<<< This blog post is also available as a YouTube video. >>>

From Jonas Schweizer and Gerd Kommer

This blog post was updated in December 2024.

Germany has a chance to win the world championship title in two disciplines: in dressage and in the share of bank deposits in the liquid assets of private households. In dressage, the German national team has won twelve of the 15 possible world championship titles in team competition since 1966. [1] When it comes to the share of bank deposits in liquid assets, we are likely to dominate in a global comparison. The media regularly carries the headline “Germans are world savings champions”, i.e. champions in accumulating bank deposits. Unfortunately – unlike the equestrian titles – this is no reason to celebrate. We will explain why not in this blog post.

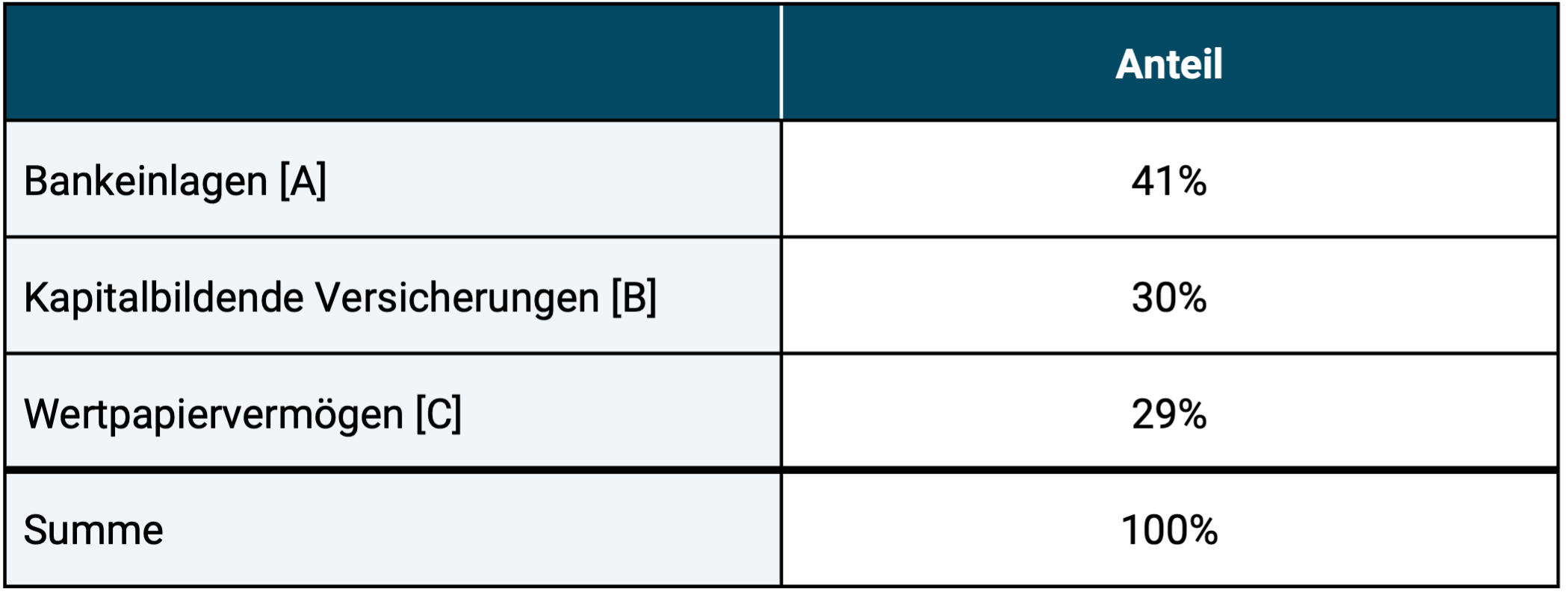

Table 1 shows the size and structure of Germans' liquid assets. Bank deposits, i.e. balances in current accounts, savings accounts, current account accounts and fixed-term deposit accounts, make up the largest part at 41%. Capital-forming life insurance, which is also a rather counterproductive investment from a return and risk perspective, comes in second place with 30%.

Table 1: Composition of Germans' liquid assets at the end of 2021

► [A] Balances in checking accounts and interest-bearing bank accounts. ► [B] Capital-forming life and pension insurance. ► [C] Investment funds/ETFs and individual securities such as stocks, bonds, certificates, derivatives. ► This table does not include illiquid investments such as direct investments in real estate, unlisted company investments and claims to statutory pension insurance or equivalent pension funds. ► Source: Bundesbank.

For rational households aiming to build wealth, bank deposits are not sensible investments for the following two reasons:

Reason #1: From an economically correct perspective, you cannot build wealth with interest-bearing bank deposits (naturally even less so with non-interest-bearing ones). We analyzed the structural and ultimately insurmountable “lack of returns problem” of interest-bearing bank deposits in our own blog post (here). In this article we therefore want to concentrate on reason number 2.

Reason #2: Bank deposits are too risky. We will show below why and in what way they are, and what exceptions there are to this strangely little-known fact.

Another conceptual clarification. When we talk about “deposits” or “balances” in this blog post, we mean cash balances in banks, e.g. B. Current account deposits, interest-bearing daily deposits, fixed-term deposits, savings account balances, but not securities or fund investments in a securities account. Unlike the balance in an account, the contents of a securities account are generally not at risk if the bank holding the securities account goes bankrupt, since the bank only acts as a trustee or administrator for a securities account.

Now to clarify why bank deposits are risky.

Causes of the risk of default on bank deposits

In the case of a bank deposit, the bank is the debtor and the depositor (saver) is the creditor, i.e. the lender. Unfortunately, banks are economically fragile debtors. There are two reasons for this: In no other industry are the equity ratios as consistently low and, conversely, the debt ratios as high as in the banking sector. Over 90% of a typical bank balance sheet consists of debt. These debts include savers’ deposits.

The second reason: Banks are the only industry that is significantly affected by the risk of “runs” by their depositors (customers), i.e. their main lenders. In one Bank run Many or all of a bank's depositors try to withdraw their balances at the same time out of fear for the safety of their money, while around 95% to 99% of these balances are not even available to the bank in a liquid, immediately available form. This can lead to the bank's liquidity or regulatory insolvency within a short period of time, often just a few days. Recently, the head of the Bundesbank, Joachim Nagel, confirmed that the likelihood of a bank run has increased with the advent of social media (here).

Above we mentioned that under civil law, a bank deposit represents a loan from the depositor to the bank. Because this is the case, the bank balance legally belongs to the bank and not to the depositor, as almost all bank customers mistakenly assume. The depositor only has one claim, a claim for repayment, against the bank. If the bank becomes insolvent, the realizable value of this repayment claim can fall below 100% and even to zero.

Bank failures of individual institutions or bank failures as part of a systemic banking crisis are in a way like earthquakes. They are rare and their occurrence cannot be reliably predicted, but that They do happen, that's for sure. The last major global banking crisis with hundreds of formal or de facto bank bankruptcies (around 15 in Germany) occurred from 2008 to 2011. In March 2023, a mini-banking crisis occurred in which one of Europe's largest banks, Credit Suisse, and three medium-sized US banks collapsed. Between 2011 and today, around half a dozen of 1,700 banks in Germany have involuntarily relocated to the afterlife due to bank-specific problems (mostly management incompetence). Bank failures occur equally in private banks, cooperative banks, state banks (savings banks) and quasi-banks called building societies. [2]

Bank failures and systemic banking crises have been “completely normal” in economic history over the last centuries – as well as in the last 50 years – even though they mostly only occur at long intervals. “Bank failure” here does not necessarily mean formal legal bankruptcy, but rather an existential economic emergency (new German “bank failure”), which either results in government support measures, a takeover by a competitor or a formal bankruptcy with subsequent liquidation. In all of these cases, “bankruptcy” means that some or all account holders face the prospect of repayment of their deposits over a longer period of time and/or suffer actual losses. The shareholders and bondholders of the affected bank will usually lose a large part of their investment.

To illustrate a few figures on bank failures from the recent past: In the five years from 2008 to 2012, 465 banks went under in the USA (around 7% of all institutions) and around 15 in Germany, including the second and third largest banks at the time as well as the largest real estate bank (Commerzbank, Dresdner Bank, Hypo Real Estate) as well as several state-owned state banks. And even after the end of the systemic banking crisis at the time (around 2012/2013), more than a dozen banks in Germany formally or de facto went bankrupt and probably more than 20 more were taken over by competitors due to chronic weakness in earnings before the inevitable insolvency could occur.

There was hardly a country in the EU that did not experience a banking crisis in 2008/2009. The two largest Swiss banks, UBS and Credit Suisse, also suffered severe losses that, from the perspective of the time, threatened their existence. Credit Suisse then collapsed a few years later in 2023 as part of a “small” systemic banking crisis in early 2023. However, the period around 2008/2009 was not a one-off special case. Serious national banking crises between the Second World War and 2008/2009 occurred in the USA, Japan, Norway, Spain, Sweden, Switzerland and Great Britain, to name just the better-known cases. In economically less developed countries, bank failures and near-bankruptcies (insolvencies) are even more common.

Over the past 150 years and before, many thousands of banks have collapsed in industrialized countries worldwide, mostly in the context of a bank run (see here and here and here and here and here).

The belief sometimes expressed by private investors that the local small bank is safer than large national or international banks is comically naive. This wishful thinking probably comes from the fact that such “small bankruptcies” never occur Mirror, the daily news or on YouTube emerge and/or from confusing familiarity with certainty - a well-known cognitive error that everyone is subject to to some extent. Small banks that do not have a rating would typically have a bad one.

Regarding deposits in savings banks, many citizens believe that the deposits of these state banks are guaranteed by their owner (city, district). None. This so-called “guarantor liability” from 1931 was rightly abolished in 2005 because it distorted competition. Therefore, a municipality may not carry out a bailout of its insolvent savings bank, even if it could exceptionally do so.

Bank bankruptcies are therefore a normal phenomenon in the market economy, even if they are less numerous and more irregular than corporate bankruptcies in other sectors. Of course, there will continue to be individual bank failures and national or systemic international banking crises.

Some readers will object at this point that there is a security system for bank deposits. Yes, there are various security systems, but unfortunately their security effect is very limited.

The state deposit insurance

In Germany and all EU member states there has been a so-called statutory deposit guarantee for bank deposits up to a limit of 100,000 euros per bank-customer combination since 2014.

However, the “statutory deposit protection” up to 100,000 euros does not represent a formal government guarantee as in the USA. [3] but only a “legal right to compensation through a private, state-supervised compensation system”. From the perspective of bank customers, the legal certainty that exists in the USA is missing. Nevertheless, the statutory deposit insurance in the EU is likely to come close to a formal government guarantee of 100,000 euros per customer, but it does not represent a hard legal claim. Why is the government deposit insurance limited to 100,000 euros?

Two reasons: (a) Replacing just 100,000 euros for millions of customers in a systemic banking crisis would push every country in Europe to the limit of its financial strength. More than 100,000 euros would simply be impossible, as we will show below. (b) Over 90% of all account balances in Germany (and probably every other EU country) have a balance of less than 100,000 euros. From the point of view of most politicians in the Bundestag, the larger assets would belong to the “rich” minority, which is known to be unworthy of protection.

Keyword “Limits of its financial strength”: No Western state has sufficient financial reserves to cope with a major systemic banking crisis all bank balances or even just the majority of them. This can be easily shown using Germany as an example: the total bank balances in this country amounted to around 3,260 billion euros at the end of 2023. This was offset by state tax revenues of 916 billion euros in 2023. However, 100% of these funds are already earmarked for other purposes, e.g. B. for civil servant salaries, the maintenance of public infrastructure and other government expenditure.

Could the government take on debt to finance a general bank bailout? Unfortunately, once again missing. Such an unlimited debt-financed bailout in the context of a major systemic banking crisis is unlikely to be possible for any Western country today, since the debt ratios of most countries are already at a level that can no longer be significantly expanded without triggering serious negative consequences.

Even “printing money” to finance an unlimited bank bailout, including all bank deposits, would probably not work as a solution. Of course the capital markets, especially the bond market, would see through this cheap deception. Nominal and real interest rates would probably rise, making government refinancing more expensive in the future. Furthermore, due to the rise in interest rates, there would be severe price losses in existing government bonds - with potentially dire effects on institutional investors such as insurance companies, pension funds, banks and charitable foundations that hold these bonds. The increased interest burden on national debt could trigger a national crisis or even a national bankruptcy some time later.

If a state – regardless of whether it is called the USA, Germany, Switzerland or Liechtenstein – ex ante, i.e. if, outside of a banking crisis, an unlimited, formal guarantee was issued for all national bank deposits (either verbally by a member of the government or in legal form), the rating agencies would have to immediately drastically downgrade the credit rating of the country in question (lower the credit ratings of the government bonds in question) due to this gigantic, unrealistically fulfillable “contingent liability”. There would again be severe price losses for existing government bonds and an increase in the interest costs of new bonds. Possible consequences see above.

Because this is the case, there are either no formal government guarantees for bank deposits at all, as in Switzerland or the EU, or they are limited to “relatively small” upper limits per bank customer, as in the USA (250,000 dollars per customer there).

Interim conclusion: The state can save individual banks, but probably not many banks that become insolvent at the same time in a systemic banking crisis. In a major systemic banking crisis, the state's financial strength would realistically hardly exceed 100,000 euros per bank customer.

Could banks' private, voluntary deposit insurance schemes help?

In addition to the state deposit insurance, each of the three banking groups in Germany - cooperative banks, public/state banks and private banks - each operate a purely voluntary, i.e. not legally required, private security system with significantly higher security limits than the 100,000 euro limit of the statutory deposit insurance. Does this solve the problem of the default risk of bank deposits for savers? [4] A third time nothing. These systems will also collapse immediately in a systemic banking crisis with the simultaneous failure of several banks due to their ridiculously low reserves. They only help if a single or a few individual banks outside a systemic crisis. [5]

Why do most citizens believe bank deposits are safe investments?

In the mind of a normal private investor, a bank deposit appears to be “somehow” safe or even “the safest investment” because the balance on the account statement for a bank deposit - unlike e.g. B. a money market fund or a short-term bond – never fluctuates (ignoring deposits and withdrawals). You know with apparent 100% certainty today what will appear on your bank statement tomorrow. Unfortunately, this naive risk thinking leads to a cognitive dead end when risks that occur very rarely but are particularly high, such as bank failures. It would be foolish to assume that the typically long time intervals between two banking market crises can be ignored. A risk does not disappear because it is not observed regularly or because it is difficult to quantify the probability of its materialization over the next 20 years.

Leaving cash above the statutory deposit guarantee in a bank account for a longer period of time is like building a home for your family in a region at high risk of earthquakes, which - in order to save money - does not meet earthquake safety standards and justifying this actually hair-raising behavior by saying that the last earthquake was 40 years ago.

Why you shouldn't bet on a bank bailout

Regarding this risk of default, many investors believe that the government will always bail out banks in the event of their failure, so that depositors are not harmed. This was the case in the global banking crisis from 2008 or the mini-bank crisis in March 2023. (However, banks' shareholders and bondholders suffered losses of the order of 70% to 100%. At banks in Cyprus, depositors also lost money.)

Yes, the state will try to save shaky banks if it can. So the question is not whether he wants to, but whether he can. As we illustrated above, a systemic banking crisis only slightly more severe than the one from 2008 to 2013 would probably cross the line into “no more”.

How do large companies and institutional investors invest “cash”?

When solving difficult life challenges, an obvious and natural method is to imitate the actions of the best and most professional in the field. How do large institutional investors invest if they want a highly liquid “cash-like” investment with the lowest possible volatility risk and lowest possible repayment risk? You invest in securities-based high-quality “money market investments”, i.e. in highly diversified short-term government and corporate bonds within the upper rating levels (credit ratings) and of course without exchange rate risk.

In this context, many private investors allow themselves to be led into a mistake in thinking or understanding by a purely conceptual issue: in media articles or publications from large companies, their “liquidity” is typically referred to with terms such as “cash” or “liquid assets”. In English it is usually – and almost more confusingly – called “cash”. Here are two examples of such press releases:

“Warren Buffett keeps selling Apple stock as Berkshire’s cash pile swells to $325 billion” (Fortune Magazine, online edition November 2, 2024)” [6]

“Buffett is selling Apple shares again – and is holding more than 300 billion in cash.” (Handelsblatt online edition November 3rd, 2024)

In fact, the “cash pile” and the “cash” are not bank deposits, as one might incorrectly deduce from the terms “cash” and “cash”, but almost exclusively securities investments, namely short-term high-quality bonds in the company’s native currency. In the case of Berkshire, these are typically short-term US government bonds. From the company's point of view, bank deposits of this size would be far, far too risky.

When do bank deposits make rational sense despite the risk of bank failure?

Bank deposits are therefore too risky in terms of their risk of default. Nevertheless, there are constellations in which they make sense - the following two:

Constellation 1: In terms of risk, bank deposits are tolerable as an investment for a private household (or a small company) if the bank balance in question amounts to a maximum of 100,000 euros per private individual and bank and is therefore fully covered and protected (in the EU) by the statutory deposit insurance. The guaranteeing state must have a credit rating of A+/A1 (fifth best grade) or better and the balance must be denominated in the investor's "home currency" so that there is no exchange rate risk. (At the end of this blog post There is an explanatory table for credit ratings.)

Constellation 2: Bank deposits above the state deposit insurance are tolerable if the balance in question is only temporarily parked in the bank account for a few weeks or a maximum of a few months before it flows into a higher-yield and/or lower-risk long-term investment. Here the bank itself should have a credit rating of no worse than A+/A1.

Conclusion

Bank balances are purely in terms of risk type Return volatility low risk. In terms of risk type Repayment risk (risk of default) they are not low risk at all.

It is impossible to build wealth with interest-bearing bank deposits due to their structurally poor returns after taxes and inflation (see our separate blog post). here).

For risk reasons, informed, rational investors will only hold bank deposits if the investment amount is below the statutory deposit protection limit of (in the EU) 100,000 euros per bank-customer combination. If and to the extent that the investment amount exceeds this limit, rational investors will shift these assets within a few months into a long-term form of investment that is less risky in terms of default risk.

A simple and superior alternative to interest-bearing bank deposits are money market ETFs (see here). They are almost as liquid as overnight money, produce a better return than the average daily money and, as a diversified bond investment in a bank deposit, are generally not exposed to the “bank counterparty risk”.

Endnotes

[1] A team ranking at the World Championships was introduced for the first time in 1966. In the individual competition, the Germans' winning percentage has not been quite as high since 1966, but even in this respect DE is by a considerable margin the most successful nation.

[2] One of the largest systemic banking crises of the last 50 years was the mass wave of bankruptcies at American building societies between 1986 and 1995, the so-called Savings and Loans crisis (in the USA, building societies are called “Savings & Loans” or “Thrifts”). Over 1,000 of around 3,200 of these small and medium-sized financial institutions went bankrupt at that time.

[3] The deposit insurance there is called “Federal Deposit Insurance”. It is a formal government guarantee up to USD 250,000 per bank-customer combination.

[4] Here are some other alternative names for default risk: credit risk, repayment risk, credit risk, default risk, counterparty risk, counterparty risk, counterparty risk.

[5] In some ways, private security systems are laughable. Their formal “formulas” result in utopian high security limits. The security system in question has hopelessly few resources relative to these theoretical amount limits. So it's as if Hänschen Klein, a caretaker's assistant by profession and with total assets of 30,000 euros, would "secure" René Benko's debts (several billion euros).

[6] "Warren Buffett Continues Selling Apple Stock as His Cash Mountain Swells to $325 Billion."

literature

Baron, Matthew/Daniel Dieckelmann (2021): “Historical Banking Crises: A New Database and a Reassessment of their Incidence and Severity”; March 23, 2021; SSRN; Internet reference here

Correia, Sergio/Stephan Luck/Emil Verner (2024): “Failing Banks”; NBER Working Paper No. w32907; Sep 11, 2024; SSRN; Internet reference here

Metrick, Andrew/Paul Schmelzing (2023): “Banking Crisis Interventions Across Time and Space”; NBER Working Paper No. w29281; July 05, 2023; SSRN; Internet reference here

Park, Sangkyun (2023): “Bank Runs and Design Flaws of Deposit Insurance”; SSRN; June 11, 2023; SSRN; Internet reference here

Wikipedia article (English):