From Gerd Kommer and Robert Wilke

When the stock market has risen sharply over a long period of time - as has most national stock markets in the 16-plus years from mid-2009 to today - some investors ask themselves the question "can stocks rise forever"? The intuitive answer to this seems to be “no”, because actually – according to our gut feeling – neither a natural organism nor a man-made institution can “grow forever”.

Despite this gut feeling, the answer to the question “Can stocks go up forever?” (i.e. have permanently positive returns): Yes, they can. We will show this in this blog post and examine it from the most important perspectives.

Stocks can “rise forever”, i.e. in principle generate positive (inflation-adjusted) returns for an unlimited period of time, if two simple assumptions are made.

Condition 1 for the statement “Yes, stocks can rise forever”

To be true with sufficient certainty, the statement “Yes, stocks can rise forever” must refer to the global stock market, not smaller national markets or individual industries. Individual national stock markets and individual industries may well have negative nominal or real (inflation-adjusted) returns for decades and, in rare cases, even ultimate total losses. [1] The latter took place z. B. from 1917 in the Russian stock market and 1949 in the Chinese stock market - in both cases due to communist revolutions and the associated expropriation of all shareholders without compensation. From mid-1989, when the Japanese bubble began to burst, the Japanese stock market produced a cumulative zero return for around 20 to 30 years, depending on the currency in which you calculate. (In the 30 years before 1989, however, the Japanese stock market had the highest returns of any national stock market in the world.)

The situation is different for the much better diversified global stock market. Since there are around eight billion people on earth who literally need goods and services every day for their very survival and who, for the most part, want to improve their standard of living for their children, there has to be someone who produces these goods and services and produces them in increasing quality. This is what companies in the global economy do. Of these, listed companies (the stock market) only make up a small proportion (less than 0.1%). However, due to their size, they generate around 30% of all global corporate profits and probably a similarly large share of goods and services.

Condition 2 for the statement “Yes, stocks can rise forever”

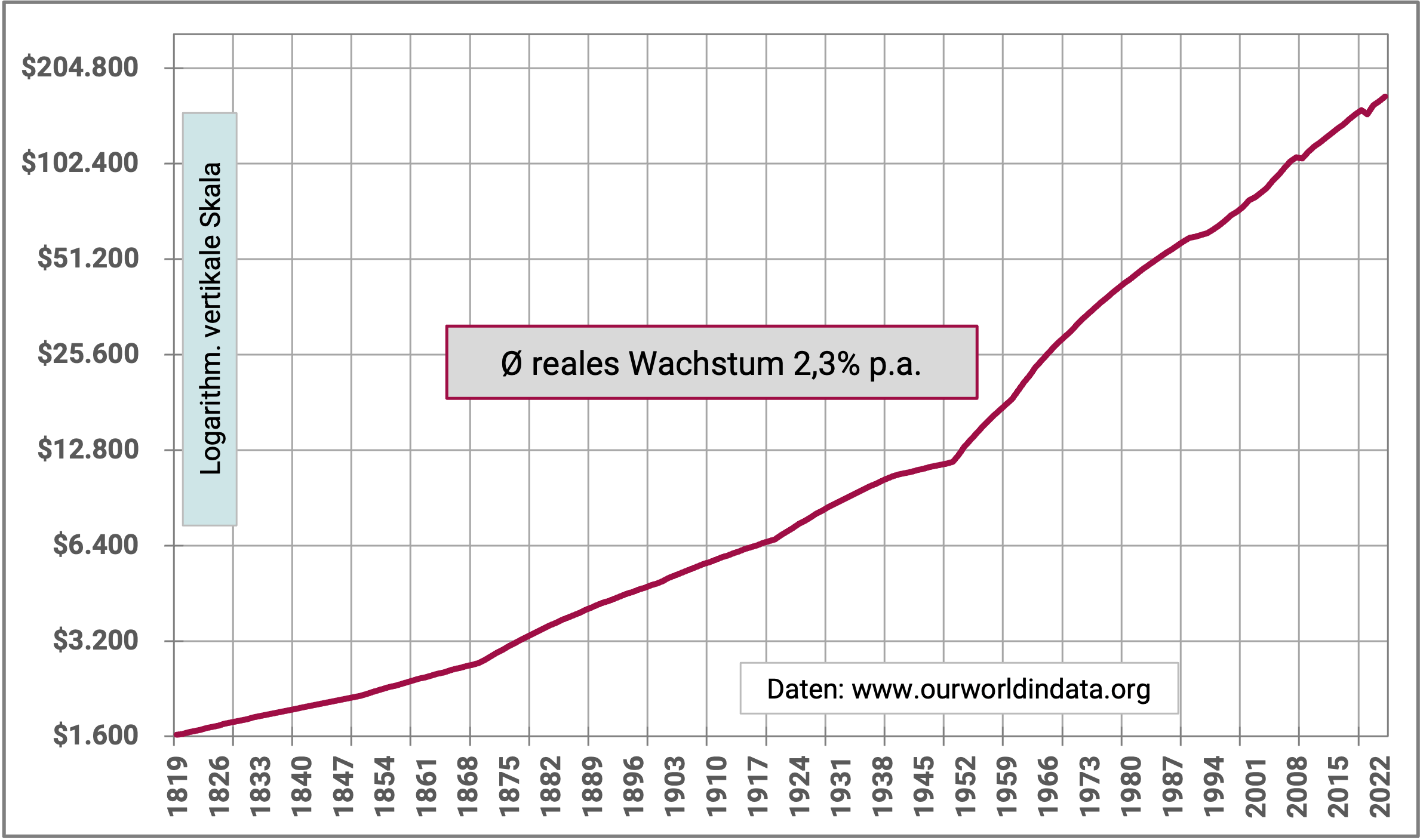

The global economy will continue to grow in the long term - just as it has done over the last 200 years since around 1800 with the emergence of the modern market economy, despite countless wars, civil wars, currency crises, economic crises, state bankruptcies, [2] Stock market crashes, natural disasters, pandemics and major demographic changes. Figure 1 illustrates this growth since the emergence of the modern market economy at the beginning of the 19th century.

Fig. 1: Global gross domestic product growth in trillion US dollars from 1820 to 2023 (204 years) – adjusted for inflation (in 2022 USD)

► 1 trillion = 1,000 billion. ► The gross domestic product (GDP) of a country is the sum of all domestic income within a calendar year: wages, salaries, entrepreneurial income (e.g. profits) and capital income (e.g. interest, dividends).

In the 1,800 years from the birth of Christ to 1800, in the pre-capitalist period, the world economy only grew at an average of 0.1% p.a. and four fifths of this low growth resulted from the increase in population alone, not from growth per capita.

The modern market economy in its current form emerged, as mentioned above, from around the year 1800. At this time, religiously legitimized feudalism (absolutist monarchism), an anti-market social order in key aspects, began to gradually die out in western countries over 100 years until the end of the First World War. Although markets existed before 1800 as places for the exchange of goods and services, the essential legal and institutional basic elements of the modern market economy were only limited to a tiny part of the total population in previous centuries: freedom of occupation and freedom of movement for private individuals, freedom of trade, freedom of movement of capital and freedom of establishment for companies. [3] The right to property existed for large parts of the population, e.g. B. women and serfs, also only limited before around 1800.

Radical ecological movements with a “degrowth” agenda have existed in most Western countries for several years [4]. These pursue the political goal of significantly reducing economic growth. If the “degrowthers” were to establish themselves on a large scale across national borders - which is not to be expected - and if this were to lead to a politically motivated permanent zero growth in the global economy, this would also lead to a zero return on the global stock market in the sense of the global equity investment class. [5] This is because the world stock market only generates a long-term positive real return if corporate profits at a global level also increase in real terms in the long term, i.e. economic growth takes place. Constant (stagnant) corporate profits (zero growth) would not be sufficient for positive returns.

As we have now seen, the fundamental conditions for positive returns in the global stock market are likely to be met in the long-term future. Nevertheless, doubts about the possibility of such a “perpetual rise in the stock market” are often encountered in traditional and social media. Most of these doubts are based on misunderstandings or errors in thinking. We address the most important three below.

Mistake 1: Misunderstanding exponential functions

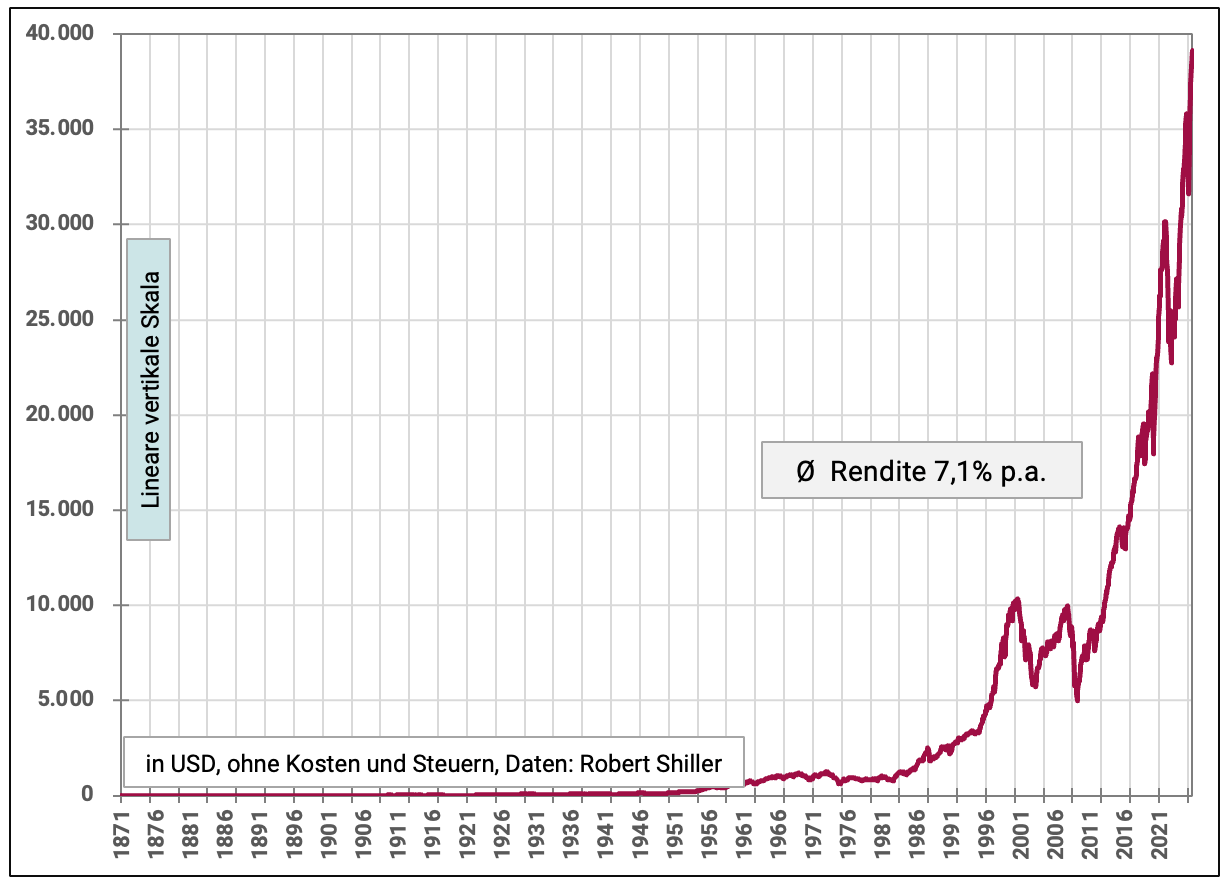

Figure 2 shows the development of the US stock market over the last 155 years in the form of a conventional stock market graph. Due to the compound interest effect (a simple mathematical exponential function) in conjunction with a linear vertical appreciation scale (the cumulative return), the development of this national stock market appears to us as if it is "unsustainable" over time, as in the last 20% or so of the time window shown, the increase in value seems to literally explode.

Figure 2: Indexed performance of the US stock market from 01-1871 to 10-2025 (154.8 years), adjusted for inflation - linear vertical scale

► Longest possible period for which the data series is available. ► Total returns = price increases + dividends. ► The US stock market is shown because monthly returns for the global stock market (which are the basis here) are only available from 1970.

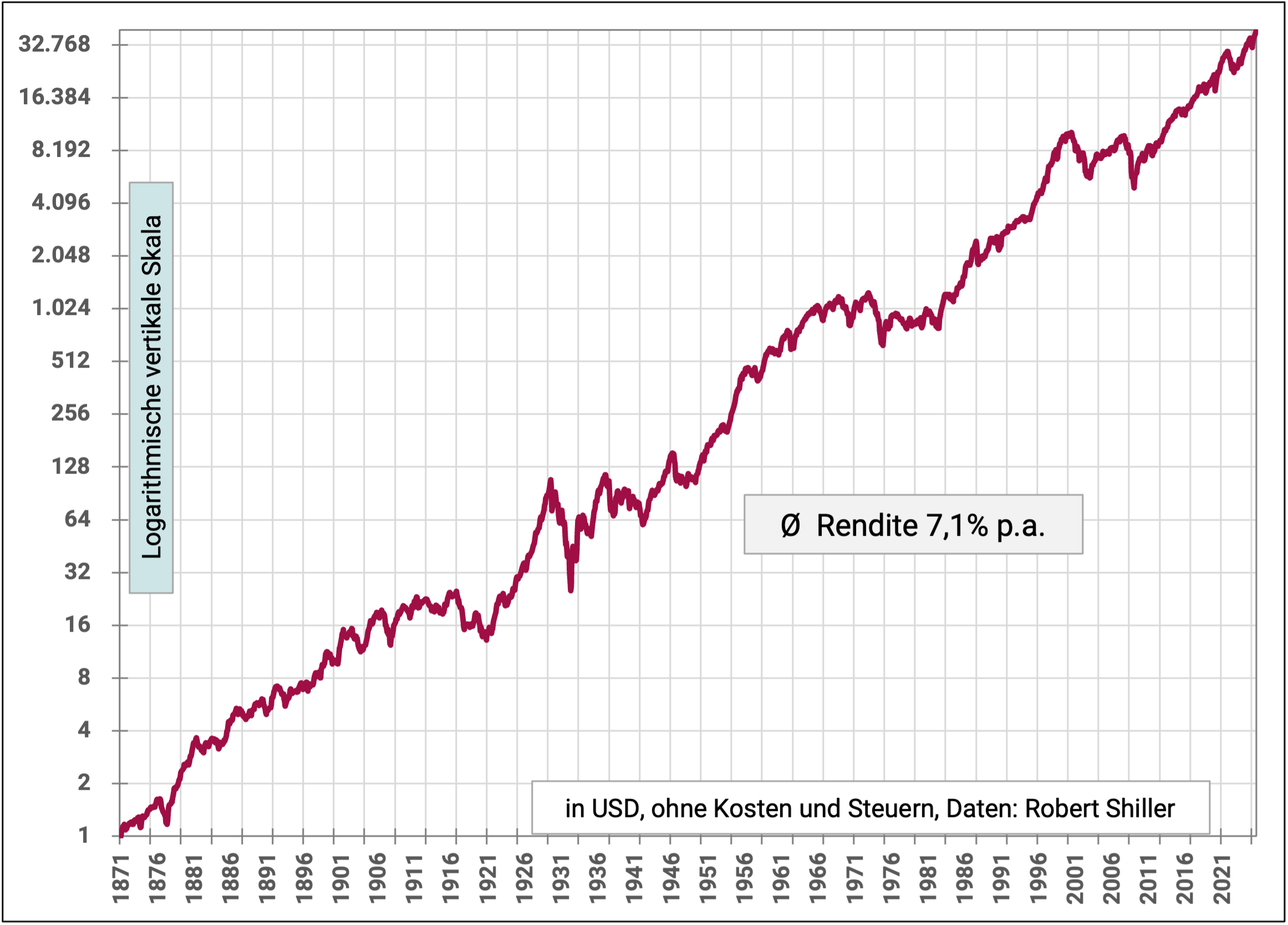

However, this return or growth “explosion” in Figure 2 is merely an optical illusion. This can be seen if you compare Figure 2 with Figure 3. The two graphics are based on the same data. Figure 2 has a “normal” linear Y-axis (vertical scale), whereas Figure 3 has a logarithmic scale. The logarithmic scale means that a given percentage increase in an interval - e.g. B. 10% per year - visually always corresponds to the same slope of the curve, regardless of whether this 10% increase occurs at the beginning of the horizontal time axis or at the end. This is not the case with the linear vertical axis in the case of long-term positive returns. Therefore, it misleads our intuition because it gives the impression that the stock market returned much more strongly in the last fifth of the period than in the rest of the period, i.e. that somehow an “unhealthy development” or “bubble formation” took place.

Figure 3, on the other hand, shows that there was a high degree of stability and “uniformity” in the return development of the US stock market over these 155 years with respect to the long-term trend. There is – correctly – no sign of a concentration of the increase in value in the last third or fifth of the period. The overall development now appears much more continuous, “sustainable” and in some ways “harmless”.

Figure 3: Indexed performance of the US stock market from 01-1871 to 10-2025 (154.8 years), adjusted for inflation - logarithmic vertical scale

The 45-degree slope in the trend cumulative return seen in Figure 3 is ultimately “arbitrary”. If we had let the vertical scale not end at 32,700 points, but at a higher value, then the red line would be flatter and the growth shown (return) would visually appear more moderate.

By the way, market capitalization, i.e. the market value of the equity of all listed companies (the market value of all stocks), increases much more slowly than the nominal or real cumulative return of the stock market, as shown in the figures, suggests. Reason: Stock returns are typically expressed as Total returns (price increases + dividends), as in Figures 2 and 3. However, these total returns exclude investors' "withdrawals" to finance taxes, incidental costs of investing and - most importantly - consumption not with one. The actual net returns in terms of the increase in market capitalization after deducting these expenses are likely to be noticeably lower. Maybe not even half as high.

Mistake 2: “Reaching an all-time high in the stock market signals that the market has ‘heated up’ and you now need to be careful.”

One of the most important reasons in investor practice why private investors, after the stock market has been rising for a long period of time, worry that the market can actually no longer continue to rise like this is the almost constant “all-time high” propaganda in the media. All-time highs in the stock market are reported by media and finfluencers [6] as a signal: “Attention, the stock market is overheated. Be careful now!” abused. In reality, an all-time high says nothing about whether a stock market is "expensive" or "highly valued" - simply because the all-time high is not a valuation metric, not even close.

All-time highs occur all the time. In the four years from November 8th, 2021 to November 7th, 2025 there were e.g. For example, the MSCI World Index (in euros) reached an all-time high on 108 trading days (working days). That was about every tenth day. Even if stocks only had a paltry nominal average return of 1% p.a. for over 100 years (i.e. about one-ninth of the actual nominal average return and far below average corporate earnings growth), there would still be new all-time highs all the time.

Because the media has been spreading the “all-time high as a warning signal” nonsense more frequently and more shrilly in recent years in order to increase views and circulation, we have it in a separate one Blog post analyzed.

Mistake 3: “The global stock market cannot grow faster than the global economy in the long term”

A technically more sophisticated false claim about the viability of historical stock returns, which is heard less frequently than the all-time high nonsense, goes like this: The global stock market returns observed in the past (long-term average inflation-adjusted 5% to 6.5% p.a.) cannot be continued in the future because these returns significantly exceed the growth of the global economy. Regarding the numerical background: Real growth in the global economy over the last 60 years has averaged around 3.0% p.a. (approx. 1.5% p.a. on a per capita basis). However, the global stock market produced a real return of over 6% p.a. during this time.

An academic essay states: “Financial assets cannot outperform the economy indefinitely because financial assets would ultimately become the economy itself.” [7] Similar statements are repeatedly made by financial journalists critical of growth.

Fortunately, this is also a mistake in reasoning, one that is based on two technical errors:

Misconception 1: A significant portion of the income from stocks or other investments is used by their owners for consumption purposes and to cover costs and taxes (as mentioned above). In other words, the “net return” of stocks after consumption is anyway much lower than the gross return before withdrawals and costs. This means that the gap between (net) stock market returns and economic growth is shrinking significantly.

Misconception 2: Gross domestic product consists of several components that could be called "asset classes" in a sense: wages/salaries (human capital), various forms of capital income, including equity income, debt income and rental income (while avoiding double counting). Since equity income is the riskiest of all these types of income, it must also have the highest long-term return, while the other types of income must have correspondingly lower returns. We have the exact logic of this economic situation in one of our own Blog post explained.

What are the current ratings?

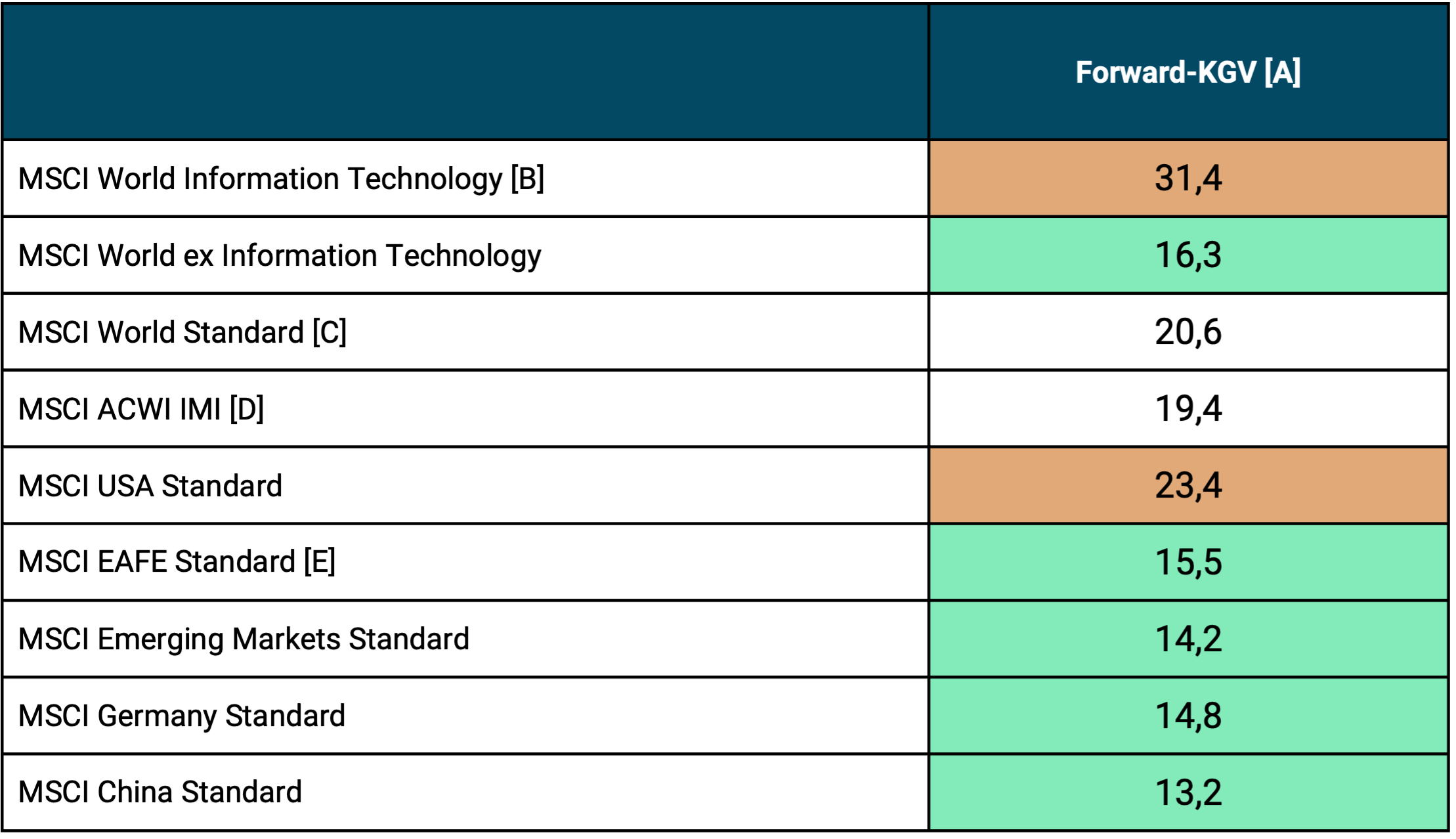

Finally, in the following table we take a quick look at the current valuations of the global stock market and some of its smaller sub-segments.

Table: The forward P/E ratios as of October 31, 2025 in the world stock market and in some large sub-segments of the market

► [A] P/E ratio = price-earnings ratio, a valuation indicator. The P/E variant “Forward P/E” is not based on the historical profit from the last 12 months, but rather the forecast profit for the next 12 months. In our view, forward P/E ratios tend to be more meaningful than conventional, historical “trailing” P/E ratios. Trailing P/E ratios would be higher for all indices shown here. ► [B] “Tech Stock Sector”. ► [C] The MSCI World Index currently consists of 73% US stocks and 29% tech sector stocks. ► [D] ACWI IMI = All Country World Index IMI = industrialized countries + emerging markets including small caps = 99% of the market capitalization of the world stock market. ► [E] EAFE = MSCI World ex USA and Canada (EAFE = Europe, Asia, Far East). ► Source: MSCI Index Fact Sheets.

The P/E table illustrates that, with the exception of the global tech sector and the US stock market, current valuations for countries and regions outside the US and outside the tech sector are relatively close to their historical average (“normal”) valuations. These averages vary from index to index and depending on whether you go back 20 years, 50 years or even longer. However, for the sake of simplicity, a benchmark of 17 for industrialized countries and 15 for emerging countries can be assumed to be somewhat “normal”. In practice, deviations of plus/minus 10% from the historical average can be ignored.

Against this background, a globally diversified stock portfolio in which care is taken not to weight US stocks and tech stocks very highly is likely to currently have a historically normal valuation and therefore not be “expensive”.

Conclusion

This blog post attempts to answer the question: “Can stocks go up forever?” The answer is yes if “stocks” in the question means the global stock market, not one of its many sub-segments, and if we at the same time assume that the global economy will continue to grow in the next 50+ years at about the same rate as the average over the last 200 years.

However, if the global economy produces significantly lower growth in the future, this will not only reduce the returns of the equity asset class, but very likely all important asset classes, including the most important for humanity, namely human capital, i.e. wages and salaries.

Structural factors inhibiting growth in the future ahead could be (a) Demographics (aging, increase in the dependency ratio [8]), (b) today's historically high debt ratios of states, companies and private households, and (c) the political and social inability to carry out painful economic reforms, which is becoming increasingly obvious in Western countries (example: inability to reform the over-indebted state pension systems). On the plus side is the growth-promoting effect of the further development and spread of artificial intelligence.

Excursus: Is capitalism subject to a “compulsory growth”?

The thesis that capitalism is subject to a “compulsory growth” is popular among left-wing intellectuals, large sections of the media and many politicians. Here a YouTube video with a representative of this false thesis. It is based on a rhetorical “conversion trick”.

Yes, an open society is indeed subject to a “growth constraint”, since permanently negative per capita economic growth and perhaps even mere “zero growth” in such a society after ten or 15 years would lead to serious intra-societal distribution conflicts, to mass emigration of people with above-average professional qualifications, to capital flight (departure of companies), to an increase in crime and possibly even to a civil war. “Open, democratic society” here means open in the sense of the possibility of free emigration of people and open in the sense of freedom of movement of capital, i.e. the departure of companies.

However, the aforementioned dire consequences of long-term negative economic growth are not related to the specific economic system of the society affected by it, but on the contrary are independent of it. These adverse consequences would occur in any open society, regardless of whether it has a market economy, a socialist or a fundamentalist-religious-collectivist economic system.

For example, the communist states of the former Eastern Bloc were not open societies. These one-party dictatorships were able to afford very low and probably even negative per capita growth for many years because there was no freedom of movement (free emigration) and no free movement of capital. [9]

The “capitalism compulsion to grow” claimed by ideologists is therefore not specific to capitalism. Rather, it is specific to an open, modern society. Only a radical authoritarian regime with closed borders and strict capital controls can survive with zero growth or negative economic growth for a long period of time and can therefore escape the “compulsory growth”.

Endnotes

[1] Individual listed companies often experience price losses of 80% or more, in the short or long term, but this is not about individual stock risk. We have written our own blog post on individual value risk: Kommer/Weis: “The questionability of individual stock investments”

[2] “State bankruptcy” means that a state is temporarily no longer able to fully service the capital (interest, repayment) on the bonds (debt) it issued at a given time.

[3] These are essentially the so-called “four basic freedoms” for employees and companies within the EU.

[4] See the articles “Degrowth” in the English Wikipedia or “Growth-critical movement” in the German Wikipedia.

[5] We will address the dramatic negative consequences of long-term zero growth at the end of this blog post.

[6] Finfluencer = influencer in the field of finance.

[7] “Financial assets cannot outperform economic performance in the long term because otherwise they themselves would represent the entire economy in the long term.” Source: Ibbotson, Roger/Straehl, Philip: “The Long-Run Drivers of Stock Returns: Total Payouts and the Real Economy”; In: Financial Analysts Journal; 73; No. 3; 2017.

[8] Dependency Ratio = the ratio of working people to non-working people in a country.

[9] The economic growth rates published by these countries at the time were manipulated upwards.