From Gerd Kommer and Praval Kapoor

Emerging market stocks have produced worse returns than developed market stocks over the past decade. In addition, there has been unpleasant political news from China, the largest emerging country, for a good two years. Consider the brutal Covid lockdown and numerous arbitrary acts of the Chinese state dictatorship, which also affect foreign shareholders and may have contributed to the low returns on the Chinese stock market.

Against this background, skeptical media headlines about emerging market investments such as the following article headings have been appearing for some time:

“Emerging markets: All risks and few rewards?” [1]

(Financial Times, February 15, 2022)

or

“MSCI Emerging Markets: This index is not good for much”

(FAZ, October 10, 2022).

In this blog post, we will therefore examine the question of whether equity investments in emerging markets are still attractive for private investors today and, if so, how we believe they should be carried out. We do this by taking a closer look at the following five aspects of equity investing in emerging markets (EM).

(1) What should be the main reason for a rational, scientific investor to include EM stocks in their portfolio?

(2) What are the historical returns of EM stocks?

(3) Is China the problem in the MSCI Emerging Markets Index?

(4) How are EM stocks currently valued?

(5) From an implementation perspective: How should one invest in EM stocks?

(1) What should be the main reason for a rational, scientifically minded investor to include EM stocks in their portfolio?

The main argument for EM equity investments is not their higher long-term returns, as the media and financial industry typically postulate, but rather that EM equities are generally a significant part of the global equity market. If you don't have any EM stocks in your portfolio, you are by definition not investing in them global Stock market, not in the “Welt-AG”, but only in a part of it.

Emerging markets are not a niche event in the real economy either. They make up over 85% of the world's population, represent over 70% of the planet's landmass, are home to around four fifths of the world's known raw material reserves and - depending on the calculation method - generate between 40% and 55% of global economic output.[2] Few doubt that this share will continue to rise – as it has in the past 20 years.

In the three and a half decades from 1988 to 2022, EM stocks have an attractively low correlation to industrial country stocks (developed markets stocks/“DM stocks”) with a value of +0.73. In recent years, this value has actually fallen in trend because the much-cited globalization is now in reverse gear. This is regrettable from a real economic perspective, but it can be an advantage for capital market investors.

Due to the relatively low correlation between EM stocks and DM stocks, adding 10% to 30% EM stocks to a DM stock portfolio improves the risk-weighted return of the stock portfolio in the long term. A rational, evidence-oriented investor should actually welcome this.

(2) What are the historical returns of emerging market stocks?

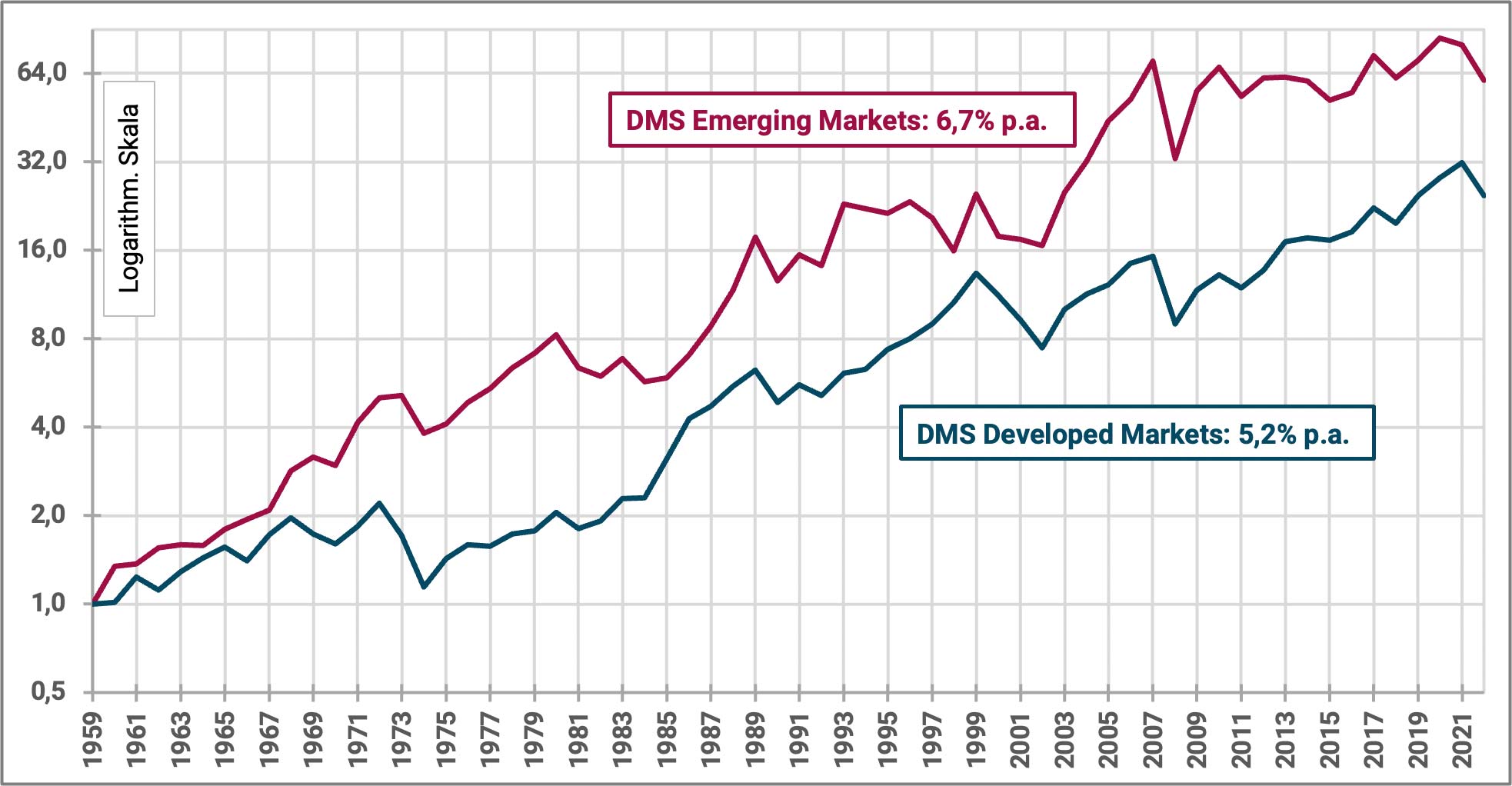

In the long term, EM stocks return better than those of developed markets. The following figure illustrates this for the 63 years from 1960 to 2022.

Figure 1: Development of the DMS Emerging Markets Index and the DMS Developed Markets Index from 1960 to 2022 (63 years) – real in USD

► Inflation-adjusted returns in USD excluding costs and taxes. ► Data source: DMS Dimson/Marsh/Staunton – Morningstar.

If you divide the 63 years shown in Figure 1 into two equal halves, the first half results in significant EM outperformance, while the second half results in almost identical returns between EMs and DMs. Such a return distribution pattern is by no means unusual and could equally well occur between two other well-defined asset classes, such as US Treasuries and US stocks, or value stocks and growth stocks. Per se, one cannot deduce from this “uneven outperformance distribution” over long periods of time that for EM stocks during the second half period, e.g. B. after the turn of the millennium, a negative structural break occurred in the sense of permanently lower returns.

If anything, the macroeconomic conditions in emerging markets as a group are better today than they were 15 or 25 years ago.

If one relates EM stocks to the asset class Stock Germany, the attractive properties (higher absolute EM returns and low correlation) would become even more apparent, as German stocks have, on balance, performed worse than the MSCI World over the last few decades. Furthermore, the correlation between EM stocks and German stocks is still slightly lower than that between EM stocks and DM stocks.

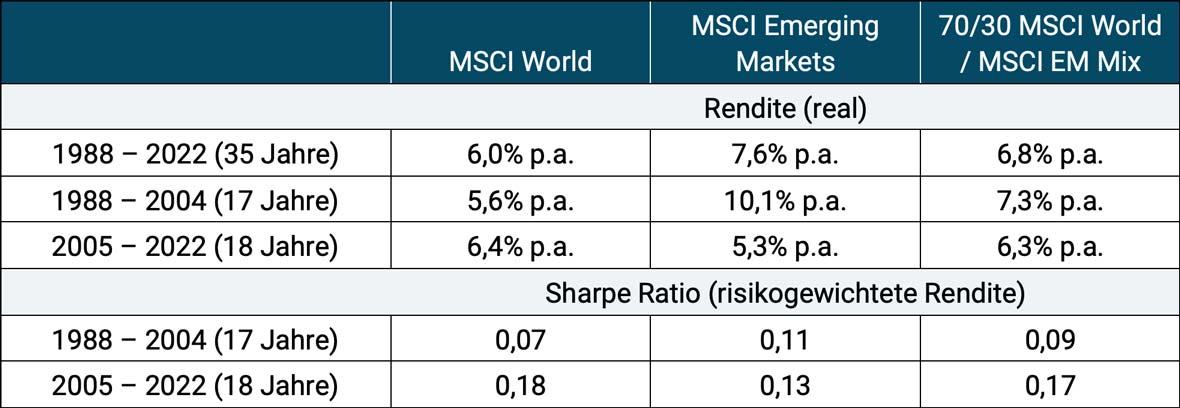

Table 1 highlights the performance of EM stocks and their role as a diversifier in a global equity portfolio using the well-known MSCI World and MSCI Emerging Markets indices for the shorter period of 1988 to 2022 (35 years). That's how far back the MSCI EM index goes.

Table 1: Comparison of the returns of the MSCI World, the MSCI Emerging Markets and a 70/30 mix of MSCI World and MSCI EM from 1988 to 2022 (35 years) - real in DM or euros

► Inflation-adjusted returns in DM or euros without costs and taxes. ► Maximum data series going back; The data series for the MSCI China does not begin until January 1993. ► Sharpe ratio: cf. Definition on Investopedia. ► Data source: MSCI, Bundesbank.

The data in Table 1 shows that adding EM stocks significantly improved the performance of a diversified global equity portfolio in the first half of the full 35-year period. Although EMs performed worse than DMs in the second half of the overall period, they were not a detrimental admixture. The absolute return and the risk-weighted return of the mixed world portfolio were also only negligibly worse in the second time window than that of a pure MSCI World portfolio consisting solely of DM stocks. The reason for this surprising result at first glance is the low correlation between EM and DM stocks. If two investments A and B have a sufficiently low correlation with one another, a mixture of the two can, for financial mathematical reasons, in the best case scenario even result in a higher return than the more profitable of the two individual investments. Reason: Mixing reduces the so-called “volatility drag” (the negative effect of volatility on returns), from which every fluctuating investment inevitably suffers.

(3) Is China the problem in the MSCI Emerging Markets Index?

In our opinion, there is little convincing evidence to support this thesis, which has been heard in the financial media due to the poor Chinese stock returns, the relatively high weight of China in the MSCI Emerging Markets Index and the unpleasant political news from China in the recent past.

Among the 24 countries in the MSCI EM Index, China's return contribution was weak overall in the 30 years since 1993 (beginning of available data), but improved noticeably in the second half of that 30-year period - both in absolute and relative terms (relative to the average of the remaining member countries). If China was “the return problem in the MSCI EM index,” it was only in the first half of the 30 years. In the second, China's returns were in the middle of the 24 EM countries.

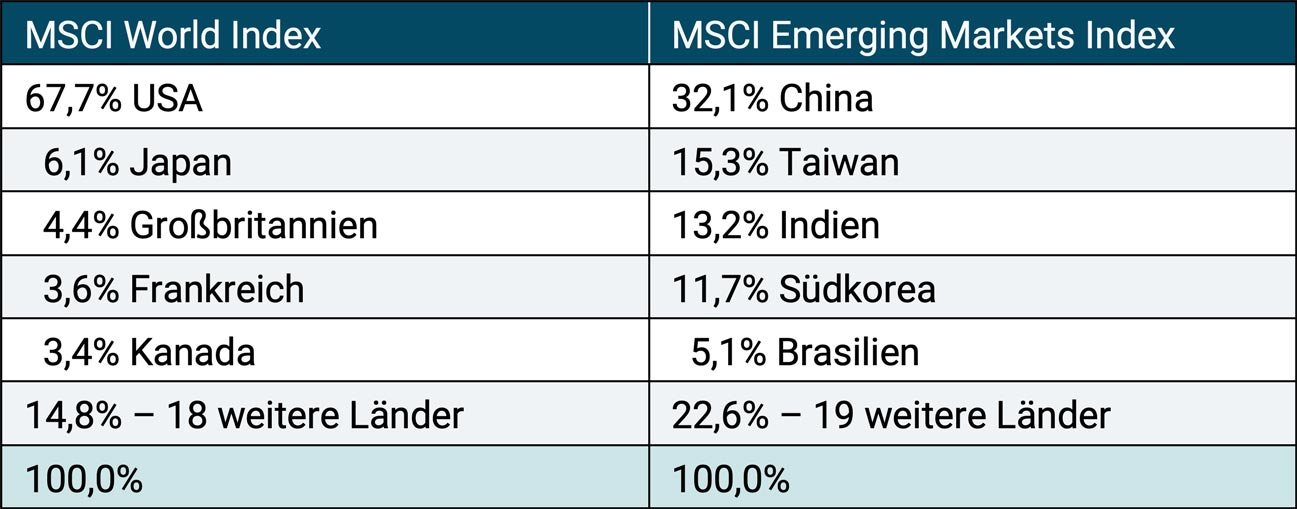

In this context, one occasionally encounters complaints in the media and in the blogosphere that China has too high a weight in the MSCI EM Index. In principle, high weights for an individual country in a regional index, i.e. a certain “top-heaviness” of the index, are the norm, not the exception. The stock market is not “evenly divided in terms of size” – neither in terms of countries, sectors, nor individual stocks. Having said that, the MSCI EM is clearly better diversified across its 24 member countries than the MSCI World Index across its 23 members - this is shown in Table 2.

Table 2: The weights of the five largest countries in the MSCI World Index and the MSCI Emerging Markets Index (as of February 2023)

► Source: MSCI (fact sheets of the two indices)

From the perspective of a passive investor seeking a well-diversified global equity portfolio, the high proportion of the USA in the MSCI World Index could appear to be a worrying cluster risk rather than the comparatively smaller proportion of China in the MSCI EM. It should also be borne in mind that the MSCI EM only has a weight of around 10% in a market capitalization-weighted global equity portfolio and therefore China Overall portfolio level only 3.2%. This value drops even further if the portfolio also contains a non-stock component (cash, bonds, raw materials, precious metals, crypto, etc.), which is likely to be the case for most investors.

On the issue of the lack of rule of law in China, which has been taken up by the financial media, especially in the past two years, and which is certainly also relevant for shareholders. It was known decades ago that China is not a constitutional state, so it is not a new development. Constructing this as a “structural break”, a “new factual situation” or a “game changing event” that has occurred in recent years with regard to China stocks or EM stocks in general (as some “experts” do) does not seem very convincing.

“Weak scores” in the rule of law or democracy category are a feature of many EM countries, not just China. We should not overlook the fact that each country started out “at the bottom” at some point when it comes to the rule of law and democracy – including countries that are now high up in international comparison when it comes to these criteria.

In addition, the Chinese stock market is currently particularly attractively valued (see Table 3 below), which results in an expected return for the future that is around a fifth above normal levels.

In addition, EM stocks as an asset class offer better long-term returns than DM stocks for precisely this reason. because they are exposed to higher political risk (the “EM premium”). To the extent that EM stocks offer better returns in the long term, this is primarily compensation for this political risk (Kelly et al. 2023). Despite this, the financial media and financial industry marketing still regularly promote the old and false theory that EM stock returns are higher in the long term due to the higher economic growth of EMs relative to DMs.

Yes, emerging markets undoubtedly have this higher GDP growth. They have had it in the past and will have it in the future. Nevertheless, the thesis of higher stock returns due to higher economic growth is nonsense. We have last here showed why this is not true.

Furthermore, any active or passive investor who believes that China is the problem in the group of 24 MSCI EM countries can quite easily ignore this country. A passive investor could do this, for example, by using an ETF on the MSCI EM ex China Index do. Two ETFs based on this index are currently offered in Germany.

(4) How are emerging market stocks currently valued?

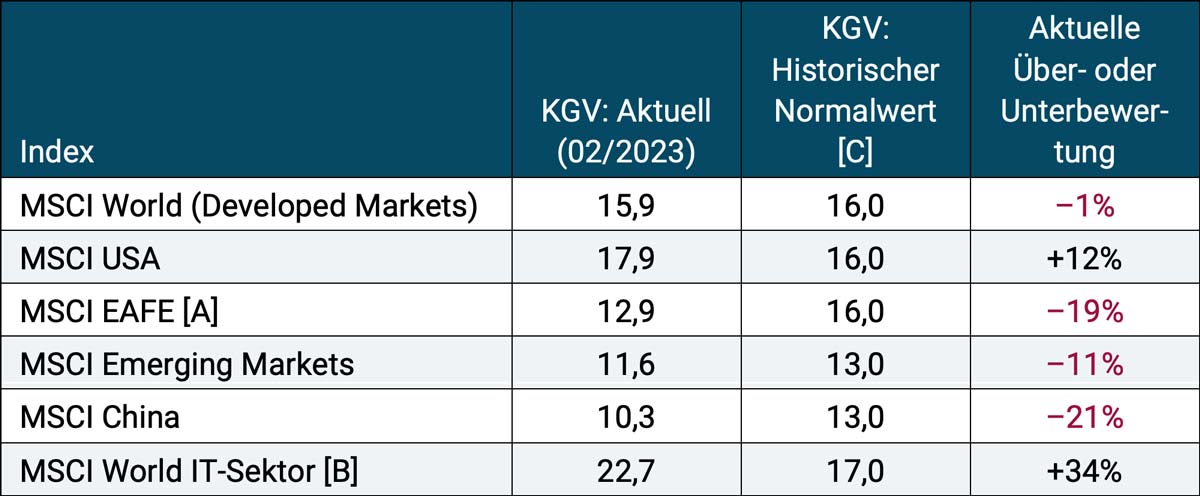

Expected returnn - i.e. the long-term average statistical returns expected from an asset class in the future - are a function of the valuation level of the asset class at the time of observation. Table 3 shows how EM stocks perform relative to the relevant alternatives from this perspective.

Table 3: The price-earnings ratios (P/E ratios) for four regions + China and the global information technology sector as of February 28, 2023

► [A] MSCI EAFE = Europe, Australasia, Far East (all industrialized countries except USA and Canada). ► P/E ratio = Forward P/E’s (Forward Price Earning Ratios). ► [B] MSCI World Information Technology Sector. ► [C] The P/E normal values shown here are rounded numbers derived by us from history. Slightly different average values can often be found in the relevant sources. ► Data source: MSCI.

The table shows that at the end of February 2023, the US national stock market was trading above its historically average valuation level. The valuations of the remaining industrialized countries (EAFE index) and those of the EMs were below their fair level.

The comparatively poor EM returns over the past ten years or so are reflected in the now quite favorable valuation level. This is advantageous from a countercyclical perspective. When it comes to asset classes, investing countercyclically means preferring those that have performed poorly in the recent past and therefore now have an attractive valuation level relative to the relevant alternatives - or staying invested in these asset classes if you already are.

The global high-tech industry is still in “lower bubble territory” in the DM countries – despite the quite heavy price losses in 2022. We know that tech stocks do not deliver higher returns than the rest of the stock market in the long term here shown. In this respect, below-average returns could be expected in this segment in the coming years.

From a valuation perspective, there is currently no reason not to invest in emerging markets or - to put it another way - there are good reasons to continue an existing EM equity investment, at least as long as it is broadly diversified. The US fund company AQR, which we greatly respect, sees the situation even more optimistically. A few days ago she wrote “the expected premium for investing in emerging versus developed equity markets is on the upper end of its past 25-year range.” [3]

(5) From an implementation perspective: How should one invest in EM stocks?

Anyone who is convinced by the data and logic presented here is faced with the practical implementation question “how to invest in emerging market stocks?” We recommend observing the following basic principles.

- The principle of “broad diversification” is particularly important for EM stocks. Betting on individual EM countries or individual EM stocks is unnecessarily risky. In Germany, over 80 ETFs are offered on broad EM stock indices (excluding EM bond indices), of which around 20 ETFs are on the well-known MSCI Emerging Markets Index and a further 60 are on other EM region indices as well as EM indices with a focus on sustainability. There are also around 100 ETFs on individual EM countries, smaller EM regions or other narrow EM specialty indices. From active Managed emerging market funds are not recommended because their average performance is below that of corresponding ETFs. The few exceptions to this basic rule change constantly and are driven by chance. They cannot be reliably predicted.

- Anyone who is convinced of factor investing (smart beta investing) (like we are) can also apply this variant of passive investing to EM stocks and overweight certain factor premiums such as small size, value and quality in the portfolio via corresponding ETFs in order to achieve additional returns.

- The return and risk of a portfolio must be assessed primarily at the overall portfolio level. Anyone who cannot mentally free themselves from the error of considering the individual returns and risk levels of individual portfolio components as decisive should probably not make any EM equity investments because that could be a ticket to disappointment for them.

- The old rule of thumb, which is often forgotten despite its banality, also applies to EM stock investments: only money that the investor's household will most likely not need in the next five years should be invested in stocks.

- If you like EM stocks in general but don't like China, the local ETF landscape offers plenty of opportunities to exclude or downweight the Middle Kingdom from your portfolio.

If you would like to deepen your investment knowledge of emerging markets from a different perspective, you could read our blog post “Emerging market government bonds – an asset class worth considering?” from July 2019 worth reading (see here).

Endnotes

[1] “Emerging Markets: All Risk, Little Reward?”

[2] Around 40% if you calculate national GDPs based on normal USD exchange rates and around 55% if you use exchange rates adjusted for purchasing power.

[3] “The expected premium for investing in EMs versus DMs is at the upper end of its [historical] spectrum over the last 25 years” (Aghassi/Villalon 2023).

literature

Kelly, Bryan / Lubos Pastor / Pietro Veronesi (2023): “The Price of Political Uncertainty: Theory and Evidence from the Option Market”; NBER Working Paper No. w19812; 19 Feb 2023; Internet reference: here

Aghassi, Michele /Daniel Villalon (2023): “Re-Emerging Equities”; AQR; March 28, 2023; Internet reference here