From Gerd Kommer and Daniel Chancellor

This blog post was updated in October 2024.

The Germans are a nation of people who don't like the capital market. As we know from the statistics, they do not give their financial love to the stock market, but to three other forms of investment: bank deposits, capital-forming insurance and real estate.

We described the disadvantages and risks of capital-forming life insurance in a previous blog post (here). We recently wrote a blog post about the widely overestimated long-term increases in the value of residential real estate (here).

So let's get to the actual topic: Why and how money market funds are superior to interest-bearing bank deposits as a solution for low-risk and high-liquidity investments. At the end of this blog post we will name specific money market funds for readers who want to implement the findings from this blog post straight away.

Money market funds have an advantage in terms of return and an advantage in terms of risk relative to interest-bearing bank deposits.

Money market fund investments typically deliver returns that are 0.3 to 1.2 percentage points higher per year than the average overnight money at one of the approximately 1,700 banks in Germany. Only if you do labor-intensive “call money hopping” can you match or slightly exceed the returns of a good money market fund with call money. More about daily money hopping below.

With fixed-term deposits (also known as time deposits) with terms between one month and 24 months, you can also easily beat the return of a money market fund ETF, but fixed-term deposits are more inflexible and illiquid than a money market fund or overnight money, which can be immediately converted back into normal cash at any time [1]. With fixed-term deposits, this only works on the due date. When it comes to fixed-term deposits, you have to plan carefully and ask yourself with every new investment: “When will I need this money again at the earliest?” If you mess up this planning, you will lose the interest earned and possibly even a little more by paying a “penalty” to the bank. Added to this is the often annoying work of extending fixed-term deposits, which is no longer necessary with overnight deposits and money market funds. Ergo: You basically can't compare fixed-term deposits with overnight deposits and money market funds, as they are significantly more illiquid and work-intensive.

The second advantage of money market funds over interest-bearing bank deposits concerns risk, namely default risk [2]. As is well known, banks can and often do go bankrupt. We have written a separate blog post about the surprisingly high risk of bank failure (here). Bottom line: Bank deposits can only be described as low-risk up to the upper limit of the statutory/state deposit insurance limit. In the EU, this upper limit is 100,000 euros per bank-customer combination. Anyone who holds a larger sum at a single bank is exposing themselves to an unnecessarily high risk of default, unnecessary because it can be easily avoided without negative returns by having a portfolio with money market fund shares.

With “deposits” or “balances” are only Cash-This refers to bank balances (e.g. current account balances, interest-bearing daily deposits, fixed-term deposits, savings accounts), but not securities or fund investments in a securities account. The contents of a customer deposit are generally not at risk if the depository bank goes bankrupt, as the bank only acts as a trustee or administrator for a deposit. There is a fundamental difference here that not all bank customers are aware of.

Incidentally, the so-called “statutory deposit protection” in the EU of 100,000 euros per bank customer is not a formal government guarantee like in the USA. [3] but only a “legal right to compensation through a private, state-supervised compensation system.” From the perspective of bank customers, the legal certainty that exists in the USA is missing. Nevertheless, statutory deposit protection in the EU is likely to come close to a formal government guarantee of 100,000 euros per customer.

Many Germans mistakenly believe that deposits at savings banks are guaranteed by their owners (city, district) because they are state-owned banks. None. This so-called “guarantor liability” from 1931 was rightly abolished in Germany in 2005 because it distorted competition. Therefore, a municipality may not carry out a bailout of its insolvent savings bank, even if it could exceptionally do so.

It is doubtful whether the frequently practiced depositor strategy of spreading his bank balances across several banks in order to stay below the 100,000 euro limit in all of them is completely legally secure. This risk reduction method corresponds to the letter of the law (Deposit Insurance Act/EinSiG) but undoubtedly does not correspond to its spirit. Very wealthy households who really want to be on the safe side avoid this approach. This is also pleasingly easy thanks to the use of money market funds.

Below we compare money market funds and overnight funds in detail in a table. But before we do that, a quick summary of what money market funds actually are.

This is how money market funds work

Money market funds were invented in the USA in the early 1970s and arrived in the German private investor market around 25 years later, in the mid-1990s. So they are by no means new. Despite their age, they are still rarely used by private investors (in contrast to companies and institutional investors).

The so-called money market or money market is a sub-segment of the bond market. It includes very short-term loans and bonds (typically with a remaining term of up to 18 months) in the debtor's high credit rating range and without exchange rate risk. [4] Because GMF investments only have short remaining terms, the so-called interest rate risk (price loss if market interest rates rise) is low and, for certain GMFs, even zero (see our blog post on interest rate risk here).

Money market funds are de facto just as liquid and convenient as overnight deposits and more liquid and convenient than fixed-term deposits. The running costs of GMF range from 0.05% to 0.4% per annum of the money invested. GMFs in ETF format tend to be at the lower end of the range mentioned.

The question still remains as to why GMF, although they have been available in Germany for around 30 years, were hardly known among private investors in this country until recently. There are three reasons for this: (a) Bank deposits – the more familiar and familiar alternative to GMF – are mistakenly perceived as safe or at least more secure (see above). (b) Germans generally don’t like capital markets. (c) If you dare to enter the capital market at all, then it has to be stocks. The Germans have always been strange with the bond asset class (which GMF is primarily concerned with).

One of the two authors of this blog post lived in Anglo-Saxon countries for over 16 years and worked in the financial industry there. He can therefore judge the strange German aversion to bonds from his own experience. For an American, no matter what level of education or income he comes from, it is completely undisputed that short-term US government bonds are the safest investment on the planet. Of course also safer than real estate. The average Australian, British or French person sees it similarly with regard to national short-term government bonds. Unlike most Germans.

In the end, it remains unclear why Germans have such a “difficult relationship” with government and corporate bonds. The experiences of the hyperinflation of 1922/1923 or the currency reform of 1948/49 are not a plausible explanation because these currency crises damaged bank deposits just as much as domestic bonds. (We have a detailed one Blog post written to bonds. He provides an overview of bonds and the bond market. Bonds are more complex than stocks and the global bond market is significantly larger than the stock market.)

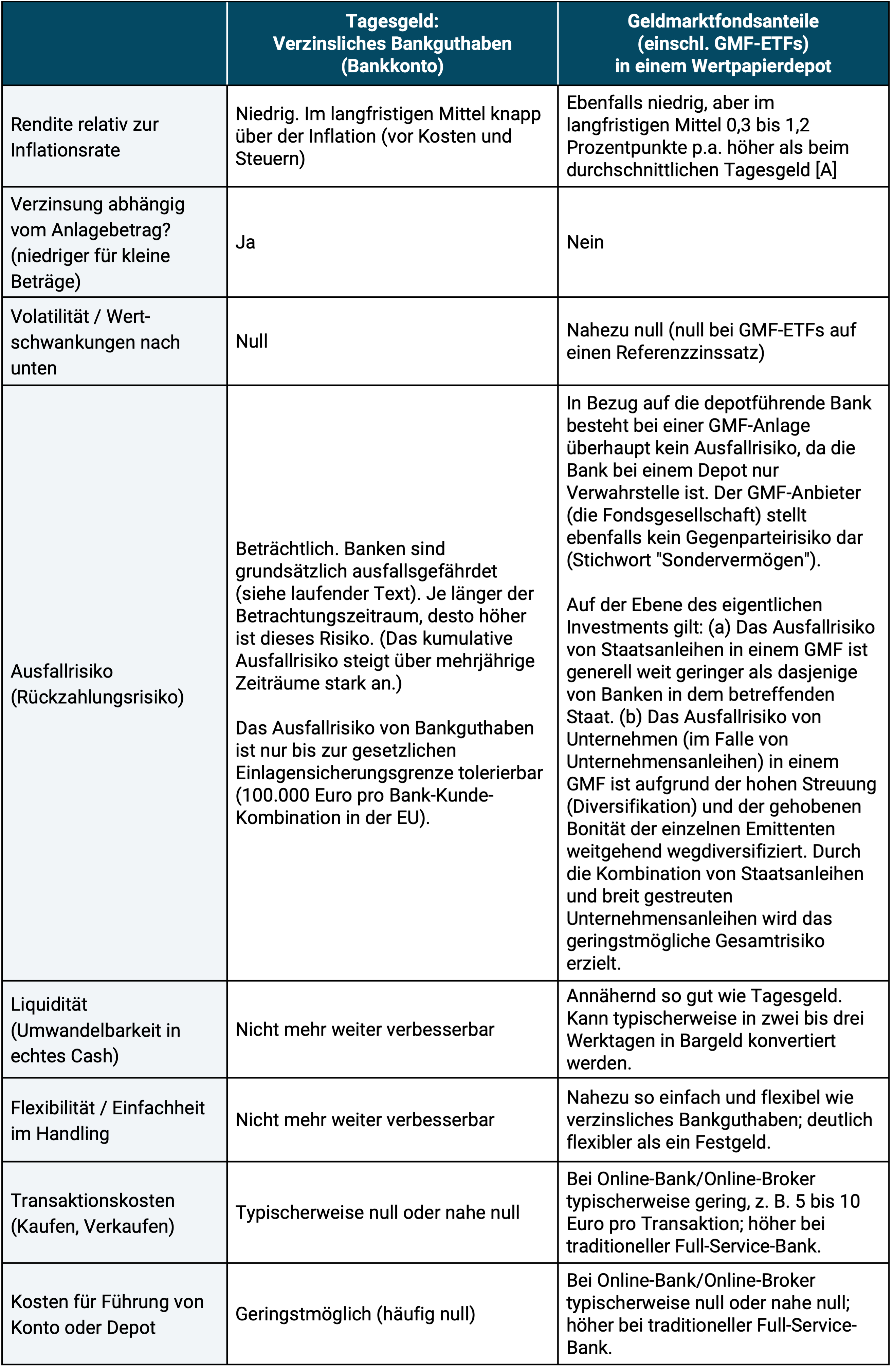

Be that as it may, the following table compares the two “cash investments” bank deposits and GMF and compares them based on the most important criteria.

Table: Comparison of the two main types of “cash investments”: bank deposits and money market funds

[A] In the zero interest phase from the beginning of 2017 to mid-2022, the average nominal interest rate on money market funds offered in Germany was minus 0.4% p.a. compared to an average interest rate on overnight deposits of 0% p.a. The inflation rate over this 5.5 year period was 3.8% p.a.

A money market investment in the strictest sense may not involve any exchange rate risk. Accordingly, a daily deposit in US dollars for an investor in Germany would be euros with the functional currency (“home currency”) no Money market investment, but a speculative “carry investment in the interest rate area”. The exchange rate fluctuations between the dollar and the euro cause strong daily fluctuations in value in euros and thus an unacceptably high level of volatility for money market investments in the true sense of the concept.

There are three types of money market funds

There are three different types of money market funds and money market-related funds:

- Classic actively managed, non-exchange-traded GMF: In our view, they have several disadvantages relative to the better alternative ETF-GMF (see below): (a) Less control on the part of the investor over what their money is invested in. (b) Buying and selling takes two to three business days longer than an ETF GMF. (c) Some actively managed GMFs incur an initial sales charge. Then the purchase costs are often noticeably higher than with an ETF-GMF.

- GMF ETFs that track a bond index (note: the specific names of bond indices are hardly known among private investors): With such a GMF ETF, the fund buys the bonds that the bond index specifies (“physical replication”), just like with most stock ETFs. The bond index can refer to short-term government bonds, short-term corporate bonds, or both.

- GMF ETFs that track a reference interest rate, i.e. not a bond index. Short-term (“variable”) reference interest rates are interest rates that apply in interbank lending and are recalculated every day according to a method specified and monitored by the financial regulator. The best known and most important of these interest rates for GMF ETFs is the ESTR (Euro Short Term Rate). The physical replication method is impossible for ETFs on a reference interest rate for obvious reasons. That's where this comes from Swap method (“Swap” = exchange) is used. With a swap ETF, investor funds are also invested in bonds. The ETF (as a legal entity) pays the income from these bonds to another contracting party, usually a bank, every day at approximately 5 p.m. This in turn pays the ETF the reference interest rate in return (hence “exchange”). This means that, like a normal bond ETF, the investor's money is invested in high-quality bonds. Swap ETFs have an undeservedly bad reputation among some investors, but they are ultimately just as safe as conventional ETFs. An often overlooked, small advantage of GMF ETFs based on reference interest rates is that, like overnight money, they have no risk of price loss at all in the event of a significant increase in market interest rates.

With regard to the mode of use for current income (interest), there are both accumulating GMF and distributing ones.

Money market funds are regularly compared with fixed-term deposits (also known as time deposits) in the media and on the Internet. Since fixed-term deposits – unlike overnight deposits and money market funds – fixed Having terms of between two weeks and three years, they differ in one fundamental feature from money market funds or overnight funds. A fixed-term deposit generally requires more planning security from the investor and involves the risk of loss of returns in the event of poor planning, for example if you want your money earlier than expected. In addition, fixed-term deposits necessarily create more work for the investor.

The criticism of money market funds

The false report that GMF suffered “unexpected losses” during the Great Financial Crisis has been circulating in the financial media and on the Internet since 2008. That is at least a gross exaggeration. First of all, these “unexpected price losses” only occurred in a minority of the many hundreds of European and American GMFs. Secondly, the price losses for the affected funds ranged between 0.5% and 3.5%. So they were manageable, especially when you put them next to the simultaneous crashes in stocks and real estate (real estate outside the DACH countries) in the order of 50% and when you consider that bank deposits in hundreds of banks at the time would probably have fallen by more than half without government bailouts. [5] Thirdly, the current interest rate on GMF in 2008 was three to four percent p.a. If you calculate the interest paid out immediately before or immediately after the price losses against the price losses, hardly any investor lost money.

Such mini-price losses - which statistically occur perhaps every ten years - will mainly occur when interest rates suddenly and sharply rise - an advantageous development for money market investors! Due to the increase in interest rates, the small price loss is quickly made up again. Afterwards, the investor is even better off than before because of the increased interest rates.

Because the mini-price losses caused a media and political shitstorm at the time, the frightened fund providers then implemented voluntary measures that reduced even this moderate risk even further. A few years later, the EU also tightened regulations with the aim of protecting investors.

A strange experience that we have from time to time in connection with GMF is customers who initially reject our suggestion of a GMF investment on the grounds that a bank deposit is safer than the GMF we propose. This mainly contains (German) government bonds and can “fluctuate”. When we asked what would happen if the bank holding the account went bankrupt, such as Commerzbank in 2008 (then the second largest bank in Germany), Hypo Real Estate in 2009 (then the largest German real estate bank) or Credit Suisse in 2023 (the second largest Swiss bank), the client replied that these banks were rescued by the state. This underlines the low risk.

Yes, they were rescued by the state - by the institution whose bonds the customer in question considers to be riskier than a bank deposit. 🤔

But instead of basing your own investment on a voluntary and therefore uncertain rescue operation by the state, it is wiser to invest straight away in the securities for which you have the strongest conceivable legal claim to full repayment by the state: the government bonds themselves. [6] And even this risk can be reduced even further by choosing one or two GMFs that diversify across bonds from several high-quality countries and hundreds of companies.

Bank deposits only make sense in these cases

Against this background, there are only two constellations for rational households in which they hold assets in the form of bank deposits:

- Constellation 1: The bank balance is within the statutory deposit guarantee of 100,000 euros (or 200,000 euros for married couples) and the “guarantor” state has a credit rating of at least AA (or Aa2) from two well-known rating agencies (the third best credit rating). This applies to Germany and Austria, but not to many other EU states. (Wikipedia contains an explanation of credit ratings for the bonds (debt) of companies and governments - see here.)

- Constellation 2: Although the bank balance exceeds 100,000 euros (or 200,000 euros), the excess amount is not covered by the statutory deposit insurance, but only exists for a few weeks or a maximum of a few months. This is therefore only a short-term “parking of money”. This is typically necessary because the owner has received a lot of liquidity in the short term, e.g. B. from an inheritance, the sale of a property or a share in a company and because the implementation of the long-term investment (with less risk of default than with a bank deposit) still takes a certain amount of time.

Conclusion

We can and should assume that a new systemic banking crisis will occur in Europe or worldwide in the next 20 years.

Real state deposit insurance like in the USA does not exist in Germany, the rest of the EU, Switzerland and Liechtenstein. Nevertheless, we can assume that in Germany and Austria 100,000 euros per bank-customer combination in a bank account is actually guaranteed by the state (200,000 euros for married couples).

Whether in the next systemic banking crisis there will be a government bailout of all deposits including those above of 100,000 euros can be questioned for a number of reasons. It is clear that in a crisis that exceeds the magnitude of the one in 2008, the state resources would not be sufficient for a bailout above the 100,000 euro limit. Those in the banks' private, purely voluntary deposit protection systems don't anyway.

Because the security of bank deposits above 100,000 euros is questionable, wealthy private households should, in their own interest, only keep bank deposits within the limits of the two constellations 1 and 2 mentioned above.

Money market fund investments are a superior alternative to overnight deposits and fixed-term deposits. They produce better returns in the long term, with a lower risk of default and virtually the same level of liquidity.

Short list of four money market funds in ETF format:

(a) Passive money market fund ETFs that track a bond index on government bonds (with physical replication) - Currency Euro

- Amundi ETF Gov. 0-6 months Euro Investment Grade: Short-term government bonds from the Eurozone with a rating between AAA and BBB–, physical replication, accumulating, WKN A0RNWC

- Xtrackers II Germany Government Bond 0-1 UCITS ETF: Short-term German government bonds, physical replication, accumulating, WKN DBX0T8

(b) Passive money market fund ETFs that reflect a reference interest rate in euros and are based on the swap method - currency euro

- Xtrackers II EUR Overnight Rate Swap UCITS ETF 1C: Replicates the ESTR reference interest rate + 0.085%, accumulating, swap-based, WKN DBX0AN (the same ETF is also available in a distributing variant)

- Lyxor Euro Overnight Return UCITS ETF Acc: Replicates the EONIA reference interest rate + 0.085%, accumulating, swap-based, WKN LYX0B6

GMF ETFs on corporate bonds are also offered. These bring a slightly higher return than those on government bonds or reference interest rates. However, the return advantage also comes with higher volatility, which can be particularly unpleasant in phases of severe market turbulence.

Important disclaimer: The investment products listed are express not It is not about investment recommendations, but simply about naming some money market funds as examples. Please inform yourself and – very important – read all product documents before making an investment decision.

Endnotes

[1] “Hit lightly” because the vast majority of money market funds have a very short “duration” of less than 12 months (the weighted average term of the bonds contained in the funds). If a fixed-term deposit has a longer term, this can result in a small return advantage.

[2] Here are some other alternative names for default risk: credit risk, repayment risk, credit risk, default risk, counterparty risk, counterparty risk, counterparty risk.

[3] The deposit insurance there is called “Federal Deposit Insurance”. It is a formal government guarantee up to USD 250,000 per bank-customer combination.

[4] A bond is a loan intended for trading (purchase, sale). With a bond, the creditor (lender) can sell his claim to a third party at any time without the consent of the borrower (debtor). This is usually not the case with loans.

[5] At that time there was no EU-wide statutory deposit insurance.

[6] Why a state's bonds are, with rare exceptions, the investment with the lowest risk of default within that state must, do we have here explained.