From Gerd Kommer and Marla Bergemann

Anyone who deals with the old, always interesting investment question of whether and how it is possible to systematically achieve returns that are above the market average - to beat the market - will inevitably come across the topic at some point University Endowment Funds bump. [1] Endowment funds are foundation assets of private American universities that invest their funds in the capital market. With the income generated, the endowments finance that part of the operating costs of the respective university that cannot be covered by tuition fees, research funds and government funding.

The endowment funds come from alumni donations and non-withdrawn income. The endowments of the particularly well-known, long-established US private universities are among the largest private investors in the world. Combined, the assets of the approximately 710 endowment funds of American universities amounted to over $820 billion in 2021. Most of the really large endowments have existed for over 100 years.

The best-known endowment in the investment community is that of the elite Yale University. Its recently deceased Chief Investment Officer, David Swensen, is considered the inventor of the modern endowment investment model. Swensen also wrote two investment books that were highly respected in the industry. [2]

We will show below that the special return track records of the supposed elite investors are actually not far off. The excess returns from endowment funds are a thing of the past, if they ever existed at all. Nevertheless, the idea of excess returns from Yale and the endowments of other elite universities still exists in the imaginations of financial journalists and investment bloggers. This is what publications like these show:

"Rich with the Yale formula: How the masterminds invest - Renowned US universities manage assets worth billions and achieve top returns. What private investors can learn from Yale, Harvard and Co" (Article title on the portal finance.net, 31.03.2018)

“Invest like Yale & Co: How to achieve double-digit returns” (Article title from the Swiss Trade newspaper, 31.12.2019)

“Yale: This is how the elites invest – and YOU can simply imitate it” (YouTube video from Mission Money, 22.01.2020)

First, let's look at the characteristics of the endowment investment model, the investment approach coined by David Swensen according to the prevailing mythology, which is in fact typical of most university endowments. This approach is characterized by three main characteristics:

(a) A particularly active investment management, i.e. the conscious avoidance of broad diversification and buy-and-hold.

(b) A high proportion of investments in illiquid, “alternative assets” such as private equity (PE), hedge funds, real estate, raw materials. In investment jargon, “alternative” stands for alternative to “conventional” assets and asset classes, i.e. primarily stocks and bonds. In the last 13 years or so, the share of alternative assets in the 12 largest endowments was almost 60% (Chambers et al. 2020). [3] The idea behind this high ratio is that higher returns can be achieved with alternative assets than with public assets (stocks, bonds) and that these private assets have a low correlation to stocks and bonds. The low correlation should help to mitigate the volatility (intensity of fluctuations) of the overall portfolio.

(c) A comparatively small proportion of low-risk bonds for public, non-profit investors.

In addition, endowments are free from the various regulatory restrictions that apply to normal investment funds (“mutual funds” including ETFs), e.g. B. the prohibitions on short selling, debt financing (leverage) or investments in unlisted securities above a 10% limit.

Let's come to the question of returns and thus, in the first step, data availability. Since endowment funds, as private institutions, are not required to publish their returns, there is no easily accessible database in the public domain. We must therefore limit ourselves to the data in scientific studies and other specialist publications.

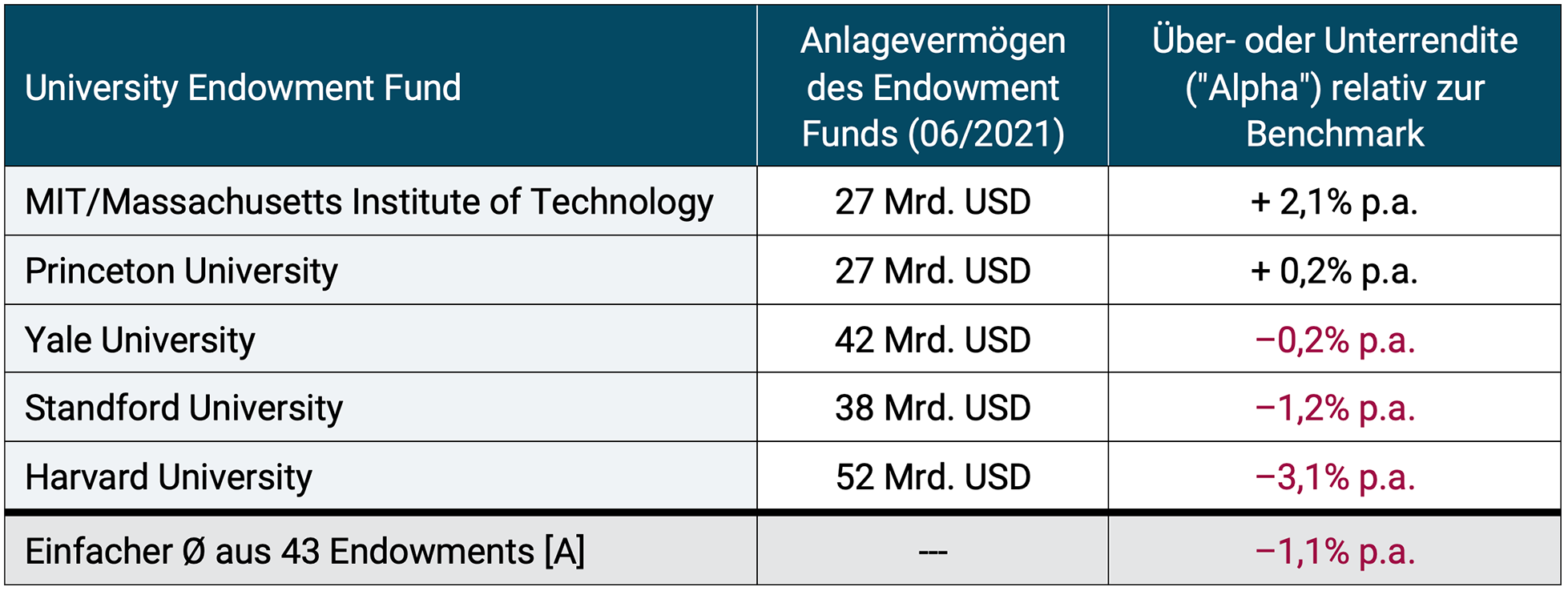

In the table below, we look at the relative investment track record of the five largest endowments in the recent past, as well as the average for the 43 largest endowments.

Table: Excess or under-returns of the five largest university endowment funds in the USA and the average of the 43 largest endowment funds, relative to a passive benchmark - period 07/2008 to 06/2019 (11 years)

► Source: Ennis 2020, www.insidehighered.com. ► [A] Median value for the 43 largest university endowment funds in the USA. ► Endowments' fiscal years typically end on June 30 of the year. ► The benchmark is a passive portfolio consisting of a US equity index, a non-US equity index and a US bond index (details in Ennis 2020). ► The internal costs (e.g. personnel costs) of the investment management endowments are not included in these figures - see explanations further down in the text. ► The starting point 07/2008 for this period was chosen by Ennis because the high weighting of alternative assets in endowment funds became an overall disadvantage to returns at the start of the Great Financial Crisis in mid-2008, while it had an advantage in the 10 to 15 years before. The aim of his evaluations is, among other things, to identify the negative return contribution of alternative assets.

The table shows the figures for only eleven years in the recent past and does not contain any data on the risk level of the portfolios. From a scientific perspective, the questions arise as to what the returns look like over longer-term periods and what influence taking risk into account would have.

In short, considering longer time periods and incorporating risk would not change the overall picture suggested by the table. This emerges from the scientific studies mentioned at the end of this blog post and other studies.

Here's another highlight from these studies: Ennis (2020) shows that the average endowment underperformed in both absolute and risk-adjusted terms from 1974 to 2020 (47 years). Based on different research methods and sometimes different data sets, Hammond comes to almost identical results for the period from 1962 to 2019 (58 years) and Dahiya/Yermack for the period 2009 to 2017 (nine years) (Hammond 2020, Dahiya/Yermack 2021). In the Hammond study, the average endowment produced a return of 8.1% per annum over those 58 years, versus 9.1% for a simple passive 60/40 benchmark. The 60/40 benchmark therefore produced a 71% higher final asset value.

When assessing these numbers, the following aspects are worth considering:

Above we mentioned the high allocation to alternative assets as a special feature of the endowment fund model. This characteristic only emerged in the 1980s, initially at a moderate level. From the mid-1990s onwards, the percentage of alternative assets at large endowments increased year on year to around 60% around 2015. It has remained there ever since. Alternative assets had their “golden age” in terms of returns between 1994 and the beginning of the Great Financial Crisis in 2008 - a phase in which they outperformed the stock and bond markets overall. Since 2009, however, this picture has largely been reversed. This is certainly true in relation to Hedge funds, raw materials and property, less for P.E. (To be clear, PE has also underperformed the broader stock market in the 20 years ending 2021.) In other words, alternative assets have, on balance, hurt endowment returns since 2009.

The fact that alternative assets have lower volatility than stocks is rumored by the sellers of these assets and many investors believe this claim. The fact is that the volatilities reported externally by hedge funds, private equity funds and real estate funds are smoothed out and trivialize the actual fluctuations in value and returns. This happens because these funds invest in unlisted assets whose prices and price changes over time they estimate themselves for monthly or quarterly return reporting. The problem is well known and undisputed. The calculated fluctuations in returns of such funds cannot therefore be compared with those of listed portfolios. The contribution to reducing the volatility of illiquid assets to the overall portfolio is in any case partly an illusion (Chandra et al. 2019, 2020).

The figures given in the table, as well as most of the return data that are determined in the scientific studies evaluated here, probably do not take into account all of the endowments' ancillary investment costs, since the endowments generally do not offset the personnel costs and other expenses of their investment departments against the (selectively) published returns. Ennis estimates these costs at 0.8% to 1% per annum. In this respect, the reported results may even be biased in favor of the endowments.

Harvard, the world's largest endowment, not only represented the red lantern among the five named in the table during the 11-year period shown, Harvard has been delivering meager returns for much longer. In the 20 years ending June 30, 2021, the performance of the endowment was both below that of an S&P 500 stock ETF on a buy-and-hold basis and below that of a passive 60/40 portfolio consisting of an S&P 500 ETF and an ETF on medium-term US corporate bonds (Hulbert 2020, 2021). In the 2021 fiscal year (as of June 2021), Harvard achieved an investment return of 33.6% and Yale 40.2% (both excluding endowment staff costs). With an ETF on the American S&P 500 index you would have earned 40.6%.

How should all of this be assessed overall? For this we quote from the expert studies mentioned in the bibliography:

"The special investment expertise of top universities is now just a myth. These returns could easily be achieved through passive investing." (Dahiya/Yermack 2020) [4]

“In the 12 years since the 2008 financial crisis, investment returns from U.S. endowments have been dismal, particularly the performance of endowments at top universities such as Harvard, Stanford and Yale.” (Edesses 2021) [5]

“Alternative asset classes have failed to provide diversification benefits and have had an adverse impact on endowment performance.” (Swedroe 2020) [6]

Now that we have seen that endowments as a group are underperforming and that the Yale model is now damaged or perhaps broken, the question remains as to why the perception of endowments' particularly attractive returns is still prevalent in the media and among the investing community.

This is probably due to a combination of the following reasons: (a) Older investors selectively remember the significant outperformance that several large endowments experienced temporarily in the years up to the end of 2008 and which was widely reported in the media at the time. (b) The endowments' clever self-marketing. Just look at the corresponding one Yale University website which is sometimes overflowing with embarrassing self-congratulation, but does not contain any benchmarking that objectifies the performance of the endowment management. One should expect serious benchmarking from an institution that claims high scientific and ethical standards, that is tax-exempt and that receives government subsidies. (c) Numerous journalists and bloggers who fall for this clever marketing. However, this trap is perhaps not so surprising when you realize that colorful stories from “guru investors” can always increase click rates and circulation. (d) Many private investors simply want to continue dreaming the old dream of “gurus producing excess returns”.

Conclusion

University Endowment Funds have had their golden age of returns for over a decade. There are some indications that the drought in returns will continue. A sober look at the facts actually rules out still viewing the Yale investment model as a model worth following.

An indirect lesson that can be derived from the data: Overall, alternative assets have been generating worse long-term returns than stocks and bonds for several years. The reason is probably that over the past 20 years a lot of new money has flowed globally into these asset markets with limited absorption capacity.

According to Ennis, given the disappointing return on investment results of their endowments, the governing bodies of these universities must ask themselves whether they are adequately fulfilling their statutory fiduciary duty by tolerating such waste of resources.

Endnotes

[1] Endowment = English for equipment, endowment, foundation.

[2] David Swensen: “Pioneering Portfolio Management: An Unconventional Approach to Institutional Investment”, Free Press, Fully Revised and Updated, 2009, 432 pages (1st edition 2000) and David Swensen: “Unconventional Success: A Fundamental Approach to Personal Investment”; Free Press, 2005, 403 pages.

[3] Alternative assets such as private equity and hedge funds are referred to as alternative “asset classes” by journalists, bloggers and occasionally even specialist authors. That's wrong. If the term asset class is supposed to have any clear, delimiting meaning, then private equity and hedge funds are not asset classes. Rather, they are active investment strategies that... real Invest in asset classes, namely stocks (equity), bonds (debt), cash, exchange rates, real estate, raw materials.

[4] “The investment wisdom of top universities today amounts to little more than a myth, as one could expect to earn these types of returns simply by chance.” (Dahiya/Yermack 2020)

[5] "The investment performance of US endowments in the 12 years since the 2008 financial crisis has been nothing short of abysmal; especially the performance of the endowment funds of top universities, such as Harvard, Stanford, and Yale." (Edesses 2021)

[6] “Alternative asset classes have failed to deliver diversification benefits and have had an adverse effect on endowment performance.” (Swedroe 2020)

Literature/sources

Chambers, David / Elroy Dimson / Charikleia Kaffe (2020): “Seventy-Five Years of Investing for Future Generations”, In: Financial Analysts Journal, 2020, Vol. 76, No. 4

Chandra, Swati / Antti Ilmanen / Nicholas McQuinn (2019): “Demystifying Illiquid Assets: Expected Returns for Private Real Estate”, AQR, White Paper, Internet reference: https://www.aqr.com/Insights/Research/White-Papers/Demystifying-Illiquid-Assets-Expected-Returns-for-Private-Real-Estate

Chandra, Swati / Antti Ilmanen / Nicholas McQuinn (2020): “Demystifying Illiquid Assets: Expected Returns for Private Equity”, In: Journal of Alternative Investments, 2020, Vol. 22, No. 3

Dahiya, Sandeep / David Yermack (2021): “Investment Returns and Distribution Policies of Non-Profit Endowment Funds”, April 27, 2021, NBER Working Paper No 25323, Internet reference: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3291117

Edesess, Michael (2021): “The Spectacular Failure of the Endowment Model”, May 17, 2021, Advisor Perspectives, Internet reference: https://www.advisorperspectives.com/articles/2021/05/17/the-spectacular-failure-of-the-endowment-model

Ennis, Richard (2020): “Institutional Investment Strategy and Manager Choice: A Critique”. In: Journal of Portfolio Management, Fund Manager Selection Issue, 2020, Vol. 46, No. 5

Hammond, Dennis (2020): "A Better Approach to Systematic Outperformance? 58 Years of Endowment Performance", In: Journal of Investing, Vol. 29, No. 5

Hulbert, Mark (2021): “Harvard’s endowment return is worse than the S&P 500 and that should be a lesson for your own portfolio”, Oct. 30, 2021, MarketWatch, Internet reference: https://www.marketwatch.com/story/harvards-endowment-return-is-worse-than-the-s-p-500-and-that-should-be-a-lesson-for-your-own-portfolio-11635138315

Hulbert, Mark (2020): “What the Harvard endowment’s below-average grade can teach you about index funds and your investments”, Oct. 10, 2020, MarketWatch, Internet reference: https://www.marketwatch.com/story/what-the-harvard-endowments-below-average-grade-can-teach-you-about-index-funds-and-your-investments-2020-10-09

Swedroe, Larry (2020): “The Best and the Brightest Fail at Investment Management”, August 11, 2020, Advisor Perspectives, Internet reference: https://www.advisorperspectives.com/articles/2020/08/11/the-best-and-the-brightest-fail-at-investment-management