From Gerd Kommer and Felix Grossman

In this blog post we look at four “prophets of doom” known in Germany: Marc Friedrich, Max Otte, Dirk Müller and Markus Krall. We show the high opportunity costs, i.e. lost profits, suffered by those who invested in the funds and portfolios of this quartet. We also show that and why those who sympathize with the theses of the prophets of doom almost never consistently implement their general investment recommendations.

What we don't explore in this article is how poor the forecast quality of our four "experts" has been so far. Anyone who would like to take a closer look at this fact, which is not very encouraging for the credibility of the quartet of forecasters, is referred to our detailed list of publications at the end of this article. In these publications, countless incorrect forecasts made by the four are documented in a reader-friendly manner.

The books we are referring to in this blog post are:

- Markus Krall: “The Draghi Crash: Why unleashed monetary policy is leading us to financial catastrophe”; 208 pages; June 2017 [updated with further investment recommendations by Krall's follow-up book "When Black Swans Have Babies", December 2018]

- Dirk Müller: “Powerquake: The world facing the greatest economic crisis of all time – background, risks, opportunities”; 350 pages; September 2018

- Marc Friedrich/Matthias Weik: "The biggest crash of all time: economy, politics, society. How you can protect your money now"; 400 pages; October 2019 [updated with further investment recommendations through Friedrich's follow-up book "The Greatest Opportunity of All Time", April 2021 - Friedrich separated from his long-time business partner and co-author Weik at the beginning of 2021]

- Max Otte: “World System Crash: Crises, Unrest and the Birth of a New World Order”; 640 pages; October 2019

The titles and subtitles of these books alone make it clear that these are not the usual announcements of stock market crashes or market corrections that have been raining down on the investment community in print media and on the Internet for ages. Rather, the books mentioned here and their authors proclaim the economic apocalypse, the “system crash”, the overall collapse of our banking system and monetary system, the “collapse of the Eurozone”, the national bankruptcies of Germany and other countries, including, in the Friedrich/Weik case, the USA and Switzerland, as well as the emergence of a “new world order”, the “reset”.

Two of the four constant doom painters – Krall and Friedrich/Weik – each name a specific date for the “meltdown” in Germany: Krall the last quarter of 2020, Friedrich/Weik “2023 at the latest”. Krall's prediction did not come true and must therefore already be considered wrong. With Friedrich/Weik we have to wait another two and a half years for the Armageddon prediction to be confirmed or refuted.

In their books, Müller and Otte remain vague with regard to specific points in time for what they describe as the “greatest economic crisis of all time” or the “world system crash”, but they also use vocabulary such as “foreseeable”, “soon” or “it won’t work like this for much longer”.

Speaking of timing and validation of forecasts: Three of the four - Friedrich, Otte and Müller - predicted the near or imminent “bankruptcy” of Germany and the collapse of the Eurozone, deflation or runaway inflation, sometimes years before the books listed above were published. As mentioned, at the end of this article there is a compilation of publications that describe these and other incorrect forecasts in great detail.

What all four naysayers have in common is that they implicitly or explicitly transfer economic problems and issues (many of which only concern Germany or the Eurozone) to the investment market. This is clearly wrong. We'll explain why it's wrong here. It cannot be clarified whether the naysayers make this mistake out of sheer ignorance or with manipulative intent.

Below we will examine two issues for each of the four end-time prophets:

Firstly, what investment recommendations the respective prophet of doom (hereinafter referred to as “UP”) makes in his book mentioned above and secondly, what are the opportunity costs (the lost profits) of those investors who implemented the investment recommendations of the four in liquid assets.

Prophet of Doom 1: Marc Friedrich (and Matthias Weik)

We start with the shrillest of the four apocalyptists, Marc Friedrich.

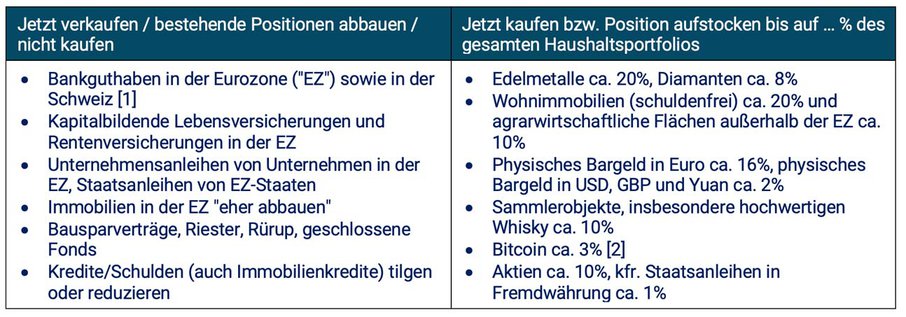

Table 1: What Marc Friedrich recommends for the downfall

► Information according to Friedrich/Weik: “The Biggest Crash of All Time”, 2019. ► [1] Friedrich/Weik are of the opinion that Switzerland will collapse along with the Eurozone because the Swiss National Bank has become too connected to the Euro and the Eurozone and has become “dependent” on them. ► [2] In his new book (“The Greatest Opportunity of All Time”, April 20, 2021), Bitcoin and other cryptocurrencies are said to comprise “up to 20%” of a household’s total portfolio. Since the book was published, the Bitcoin price in euros has fallen by around 35% (as of June 29, 2021).

According to our consulting experience with wealthy private households who have read the Friedrich/Weik book and sympathize with the core statements made in it, these households practically never implement the investment recommendations summarized in Table 1. This should hardly be surprising if you take a closer look at the individual recommendations. Ultimately, they are simply too “unconventional” or, to put it less benevolently, too otherworldly relative to the investment situation of normal and even more wealthy households. We will explain why you can see it this way below.

Now about the opportunity cost. Those who followed Friedrich/Weik in the four years since the investment fund managed according to their ideas (“Solit Value Fund”) existed, have fared rather miserably all in all. A simple ETF investment in the global stock market on a buy-and-hold basis would have produced more than double the return. After all, an investor in the Friedrich investment fund fared better in terms of risk than the ETF investor.

Table 2: Return and risk of the Friedrich investment fund compared to the general stock market

►[1] 01/2017 = Launch date of the Solit value fund. ► [2] Period since the start of the “Corona stock crash”. ► [3] The fund return shown does not include the Solit fund's initial issue premium of 4%.► [4] Index return minus an ETF expense ratio of 0.4% p.a.

It wasn't just from the launch of the Solit fund in January 2017 that Friedrich caused his followers to lose profits. Nine years ago, in mid-2012, and since then again and again, Friedrich/Weik announced national bankruptcies, the collapse of the Eurozone, the end of the “fiat money system”, a sharp increase in inflation and the “foreseeable” bursting of various bubbles, for example the “government bond bubble”. Anyone who took these predictions, which have so far largely failed to come true, as an opportunity to sell off risky, high-yield assets such as European stocks, long-term bonds or German real estate at this time was likely to have done badly financially and the more disciplined (i.e. earlier) they followed Friedrich/Weik, the worse they would have done. The recommendation to invest 3% of the released capital in Bitcoin - a very profitable investment since the Friedrich book was published in October 2019 - did not make up for this lost income.

Prophet of Doom 2: Max Otte

We move forward to Max Otte, who made new headlines last May when he became chairman of the Values Union, a party unit within the CDU/CSU.

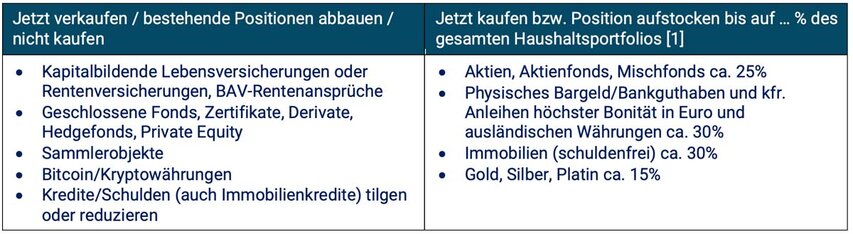

Table 3: What Max Otte recommends for the downfall

► Information according to Otte “World System Crash”, 2019. ► [1] Shown here is the “very conservative crisis depot” in Otte, 2019, p. 483.

Here, too, the assessment arises that only a few wealthy private households that agree with Otte's economic worldview consistently implement these investment recommendations. Consider his advice to pay off all real estate loans to the maximum or to shift 60% of assets into physical cash, bank deposits and short-term bonds of the highest credit rating in euros or foreign currencies.

What is noticeable about Otte is that his recommendations differ significantly from those of Friedrich/Weik. In principle, the same applies relative to the three other UPs and it ultimately applies to all four of them. These differences, some of which are considerable, are remarkable in that the economic worldview of the four is very similar. At the end of this article we will talk about the important but often overlooked issue of what the large deviations between the UPs' investment recommendations mean for a private investor who fundamentally agrees with these pessimistic views.

Back to Otte. Those who invested in his investment fund have also had to pay an opportunity cost, as shown in Table 4. One consolation: The relative disadvantage - the percentage under-return compared to the ETF benchmark - is the smallest for Otte of all four turbo pessimists.

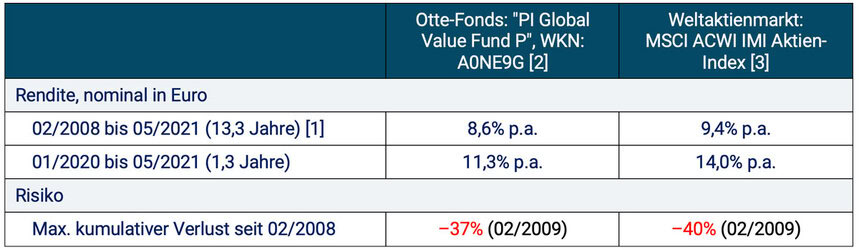

Table 4: Return and risk of the Otte investment fund compared to the general stock market

► [1] February 2008 was the launch date of the Otte fund. ► [2] Largest and oldest of two Otte funds. ► [2] The fund return shown does not include the fund's initial issue fee of 5%. ► [3] Index return less an ETF expense ratio of 0.4% p.a.

He also did not fulfill Otte's claim to protect his investors from the worst turbulence in the stock market. In terms of risk, measured by maximum drawdown (maximum cumulative loss), it was only marginally better than a world equity ETF on a buy-and-hold basis over the last 13 years, and even worse in terms of volatility, which is not shown in the table.

Prophet of doom 3: Dirk Müller

We now come to Dirk Müller. It can be said that in the past 10+ years, probably no other fund manager and “investment expert” in Germany has had more media presence than him.

Müller's investment recommendations are similar to Krall's in some respects, but differ significantly in others, as we illustrate in Table 9 below.

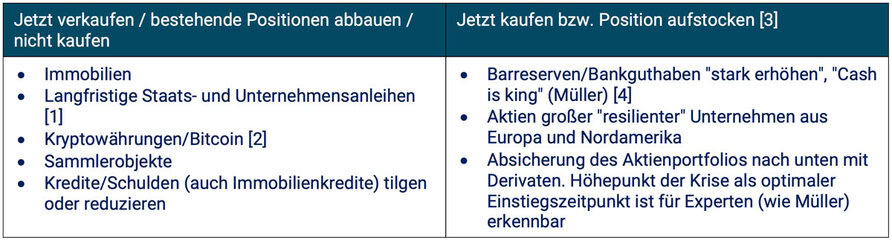

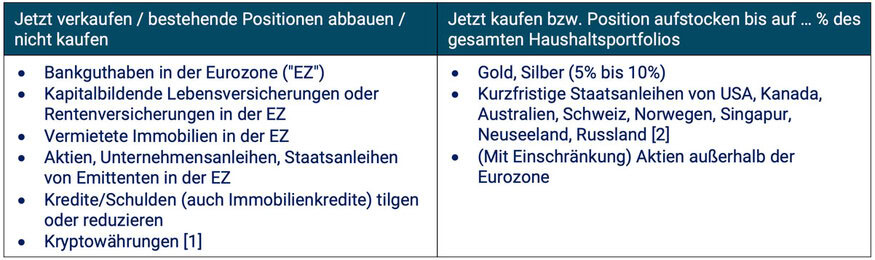

Table 5: What Dirk Müller recommended for destruction

► Information according to Müller: “Powerquake: The world facing the greatest economic crisis of all time”, 2018. ► [1] Müller writes nothing about capital-forming life and pension insurance, although in the classic form these invest primarily in government bonds, which he rejects as direct investment. ► [2] Müller quotes Gerald Hörhan approvingly regarding cryptocurrencies: “I have never experienced a form of investment that has attracted as many weirdos, lunatics, parrots, sleazy profiteers and lunatics as the current cryptocurrencies.” ► [3] Müller does not give any percentage values for the distribution of the asset classes mentioned in this column in the household's overall portfolio. ► [4] Bank balances: Even beyond the state deposit protection of €100 thousand per bank-customer combination.

Among all four turbo-pessimists, Müller's followers, to the extent that they followed him, suffered the greatest investment pain in the form of opportunity costs, as shown in Table 6.

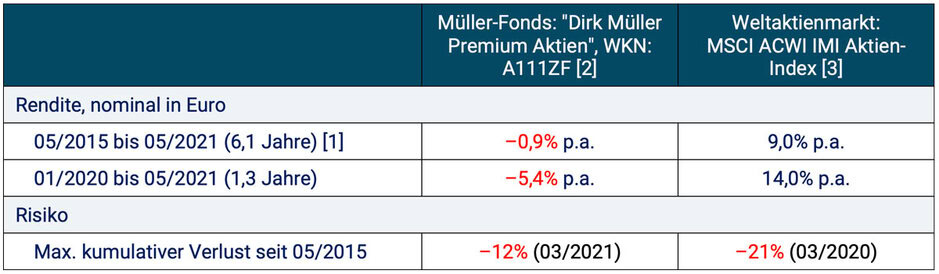

Table 6: Return and risk of the Dirk Müller investment fund compared to the general stock market

► [1] May 2015 was the launch date of the Müller fund. ► [2] The fund return shown does not include the fund's initial issue fee of 4%. ► [3] Index return less an ETF expense ratio of 0.4% p.a.

Anyone who invested in the Müller fund six years ago is now worth less than when they started. With a global equity ETF, however, this investor would have cumulatively increased his wealth by almost 70%. These enormous opportunity costs do not include those that Müller caused through his perma-pessimistic warnings to investors long before the launch of his own fund (May 2015). So he said, for example: B. in one of his books in March 2009: “Stocks and equity funds simply don’t belong in your portfolio in these uncertain times.” The cumulative return of the global stock market in the 36 months from this forecast was +82% (MSCI-ACWI-IMI index in euros).

On the positive side, investors in Müller's fund have had to endure a significantly smaller maximum drawdown over the past six years than a global equity ETF investor. Everyone has to decide for themselves whether this compensates for the gigantic under-return in a pure stock fund.

Prophet of Doom 4: Markus Krall

We now come to the last member of the foursome, Markus Krall. He stands out in that he provides more detailed justification for his gloomy predictions, particularly his “domino theory” of a systemic banking crisis in the Eurozone. But Krall has not published an academic study on his theory or a mathematical model that others could verify.

Krall differs from the three other ultra-observants in a second point. He is the only one of the four who does not run his own fund. Krall has been managing director of Degussa Goldhandel GmbH in Munich since September 2019; he was previously a management consultant.

As far as we know, Krall only appeared in public with pessimistic predictions with the publication of his book “The Draghi Crash” in mid-2017 – significantly later than the other UPs. In the book he predicted a systemic banking crisis in Europe and a collapse of the Eurozone by the end of 2020 or early 2021.

Table 7: What Markus Krall recommends for the downfall

► Information according to Markus Krall: “When black swans have babies”, 2018. ► [1] In 2021, after the publication of his two books analyzed here, Krall began to take a less negative, merely “skeptical” position on Bitcoin. ► [2] In his two books analyzed here, Krall does not give any percentage values for short-term government bonds for their share in the overall portfolio, but from the overall context one can conclude that the figure is well over 50%, especially since he specifically mentions “5% to 10%” for precious metals.

As we will see in more detail in the direct comparison below in Table 9, Krall's investment recommendations differ greatly from those of the three other UPs. Krall relies 90% on what, in our consulting experience, those who consider his theses plausible instinctively detest most: short-term government bonds with high credit ratings. This aversion, which is widespread among wealthy people, is directed not only at euro-denominated bonds, but also at short-term government bonds in general. Short-term government bonds with high credit ratings – in economic theory the “risk-free asset” – have had essentially the same “zero yield” in all Western currencies in recent years. (We know that this ultimately applies to the last 120 years here shown.)

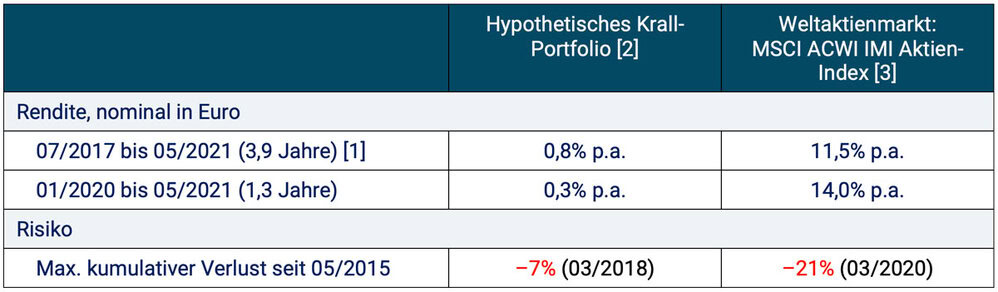

In Table 8 we calculate the return of a hypothetical Krall portfolio. We derived the structure of this portfolio to the best of our knowledge and belief from the information in the two books analyzed here. The exact composition of the portfolio is given in the table footnotes.

Table 8: Return and risk of a Krall portfolio compared to the general stock market

► [1] July 2017 was the publication date of the book “Draghi-Crash” by Krall. ► [2] Hypothetical portfolio structured by Gerd Kommer Invest GmbH according to the two Krall books used here as follows: 30% one-month US government bonds, 30% one-month Swiss government bonds, 30% one-month Australian government bonds, 5% gold, 5% silver. All returns in euros. ► [3] Index return less an ETF expense ratio of 0.4% p.a.

In the almost four years since the publication of the Krall book on which this is based, those who followed Krall's investment recommendations have had to accept significant opportunity costs. Krall would probably justify this by saying that the excess return on his portfolio will come at the latest when the “Draghi crash” takes place, which he had announced would begin at the end of 2020. Afterwards, according to Krall, investors should buy “the then beaten-down” assets such as stocks and real estate in the Eurozone at a bargain price after a loss in value of up to 90% and thus achieve attractive returns in the long term.

The overall investment recommendations of the four prophets of doom

In their extreme pessimism about Germany, the Eurozone and the similar monetary policy in all Western countries since around 2008 (including in countries like Switzerland, Norway, Canada or Australia), the four UPs are on the same line. However, their investment recommendations for the “systemic crisis” they predict differ considerably in some key aspects, as Table 9 illustrates. For someone who is convinced by the largely consistent problem diagnoses of the four UPs, this could represent a credibility and implementation problem.

Table 9: Where and how the four prophets of doom give divergent or contradictory recommendations

► [1] Bank deposits: Also within the state deposit insurance of €100 thousand per bank-customer combination. ► [2] Müller: “China is the largest bubble in the history of humanity.” ► [3] Müller: “Bitcoin is a pyramid scheme.” ► [4] See note on Krall’s position on Bitcoin in Table 7.

After all, there are also some important investment pieces of advice on which the four doomsayers agree, namely

- the high importance of diversification (dispersion) in general and international diversification in particular,

- the reduction of real estate exposure (volume of an investment) in Germany and the Eurozone, especially for rented residential properties,

- the usefulness of adding physical gold,

- the earliest possible repayment of all debts of a household, as far as financially and contractually possible. (The economic rationale of repaying loans is justified by everyone with the risk of deflation in the future. In deflation, borrowers/debtors suffer particularly badly.)

From our consulting practice in recent years, we conclude that only a tiny fraction of all private households that fundamentally sympathize with the Armageddon worldview of our four persistent pessimists would be prepared to consistently implement their investment recommendations. Let's illustrate this using Markus Krall as an example.

According to him, a private investor would have to sell or significantly reduce all Eurozone assets by now (actually as early as 2017, when his first book was published) - with the potential exception of the owner-occupied home and his own company, if any. (With regard to these two assets, Krall remains rather vague, although the logic of his general argument actually suggests that they should be sold.)

What does this mean specifically for a consistent Krall supporter? It means the liquidation of bank balances at banks in the Eurozone (including within the state deposit insurance), the termination of all life insurance and private pension insurance, the sale of all securities and fund investments from issuers in the Eurozone and the repayment of all debts, as far as contractually possible. The budget should then transform the funds released in this way into around 10% physical gold and silver and around 90% into short-term government bonds from some non-Euro countries in local currency - both with a depository abroad. Near the climax of the system crash, he should then sell his short-term non-Euro government bonds, which have remained stable in value, back into stocks, real estate and others at the then dramatically lower Eurozone asset prices Tangible assets redeploy.

Conclusion

In this article we have shown that those who have followed the four prophets of doom - Marc Friedrich, Max Otte, Dirk Müller and Markus Krall - in recent years have had to suffer painful opportunity costs. Such opportunity costs are the general underlying problem of “crash timing” and ultra-pessimistic investment approaches, which ultimately lead to investors staying on the sidelines of the markets for years and therefore too long. This basic problem makes the presented approaches unattractive in the long term.

We have also shown that the investment recommendations of the Pessimist Quartet are “unconventional” and are unlikely to be implemented by wealthy private investors who partially or fully agree with these worldviews – one could sarcastically see this as the proverbial difference between theory and practice.

Thirdly, we have shown that the investment recommendations across the four prophets of doom differ in significant parts or even contradict each other, although the derivation and description of the causes of the expected collapse for the four are largely the same.

Selected freely accessible Internet publications on the predominantly false forecasts of Friedrich, Otte, Müller, Krall and other crash prophets

- Gurol, Julia (2014): “The Errors of the Crash Prophets”; Wirtschaftswoche, August 28, 2014

- Johnston, Michael (2015): “A visual history of market crash predictions”; Website of a US asset manager, July 16, 2015

- Mahler, Armin (2019): “Is the biggest crash of all time really imminent?”; Spiegel Online, November 22, 2019

- Bartz, Tim/Mahler, Armin (2019): “Crash or nonsense – best-selling author versus economics professor. A debate”; Spiegel Online, December 20, 2019

- Beutler, Thomas (2019): “Beware of the crash prophets”; Financial blogger website, December 25, 2019

- Neumann, Markus (2020): “Matthias Weik & Marc Friedrich: False forecasts pave their way”; Financial blogger website, January 8, 2020

- Neumann, Markus (2020): “The theses of the crash prophets Weik and Friedrich checked”; Focus Money Online, January 10, 2020

- Maiwerk financial partner (2020): “Friedrich & Weik fact check – How much value do their forecasts have?” YouTube video from a financial advisor, May 16, 2020

- Lorenzen, Jannes (2020): “A Reckoning: The Failure of the Stock Market Crash Prophets”; Financial blogger website, May 29, 2020

- Financial flow (2020): “How do the funds of crash prophets like Dirk Müller & Co. perform?” Finance portal, YouTube video July 12, 2020

- Muschak, Thomas (2020): “What to think of crash prophets”; Financial Advisor Website, September 24, 2020

- Atypical-Still (without author) (2020): “The Crash Prophet Crush Saga: The (Biggest) Crash of Crash Prophethood (of All Time!)”; financial blogger website; October 14, 2020

- Atypical-Still (without author) (2020): “The Crash Prophet Crush Saga: the Wall, the Nail and the Pudding”; Financial blogger website, October 16, 2020 (continuation of the first article above)

- Esnaashari, Hamed (2020): “Please pick up Mr. Dax Dirk Müller & Markus Krall from the crash paradise – the stock rally will start soon”; Financial portal Wallstreet-Online.de, November 15, 2020

- Lorenzen, Jannes (2020): “Crash prophets: 13 criticisms of how crash predictions harm your investments”; Financial blogger website, December 23, 2020

- TIM – This interests me (without author) (2020): “Failed stock market crash predictions”; Unspecified website, 2020 (exact publication date missing)