From Gerd Kommer and Alexander Weis

Note: This blog post was extensively updated in March 2024.

Investing in stocks with particularly high or particularly stable dividends is an investment style that is at least 60 years old and has probably become more popular in the last 20 years or so. [1] “Dividend investing” or “generating passive income with dividend stocks” is extremely common among both passive and actively oriented private investors – in Anglo-Saxon countries it is also referred to as income investing or cash flow investing.

Free of fantasies, but full of facts: The L&G Gerd Kommer Multifactor Equity UCITS ETF. Find out more >

The financial advice book market, the financial media and YouTube are overflowing with publications on dividend investing. Four examples out of thousands:

- “Stocks for passive income: Using the dividend strategy to achieve financial freedom” (financial guide book)

- “Extra salary with stock ETFs” (YouTube video)

- "These 5 dividend stocks offset inflation! €9,000 dividend for me" (YouTube video)

- “Incredibly high payouts – these DAX stocks are the real dividend stars” (online edition of the daily newspaper Die Welt)

Contrary to such publications, whose titles are obviously motivated by shameless clickbait, dividend-focused investing overall has more disadvantages than advantages. It tends to produce worse returns than comparable non-dividend investing with roughly identical risk. We show this using historical data in Table 1.

The table compares the returns of an actively managed dividend-oriented fund (column 2), a passive dividend index in which you can invest via ETF (column 3), the well-known passive MSCI World Index without a particular dividend focus (column 4) and an index that tracks stocks that make distributions primarily via share buybacks rather than via dividends (column 5). [2]

Table 1: Illustration of the non-existent dividend yield premium from June 2005 to January 2024 - nominal returns in euros

► Without costs and taxes (DWS fund including ongoing costs, without issuing surcharge). ► Reason for choosing the starting point: The MSCI World Buyback Yield Index only goes back to June 2005. ► The DWS Top Dividend is the largest actively managed dividend-focused fund in Germany marketed to private investors. ► Volatility: Annualized standard deviation of monthly returns. ► Simplified Sharpe Ratio: Ø monthly returns ÷ volatility. ► German inflation was 2.2% p.a. over the entire period ► Data: MSCI, fondsprofessional.de.

The data speaks for itself. Dividend or income investing – whether active or passive – does not have a return advantage, but rather a disadvantage. When it comes to risk, there is only a moderate advantage. The risk-weighted return (Sharpe Ratio) of high dividend investing is noticeably worse than normal investing without a dividend focus.

These numbers would not look fundamentally different if, for example, B. looked at the last ten years or the last 50 years. In the immediate past five years, the general performance of high-dividend stocks has been particularly poor by comparison.

It is important that the analysis is not based on a single country (e.g. the USA or Germany), a single active dividend fund or a short period of time (e.g. five years), but on the world stock market and periods of at least 15 years.

How should dividend investing be viewed from the perspective of theory, i.e. from the perspective of factual logic and science?

The Modigliani-Miller Dividend Irrelevance Theorem

In 1961, two American finance professors, Franco Modigliani and Merton Miller, published a groundbreaking paper in which they showed that in a world without taxes and transaction costs, dividend policy [3] of a company has no influence on its corporate value and its change, i.e. the stock return (Modigliani/Miller 1961). The two researchers later received the Nobel Prize in Economics for this work, among other things. Therefore, from the perspective of two super-smart economists, high dividends per se are not crucial in the context of maximizing returns. In other words: it is not the procedural manner in which the company's profits are passed on to the owners that is crucial, but rather how high the profit is. The validity of the so-called “Modigliani-Miller Dividend Irrelevance Theorem” is sometimes questioned on the grounds that it does not take taxes and transaction costs into account. However, such criticism is based on shaky grounds, as dividends are a form of cash distribution that are tax-free for companies and shareholders combined in most jurisdictions is more expensive than their two alternatives, namely distributions through share buybacks or the waiver of distributions, i.e. equivalent price increases (the latter two have the same effect on returns in financial mathematics). In Germany too, price gains at the level of private investors are de facto taxed lower than dividends because of the present value effect from their “downstream” taxation (see here).

Dividend yields are only part of the total return

Stock returns are – this is banal – the sum of price gains and dividend yields. For a purely rational investor, it is irrelevant how high the relative shares of these two components are in the total return. A central element of the Dividend fallacy [4] There is a misconception that a dividend in a “good” company does not reduce the share price by the same amount at the time of distribution (which is of course the case); You get something “for free” with the “dividend pearls” – obviously wishful thinking. Dividends are payments to the shareholder from his own pocket, the profits of the company he owns. The higher the dividend yield, the lower the price return.

Nevertheless, for many private investors, a total return of - let's say 10% - feels more valuable if it consists of 7% price gains and 3% dividends than a total return of only 10% price gains. Likewise, many private investors perceive a withdrawal in the form of a dividend as “somehow” less of a reduction in their portfolio assets than a withdrawal of the same amount via the sale of shares.

A rational investor seeks to maximize the total return, not the smaller part of it, the dividend yield. Furthermore: If this rational investor wants to withdraw liquidity from his portfolio, he is indifferent between the two alternatives of selling shares (realizing price gains) or receiving dividends. Both are economically “withdrawals”.

Dividend stocks are no help in “preserving substance”

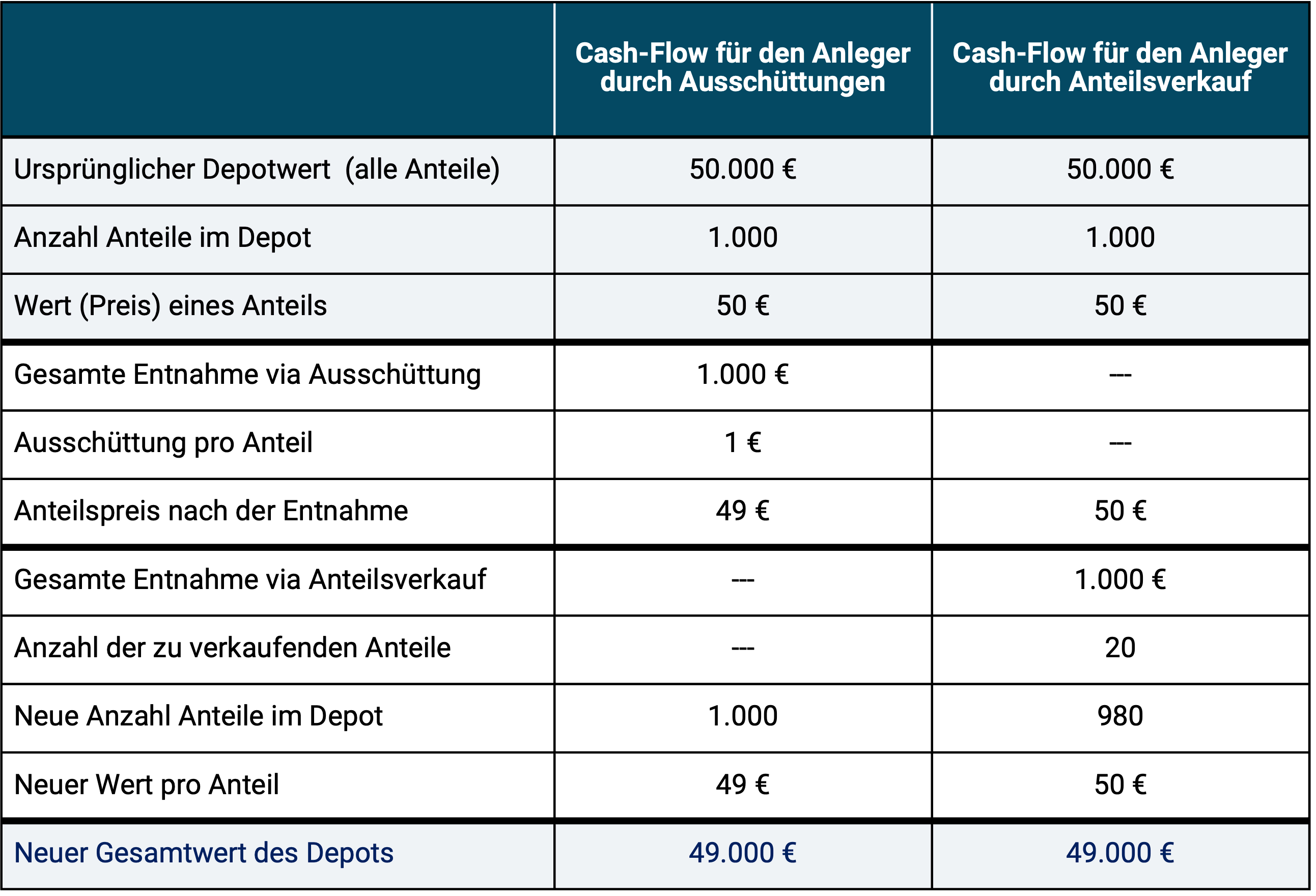

Many private investors still somehow view withdrawals from portfolios through dividends as less negative than withdrawals through share sales. This is also a variant of the Dividend Fallacy. The error works like this: If the investor - in order to take cash from his portfolio - continually sells shares (which could be shares in a stock portfolio or fund shares in a fund portfolio), he will "at some point" have nothing left because he will then have sold all of the shares. With withdrawals via dividends, however, this risk does not exist because no “capital”, no “substance” (i.e. no shares) is being sold. The following comparative example calculation illustrates that this gut feeling assessment is wrong (Table 2).

Table 2: Irrelevance for the investor's portfolio value between withdrawals via dividends (distributions) and withdrawals via share sales

What does the sample calculation in Table 2 show? It's up to the investor whether he generates his cash flow (withdrawals) through distributions or sales of shares. The “loss of substance” or “loss of capital” in the sense of the change in the total portfolio value – and that is all that matters – is exactly the same size in both constellations: in our example, 1,000 euros. The new portfolio value resulting after the withdrawal is of course also the same: 49,000 euros. For the sake of completeness: Over time, entire If the company value (or portfolio value at the investor level) is distributed to the shareholder (or all shareholders at the level of the entire company or fund) in the form of dividends (distributions), the investor would still have nominal shares in the portfolio at some point, but these would have an equivalent value of zero and therefore here too, just as if all the shares were sold over time, there would be “nothing left”.

Dividend yields used to be much higher – so what?

Occasionally, admirers of the “dividend nobility” [5] proclaims the great importance of dividends for stock returns by pointing out that historically around half of the stock market's total return comes from dividends. Foregoing these dividends would be tantamount to foregoing the total return – another error in reasoning. As mentioned, the total return of the stock market (or an individual stock) results from the sum of price gains and dividends. If dividends are lower, capital gains will be correspondingly higher. Both – capital gains and dividends – come from the same source, the company’s profits. Dividend yields were, on average, significantly higher in the first half of the 20th century than after 1950, while the opposite was true for total returns - and these are the only ones that matter. High dividend yields do not equate to high total returns.

In this context, it may be interesting to note that share buybacks, the main technical alternative to dividends, were not legalized in most countries until the 1980s and 90s. Many age-old myths surrounding dividends would be less common today if share buybacks had been around for as long as dividends (Damodaran 2014).

Dividend investing with individual stocks

Whether you want stocks with a high dividend yield and It is highly doubtful that investors can reliably identify attractive total returns through stock picking. We know from literally thousands of academic studies since about 1960 that active investing, including stock picking, only produces under-returns with any real reliability.

Even the professionals of a “leading” fund company in this country only have an unimpressive record of stock picking for dividend stocks - see the weak returns of the DWS fund included in Table 1, which pursues a dividend-focused strategy. (The balance sheet of the second and third largest actively managed German equity funds with a dividend focus – Deka Dividendstrategie/WKN DK2CDS and Fidelity Global Dividend Fund/WKN A1JSY0 – is similarly bad.)

Some of the world's most profitable stocks of the past 40 years have never paid a dividend at all or only started paying dividends after decades of phenomenal stock returns fueled solely by price gains. These include Apple, Microsoft, Amazon, Alphabet (Google), Meta (Facebook), Nvidia, Tesla and Warren Buffet's legendary company Berkshire Hathaway (without a dividend for over 50 years). It would also be easy to find stocks that had high dividend yields in individual years or over long periods of time while at the same time having particularly poor overall returns.

And investors who rely on distributions?

My colleague Alexander Weis and I have explained in two blog posts that distributing funds or individual stocks generally do not even bring advantages for those households that need ongoing inflows from their portfolio to cover living costs - here and here.

The only real advantage of dividend investing

At least one good thing can be said about dividend investing: Dividend investing seems to be what motivates some private investors to buy stocks and to be patient with these stocks. As long as this purely psychological advantage exists, you can perhaps “nod off” dividend investing despite everything. Motto: “Dividend shares are second choice, but still better than no shares at all.”

Conclusion

Historically, dividend investing has tended to produce worse returns than comparable investing without a dividend focus. Dividend stocks also offer significant advantages when it comes to risk.

Science and factual logic see more disadvantages than advantages in dividend-oriented investing.

However, the lack of systematic benefits of dividend investing will not stop the financial industry, the financial media and an army of finfluencers from further encouraging private investors in the false belief that dividend investing has real, objective, lasting benefits in order to sell expensive products or increase circulation and click-through rates.

If you want to understand the facts in detail in the scientific literature, we recommend the study by Hartzmark/Solomon (2019).

Endnotes

[1] There may not have been any dividend-oriented investing before around 1950, because dividend yields existed until around 1950 general and permanent were higher than the interest rates on low-risk government bonds and considerably higher than the returns on interest-bearing bank deposits. Because the vast majority of stocks back then had high dividend yields, no one would have dreamed of selecting stocks specifically based on a high forecast dividend yield.

[2] Various ETFs are offered on buyback indices in the German market.

[3] Dividend policy refers to the amount of the dividend or dividend yield and its changes over time.

[4] Fallacy = mistake or mistake in thinking. Comprehensive information about the various manifestations of the Hartzmark/Solomon Dividend Fallacy 2019.

[5] In Anglo-Saxon financial jargon, stocks with high or particularly consistent dividends are considered somewhat childish Dividend Aristocrats designated.

literature

Damodaran, Aswath (2014): “Stock buybacks: They are big, they are back and they scare some people!” Internet reference: here

Hartzmark, Samuel/Solomon, David (2019): “The Dividend Disconnect”; in: The Journal of Finance; 74; No. 5; Oct. 2019

Huang, Mia (2022): "Should You Chase Dividend Stocks to Combat Inflation and Rate Hikes? April 5, 2022; Dimensional Fund Advsiors; Internet reference: here

Kanuri, Srinidhi/Malhotra, Davinder/McLeod, Robert (2017): “Performance of Dividend Exchange-Traded Funds During Bull and Bear Markets”; In: The Journal of Index Investing, Summer 2017

McCullough, Adam (2017): “The Perils of Funds that Narrowly Target High-Yielding Stocks”; (Morningstar; August 2017; Internet source: here

Modigliani, Franco/Miller, Merton (1961): “Dividend policy, growth, and the valuation of shares”; In: The Journal of Business; 34; 1961

Röhl, Christian (2023): “When dividends become a fetish – high dividend stocks as a zero-sum game”; Dec 2023; Post on LinkedIn: here

Snaker, Todd/Kesidis, Savas (2017): “An analysis of Dividend Oriented Equity Strategies”; Vanguard Research; Internet reference: here

Swedroe, Larry (2023): "The Evidence Against Favoring Dividend-Paying Stocks; March 13, 2023; Advisor Perspectives, here