From Gerd Kommer and Jonas Schweizer

This blog post was updated in September 2024.

Economic knowledge helps with wealth creation – a trivial statement. However, we will show below that this seemingly self-evident truth does not apply to the very type of economic knowledge that a typical private investor spends the most time and attention acquiring.

The following figure shows the five main subcategories of “economic knowledge” from an investor’s perspective.

Figure: The five areas of “economic knowledge” that are essential for investors

At a quick glance, the five sub-areas or categories of economic knowledge can be characterized as follows:

(A) Investment theory: Financial knowledge that can be learned from a technically oriented financial guide book, asset management textbook or other sources - for example, you can find answers to the questions "What is a share?" (simple level) or “What is return order risk in a withdrawal scenario?” (intermediate level) or “What is the concept of duration in bonds?” (higher level). Simple or advanced financial mathematics and statistics also belong to this field.

(B) Investment practice: Knowledge and experience of financial services providers, their various conflicts of interest, business interests, fee structures and specific risks. This includes banks, insurance companies, fund companies, online brokers, financial advisors, asset managers, insurance brokers, real estate agents, credit brokers, precious metal traders, crypto exchanges, “finfluencers” and others. Tax knowledge also falls into the area of investment practice.

(C) Investment psychology: Knowledge about the typical reasoning errors and cognitive biases that we are all subject to to varying degrees when making our financial decisions. The research discipline of Behavioral Finance – a connection between empirical psychology and financial economics – has provided significant insights into this over the last 30 years.

(D) History of financial and capital markets: The history of the financial and capital markets over the past 200 years, including knowledge of long-term historical asset class returns and risks. The typical financial advice book only provides superficial information and what little is often distorted or incorrect. Most private investors hardly concern themselves with this category of economic knowledge, even though it is particularly helpful for successful investing.

(E) Economic policy: Knowledge of economic policy, economics, socio-political and geopolitical issues. Investors primarily obtain this information from the business section of newspapers, from business magazines, economic policy television programs and from non-fiction books. More and more also from social media sources and from finfluencers who inform (and disinform) about economic policy issues.

From the perspective of a private investor who invests on their own, it can be said that he or she can never actually have enough knowledge and expertise in the first four of these areas of knowledge. The fifth sub-area (economic policy and economics, sub-area E), however, is insignificant for sustainable success when investing in capital market products or real estate. Paradoxically, the majority of private investors devote more time to acquiring knowledge in this sub-area than all four other sub-areas combined - probably because it has more entertainment value and is less technical.

An example of an economic policy newspaper article: “Wall Street expert Koch: America’s economy will soon lose considerable momentum” (Handelsblatt, June 2022). Firstly, in the short and medium term – as we will show in detail below – there is no exploitable connection for private investors between observable real economic phenomena and the capital markets. Second, such forecasts are often wrong, just as Koch's complacent forecast was wrong. Another example of a non-fiction book: “Ice Age in the Global Economy: The Most Sensible Strategies for Saving Our Assets” by the economist Daniel Stelter from 2016. From 2016 to today, the capital markets have had disproportionately high returns. An example of a YouTube video: "Markus Krall: The crash is coming in 2021! Printing money has replaced thinking" from the YT channel of the finfluencer Marc Friedrich in November 2020. As is well known, there was no crash in 2021. At best, there was a moderate crash in the stock and bond markets in 2022 - probably due to the “interest rate turnaround” at that time. But this too was quickly made up for in the stock market. In the interest rate market it was simply a healthy return to more normal conditions.

Why is economic policy and economic information largely useless for investors or – if you make investment decisions based on it – often even very harmful?

Because with such information there is the comparatively weakest connection between a given piece of information and what happens in the capital markets in the following twelve months or 20 years. To the extent that there is a connection at all, it is often the opposite of what our gut feeling and the disseminators of this information would have us believe.

We will illustrate this below using eleven “false economics theses”, [1] which, unspoken or expressed, underlie the widespread idea that economic or economic policy issues have some kind of causal effect that can be exploited by private investors in the markets for stocks, bonds, precious metals, raw materials, cryptos or financial products based on these asset classes. And because that is the case, it pays to be well informed about the economy and the current economic policy discussion.

False economics thesis 1

"High economic growth in a country tends to produce high stock market returns; there is a systematic relationship between a country's economic growth and its stock market returns."

→ The facts: No, statistically speaking and in a way that investors can use, no such relationship exists. The correlation between national economic growth in a year and national stock market returns in the same year or the year before or after is zero. Countries with above-average economic growth can have lower stock market returns over 30 years than countries with below-average growth. That's why the idea that you have to invest more in areas where experts (or yourself) expect high economic growth based on the past and present is useless or even disadvantageous as an investment strategy. An example: Over the last 30 years, no country in the world has had higher economic growth than China. Nevertheless, the Chinese stock market has delivered one of the weakest returns of the approximately 45 industrialized and emerging countries over these three decades, worse than those of Germany and Japan. In 2022 we will have a look at why there is generally no connection between economic growth and stock returns that investors can exploit YouTube video explained. If you want to know more, please refer to the scientific studies by Cornell 2010 and Ritter 2012.

False economics thesis 2

"Stock markets of countries with high government debt tend to perform worse than the stock markets of countries with low government debt. Government debt is bad for capital markets."

→ The facts: This claim, which is often made explicitly or implicitly by business journalists and social media “experts,” cannot be substantiated with empirical data. If you look at the current 47 industrialized and emerging countries according to the MSCI definition and measure the correlation between their national debt relative to gross domestic product on the one hand and their stock market returns in the previous three, five or ten years on the other hand, the result is correlation values just below zero. In other words, there is no statistical evidence of a connection. Let's take one of these 47 countries, the USA: As of September 2022, the country had the fifth highest national debt ratio in the group of 47 and at the same time the highest stock market return in the past ten years. Government debt or accumulating government debt does not have a systematic impact on stock returns, even if this contradicts our intuition. This would probably also be the case if one measured in the other direction of the timeline (national debt versus future, rather than past, stock market returns).

False economics thesis 3

“Fiscally conservative and soundly governed countries have higher long-term stock returns than fiscally unsound governed countries.”

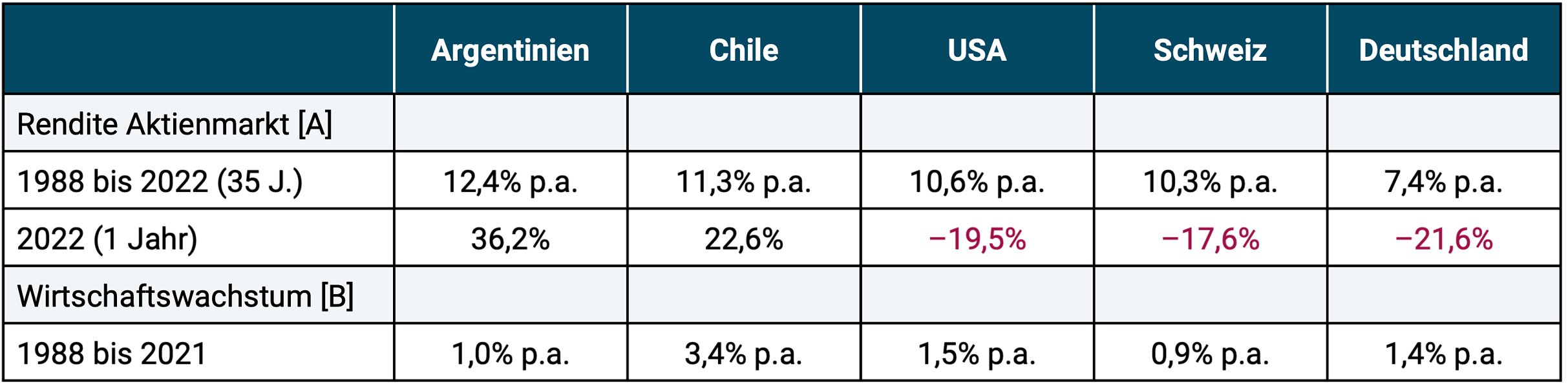

→ The facts: Sorry, no. Let's just let the numbers do the talking by comparing the stock market returns of four economically soundly governed states with those of one fiscally and monetary policy particularly unsound governed state: Argentina.

Argentina recorded three sovereign bankruptcies (four if you count one a few years earlier) during the 35-year period considered in the table below, compared to zero for the four other countries. [2]

Table 1: Comparison of five countries' stock market returns from 1988 to 2022 - nominal returns in USD

► [A] Stock market: Returns from the national MSCI Standard Index. ► [B] Economic growth: Real GDP growth per capita in local currency. ► Without deducting costs and taxes. ► Longest common time series available for all five countries. ► When it comes to risk-adjusted returns (simplified Sharpe ratio), Argentina is on a par with Chile and better than Germany. ► Data: MSCI, World Bank.

False economics thesis 4

“Smart investors exit the stock market when a recession or significant economic downturn is predicted.”

→ The facts: No, smart investors don't do that. First of all, it should be noted that forecasts by experts (bankers, economists, central bank representatives, business journalists, YouTubers) about the start and end of an economic downturn (recession) are notoriously unreliable, i.e. wrong in half of all cases or even more often. Anyone who follows such forecasts will, in the majority of cases, switch from the stock market into cash too early or too late. Even if economic key figures, so-called “leading indicators” are used to forecast approaching recessions (instead of classic “expert forecasts”), the result is no better. The forecasts are not very reliable, i.e. sometimes right, sometimes wrong. But even if these forecasts were more reliable than they actually are, following them would mostly be harmful: for the USA, it has been shown that in more than half of all recessions there between 1926 and 2020 (94 years), stock returns exceeded the money market interest rate (overnight interest rate) (Lee 2022). This most likely has to do with the fact that (a) the stock market has long since priced in corresponding information when forecasts based on it are published and (b) the stock market, as a “structurally forward-looking social mechanism,” is more likely to predict the real economy than the real economy predicts the stock market.

False economics thesis 5

"Rising interest rates are bad for stock returns. A smart stock investor exits the market after interest rates have risen significantly or are predicted to rise further."

→ The facts: Stock returns have historically been lower on average in phases of rising interest rates than in phases of falling interest rates, but still higher than the returns on risk-free money market investments (Simpson Hendrix/Roberts 2022). What makes matters worse – as we already mentioned with regard to the false economics thesis 4 – is that the profitable use of interest rate change forecasts first requires sufficiently reliable forecasts. However, this accuracy is simply not the case.

False economics thesis 6

"Strategies in which investment decisions are based on the determined or forecast changes in certain macroeconomic indicators and variables in the short and medium-term future produce attractive returns. These include, for example, the development of interest rates (mentioned above), the yield curve, [3] high yield spreads, [4] the development of the money supply, the development of inflation, the development of exchange rates, the development of corporate profits, the change in the order situation of companies, the change in the unemployment rate, the confidence of purchasing managers in surveys, consumer confidence and a hodgepodge of other alleged or actual “economic indicators”. The latter term must be put in quotation marks because (a) not a single economic indicator really reliably predicts the short or medium-term development of the economy and (b) the stock markets rarely develop parallel to the real economic situation in the short and medium term anyway.

→ The facts: None. Overall, such strategies do not outperform and probably even underperform a comparable passive buy-and-hold strategy. In Table 2 we show this as an example Macro hedge fund index, these are hedge funds with the active market timing approach described in the thesis (in industry jargon “macro timing”).

Table 2: Comparison of a Macro Hedge Fund Index to a Passive Stock-Bond ETF Portfolio from 2008 to 2022 (15 Years) - Nominal Returns in USD

► Without deducting taxes. ► [A] Volatility = annualized standard deviation of monthly returns. ► Costs: For hedge funds, the ongoing costs are already taken into account. For the 20/80 stock-bond portfolio, you would still have to deduct ongoing costs of approx. 0.1% p.a. (stocks MSCI ACWI IMI index, bonds: 5-year US government bonds). ► Longest common time series available for the two strategies. ► Data: HFRI, MSCI, Dimensional Fund Advisors.

The managers of most conventional, actively managed investment funds (mutual funds) also base their investment decisions largely on forecasts of macroeconomic variables. The fact that actively managed investment funds (stocks, bonds) underperform corresponding passive ETFs in typically 60% to 100% of all cases over periods of 3+ years has been proven and shown so often that we don't need to repeat it again here.

Our valued investment book author and financial market researcher William Bernstein writes about the widespread assumption that poor macroeconomic conditions are associated with poor stock market returns and vice versa: "It's natural for people to assume that when the economy is in good shape, future stock returns will be high, and vice versa. The opposite is true: Market history shows that when there's economic blue sky, future returns are low, and when the economy is on the skids, future returns are high." [5]

False economics thesis 7

“The government bonds of countries whose currencies chronically depreciate against other “hard currencies” produce worse returns than the bonds of hard currency countries (whose currencies persistently appreciate).”

→ The facts: This intuitively obvious assumption is also wrong at least so often that its investment implementation causes more harm than good in the long term, as the following table suggests. We compare the government bond yields of one “soft currency” country, Italy and the Italian lira, which existed until the end of 1998, with the government bonds of two hard currency countries. The lira depreciated sharply against both hard currencies in the 14 years from 1985 to 1998 (after which the euro was introduced). Nevertheless, Italian government bonds delivered better returns than German or Swiss equivalents.

Table 3: Comparison of returns on government bonds: Italy, Germany, Switzerland from Jan. 1985 to Dec. 1998 (14 years) from the perspective of a German private investor - nominal returns in DM

► Without costs and taxes. ► [A] For all three countries: “FTSE Government [Country] Bond Index 1-5 Years”. ► Longest data series available together. ► Data: Dimensional Fund Advisors, Swiss National Bank, Banca d’Italia.

A similar situation applies with regard to the stock markets of weak currency countries. In the long run, their returns - measured in hard currency - are as high as or higher than the stock market returns of hard currency countries (Dimson/Marsh/Staunton 2006).

False economics thesis 8

“Countries with a high government spending ratio (the ratio of annual government spending to gross domestic product, also short State quota called) have worse stock market returns than countries with a low government ratio.”

→ The facts: No, that is not the case. The correlation of the 2022 government spending ratio and national stock market returns in the ten years to the end of 2022 was negative 0.2 for a random sample of 25 developed and emerging markets. This means that the countries with a high government spending ratio tend to be marginal in the decade in question higher, did not show lower stock market returns than countries with a low ratio.

False economics thesis 9

“If, in an important election, a more free-market candidate (or such party) wins over the less free-market candidate (or such party), this will have a positive effect on the stock market in the short or medium term.”

→ The facts: For the USA, it has been proven many times that this seemingly plausible regular table theory is not empirically correct. Nevertheless, it is being spread epidemically by journalists, finfluencers, conservative politicians and other “experts” in the run-up to important elections in practically every country. In the United States, national stock market returns over the last 250 years have been slightly lower on average under free-market presidents (typically from the Republican Party) than under more left-wing, interventionist presidents (typically from the Democratic Party). Reason: An open economy is far too complex a system for such grossly simplified, naive “theories” to work reliably. Shortly before the federal elections in September 2021, we addressed this topic in a short article (here). Although a coalition won that has been pursuing an anti-market economic policy to this day (September 2024), the German and even more so the global stock market has risen significantly since then. The “zero interest rate problem” in Germany that existed until the end of 2021 has disappeared.

False economics thesis 10

“The gradual loss of purchasing power of currencies (USD, Euro, Swiss Franc, British Pound, Yen, etc.) is detrimental to our wealth creation.”

→ The facts: Have over periods of 50+ years all Currencies that exist today (including the Swiss franc and the Norwegian krone), if they have existed for that long, have lost over 50% of their consumer goods purchasing power. To illustrate: an average inflation rate of 2.0% p.a. reduces the purchasing power of a currency by 87% over a period of 100 years. Is this harmful to the affected population? Probably not. In any case, it is not harmful as long as household incomes rise on average in the long term at a rate that is above inflation. And that is exactly what has been the case in all Western countries for the last 30, 50 or 100 years. The vast majority of economists employed at universities (i.e. economists without a conflict of interest) consider moderate inflation rates of around 2% p.a. not only not to be harmful, but even to be beneficial. For reasons of space, we will not explain the reasons for this here. However, in this context we have another Blog post showed that under the so-called "gold standard", which was the norm for currencies worldwide in the 19th century and the first third of the 20th century, the average inflation rate was significantly lower than later under paper money currencies ("FIAT currencies"), but economic growth and thus the increase in household incomes was higher under the modern FIAT money standard than under the gold standard. Moderate inflation rates are therefore by no means negative, but are very likely useful.

False economics thesis 11

“A high level of technical progress and innovation in an individual company, industry or country leads to above-average returns for that segment of the stock market.”

→ The facts:This deterministic cause-and-effect relationship most likely does not exist for periods of six months to around 20 years in the future and therefore cannot be exploited reliably enough by investors. Why doesn't he exist? Mainly because it is estimated that over 90% of the social and/or economic benefits of a commercially viable innovation do not accrue to the originator of that innovation, but to others or the rest of the economy. We have this using the example of artificial intelligence here shown. We know that tech stocks generally do not outperform in the long term here and here proven.

We have now seen that basing investment decisions on economic policy and macroeconomic variables or their expected changes is unlikely to achieve anything on balance and in many cases, probably in the majority of cases, is even detrimental to returns. That’s why the successful fund manager Peter Lynch once said “If you spend 13 minutes a year on economics, you have wasted ten minutes”. He wanted to express that typical economic considerations are simply not suitable as a basis for investment decisions. Nevertheless, the media reporting aimed at private investors and the marketing statements from financial service providers on the subject of investing are often based on such analyzes and arguments. Because journalists and finfluencers are under pressure to constantly report “new things,” no matter how wrong or unproven they are, and of course because for most of them “circulation” or click rates are more important than reporting pure facts, telling the truth or simply keeping their mouths shut.

What is economics knowledge useful for then?

Economics knowledge is important for us as citizens. In our role as voters, we cannot have enough economic expertise because it helps us to better and more quickly identify politicians and parties that cause economic and political damage and then to sort them out on the ballot. In general, economic policy knowledge advances our understanding of the world in general and the economy in particular.

Conclusion

Of the five sub-areas of economic knowledge described here, only four are sufficiently causally linked to long-term investment success: (A) investment theory, (B) investment practice, (C) investment psychology and (D) capital market history.

On the other hand, a lot of knowledge in sub-area E - economic policy/economics - will tend to have no impact on long-term investment success for investors and - if investments are frequently followed by the "certainties", myths and errors widespread in this field - will have a negative impact on balance.

If you are a private investor and want to increase your probability of success in wealth creation and asset protection, we recommend that you concentrate your limited time on areas A to D and only consume and implement “news” on economic policy in your role as a citizen and voter.

Endnotes

[1] Economics = economics.

[2] “State bankruptcy” means that the capital service on government bonds was no longer provided as contractually agreed.

[3] Normal versus inverted yield curve.

[4] For corporate bonds: The difference between the current yield of investment grade bonds and high yield bonds for a given duration and currency.

[5] "It is only natural for people to assume that stock returns will be high in the future when the economy is doing well and vice versa. The opposite is true: market history shows that future returns are low when the economy is doing well and high when the economy is misfiring."

literature

Dimson, Elroy/Marsh, Paul/Staunton, Mike (2006): “ABN AMRO Global Investment Returns Yearbook 2006”; ABN AMRO; Unpublished; Amsterdam 2006

Cornell, Bradford (2010) “Economic Growth and Equity Investing.” In: Financial Analysts Journal; 66; No. 1; January/February 2010

Lee, Marlena (2022): “Three Crucial Lessons for Weathering the Stock Market’s Storm”; Working Paper; Dimensional Fund Advisors; June 17, 2022; Internet reference: Here

Ritter, Jay: (2012): “Is Economic Growth Good for Investors?” In: Journal of Applied Corporate Finance; 2012; 24; No. 3; 2012

Simpson Hendrix, Kaitlin/Roberts, Trey (2022): “How Stocks Respond to Hikes in Fed Funds Rate”; Working Paper; Dimensional Fund Advisors; May 5, 2022; Internet reference: Here