<<< This blog post is also available as a YouTube video. >>>

From Gerd Kommer and Daniel Ganowski

Ray Dalio is the world's most famous hedge fund manager. His investment firm, Bridgewater Associates, owns the world's largest hedge fund Bridgewater Pure Alpha II (mostly just called Pure Alpha), with assets under management of around $50 billion in this fund and another approximately $50 billion in two other Bridgewater funds.

According to Dalio, no other hedge fund house in the world has made more money for its investors in the last 40 years than Bridgewater. We'll talk more about this dubious marketing statement below.

However, Ray Dalio is not only a celebrity hedge fund manager and seventeen-time billionaire, he has also published several long books on lifestyle, economic policy and national debt in recent years. He also created the “all-weather portfolio,” which is aimed at American do-it-yourself investors.

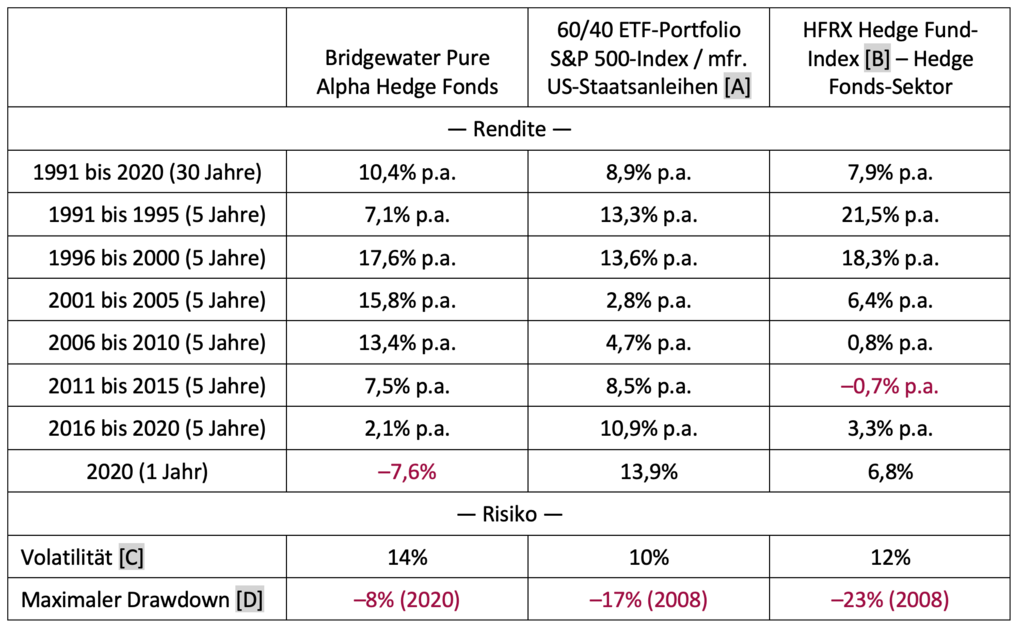

Like most hedge fund firms, Bridgewater does not publish the performance of its three funds. Nevertheless, journalists always manage to find out the returns for individual years or sub-periods. With these individual fragments of data, the annual returns of the Pure Alpha fund since its launch in early 1991 30 years ago can be linked into a continuous data series. We have done this in the table below.

In the table we compare the performance of the Bridgewater Pure Alpha with that of a simple, passive 60/40 portfolio made up of the well-known S&P 500 stock index and medium-term US government bonds. A private investor could have implemented this 60/40 portfolio at low cost using just two ETFs. In addition, we present the return and risk of the entire hedge fund sector in the table using a global hedge fund index.

Also works without paint: The L&G Gerd Kommer Multifactor Equity UCITS ETF. Find out more >

Tabel: Comparing return and risk of Ray Dalio's Bridgewater Pure Alpha fund, a 60/40 stock/bond ETF portfolio, and the general hedge fund sector over the period 1991 to 2020 (30 years)

► All returns in USD, nominal, before taxes. The running costs are already included in all three systems. For the ETF portfolio, ETF-typical costs were deducted from the underlying index returns. ► [A] The bond portion of the ETF portfolio is represented by five-year US government bonds. ► [B] Before 1998 HFRI index, then HFRX index, as no HFRX data is available before 1999. ► [C] Standard deviation of calendar year returns for the entire 30-year period. ► [D] Maximum cumulative loss for the total period of 30 years. Since the calculation is based on annual returns (instead of monthly returns), the values shown tend to be too low. ► Data sources: For Bridgewater, several media articles, e.g. T based on information from Bridgewater itself or on the financial data service Bloomberg. There is a possibility of errors on our part when linking this data from different sources. However, we believe that the probability and magnitude of these errors are negligible. Data source for the HFRX index: Hedge Fund Research (hfr.com). Data source for the indices underlying the ETF portfolio: Dimensional Fund Advisors.

What can be concluded from this table?

The Bridgewater fund has dramatically underperformed the ETF portfolio in the last five years and slightly in the five years before that. Even in the very first five years after the fund was founded in 1991, the hedge fund returned worse than the ETF benchmark. What the table doesn't show: You have to go back 17 long years from 2020 to the beginning of 2004 until the cumulative return of the Dalio fund finally exceeds that of the ETF portfolio for the first time. In other words: Pure Alpha, the largest hedge fund in the world, has been underperforming a simple passive benchmark for over a decade and a half.

The return track record of the entire hedge fund sector is even more disappointing compared to the simple ETF alternative. Although the HFRX hedge fund index was ahead in the first three years starting in 1991, since the beginning of 2004 its performance relative to the index fund alternative has been so consistently pathetic that hedge funds have now cumulatively underperformed the ETF alternative over the last 30 years.

Another footnote: In a 2007 public $1 million bet between Warren Buffett and a hedge fund investment advisor, the S&P 500 index outperformed each of five hedge funds of funds selected by the advisor over the 10-year period from 2008 to 2017 (ours Blog post on this from March 2018).

Interim conclusion: Hedge funds as a group are, without any ifs or buts, an investment disaster.

Hedge funds are called hedge funds because they supposedly never or only rarely produce losses. The reality is different for both Dalio and the hedge fund sector as a whole. If you look at the two risk indicators shown here, the Bridgewater fund provided at best a moderate risk advantage over the ETF portfolio over the entire period (30 years). The hedge fund index – the average of thousands of hedge funds – performs worse than the ETF portfolio on both risk metrics. Not to be forgotten: In this risk comparison, we did not take into account the fact that the volatility figures communicated externally by hedge funds may have been embellished in favor of hedge funds. There is little debate in research that these numbers are systematically smoothed (“return smoothing”) by the fund management (Cassar/Gerakos 2011), because many hedge funds invest in unlisted assets, the prices of which they then have to estimate themselves for the monthly externally reported returns. If you now take into account that hedge funds are subject to no or only limited supervision, it should not be surprising if the fluctuations in these price estimates arrive “somewhat muted” in an Excel file that is sent to investors or to the hedge fund index provider. In our table, we have generously ignored such quality concerns in hedge fund risk numbers.

The catastrophic returns of the hedge fund sector are by no means new, as the table shows, but have been the norm for 15+ years. Back in 2012, the British industry insider Simon Lack published a book in which he demonstrated that, when correctly calculated, hedge funds as a group underperformed short-term US government bonds - or savings account returns - during the two decades before 2012 (Lack 2012).

Anyone who believes that the average doesn't matter as long as at least a minority of the best star hedge funds deliver top returns is making an old investor mistake. This consists of taking the consistency of performance in funds as a given, just because that corresponds to our gut feeling. However, as is so often the case when it comes to historical returns, intuition can be misleading. Sufficiently reliable performance continuity that can actually be exploited by investors does not exist in hedge funds any more than in normal, actively managed investment funds. The data in scientific studies show that last year's “winning funds” are statistically not significantly more likely to be ahead again in the following year than last year's “loser funds” (Guirguis 2020). The Bridgewater fund is no longer an exception given its erratic returns over the last ten years.

What are the reasons why the performance curve of the largest and most famous hedge fund, as well as the entire hedge fund sector, has been pointing so clearly south for years?

The answer could be summarized under the heading “overpopulation”. In 1990 there were around 100 hedge funds worldwide. There are now an estimated 13,000. The global economy, from which the returns of all capital market investors must ultimately come, has grown in real terms by around 2.5% per annum or cumulatively by 110% over these 30 years. The number of hedge funds, on the other hand, shot up by 17% per annum or cumulatively by 11,000%. The “extra-return cake” (in technical jargon, “alpha”) that hedge funds and other active investors are fighting over has only expanded comparatively slowly, while the number of alpha hunters (including hedge funds) has literally exploded. Logical if there is less and less left for the individual.

This applies to hedge funds in general and this also applies to Master Dalio. The numbers in our table leave little doubt.

One might now ask, why has the number of hedge funds increased so enormously in the last few decades? The answer to that is simple: hedge fund managers literally earn their money's worth from their clients' capital. The management fee for a typical hedge fund is between 2.5% and 3% of the investor's assets per year. On this basis, Ray Dalio became a billionaire several times over over a period of a good 40 years. The vast majority of this wealth comes from such fee income.

Curiously, it is precisely this incredible personal wealth of some hedge fund managers that helps them more than anything else to successfully market their investment performance, which in most cases is by no means presentable in the long term. Like that?

Anyone who regularly reads articles about Dalio and other hedge fund manager billionaires in media articles and on the Internet will find a reference to the personal wealth of the respective “superstar manager” in every second publication. The economic success of the hedge fund manager is explicitly or implicitly discussed as an entrepreneur mixed and confused with the little or no long-term success of its financial products for its customers. But one has very little to do with the other.

Some of these media articles, which report on the funds of very rich hedge fund managers such as Ray Dalio, John Paulson, Paul Singer, David Einhorn or others, can hardly be surpassed in terms of embarrassing submissiveness on the part of the journalistic author. In the case of Dalio, this submissive star cult goes so far that journalists repeatedly parrot a clever Dalio marketing slogan in their articles as “facts” or “information” and thus do good and free advertising for him.

For years, Dalio and his employees have regularly announced that Bridgewater has "made more money for its clients than any other hedge fund firm on the planet." First of all, this information cannot be verified by outsiders and can therefore only be classified as advertising from the outset. Furthermore - and more importantly - it cannot of course be concluded from this statement that Bridgewater customers are relative to the investment alternatives available to them - e.g. B. a passive index fund portfolio - would have achieved attractive returns, although it is precisely this conclusion that should and will probably stick with most recipients of the advertising message. Thirdly, despite its clever suggestion, the advertising slogan in no way proves that Bridgewater is one of the world's best fund houses. There are probably more than a dozen, perhaps three dozen fund companies worldwide that have earned more for their customers over the last 20, 30 or 40 years, and in many cases far more than Bridgewater. The three largest index fund companies, BlackRock, Vanguard and State Street, leave Bridgewater in the dust by orders of magnitude in this regard because they (a) manage much larger client funds and (b) produce equally good or better returns. But these are not elite hedge fund companies, but rather normal investment fund companies. Because of this purely technical difference, which is irrelevant here, Dalio can spread the quoted saying further and naive journalists will hastily repeat it in their reporting for a few years to come - as even the venerable British Economist recently did (The Economist, July 30, 2020).

Summary

Dalio and his flagship fund Pure Alpha have been producing meager returns for a decade. Over the last five years, these returns have been particularly poor. Despite his featherweight performance as a fund manager over the past decade, Dalio is still hailed in the media and on the Internet like a reigning heavyweight world champion. This shows that Dalio is making up for his fund manager deficits, which can no longer be hidden, with world-class entrepreneurship and public relations.

The hedge fund sector as a whole has been a returns disaster for 15 years and probably longer. When it comes to hedge funds in general, the financial media seems to be slowly realizing, several years late, that the emperor is naked.

literature

Cassar, Gavin/Joseph Gerakos (2011): “Hedge Funds: Pricing Controls and the Smoothing of Self-Reported Returns”; In: The Review of Financial Studies; 24; 2011; pp. 1698-1734

Guirguis, Michel (2020): “A Multi-Factor Performance Model: Evidence From the Hedge Fund Industry”; June 24, 2020; Internet reference: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3615538

Lack, Simon (2012): "The Hedge Fund Mirage. The Illusion of Big Money and Why It's Too Good to Be True"; Wiley & Sons; 2012; 212 pages