From Gerd Kommer and Marcel Lauterwasser

Around 40% of Germans' liquid assets are in interest-bearing and non-interest-bearing bank accounts. Since the five-year period of zero interest rates ended in mid-2022 and people are now “finally getting interest again,” this rate is unlikely to fall any time soon. [1] In this context, some households have even developed a new leisure activity for themselves, “call money hopping”, the constant switching back and forth between those banks that offer the most attractive call money interest rates at a given time. [2]

In this blog post, we will use historical data and economic logic to show that, if viewed from an economically correct perspective, you cannot build wealth with interest-bearing bank deposits (current deposits, fixed-term deposits, time deposits), even outside of the zero interest period. At best, you can use it to preserve and conserve assets that already exist. It is doubtful whether all households that transfer money to interest-bearing bank accounts every month for years in order to save for their retirement are clearly aware of this fact.

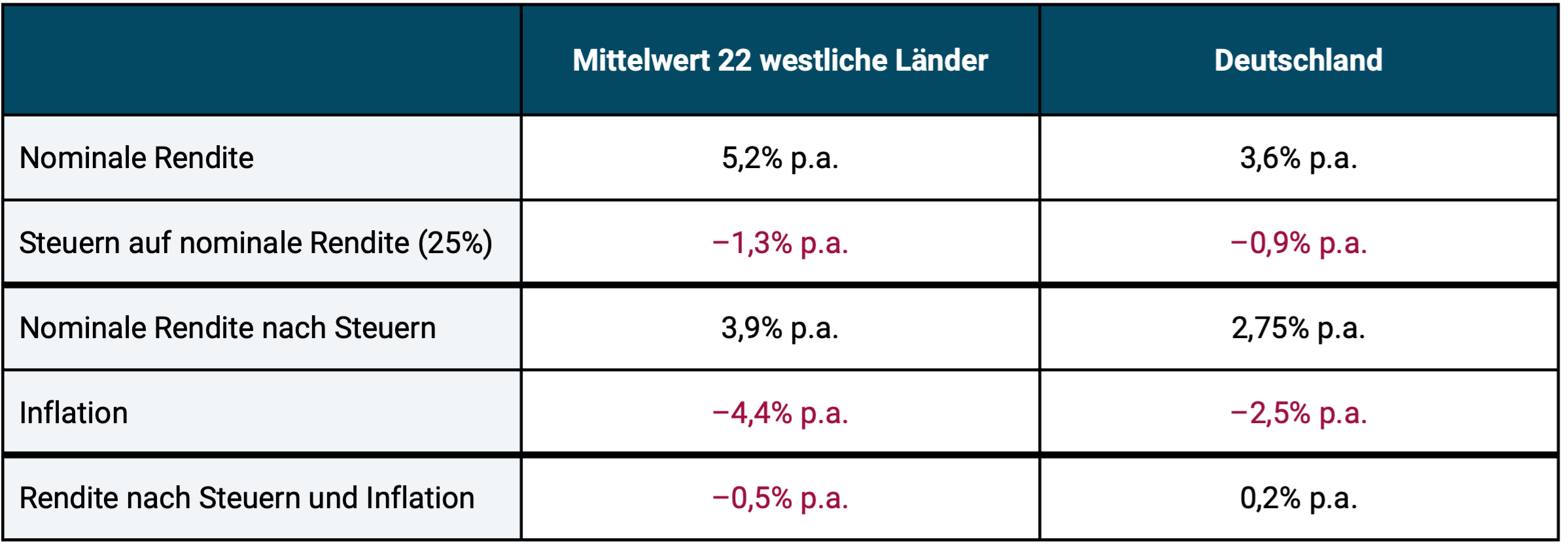

In Table 1 we show that neither in Germany nor in other Western countries could sustainable wealth be created with bank deposits during the 74 years from 1950 to 2023.

Table 1: The average return on interest-bearing bank deposits (money market interest) from 1950 to 2023 (74 years)

► The 22 countries in the middle column are the 22 largest western economies including the USA, Japan, Germany, Austria, Switzerland. The return of 5.2% p.a. in the top line is the simple average of the returns in the respective national currency. The returns are based on short-term government bonds from the respective countries, as no data is available for interest-bearing bank deposits for all countries over the period relevant here. Bank deposits may have had slightly higher pre-cost returns. In return, no bank costs were deducted, which would have absorbed the slightly higher yield compared to government bonds in most countries until around 2010. ► We assumed a tax rate of 25%. ► Data source: Dimson/Marsh/Staunton.

The data in Table 1 clearly shows that anyone who believes that interest-bearing bank deposits can be used to build long-term wealth is making at least one of the following two mistakes:

- Failure to take taxes into account. It is important to remember that the state perfidiously levies taxes on nominal returns, not on real returns, which would be more economically appropriate and ethically fair.

- The failure to take inflation into account, although at the same time it is undisputed that only returns after deducting inflation represent a real increase in purchasing power from the underlying assets. Only real returns are “real” returns.

In the long term, taxes and inflation eat up all or almost all of the return on interest-bearing bank deposits, even at times when nominal interest rates appear attractively high.

See wealth creation where there is none

However, there is an apparent exception to our thesis, according to which interest-bearing bank deposits can be used to build real wealth in the medium and long term. This apparent exception looks like this: As we can clearly deduce from Table 1, in the long term, after deducting taxes and inflation, an interest-bearing bank deposit will most likely produce a zero return or even a slightly negative return, i.e. no real asset growth. So far, so bad.

Nevertheless, a saver - let's call him Ferdinand - who adds new funds to an interest-bearing bank account over a long period of time will see a gradual increase in the nominal balance in that account. This process probably appears to Ferdinand as “building wealth” if he is a typical account saver like Olaf Scholz. [3]

Whether Ferdinand is correct in this perception can be a matter of differing opinion, and we are. First of all, this increase in assets in the account would be substantially smaller if Ferdinand deducted inflation. A very large part of the increase in wealth achieved through nominal interest only represents apparent wealth, since the loss of purchasing power in the meantime is not taken into account. If you subtract inflation from the nominal returns in Table 1 (even without taking taxes into account, which also reduces returns), the inflation-adjusted (real) asset value after 25 years is only about half of the nominal asset value.

An equally weighty argument looks like this: The savings made by Ferdinand in the past through usually painful renunciation of consumption, his existing savings assets, after inflation and taxes, do not produce any appreciably positive returns after inflation and taxes, as we have seen. One can sarcastically derive from this: Ferdinand works long and hard for his fortune, but his fortune does not work for him. It's just plain lazy, so to speak. This means that this saving process, which is difficult for most households, lacks the “soul of investing”, namely the compound interest effect or, to put it more precisely, the fundamental opportunity to benefit from it in any significant way. A bank balance simply provides too low an average return after taxes, inflation and costs to have a true compound interest effect. And in this sense it can be stated that no real wealth creation takes place and cannot take place.

Are the measly real interest rates on bank deposits a rip-off?

If one considers that the bottom two thirds of the wealth distribution in the population in particular hold all or most of their liquid assets in the form of bank deposits, someone could object that this is a bad case of “rip-off” by the banks.

We don't see it that way.

Returns on the financial market are primarily compensation for risk, i.e. “compensation for risk pain”. The three most important forms of risk here are (a) repayment risk (default risk), (b) fluctuation risk of assets (volatility) and (c) illiquidity risk (not being able to convert the value of the investment into cash at a desired time immediately and without serious deductions from the market value).

Yes, a bank balance that is within the statutory deposit insurance limit (the portion of the balance that is de jure or de facto guaranteed by the state) actually represents one of the lowest-risk investments that private investors can achieve with regard to these three risk types. [4] Such a bank balance that is “guaranteed” against default is far less risky than an investment in stocks, long-term bonds, real estate, gold, Bitcoin, raw materials or collectibles and of course also far less risky than financial products that contain these asset classes in a “packaged form”, for example capital-forming life and pension insurance, certificates and investment funds.

If returns are primarily risk premiums and if an investor does not want to take any risk or at least the lowest possible risk on this planet, then in such a case (with bank balances within the statutory deposit protection limit) he cannot logically expect a real return, i.e. a return after deducting inflation, taxes and costs. Against this background, the meager returns shown in the bottom row of Table 1 are not surprising, but on the contrary, very plausible. They will therefore not fundamentally change in the long-term future.

Bank interest rates in bad market phases

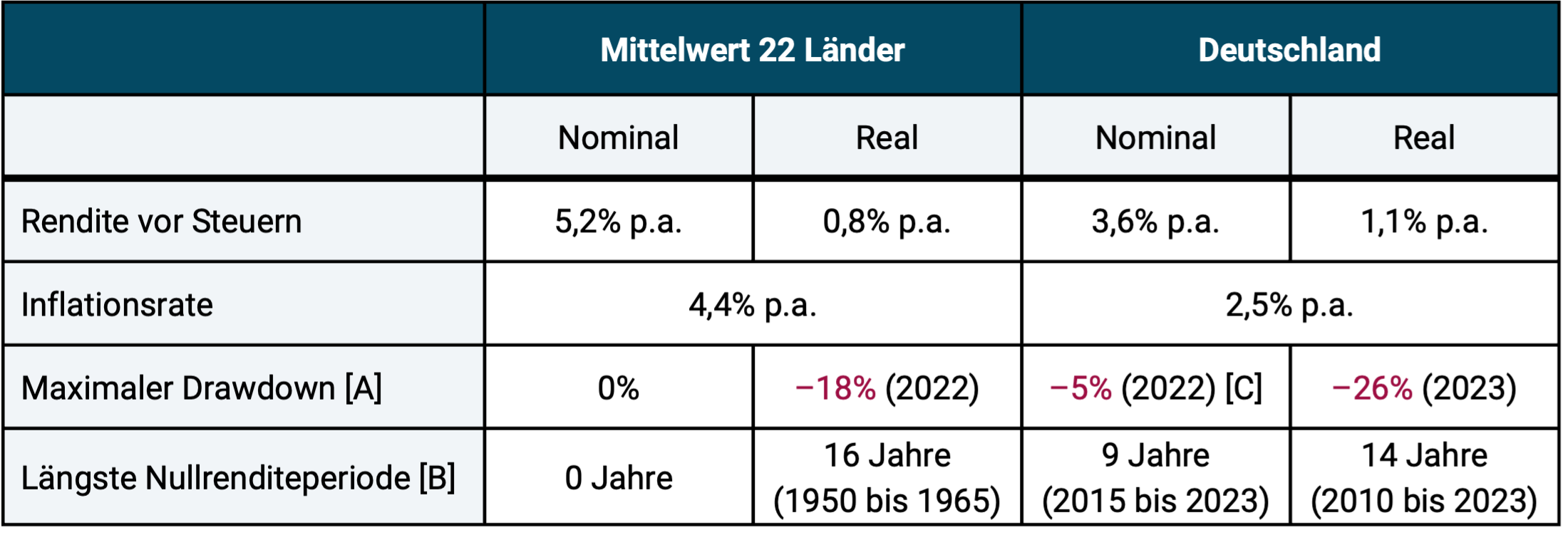

In a certain way, the average returns in Table 1 represent the low attractiveness of interest-bearing bank deposits even too positively. If you, as an account saver, are unlucky enough to make your largest savings in a bank deposit during a period of time that is unfavorable in terms of the market, things will turn out even worse than what Table 1 expresses. We illustrate this in Table 2. It is based on the same raw data and the same period from 1950 to 2023.

Table 2: Return and risk indicators for interest-bearing bank deposits (money market interest rates) from 1950 to 2023 (74 years)

► Middle columns: These are the 22 countries from Table 1 (see there). ► [A] Maximum cumulative (book) loss in the period under consideration. Max drawdown numbers shown are based on calendar year returns. If monthly returns were used instead, these values would be slightly higher. ► [B] For an investment, the period of time between an all-time high and reaching that price level again, when all current income is taken into account. There was, by definition, zero return during this period. ► [C] The negative maximum drawdown in DE is explained here by the “zero interest period” from 2015 to 2022 when nominal interest rates in Germany were negative. On average, the 21 other countries also had positive nominal interest rates during this phase. ► Data source: Dimson/Marsh/Staunton.

The bottom two lines (risk indicators) in Table 2 show that with an interest-bearing bank deposit, adjusted for inflation, you can suffer significant losses over long periods of time. (Taking taxes into account would have only slightly worsened the results in the bottom two lines, because with low nominal interest rates, such as those underlying these worst-case phases, the tax burden is also low.)

The not-so-encouraging findings about bank savings don’t end there. In our analysis, if we were to go back further than 1950, namely to the year 1900 (124 years until the end of 2023), then the average returns would be even lower, the maximum drawdowns would be even lower and the longest zero return periods would be even longer.

The risk of default on bank deposits

We argued above that bank deposits are safe up to the upper limit of the statutory deposit insurance. However, this statement expressly does not apply to amounts in bank accounts above this limit, i.e. above 100,000 euros per bank-customer combination in the EU. If a bank goes bankrupt, depositors may lose some or all of their bank balances above this threshold. [5] This repayment or default risk is underestimated by probably 98% of the population in the DACH countries.

Given the thousands of small and large bank failures around the world over the last 100 years, this could be seen as both bizarre and fatal. Strangely enough, most people who consider themselves to have a high level of commercial knowledge are also subject to the obvious error of equating the zero volatility of bank deposits with a general zero risk. We discussed the risk of default on bank deposits in our own blog post some time ago (here), which is why we will not go into this important aspect for investors any further here.

Now that we have shown the low returns and the risks of interest-bearing bank deposits, the obvious question remains as to for what purposes and in what constellations such investments actually make sense, in other words, when does a bank deposit actually make sense?

The only three sensible constellations for bank savings

Interest-bearing bank deposits make sense in the following three constellations:

- For the “personal liquidity reserve” (PLR), the emergency fund that every household should actually build up before even “thinking about investing”. In terms of amount, the PLR should be between four and ten times the household's average monthly living costs. It is up to the household to judge for themselves which end of this spectrum they would like to be at. It is wise to keep the PLR in your own interest-bearing current account.

- As a “risk-free” (low-risk) investment component as part of a diversified overall portfolio made up of several different asset classes, some of which act as “return engines” for generating real returns and others, such as interest-bearing bank deposits, are responsible for contributing stability or risk reduction in the overall portfolio. Seen in this way, the bank balance is the safety anchor, the airbag in a mixed portfolio. However, the important restriction applies that this bank balance does not exceed the amount limit of the state deposit insurance. To the extent that a household wants to make a larger, low-risk investment (needs a larger security anchor), a better alternative exists, viz Money market funds. We wrote a separate blog post about this (here). Money market funds are superior in terms of returns to interest-bearing bank deposits, they are just a little more “inconvenient” to handle.

- For temporary, short-term “money parking” if a household has just received a large sum of money and even if this exceeds the statutory deposit insurance limit. Such an inflow could come, for example, from the sale of a property, a share in a company or an inheritance. However, the household should then decide within a few months into which other investments the funds just received will flow - investments that represent a better combination of expected returns and default risk than a bank balance above the statutory deposit protection.

Conclusion

Interest-bearing bank deposits are the most popular form of liquid investments in Germany. This is unfortunate with regard to the wealth creation and retirement planning of normal households in the bottom two thirds of the wealth pyramid, because after deducting inflation, taxes and costs, this form of investment is virtually guaranteed to deliver returns close to zero and often even negative returns over long periods of time.

But long-term zero returns on an investment can also be appropriate if they are accompanied by sufficiently low volatility, sufficiently low risk of default and high liquidity and if they have been consciously selected by the investor with knowledge of all their properties, including the real zero return. This can apply in individual cases to interest-bearing bank deposits within the statutory/state deposit insurance, although money market fund investments are slightly superior here.

For investment amounts above the statutory deposit protection, interest-bearing bank deposits are no longer low-risk. Your default risk in this amount zone is unacceptably high.

All in all, interest-bearing bank deposits are only rational if their amount is within the scope of a statutory/state deposit insurance policy or – for investment amounts that are not covered by such a insurance policy – for short, purely procedural-related periods of time until a form of investment that is less risky in terms of default risk has been implemented for the long term.

Endnotes

[1] In the zero interest period from January 2017 to June 2022, the nominal short-term interest rates (money market interest rates) averaged minus 0.4% p.a., the inflation-adjusted real interest rates averaged minus 3.2% p.a.

[2] Such offers are always limited in time and amount. Money hopping requires significant time and effort to frequently open new bank accounts and close old ones.

[3] In an interview in September 2019, then Finance Minister Scholz stated that he would invest his savings exclusively in non-interest-bearing and interest-bearing bank accounts.

[4] The legal/state deposit protection limit in the EU is 100,000 euros per bank-customer combination. There is no corresponding state deposit insurance in Switzerland and Liechtenstein.

[5] The last major systemic banking crisis, in which hundreds of small, medium-sized and large banks around the world went bankrupt (and only through... volunteers survived government support measures), occurred from 2007 to 2011. The last small systematic banking crisis occurred in early 2024, in which the second largest Swiss bank (Credit Suisse) and several medium-sized US banks collapsed. Outside of general banking market crises, individual banks in Germany, the EU and around the world are constantly failing due to incompetence and occasionally criminal acts.

literature

Gerd Kommer / Daniel Kanzler: “Money market funds – the smart alternative to overnight money”; blog post; Oct. 2023, internet location: here

Gerd Kommer / Jonas Schweizer: “The underestimated risk of bank deposits”; blog post; Aug 2019; Internet reference: here