was statistically more profitable in Germany than buying a home. This is what our empirical calculation shows and which is confirmed by a large number of comparable analyzes by researchers for other countries and time periods.

These results contradict what most Germans believe about the relative economic attractiveness of buying or renting.

The fact that banks, brokers and real estate influencers claim otherwise can easily be explained by the conflicts of interest of these parties.

The fact that many journalists and media outlets have been repeating the “buying is predominantly more profitable than renting lie” for decades is probably the combined result of “parroting prevailing opinions” and “not wanting to do strenuous research”. In addition, the mainstream media is reluctant to mess with wealthy advertising customers from the real estate and banking industries.

Attachment

Appendix (1): Free Buy or Rent Calculators on the Internet (in alphabetical order)

- Financial flow, independent finfluencer

- Financial tip, consumer protection organization (non-profit)

- Frankfurter Allgemeine Zeitung (daily newspaper)

- Gerd Kommer, author, asset manager (that “Buy versus rent tool” for the book “Buy or rent” by GK can be downloaded free of charge as an Excel file from Campus Verlag under the menu item “Additional material”)

- fmh financial advice, real estate portal (owner: private individuals)

- immoscout24, real estate portal (owner: Scout24 SE)

- real estate world, real estate portal (owner: Axel-Springer-Verlag)

- Dr. Small, credit broker (owner: Hypoport AG)

- Lazy Investors, independent finfluencers

- Stiftung Warentest, consumer protection organization (owner: non-profit foundation)

Appendix (2): The assumptions and data used in the calculation in the figure/graphic

On the real estate side (homeowner/buyer): The property costs 100,000 euros in all eleven cases. (For reasons of simplicity, we use the unrealistically low purchase price of 100,000 euros for a home today, but not in the 1970s, in order to calculate with “round numbers”. If one were to assume 400,000 or one million euros instead, for example, this would have no influence on the relative final result.) The additional costs of the purchase (including property transfer tax) are assumed to be 8%, those of the sale to 8% 1.7%. [5] The purchase and additional purchase costs are financed 30% from equity and 70% from a loan. The loan interest rates are the interest rates for annuity loans to private households with a ten-year fixed interest rate (the interest rate is adjusted every ten years). It is assumed that it will take 30 years for full repayment. The increase in value of the property corresponds to that of the average German residential property during this period. The ongoing additional costs (maintenance, insurance, property tax) correspond to 1.3% p.a. of the current property value. [6] The underlying statistical data comes from the BIS Basel and Bundesbank websites.

On the tenant side (tenant + ETF investor): The tenant initially invests the equity share of 32,400 euros initially spent by the EHB in a world portfolio consisting of an MSCI World index fund (ETF), as such a portfolio is comparable to a debt-financed individual property in terms of its long-term risk. Assumedly he lives in an identical property as the EHB. The rent for this property is based on the historical rental yields for residential properties (apartments) in Germany. Since the tenant's monthly or annual rent is below the EHB's total cash outflow, the tenant saves the difference every month in his ETF portfolio, so that both always spend the same amount on housing and wealth creation. The underlying statistical market data comes from Bulwiengesa and MSCI.

At the end of each of the eleven cases/periods under consideration, both EHB and tenants sell their investments. The tenant pays tax on his ETF investment continuously (dividends) and at the end when it is sold (price gains). Price gains from stock investments were tax-free for private investors in Germany until the end of 2008, after which they will be subject to capital gains tax. [7] Capital gains on homes are tax-free in Germany. In the five cases 7 to 11, the observation period is shorter than 30 years. Therefore, you will have a remaining debt balance with the EHB at the end of the period. To simplify matters, we assume that it will be repaid from the property sale proceeds without any early repayment penalty.

The payments (initial equity deposit and subsequent payments) for the buyer and tenant for the eleven cases are as follows. Case 1: €333 thousand, Case 2: €306 thousand, Case 3: €313 thousand, Case 4: €279 thousand, Case 5: €281 thousand, Case 6: €245 thousand, Case 7: €212 thousand, Case 8: €160 thousand, case 9: 119 thousand euros, case 10: 84 thousand euros, case 11: 54 thousand euros. (Cases 1 to 6 have the same length and should therefore have approximately the same amount of deposits. The existing differences result from different interest levels.)

Appendix (3): List of scientific studies on empirical comparisons of returns from buying or renting

The studies mentioned in the following table come to the conclusion for different time periods and countries that either real estate has lower total returns than stocks or that renting + capital market investment is overall more profitable than purchasing a home with or without debt financing.

Scientific studies on historical returns on residential properties or on buy-or-rent comparisons for different countries or major cities and different time periods

► This literature evaluation primarily took into account scientific studies that cover sufficiently long historical periods, as periods of less than approximately 25 years are only of limited or no significance. ► Not taken into account were (a) publications from the banking or real estate industry that were obviously burdened by conflicts of interest; (b) studies that represent only long-term historical appreciation rather than total returns on residential real estate; (c) buy-or-rent studies that formulate purely model theoretical conditions under which either buying or renting is more attractive; (d) Forward-looking, purely predictive buy-or-rent analyses.

Endnotes

[1] In the 1970s, index funds/ETFs were not yet available for private investors in Germany, but even then a private investor could have easily acquired a broadly diversified stock portfolio on a buy-and-hold basis.

[2] “Credit leverage” = The effect of partial debt financing on the return on equity of an investment (leverage effect).

[3] The propensity to save means the percentage of a household's net income that it does not consume, i.e. invests in wealth creation.

[4] If the property is at construction risk (in the case of a new build or major renovation), the property is even riskier.

[5] The sum of these transaction costs is likely to be at the lower end of what is usual in the market.

[6] In our separate blog post “Maintenance costs – how to calculate real estate investments” let's make this assumption plausible.

[7] We did not take into account the fact that price gains from so-called “old cases” – ETF shares that were acquired up to the end of 2008 – remained tax-free to a limited extent even after 2008, to the detriment of the tenant.