From Alexander Weis and Gerd Kommer

This April 2019 post was updated in July 2024.

In the field of investing, there are many generally accepted insights and concepts that have been repeated for decades in financial industry marketing and in the media and, in recent years, by finfluencers, and yet are questionable or downright wrong. The term “tangible asset” belongs to this category.

The financial industry likes to use this conservative and descriptive term when it wants to improve the sales opportunities for certain investments; Real estate and gold and packaged financial products that contain real estate or gold are particularly eagerly supported in sales with the “theory” of real asset investment. The “tangible investment drum” is also often beaten in connection with the marketing of shares.

Journalists and finfluencers like to use the term because it sounds somehow intelligent.

In this article we will show that the real asset investment concept - as it is commonly interpreted and used - overall hinders rather than promotes the path to rational, long-term successful wealth creation.

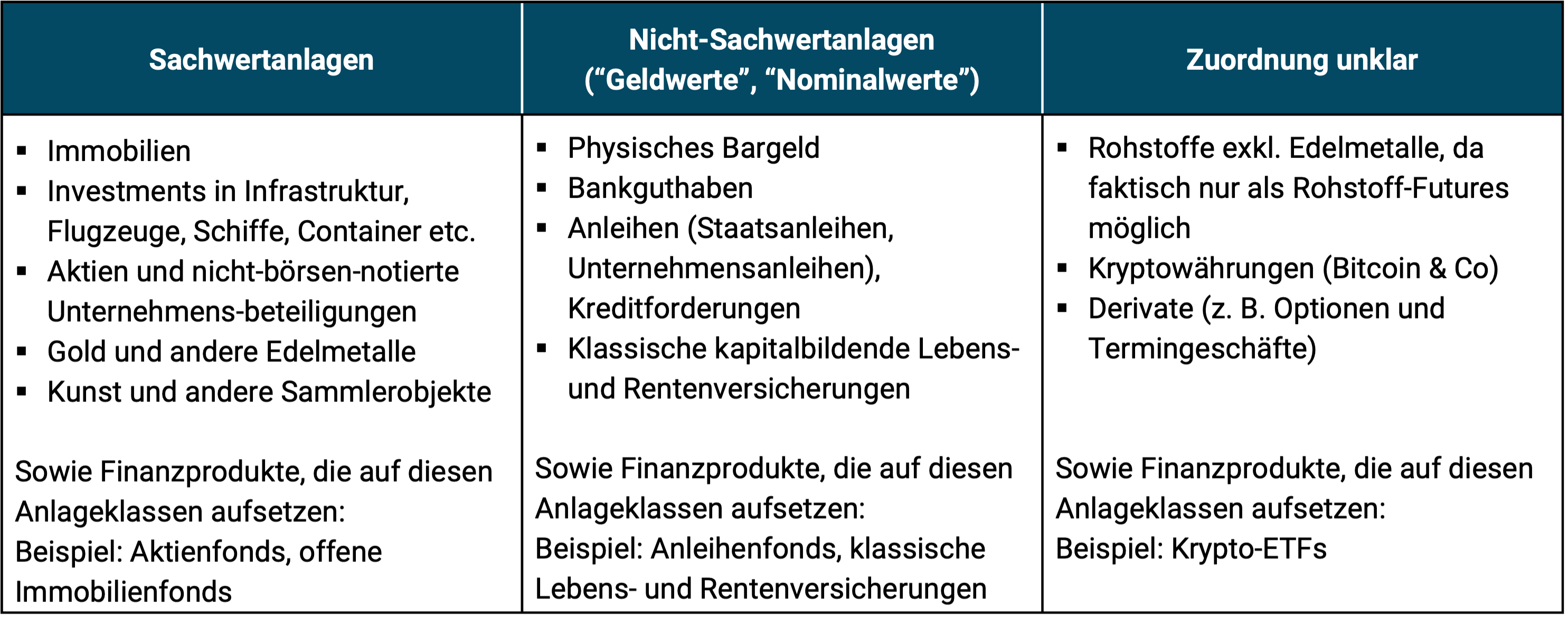

Table 1 below briefly summarizes which types of assets are commonly understood to fall into the categories of tangible assets and non-tangible assets. There is no uniform, clear term in German for non-financial investments; occasionally one comes across the term “monetary values”, which is in itself unclear. Our list reveals, among other things, that there are assets that cannot be clearly assigned to either category.

Table 1: Tangible assets, non-tangible assets and investments that cannot be clearly assigned together form the investable universe

Regarding the right column in the table (“Assignment unclear”):

(a) Commodity investments are typically classified as real asset investments (“SWAs”). This is at best half true or even completely wrong. You cannot invest directly in raw materials for investment purposes. Commodity investments are only possible through so-called collateralized commodity futures – in English technical jargon, collateralized commodity futures. These are the raw material ETFs that you can buy as a private investor. Commodity futures are Futures transactions on raw materials, i.e. derivatives and precisely no direct investments in raw materials (more on derivatives below). Direct investments are called spot market transactions in German. With direct investments in raw materials, storage and insurance costs would be so high that they would completely eat up any conceivable long-term return.

(b) Cryptocurrencies are clearly not “physical” assets, nor are they claims to physical assets and therefore are not SWAs according to the conventional “SWA theory”.

(c) Derivatives are from “underlyings”, i.e. h. Securities “derived” from original securities or assets. Examples are call and put options, swaps or futures contracts. At best, a call option on a stock can be described as a “conditional SWA.” With a put option on a share, even this SWA terminology acrobatics would no longer work.

SWAs, according to advocates of the SWA theory, have several fundamental advantages over non-tangible assets (“non-SWAs”). Briefly summarized, SWAs should have the following advantages over non-SWAs:

- Better protection against inflation and “state manipulation of the value of money” within the framework of the “paper money system” (“Fiat Money” [“Fiat” = Latin “let it be created”). A fiat money system is a monetary system in which the central banks (the state) and the commercial banks produce money, i.e. determine the amount of money in circulation. This system is contrasted by other money production systems, e.g. the classic gold standard or the so-called full money system (for the gold standard see here). It should not be an exaggeration that over 90% of all academic economists worldwide reject the gold standard and the sovereign money system. The likelihood of either of these two systems being reintroduced in a major country in the foreseeable future is effectively zero. In Switzerland, a reintroduction of the full money system was rejected in a referendum in June 2018 with a 76% majority.]);

- Better protection against state expropriation;

- More security in the event of a “system collapse”, e.g. B. a serious, chaotic crisis in the euro zone or a state bankruptcy;

- With SWAs, tax increases or increased costs can ultimately be passed on to buyers/consumers;

- Lower risk of value fluctuations/higher value stability. “value storage function”;

- Higher long-term returns than non-SWAs.

Before we consider these six pro-SWA arguments one by one, let us note that the SWA concept is practically non-existent in academic financial economics. This is an initial indication that from an investor's perspective there is no real usable content in the concept.

A second indication of this is that the SWA concept does not exist in the Anglo-Saxon world. There is only the similar, but less ambiguous and less error-prone distinction between “real assets” and “financial assets”. Real assets overlap with the German term real asset investment, but differ from it in some essential aspects. We'll talk about this below.

Argument (1) – SWAs protect against inflation better than non-SWAs

Inflation protection can be interpreted in two different ways. (a) The existence of a long-term positive real return - that is, a nominal return that is higher than inflation. In English technical jargon this is referred to as “inflation beating”. In other words: the investment in question generates an increase in purchasing power for its owner in the long term. (b) A high correlation of an investment's short-term nominal return with inflation, i.e. monthly returns, quarterly returns or annual returns). In English technical jargon this is referred to as “inflation hedging”. If there is a high correlation, When inflation rises, the nominal return on the investment increases somewhat proportionally (conversely, when inflation falls).

Regarding (a): According to everything that empirical financial economics can say on the basis of data from the last 100 years all Asset classes in Table 1 have a long-term positive real return before costs and taxes, i.e. a long-term return above inflation. Exceptions to this simple statement of facts are at most some specific types of derivatives and cryptocurrencies, for which, due to their historically short existence, it is not yet possible to make any truly reliable statements about long-term returns. In general, an asset class that does not at least slightly exceed the inflation rate in terms of returns in the long term would be of interest to very few people and would therefore soon shrink to zero or a small minimum holding. However, if all asset classes deliver a positive real return over the long term, then there is no fundamental difference between SWAs and non-SWAs in this respect and this distinction becomes obsolete.

Regarding (b): With regard to the short- and medium-term correlation of an investment with inflation, there is no asset class that really reliably protects against inflation (i.e. reliably compensates for inflation in the short term). The only and only partial exceptions are commodities (commodity futures - see explanations above) and inflation-protected bonds with a remaining term of less than 18 months - both of which are non-SWAs. (Until the early 2000s, money market investments (short-term high-quality bonds, money market funds and interest-bearing bank deposits) seemed to have relatively reliably high correlations with the inflation rate, but over the past 15+ years this has no longer been the case.

Argument (2) – SWAs provide better protection against state expropriation than non-SWAs

In our opinion, anyone who seriously and in-depth looks at this argument (risk of expropriation) from its theoretical-legal side and its historical-empirical side can only come to the conclusion that here, too, there is no fundamental difference between SWAs and non-SWAs.

The guarantee of ownership in Article 14 of the German Basic Law applies not only to physical “things” (which could be loosely equated with certain material assets), but of course also to cash and private law (obligatory) claims such as bonds, credit claims, patents, salary and pension claims and many other economic claims, e.g. B. those from derivatives.

Whoever or what the state wants to expropriate on the basis of constitutional regulations or illegal arbitrary decisions will be expropriated. Be it through direct expropriation or through confiscatory taxation. He will not make any distinction between SWAs and non-SWAs - why should he?

Historically, direct or indirect state expropriations in the SWAs of real estate and gold were particularly noticeable and frequent. One thinks of the decades-long so-called Gold bans (expropriations of gold owners below the market rate) that occurred in most western countries in the 20th century: in the USA, Australia, Canada, Germany, Austria and in many other European countries (in the later communist states anyway) - see the keyword “gold ban” on Wikipedia here; One thinks of the property-destroying activities of the German state in particular in the 20th century in the form of the First World War, the hyperinflation of 1922/23, the Second World War, the expropriation of real estate in the GDR from around 1950 and the burden equalization law from 1952 to 1982 (Wikipedia entry here). According to a myth that is repeated endlessly in the German real estate industry, real estate owners benefited from the hyperinflation from 1922/23 through the complete, advantageous devaluation of their real estate loan debts (if they existed). This assessment is mostly wrong. After hyperinflation ended, the government of the Weimar Republic quickly ensured that the relevant loan borrowers, or rather all residential property owners, “paid” for this short-term advantage. This happened through the introduction of the so-called House interest tax, which was collected from 1924 to 1943 (see Wikipedia entry here).

Overall, when it comes to expropriation risk, there is nowhere apparent a consistent difference in impact between SWAs and non-SWAs, much less one that an investor could have historically reliably exploited in advance.

However, if one wants to look for at least marginal systematic differences between SWAs and non-SWAs in this respect, then real estate is likely to have a structural disadvantage compared to other SWAs and non-SWAs among all investment forms in times of severe state crises (war, civil war, national bankruptcy, currency collapse, economic depression or hyperinflation). Firstly, international diversification cannot be achieved by direct investments in real estate for normally wealthy private investors. Secondly, real estate cannot be transferred abroad. Thirdly, particularly high-quality and expensive real estate can be a highly visible object of envy. They and the income from them can hardly or not be “hidden” at all. It is no coincidence that some politicians and journalists on the left have been calling for the nationalization of living space for years, but not of securities deposits.

On the other hand, global diversification is child's play when it comes to stocks, bonds and cash balances. Transferring the storage location of stocks, bonds and cash abroad is generally not a problem (accounts or depots abroad).

Gold does not have to be diversified, but it can also be easily stored abroad.

In general, the movement of stocks, bonds, cash and gold (i.e. mobile SWA and non-SWA) abroad is considered Last resort in the event of the collapse or serious crisis of the home state, both factually feasible and normally legal, at least until a certain point in time before the start of a serious crisis. It goes without saying that such self-defense measures, in particular the relocation of assets abroad, are becoming increasingly difficult and ineffective in terms of state access in times of the increasing number of intergovernmental agreements on the automatic exchange of information (AEOI) and the almost global abolition of banking secrecy; also that not taking into account the income from these foreign assets in the tax return is usually punishable by law in most western countries.

If a wealth tax were to be levied again in Germany, as some parties are demanding, this would of course affect both SWAs and non-SWAs and, from a tax perspective, it would probably be independent of whether the assets are located in Germany or abroad.

Argument (3) – SWAs provide greater security in the event of a “system” collapse, e.g. B. a serious, chaotic crisis in the euro zone or a state bankruptcy

According to the capital market's assessment, a national bankruptcy of Germany, Austria or Switzerland in the foreseeable future is currently extremely unlikely, but even if one does not share this view and considers a collapse of the "system" (Eurozone) in the next few years to be possible or probable, it is not obvious why one should make a systematic distinction between SWAs and non-SWAs in the investment decisions to be made here and now. (DE and AT are currently among the countries with the best credit ratings in the world and are on the same level as Switzerland, Norway, Australia and Canada. For those observers who do not trust the rating agencies, it should be noted that the international capital market is of the same opinion. This is reflected in the comparatively very low market returns, i.e. interest costs from the borrower's perspective, for German and Austrian government bonds but also in other risk indicators, such as the costs for Credit default swaps on the bonds of these countries.)

With a view to a state bankruptcy, it is more relevant to invest in assets that are economically viable outside of the country or region concerned. What is less important ex ante is whether these are SWAs or non-SWAs and in which country (Germany or elsewhere) these assets are held (“deposited”), since the tax authorities of at least Germany, Austria and Switzerland will know this location anyway.

Even more important: If such a doomsday scenario really were to occur, any even remotely realistic observer of modern politics would be guaranteed that the government would be responsible for a “fair” burden all citizens in the sense of the constitutional principle of equality (Art. 3 GG) and taxation based on economic performance and will take “appropriately” into account the motives and potential for capital flight. The wealthier a household is, of course, the higher its burden would be in absolute monetary terms.

On the other hand, if someone believes that the specific form of a household's assets (SWAs versus non-SWAs) would make a fundamental difference and one could now gain a certain advantage by concentrating on SWAs, then in our opinion this shows naivety. In the 21st century, no Western state, no matter how democratic or autocratic, no matter how competent or incompetent, can afford to deviate significantly from the basic political law that “there will be no crisis winners here”.

In connection with discussions about systemic crisis, national bankruptcy and hyperinflation, criticism of the so-called “Keynesian paper money economy”, of “debt-financed economic growth” or – more generally – of the high national debt in some industrialized countries inevitably arises. This criticism comes from the advocates of the classic gold standard, the full gold backing of a currency by central banks or the state (which existed in principle until the 1920s in most Western countries and with restrictions until 1971 for the US dollar). They are skeptical about modern “paper currencies” (these days are all around 180 official currencies worldwide) and/or flatly reject the model of money supply to an economy that has been used universally worldwide since the 1970s, the so-called “fiat money” system. For supporters of this economic school of thought, non-SWAs, especially bank deposits and government bonds, are only “paper” and not “real” values.

In this context it is often argued that all modern currencies such as B. the US dollar, the Swiss franc or the Norwegian krone would have lost over 90% of their purchasing power at the time with the abolition of the classic gold standard after around 1920 (USD 92%, CHF 79%, NOK 95%). That may be mathematically correct, but it is still irrelevant as long as household income real (after inflation) increase in the long term (i.e. increase faster than inflation) and as long as investments have positive real returns. Both have been the case for the vast majority of Western countries and the world as a whole over the last 100 years (see Table 2 below). In addition, real economic growth, i.e. h. the real increase in household income and the real returns on financial capital (stocks, bonds) after Introduction of the paper money system higher than before.

Overall, in the discussion about the economic consequences of the fiat money system and the sustainability of global national debt, ideological considerations mix with pragmatic investment-related questions in the here and now. We cannot address these ideological questions within the scope of this short text. However, for the purposes of distinguishing between SWAs and non-SWAs, we can note that the specific consequences of an ideological rejection of the modern paper money system for one concrete Investment strategy that inevitably today must be implemented for the coming years and decades are by no means “crystal clear”.

A simple, single example: Gold, the “favorite investment” of paper money opponents, had a nominal return of 5.6% p.a. in euros in the ten years to the end of 2023 compared to the global stock market of 11.6% p.a. (MSCI World Standard). Even over the last 20 or 30 years, stocks were ahead at the end of 2023. Adjusted for inflation, gold today (end of 2023) is still trading just below its peak price in January 1980 over 40 years ago. On several occasions over the past four decades, the inflation-adjusted price of gold has been more than 50% below this peak. For more on gold as an investment see here.

Anyone who believes that the state will take a drastic... Windfall profit for gold owners, which would perhaps arise if the gold standard came back (as unlikely as that is), should take the history of the gold bans already mentioned above to heart.

Be that as it may, anyone who wants to protect themselves from a systemic crisis in Germany or the Eurozone, however unlikely, must invest in assets - regardless of whether SWAs or non-SWAs - that lie economically outside these regions, e.g. B. in a globally diversified stock portfolio, in government and corporate bonds from non-Eurozone countries or, if necessary, in gold and raw materials. SWAs based in Germany, such as German stocks or German real estate, especially those that are rented, are likely to offer the worst protection in such a scenario, relatively speaking.

Argument (4) – SWAs allow their owners to pass on tax increases or increased costs to the buyers (consumers/customers, tenants); This option is missing for non-SWAs

We have already dealt with this pro-SWA argument in our recent Blog post “Cash Flow Cascade” and will therefore not repeat the statements there for reasons of space. In any case, this argument, which is often postulated but has never been substantiated with hard scientific logic or empirical figures, turns out, upon closer inspection, to be mere wishful thinking or a confusion of banal tax law administrative techniques (e.g. the tax-technical passing on of the state sales tax to end customers) with really relevant economic ones Fundamentals. The fact is that without taxes the prices for goods and services would be lower, but in return the demand for them would be higher and therefore the relevant corporate profits would be greater. To the extent that the alleged passing on or passing on technically exists, it still reduces the income of companies and landlords. Only someone who has not learned to distinguish between real economic effects and formalistic surfaces can call something like this “real transfer”.

If Siemens or any other company, due to its strong market position, succeeds in passing on increased costs or taxes in whole or in part to its customers (i.e. preventing a decline in profits), then the owners of Siemens bonds (non-SWAs) also benefit from this, not just the owners of Siemens shares (SWAs). If Siemens does not succeed in passing this on, the negative effect for the bondholders will be less than for the shareholders.

In any case, gold as an SWA cannot be said to allow its owner to pass on increased material costs or increased tax burdens on its owners to consumers.

Argument (5) – SWAs are more stable in value and returns than non-SWAs

If you look at the statistical reality over the past 120 years in the 20 or so countries for which historical data of sufficient quality are available, you can only come to the following conclusion: SWAs such as gold, raw materials, real estate and stocks have significantly higher fluctuations in value or returns (volatility) in the short, medium and long term than non-SWAs, such as bank deposits, corporate bonds and government bonds. There is complete agreement among experts on this matter. A numerical proof is therefore superfluous. Only with regard to the real estate asset class (direct investments in real estate) does the fiction of a low risk of value fluctuation persist in the private investor community. This fiction is related to the error in thinking that a risk that is not directly observable (fluctuations in the value of real estate or the equity portion of a property) is lower than a risk that is easily observable (fluctuations in the value of stocks). In this blog post we examined the topic in more detail.

The long-term returns on real estate are already lower than those on stocks and only slightly higher than those on long-term government bonds, as we show later in Table 2 of this article.

Argument (6) – SWAs have higher long-term returns than non-SWAs

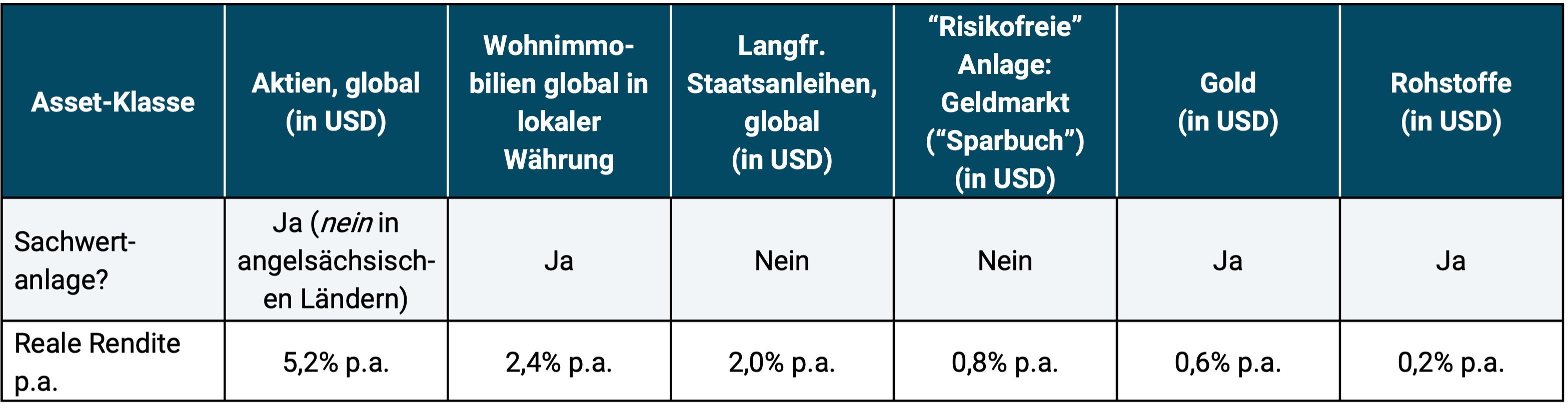

Table 2 summarizes the long-term returns of the main SWAs and non-SWAs. It shows that SWAs, stocks and real estate, generate higher returns over long-term periods than non-SWAs, bonds and money market investments. However, this return advantage is not related to the SWA nature of stocks and real estate, but is the banal result of their higher risk of loss and value fluctuation in the short, medium and long term and, in the case of real estate, also of their illiquidity. The physical assets of gold and commodities, although they fluctuate just as much as stocks and real estate, actually have the worst long-term returns of all major asset classes and, in particular, worse long-term returns than the non-SWAs, corporate and government bonds.

Table 2: Inflation-adjusted returns of major asset classes (SWAs and non-SWAs) from 1900 to 2017 (118 years)

► Before costs and taxes. ► Data sources: Stocks and bonds for 23 countries, money market only USA (One Month Treasury Bills): Dimson, Marsh, Staunton 2018; Residential real estate: 11 countries, Dimson, Marsh, Staunton 2018, supplemented by Kommer/Schweizer 2018; Gold: World Gold Council; Raw materials: David S. Jacks. Raw materials include the five main raw material groups: energy, precious metals, base metals, minerals and agricultural raw materials.

Finally, we will briefly address a particularly curious pro-SWA argument: It is occasionally claimed - and you never know whether it is meant seriously or just as a joke - that the ability to physically touch real estate, raw materials and gold represents an economic or legal advantage over “paper assets” such as stocks, bonds or bank deposits. This argument is almost comically naive. The quality (security and unrestrictedness) of ownership and ownership rights to assets, regardless of their nature, is based on the applicable legal framework and civil and public law protection of the ownership position or legal status. Of course, this applies equally to SWAs and non-SWAs and is in no important way related to the fact that certain assets can be touched tactilely.

At the beginning we mentioned the distinction between, which is widespread in the Anglo-Saxon world Real assets and Nominal Assets. It makes far more sense as an investment analysis concept than the German real asset investment vs. non-real asset investment because it contains fewer errors, ambiguities and misunderstandings and because it is based on a really relevant issue.

Real assets are investments whose total return (increases in value plus current income, if any) is typically not is contractually limited, i.e. e.g. B. Stocks, real estate, precious metals, raw materials, cryptocurrencies. Because there is no contractual upper limit on returns, it is, at least in principle, possible that these assets will suffer little or no damage in terms of returns from high unexpected inflation.

Nominal assets (also sometimes called paper assets) are assets whose total returns are contractually capped. Examples: bank deposits, bonds. Because there is a contractual upper limit on returns, it is very likely that these assets will be damaged in terms of returns by high unexpected inflation.

In the case of derivatives, the allocation to real versus nominal depends on the specific derivative, i.e. on the individual case.

The return effect of exchange rates is fundamentally ignored when distinguishing between real assets and nominal assets.

All in all, the real assets/nominal assets delineation concept is significantly superior to that of tangible assets/non-tangible assets. The latter belongs in the big ash bucket of investment errors and misconceptions, but that doesn't stop the financial industry and the media in German-speaking countries from continuing to market it.

Conclusion

- The concept of investing in real assets is ultimately a mirage in view of its claimed advantages in crisis and inflation scenarios.

- The SWA concept in the sense of the alleged advantages of SWAs over non-SWAs listed at the beginning of this article cannot be proven either factually, historically, statistically-empirically or legally. Taking the classic SWA concept into account when making investment decisions will not improve their results and may even worsen them.

- The repetition of SWA theory in the marketing material of the finance and real estate industry for decades is not because the SWA argument has a technical or solid historical-empirical foundation, but because promoting the supposed advantages of SWAs has a profit-promoting effect for these industries. The financial media, many financial bloggers and advice book authors parrot this nonsense for economic reasons.

- Science has traditionally ignored SWA theory because it is largely knowledge-free.

- In the Anglo-Saxon world there is a distinction between real assets and nominal assets, which is preferable to the German SWA/non-SWA pair of terms.

- Anyone who wants to protect themselves from a systemic crisis in Germany, Austria or the Eurozone must invest in assets that are located outside of this region. The SWA/non-SWA distinction is there ex ante irrelevant.

literature

Dimson, Elroy /Marsh, Paul /Staunton, Mike (2018): “Credit Suisse Global Investment Returns Yearbook 2018”; long version; Credit Suisse Research Institute; 251 pages.

Kommer, Gerd / Schweizer, Jonas (2018): “Better understanding the returns from direct investments in residential real estate”; Internet reference: https://www.gerd-kommer.de/blog/die-reiz-von-investments-in-immobilien/