<<< This blog post is also available as a YouTube video. >>>

From Gerd Kommer and Alexander Weis

This post was updated in March 2026.

Many private investor households use their liquid assets to permanently cover part of their living costs. These investors are in the “asset use phase” or “asset consumption phase” and are faced with the fundamental question of how they should structure their investment portfolio so that it produces a regular payout in the desired amount as reliably as possible - a kind of self-generated pension.

This task is not trivial, because different investments produce different combinations of current cash income (dividends for stocks, interest for interest-bearing investments, net rental income for real estate [1]) on the one hand and price or value appreciation gains on the other.

In this context, in our financial advisory practice we often encounter a common error among private investors: they systematically value withdrawals that come from current income (e.g. dividends, interest, rental income) differently than withdrawals that occur through share sales, i.e. sales of individual securities or fund shares.

These investors perceive consuming or “withdrawing” distributions as somehow a smaller loss of wealth than consuming/withdrawing the same amount of proceeds from share sales. Some investors justify this with a difference between “substance” or “capital” on the one hand and “current income” or distributions on the other. Consuming current income or distributions is less harmful than using up substance or capital. Anyone who only uses current income/distributions is not using up any capital.

In this blog post we show that, from an economic and rational perspective, there is no difference between consumption/withdrawals of current income (distributions) and consumption/withdrawals from share sales. Anyone who views these two withdrawal routes as fundamentally different economically tends to make worse decisions for their assets. If withdrawals from share sales are the same amount as withdrawals from distributions, the economic effect (e.g. “no consumption of capital”) is exactly the same. This blog post will show that unequivocally.

In order to understand the logic behind our argument, a conceptual clarification is first necessary, which has already been suggested above. Below we use the general term “withdrawals” for two different types of payment flows or “cash flows” from the financial portfolio or depot to the investor:

- “A withdrawals”: For the purposes of this article, these are withdrawals from a portfolio (or several portfolios) that are financed from current income (interest and dividends) from distributions.

- “V withdrawals”: This refers to withdrawals that are financed through share sales, i.e. from the sale of individual securities or fund shares. Sales of shares are sometimes described as “sales of assets” or “sales of capital”.

Below we present seven arguments that prove that the different assessments of the two types of withdrawals in terms of their wealth-reducing effect by private investors are based more on opinions than facts. Taken together, these seven arguments will lead us to the essential conclusion:

The preference for withdrawals from current income over withdrawals from share sales has no real economic basis. From a purely rational perspective, there is no reason to prefer one type of extraction over the other. Anyone who does so is making the mistake of elevating an irrelevant decision criterion into a relevant criterion. This can result in economic disadvantages. Withdrawals via share sales actually have a significant advantage over withdrawals from distributions, which we will describe below.

Argument 1: There is no significant difference in tax burden between A withdrawals and V withdrawals

From a tax perspective, there is no or no significant difference between A withdrawals (current income) and V withdrawals (sales of shares) when investing in private assets in most countries, including Germany. The tax burden of the investor making A withdrawals is the same as that of the investor making V withdrawals.

Argument 2: When it comes to transaction costs, there is no material difference between A withdrawals and V withdrawals

From a transaction cost perspective (costs for purchases and sales of securities or fund shares), A withdrawals have advantages on the surface. Anyone who analyzes in more detail, as we did in our blog post “Distributing vs. accumulating funds", will recognize that in practice this advantage either does not exist at all in most relevant investor constellations or is negligibly small. The oft-heard argument "Distributions do not cause transaction costs, but share sales do" falls short in this context. We explained why this is the case in the blog post in question. Anyone who believes or claims that A withdrawals have transaction cost advantages should/must read our blog post.

Argument 3: Investments with a high distribution yield are not fundamentally more attractive than those with a low distribution yield

Investments should – this is banal – on the basis of their so-called expected In totalreturn and their expected risk. The total return for most investments consists of a distribution return and an appreciation return. The principle applies without exception: the higher the distribution yield, the lower the appreciation yield. For example, a high dividend yield on a stock comes at the exact expense of its return on appreciation; The same applies to bonds and real estate.

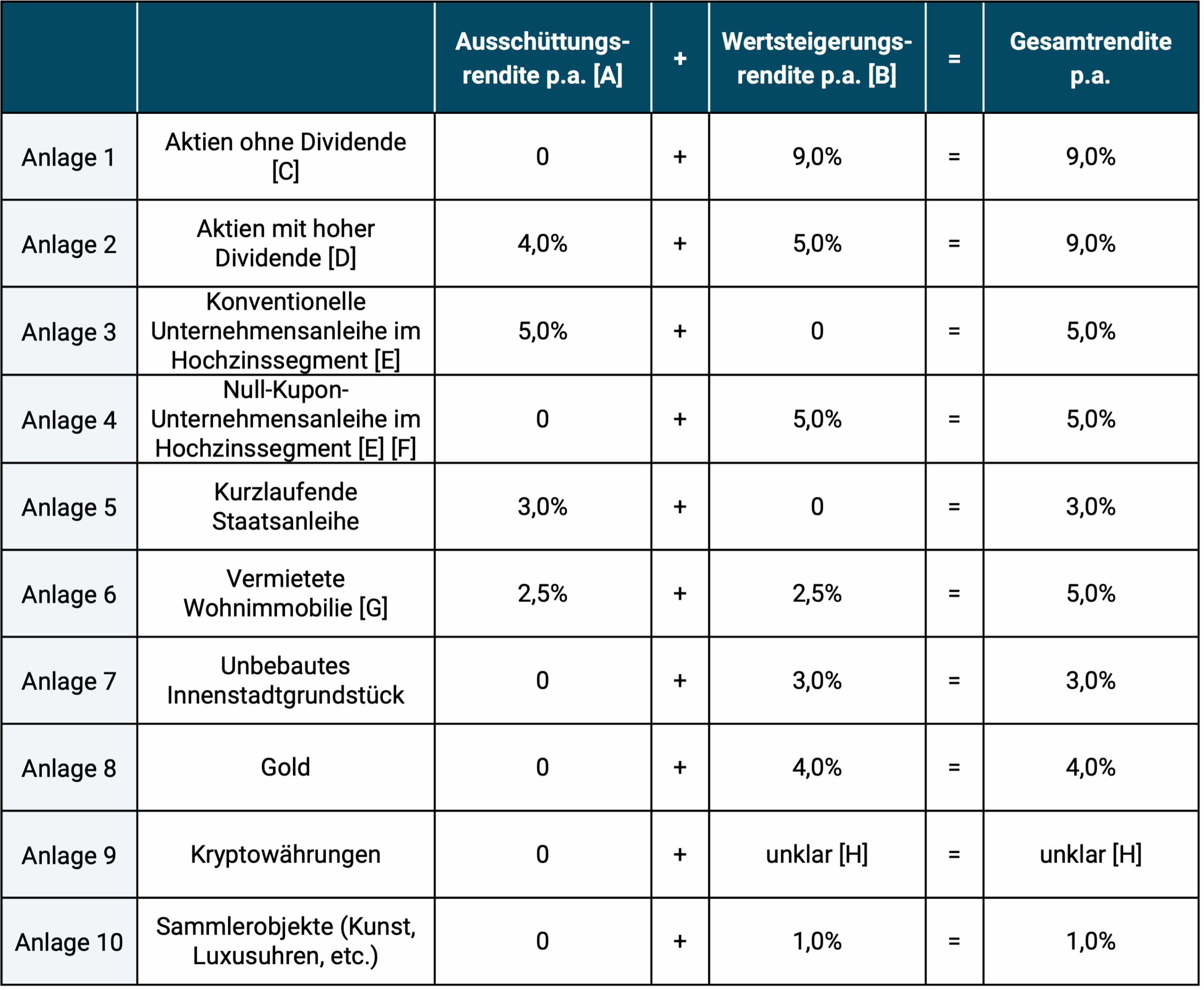

The following table illustrates the connection between distribution yield and capital appreciation return using numerical examples for various asset classes and financial products. So a high distribution yield is not a gift, not a free lunch. It reduces in full the otherwise possible return on investment. Apparent exceptions to this principle are usually confusion between “optically visible” processes everyone economic processes. Ergo: Only the total return counts. This basic economic principle cannot be emphasized strongly enough.

Many financial investments – even attractive ones – have no distribution yield at all. Four examples of this are included in the table below. For some types of bonds, investors can choose between variants with a high, medium or low distribution yield (coupon yield). [2] However, these purely formal deviations have no systematic effect on the expected one In totalreturn. If things were different, one of the most fundamental laws of the capital market would no longer apply: “There is no free lunch.”

Table: Conceptual comparison of investments, each representing different combinations of (nominal) distribution yield and appreciation yield

► The values in the total return column are our assumptions, which we have roughly derived from long-term history. ► [A] Distribution yield: For a share this is the dividend, for a bond it is the “coupon yield” and for a property it is the net rental yield. ► [B] Appreciation return: For a share or bond these are the price increases, for a property these are the price increases. The values in the appreciation yield column are our assumptions, which are derived from the historical appreciation returns for the respective investment funds. ► These nominal (not inflation-adjusted) return figures are purely fictitious. ► [C] Example: Warren Buffet's stock (Berkshire Hathaway Inc.). It has not paid a dividend for over 50 years, yet produced a total return that is well above average. ► [D] Example: The Munich Re share has had a dividend yield of around 4% p.a. in recent years. Only around 60% of all listed companies worldwide pay a dividend in a given year. A dividend yield of over 2 to 3 percent is considered high. ► [E] For bonds, the expected total return until maturity is called the “current yield”.► [F] Example: A zero coupon bond from a bank in southern Europe. ► [G] For real estate, the distribution yield corresponds to the net rental yield. This is the gross rental yield minus maintenance costs and insurance. ► [H] The oldest of over 20,000 cryptocurrencies is only around 16 years old (Bitcoin). For this and other reasons, no reliable statement can be made about the future expected returns from cryptocurrencies.

Anyone who compares the ten investments listed in the table, each with their different combination of distribution yield and appreciation return, will have to conclude that preferring investments solely or primarily because of their distribution yield, rather than their total return and other important properties such as risk and liquidity, does not seem very logical.

Argument 4: A company's dividend policy has no systematic influence on the total return of its shares

As we wrote in our blog post “Dividend strategies: facts and fantasies" explained, the two American finance professors Franco Modigliani and Merton Miller received the Nobel Prize in Economics, among other things, for showing that dividend policy (the amount and timing of dividends, i.e. payouts) has no systematic influence on the company's value and thus the shareholder return. It is irrelevant in advance whether you buy a stock with a high or low payout yield. Because this is the case, so-called "income funds" or dividend funds - stock funds that are based on Concentrating on stocks with high dividend yields - have no return benefit and are at least harmful if they have unnecessarily high costs. We have also analyzed other misunderstandings among professional and private investors around the topic of “aiming for high dividends” in the blog post mentioned. In the scientific literature, these errors in thinking are summarized under the collective term “dividend fallacy”. To summarize in one sentence: The total returns of high-dividend stocks tend to be lower in the long term than those of the market as a whole.

Argument 5: Consuming distributions is no less harmful than consuming “substance” or “capital”

A particularly widespread misconception within the dividend fallacy also appears in the same form with bonds and fund shares (including ETF shares). This mistake goes like this: If the investor continually sells shares (stocks in a stock portfolio, bonds in a bond portfolio, or fund shares in a fund portfolio) in order to take cash out of his portfolio, he will “eventually” have nothing left because he will have sold all the shares by then. On the other hand, this risk does not exist if only dividends or interest are withdrawn, because no substance or capital is being sold here. Here is a concrete example of this error in thinking, the comment under a YouTube video about an accumulating (i.e. not distributing) stock investment fund:

"I'm not interested in products without dividends. I don't want to sell any of my assets during the withdrawal phase, but rather live exclusively from the dividends. A farmer doesn't sell his field when he's old either."

Since we have already discussed the fundamental reasoning and calculation errors in this argument in our blog post on the topic mentioned above Dividend strategies have refuted it with numbers, we don't need to do it again at this point. For a given investment, how quickly a given asset is used up does not depend on whether the withdrawals are made in the form of distributions or in the form of share sales, but rather how high the withdrawals are overall and over time relative to the assets, i.e. on the level of the percentage “withdrawal rate”. Of course, if one only withdraws its distributions, an asset can, under reasonable assumptions, never become zero, but if withdrawals via share sales were exactly the same amount, the result would be exactly the same — here, too, the asset would never become zero. the same. As long as there are no differences between A withdrawal or V withdrawal with regard to taxes or transaction costs for a given withdrawal level (which is actually not the case - see above), a purely rational investor will be indifferent as to whether a given withdrawal is generated from current income or from share sales. The only withdrawal policy that actually increases the long-term survival probability of an asset is called “take less.”

Argument 6: The distinction between earnings and substance is often artificial and has no economic content

The distinction between “substance” or “capital” on the one hand and “current income” on the other is in many cases artificial: For example, many companies with traditionally high dividend yields pay these dividends from equity reserves in years of poor corporate profits or even take on additional debt because of them. Here, a current income, a distribution for the investor, is paid from “substance” at the company level. But it gets even more colorful: If a company pays a dividend in year 1 that is lower than its annual profit, as is well known, profit retention takes place at the company level. So far so good. Now let's assume that in year 2 the company's profits shrink to zero and this time the company pays a dividend equal to the unpaid profit from year 1. Does the year 2 dividend now come from "substance" or does it come from "current income"? There is no clear answer to this question. Ultimately, practically all “capital”, i.e. all “substance”, comes from previously undistributed income - the usual black and white distinction between the two concepts often seems naive.

Argument 7: In most cases, a sustainable withdrawal strategy cannot be achieved without selling shares

Without the willingness to make asset sales (sales of shares) in some years, an annual withdrawal rate of more than three and a half percent of the portfolio value is not consistently possible in typical constellations and is therefore not sustainable (see our blog post “Avoid capital consumption: not a desirable investor goal”). And even this low withdrawal rate will probably require an equity ratio of 50% or more. Due to risk reasons, only a few of the 42 million households in Germany would (unfortunately still) be able to afford an equity quota of this level in German-speaking countries. If this statement seems unreasonably pessimistic, you probably fall into the large group of private investors who overestimate the returns of all asset classes after taxes, costs and inflation and who have distortedly positive memories of their own past and future returns - a phenomenon confirmed by research. (On the question of how to estimate sustainable withdrawal rates – i.e. withdrawal rates that have a sufficiently high probability of not leading to premature “bankruptcy” – we have a blog post entitled “Monte Carlo simulation as a forecasting method" published.)

Conclusion

Consciously ignoring the difference between A withdrawals (distributions) and V withdrawals (sales of shares) not only sharpens investment thinking, it also has enormous practical benefits: With share sales, a household that is dependent on withdrawals from its portfolio can precisely and conveniently control the amount of these withdrawals over time and is not exposed to the uncertainties of one-off or chronic distribution returns that are too low, occasionally too high and always fluctuating.

So it's time for private investors to do what economics did decades ago, namely to cut off the old idea that A withdrawals are generally preferable to V withdrawals. In fact, with a specified one-off or regular withdrawal amount, it is almost always economically irrelevant whether it is financed from distributions or from share sales - in the vast majority of situations there are no material differences in terms of tax or transaction costs. The fact that you can permanently avoid capital consumption by limiting your withdrawals to A withdrawals (distributions), but not with V withdrawals, is a false, manipulative argument. If the withdrawal amount or the withdrawal rate is identical in both cases, the final wealth effect is also identical.

If significant differences are nevertheless claimed between A withdrawals and V withdrawals, then they are based almost without exception on errors in thought that have been refuted in the scientific literature for decades, on the confusion of the optically visible surface with the economically fundamental effects - more generally on incomplete thinking or on merely perceived differences. Anyone who sets aside the useless or harmful distinction between A and V withdrawals discussed here will have one less unnecessary worry and will act more financially advantageous in some balancing situations.

Endnotes

[1] Net rent = gross rent minus expenses to be borne by the landlord, e.g. B. Property tax and building insurance costs.

[2] We recommend our blog post to readers who are looking for a short but detailed introduction to the bonds investment class “Bonds as an asset class: From the basics to specialist knowledge” (January 2024). It also explains why the level of the distribution yield (coupon yield) of a bond is ultimately irrelevant to its total return (current yield).