From Gerd Kommer and Cornelia Kees

There is no longer any need to prove that active investment management in capital market investments consistently produces worse long-term returns than passive, broadly diversified buy-and-hold investing. Since around 1960, the superiority of passive strategies has been empirically confirmed again and again by scientists in countless studies. Nevertheless, here are a few numbers. Using current data, they illustrate the “active investing disaster” for actively managed equity funds (UCITS funds) sold in the EU. [1]

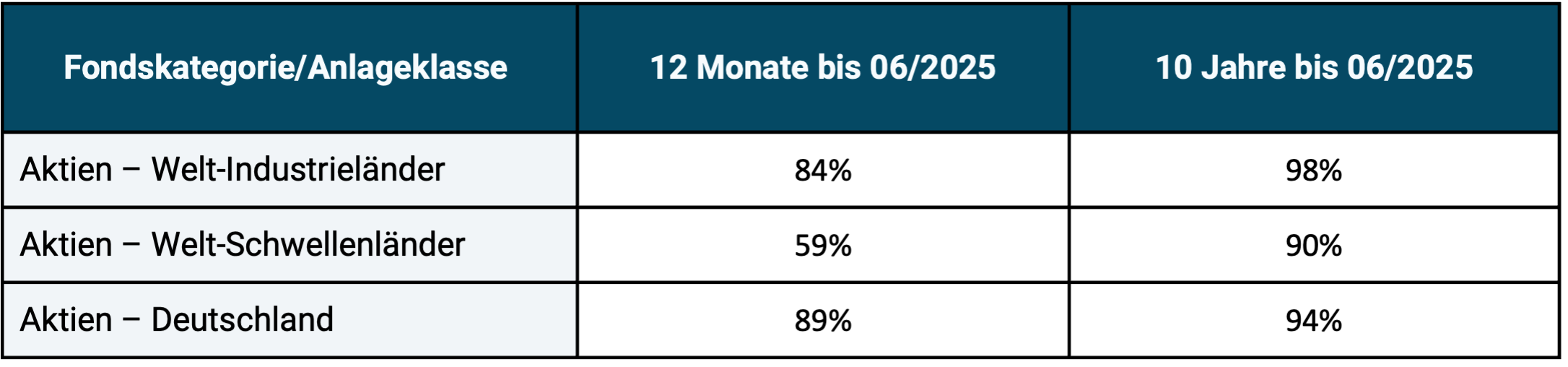

Table 1: Proportion of European-domiciled, actively managed equity funds that underperformed their passive index benchmark in two periods

► Source: S&P Dow Jones Indices “SPIVA Europe Scorecard Mid Year 2025” (Equal Weighted Funds). ► Returns in euros. ► Without taking costs into account in the benchmark, but also without taking into account any costs for any issue charges of the actively managed funds. ► Original data rounded to whole numbers.

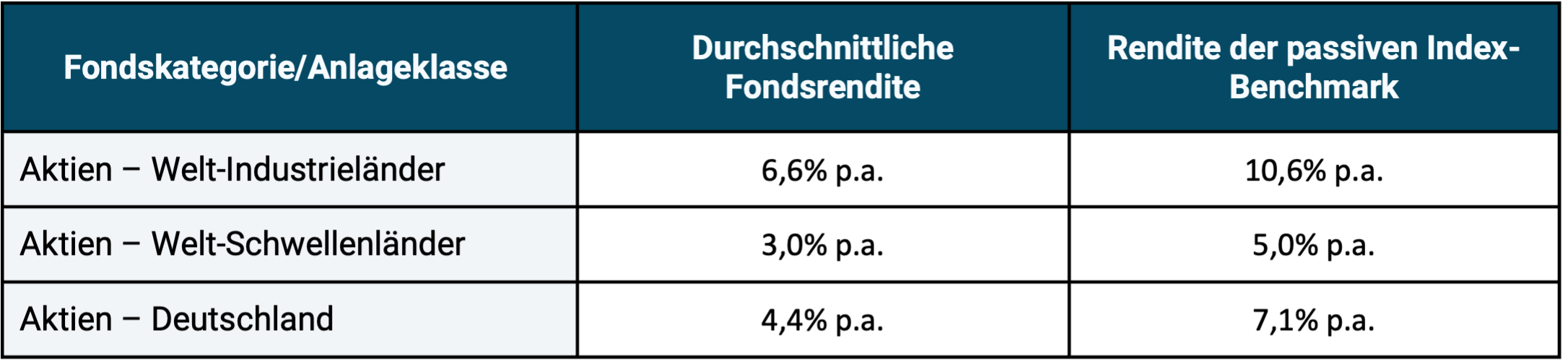

Table 2: Comparison of the average returns of the funds from Table 1 with the returns of the correctly selected passive benchmark for the period 06/2015 to 06/2025 (10 years)

► For explanations, see information below Table 1. ► Original data rounded to one decimal place.

Given the depressing results in the two tables for active fund management, an investor might object: "Maybe so, but I'm not interested in that, I'll just invest in a fund from the small minority of active funds that beats its passive benchmark." However, this obvious consideration does not help us in practice. Reason: The minority of outperforming funds that exist for each time window can be ex ante cannot be identified reliably enough, because the composition of this mostly small group probably changes randomly from time window to time window. However, due to space limitations, we do not show any data on this in this blog post.

In this blog post, we want to answer the question of why active investing performs so consistently poorly, as is selectively suggested here using actively managed UCITS funds in the equities asset class. [2]

Strangely, the answer to this question is rarely given in financial advice books, mainstream media print articles, YouTube videos, and other social media posts by finfluencers. This answer has to do with the question of the predictability of financial market sizes. Active investing is always forecast-based Invest.

Active investment management ultimately fails because the underlying forecasts are too often wrong.

These can be forecasts about the future prices of securities, the level of dividends, securities indices, interest rates, foreign exchange rates, slumps in the stock market, inflation rates, company profits, the completion or lack of company mergers, the course of restructuring measures in companies, real estate prices, precious metal prices, the Bitcoin price, economic growth rates, unemployment rates, the number of bankruptcy filings in the economy, regulatory measures, tax changes, important political ones Decisions – anything that investment managers believe will significantly impact the forward economic prospects of a particular investment asset, such as a listed company.

Forecast-based investing and its problems

Now the question arises: If forecast-based investing – as we have seen in Tables 1 and 2 – is economically damaging, i.e. works poorly, why do forecasts continue to be created, used and followed by the majority of all private investors or the service providers they commission (e.g. asset managers or fund managers)?

Below we list the six most important cognitive, social and institutional reasons for this particular form of human irrationality.

(1) The misinterpretation of the small number of actually correct forecasts

Of the millions of economic and financial forecasts made by someone somewhere around the world every year, a small number will later turn out to be correct. In most cases, these correct forecasts can be easily and plausibly explained by the law of large numbers, the operation of chance. So these are probably lucky hits from which nothing can be derived for the future, especially not that they can be reliably repeated. And yet these are repeatedly misinterpreted as evidence of forecasting ability.

If 100 million people each roll the dice ten times in a row, then statistically there will be one or two people (1.65 to be exact) who roll a six ten times in a row, even though the probability of this for a single person is only 0.0000000165 (that is less likely than six numbers in the lottery). The number of people who invest in the capital markets significantly exceeds 100 million, many make more than ten investment decisions per year and the capital markets have existed for over 100 years. Because so many of us individually do improbable things, the insight of statisticians, which only seems paradoxical at first glance, applies: “The improbable is probable.” [3]

(2) Failure to recognize “One Trick Ponies”

We all know the names of “financial experts” who supposedly or actually predicted an extremely rare major financial event, a “black swan,” and are therefore considered “great foretellers,” investment gurus, and who seem to prove that correct predictions are systematically possible. One of these gurus is Nouriel Roubini, an economics professor at New York University (NYU). In 2006 he correctly and surprisingly precisely warned of an impending major financial crisis. This actually began in early 2007 with a sharp price crash in the US housing market, which then dragged down a large part of the global banking industry and the global stock market.

Does this provide evidence that Roubini can reliably predict important macroeconomic reversals or financial catastrophes? No. Roubini is actually what American parlance calls a “one trick pony,” a horse that can only do one trick.

There are two types of forecasters in the financial industry. Type A: Someone who repeats a certain forecast over and over again for years, but is constantly wrong. However, no one in the media is interested in this failure, since forecasts from unknown people that do not come true are not worth reporting. But then the same forecast, which has been wrong several times over, comes true and is now picked up as a huge sensation by the media and literally spread worldwide. Headline: “He/she knew beforehand, but no one listened to him!” The public is not informed that one correct forecast follows many incorrect ones. No one pays any attention to the few who investigate and uncover the scam.

There is also variety 2 of the One Trick Pony. Here the actor actually makes a prediction for the first time about an important event that is considered very unlikely and promptly hits the mark. Our guru is now experiencing a tsunami of media attention. The media begs him for new forecasts, which he subsequently makes because he has recognized the marketing value he now has. The new forecasts no longer come true. But it will take years before this becomes clear enough.

This is the Roubini one-trick pony variant. His list of false predictions from late 2008 to today is too long to be expanded upon here.

But the same thing: In both one-trick pony cases, the media and the investment community are hoping for the “guru” for a few years, when in reality this was simply a case of “more luck than sense”. As it becomes apparent over a longer period of time that the guru can no longer deliver correct predictions, the media loses interest in him. The media entourage is now moving on in search of a new, fresh guru.

(3) The unwillingness of the media and many investors to recognize “manipulative forecasts.”

Manipulative forecasts (“MPs”) are those that look like “honest” or “real” forecasts, but are not. Honest, real forecasts are formulated in such a way that both their occurrence and non-reality can be unequivocally recognized. This does not apply to MPs. With MPs, only the arrival can be clearly determined, but not the non-arrival. They fulfill the philosophy of science Falsification criterion not. [4]

In most cases, the lack of falsifiability (theoretical or fundamental refutability) results from the author of the prediction deliberately omitting a clear indication of the time. A simple example of such an MP: “It will rain.” It is obvious that this forecast can only either (a) not have happened yet or (b) have happened (i.e. true) but (c) can never not have happened (i.e. false). If such an MP turns out to be true at some point, it says absolutely nothing about the competence of the author of the forecast. A reliable statement about competence would require a falsifiable prognosis.

MPs are logically pointless and statistically overwhelmingly harmful as the basis of an investment strategy. Nevertheless, the MPs that arrive are often interpreted as evidence of competence in favor of the forecaster.

Seven MP examples from the investment world:

(a) “The S&P 500 Index will continue to rise strongly.”

(b) “We see a price target of 41 euros for Deutsche Bank shares.”

(c) “The Bitcoin price will come back in the medium or long term.”

(d) “Samsung stock is undervalued and a Strong Buy.”

(e) “The US stock market is heading for a sharp correction.”

(f) “The Eurozone will break up.”

(g) “E-cars will prevail.”

In all of these cases there is no verifiable time indication. Since it is missing, the predictions can come true (become true), but they can never not come true (become false). In (c), (d), (e), (f) and (g), the predicted event is only described ambiguously. Here, the forecaster cleverly left open a second non-falsifiability loophole in addition to the non-specific time period/point in time. That's doubly clever and doubly cynical.

The following basic rule applies to the marketing of MPs to the audience: If the prediction is correct, the forecast author will claim spectacular foresight and competence and market it lucratively. If it doesn't happen, he has an almost unbeatable excuse for the first five years or so after the forecast was made. After that, no one remembers it anyway. The Anglo-Saxons call something like this a “one way bet” – a bet that you can only win.

Another MP variant is “flexible” or “vague” forecasts. They can contain a time indication, but are still not falsifiable. Example: “We see a correction potential of 20% for Tesla shares by the end of this year.” A period of time is given here, but the term “potential” is so vague that one can still only speak of one MP. In addition, the forecast is true even if Tesla first rises 50% by the end of the year and then falls 20%, i.e. has increased on balance.

If such a flexible or vague forecast has not materialized after the specified time period, the author of the incorrect forecast - in the rare cases that someone remembers the forecast - will make the protective claim that he was simply talking about a "potential" that depended on specific, but now not realized, secondary conditions or assumptions. If he was right by chance, all vagueness and all occurrence of alleged secondary conditions will be forgotten.

(4) Cleverly marketing the small number of correct predictions

Virtually all forecasters are “big talkers,” making hundreds of direct and indirect, explicit and implicit forecasts over the years. Because of the sheer volume of their chatter, talkers are bound to at some point say something that will later prove to be an impressively accurate prediction. One could speak here of the “prognostic law of chatter”. But because the big talkers are dishonest, they market their few correct forecasts loudly and intensively, but ignore their many more false forecasts. This is a cheap and easy-to-see sleight of hand, but the media and the public mostly fall for it anyway. Quite a few particularly cynical media outlets are even complicit in this manipulation.

A big reason why the big talkers among financial forecasters get away with their trick so easily lies in “Brandolini’s Law,” also known as the “Bullshit Asymmetry Principle”: “The amount of energy required to refute bullshit exceeds the amount required to produce it by orders of magnitude.” [5] The effort required by a third party to provide clear proof that this is a prognosticator who makes many estimates and who, in total, made many more incorrect forecasts than correct ones, is higher than the effort that the big talker had to put his nonsense into the world. In addition, there is little commercial gain from such proof for those who provide it. (Here an example of a complex proof of four such chatterboxes that we once undertook ourselves.)

(5) Accept the absurd world of “revised forecasts”.

In the so-called “serious financial industry”, especially in the banking sector, for example, stock price forecasts or forecasts of macroeconomic variables such as interest or inflation rates that turn out to be incorrect are routinely “revised”, i.e. replaced by new forecasts. That sounds professional, but it's the opposite. A prediction either comes true, then it was correct, or it doesn't, then it was wrong. A “revised forecast” is a new forecast that typically follows an incorrect one. The sleight of hand of “revised forecasts” doesn’t bother anyone in the financial community. Rather, it is a ritual core part of what investment banks communicate to the public about their investment recommendations day in and day out and the media readily parrots them, giving them a professional flair. Why? Because the media – especially in the business sector – constantly need new content. “Revised forecasts” provide this financial junk food for an information machine that has to be “on air” 24/7.

(6) Naively applying the laws and rules of other disciplines to the financial sector

For many people, it is part of their economic worldview, a fundamental economic belief that has never been questioned, that the advantage in specialist knowledge that financial specialists have over non-financial specialists includes the ability to predict future developments of important financial market players. Just as a doctor can often correctly and accurately predict the future course of an illness, or an engineer can often precisely predict when a machine will fail or a component will break.

Yes, there is the ability to make predictions in many areas of life, but not in the financial market, at least not systematically exploitable As far as forecasts are concerned. “Systematically exploitable” here means that the implementation of these forecasts as part of an active investment strategy produces reliably better performance after costs, taxes and risk than a technically correct, forecast-free investment on a buy-and-hold basis with broadly diversified, low-cost index funds/ETFs.

If the existence of “predictability on financial markets” is part of a person's economic worldview, personal experience with forecasting errors, even painful forecasting errors, usually does not change one's opinion. If forecast-based investing causes harm to these investors, they generally do not conclude that forecast-based investing is bad, but rather that better forecasts are needed, either better forecasts from themselves or from a financial service provider they use. In still other cases, the damage is not even recognized.

In view of all this, the question naturally arises as to why economically reliably exploitable predictions in the financial sector necessarily fail on balance.

Three structural causes for the majority of financial forecast failures

Cause 1: The information efficiency of the capital markets, which is within the framework of the Efficient Market Hypothesis is examined and documented. This information efficiency means that new information that influences the price of listed securities is reflected (priced in) very quickly in the price, faster than the vast majority of investors or analysts can react to it. Based on this “estimated” public information, no price forecasts can be made that can reliably beat the market after taking costs, taxes and risk into account. The increasing spread of artificial intelligence will further increase the already very high information efficiency of the capital markets. We have our own for this purpose Blog post written.

Cause 2: Markets are “complex, dynamic, non-linear, non-stationary systems”. Even small changes in the initial conditions of such a system often cause extreme differences in the final results, so-called butterfly effects. [6] Such “complex adaptive systems” are not the same as “complicated systems.” A gas power plant is a complicated, but not complex, system. The behavior of complicated systems is easier to predict than that of complex systems. Although we can say a lot about the general properties of a complex system, we cannot make specific, reliable and economically exploitable predictions about its behavior over a clearly defined period of time.

Cause 3: Forecasts in social systems, including markets, are even more so more self-referential (more circular), the more people there are - e.g. B. based on positive past experiences – consider this to be true. The prediction then affects the object of the prediction and thus deprives the prediction of its starting point and thus reduces its accuracy. In short: the more people believe a forecast, the more likely it is to lose its validity. Systems that are not exposed to human intervention in this sense, such as a volcano, a swarm of bees, a machine or a diseased human organ, are subject to this Self-referentiality of social systems and therefore rather meet the basic requirement for predictability. Benjamin Graham, Warren Buffett's famous mentor, put it this way: "A moment's thought will show that there is no such thing as a scientific prediction of economic events under human control. The very 'dependability' of such a prediction will cause human actions which will invalidate it." [7] Because this is the case, the use of artificial intelligence will not bring about any fundamental improvement in terms of forecasting ability. If anything, AI will contribute to the opposite, because its gradual spread and further improvement will mean that more and more people will become better informed about a given issue at an ever faster rate. In doing so, it further increases the self-referentiality and information efficiency of financial markets.

The empirical evidence that following financial forecasts leads to avoidable damage to returns over the long term, absolute losses or opportunity costs (lost profits) relative to comparable buy-and-hold investments, is overwhelming. The rational conclusion from this: practice prediction-free, passive investing as the financially more attractive and accessible alternative.

The future in social systems cannot be reliably predicted beyond useless “open”, here called “manipulative” forecasts. It is not so because of real predictability structural There are obstacles in the way that cannot be overcome by ultimately childish “prediction-repair strategies” such as the following:

- make even more, even more frequent forecasts,

- Use forecasts from other still “unburned” forecasters

- look for a better mathematical forecasting algorithm (e.g. in the form of AI).

- incorporate more comprehensive data analysis into the forecast

Conclusion

From our point of view, do-it-yourself investors would do well to make as few financial forecasts as possible, i.e. to invest on their own without any forecasts.

Anyone who has delegated their investment to a third party should give up the hopeless search for a “capable financial forecaster”.

Anyone who accepts this has excellent chances of achieving higher net worth as an investor and finding greater financial peace of mind as a person.

On the other hand, rational members of the financial industry, including the now large group of finfluencers who are involved OPM (Other People’s Money) Make money, don’t give up making predictions. Her “street smarts” made her realize that you can make good money with forecasts – even those that are mostly false and/or manipulative. This has been the case in the past and will continue to be the case in the next ten years. We dare to make this prediction. 😉

Endnotes

[1] UCITS funds are typically simply called “investment funds”. “UCITS” stands for “Undertakings for Collective Investments in Transferable Securities”. UCITS funds may essentially be freely distributed to private investors (consumers) within the EU. In addition to UCITS funds, there are other types of funds that may not be freely marketed to private investors, e.g. B. Hedge funds and other types of institutional funds.

[2] “Active underperformance” also exists in do-it-yourself private investor portfolios or in other fund categories, such as. B. Hedge funds. However, UCITS funds have the most comprehensive database.

[3] See the book by David Hand (2014): The Improbability Principle: Why Coincidences, Miracles, and Rare Events Happen Every Day; Scientific American/Farrar, Straus and Giroux.

[4] See the articles “Falsificationism” in the German Wikipedia or “Falsifiability” in English.

[5] See the article “Brandolini’s Law” in the English Wikipedia.

[6] See the book by Nassim Taleb (2007): The Black Swan. The Impact of Highly Improbable; Penguin Books. German edition: “The Black Swan”.

[7] If you think about it for a moment, you will quickly realize that economic events controlled by humans cannot be predicted scientifically. The very reliability of such a prediction will cause people to act in such a way that the prediction becomes inaccurate.