From Gerd Kommer and Alexander Weis

Note: This post was updated in February 2026.

Any consideration of the return and risk of an asset class should begin with a consideration of its historical return and risk. The general rule is to go back as far as data quality and availability allow. In the case of gold, these returns go back over 200 years or even longer, but there is an exception: return data from before the 1970s should be ignored, because before 1971 gold was the de facto currency in the US, UK and many other countries; This means that for most of these 200 years, national currencies had a legally prescribed, fixed exchange rate for gold - the so-called gold standard.

The price of gold in the currencies dollar, pound, yen, franc, etc. was set by the state and did not fluctuate freely according to supply and demand, as is the case today. If gold and money (the legal tender) are the same thing, gold can naturally only have a return of (near) zero when measured in this currency, i.e. neither a significantly positive nor a negative return. (The fact that gold had a slightly positive inflation-adjusted return even at the time of the gold standard in the 18th and 19th centuries was due to the fact that the gold standard was repeatedly manipulated by those in power.)

The (classic) gold standard was abolished between 1914 and 1933, depending on the country (at different times depending on the country). We have our own economic history story about the classic gold standard and specifically why it probably slowed down economic growth at the time Blog post published.

In 1944, when the end of the Second World War was foreseeable, the so-called Bretton Woods monetary system was introduced, in which only the US dollar had a fixed gold price. [1] Since most other Western currencies in the Bretton Woods regime had a “semi-fixed” exchange rate against the US dollar set by the central bank of the respective country, these currencies also had a “soft” link to the value of gold. There was therefore a quasi-gold standard or “watered down” gold standard, since formally only a single currency was linked to gold, and since the US government neither fixed nor ever published the gold coverage ratio of the US dollar money supply (e.g. 100% or 75% or less).

The Bretton Woods system was unilaterally ended by the US government in August 1971, thereby removing the dollar's gold price peg. With the final abolition of the (quasi-) gold standard, the rules of the game for gold in terms of investment changed fundamentally, because from then on the price of gold fluctuated freely and for the first time moved according to the law of supply and demand on the world market. For gold as an investment, August 1971 marked what statisticians call a structural break.

For anyone who accepts this argument, the price fluctuations of gold that are relevant from an investment perspective do not begin until September 1971 at the earliest. Before this date, the real gold returns were far lower than after. From 1792 to August 1971 (180 years), the real price of gold in USD fell by an average of 0.4% per year - this corresponds to a cumulative price decline of over 50%. From September 1971, gold yields rose sharply compared to the previous 180 years.

However, September 1971 is probably not a particularly suitable starting date for historical gold return benchmarking against other asset classes. The US government and some other Western countries only allowed their citizens to own private gold again at the beginning of 1975. Between 1934 and the end of 1974 there was a forty-year “gold ban” for private households in the USA. [2] In all then socialist countries, including Russia, China and India, the gold ban remained in place long after 1971. To date, China and India are the two countries with the greatest demand for gold in the world. In most years, gold demand from these two states is five to ten times greater than gold demand from American buyers.

Decades-long bans on private gold ownership existed in virtually all Western countries - democracies and dictatorships alike - including Germany in the 20th century. The legal consequences of violating these bans were sometimes draconian; In Germany, private gold ownership could be punished with death in the Third Reich. Similar atrocities continued for decades in Russia and other socialist states. The democratic Weimar Republic also introduced a compulsory levy on privately owned gold in 1923. The National Socialist ban on gold was abolished in the Federal Republic in 1955.

In the three years between the end of the quasi-gold standard (Bretton Woods system) in August 1971 and the legalization of private ownership of gold in the USA in December 1974, the real price of gold in USD rose by 238% or 44.2% p.a. a. One can probably say that structurally abnormal and therefore unrepresentative special conditions prevailed in this phase, which will not be repeated. After 40 years of banning gold, pent-up demand had formed among the US population and other countries, a huge segment of buyers, and the previously foreseeable release contributed significantly to the drastic price increase in the three and a half years to the end of 1974.

Therefore, a historical gold return analysis, if one wants to derive reliable insights for the future from it, should actually only take into account the period after 1974, because it was only from 1975 onwards that conditions had sufficiently normalized. For these reasons, a number of scientific studies - if their data analysis goes back further than 20 to 30 years - use January 1975 as the starting point of their empirical data analysis when it comes to historical gold returns that are potentially relevant for the future, e.g. E.g. Erb/Harvey 2024, Erb/Harvey 2025 or Lohre/van Vliet 2024. [3]

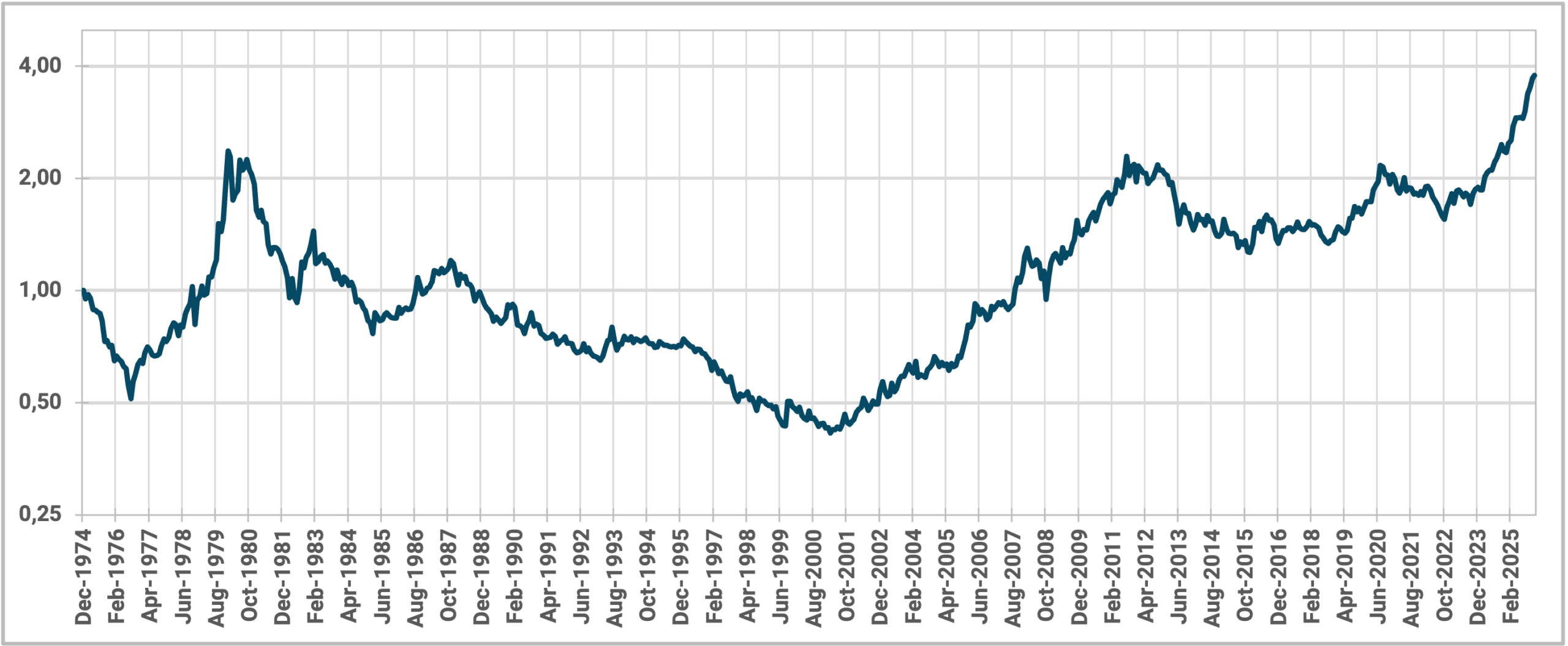

Figure 1 shows the inflation-adjusted gold price in USD, i.e. the gold price in today's money (today's purchasing power).

Figure 1: The evolution of the inflation-adjusted indexed gold price in USD from 1975 to 2025 (51 years)

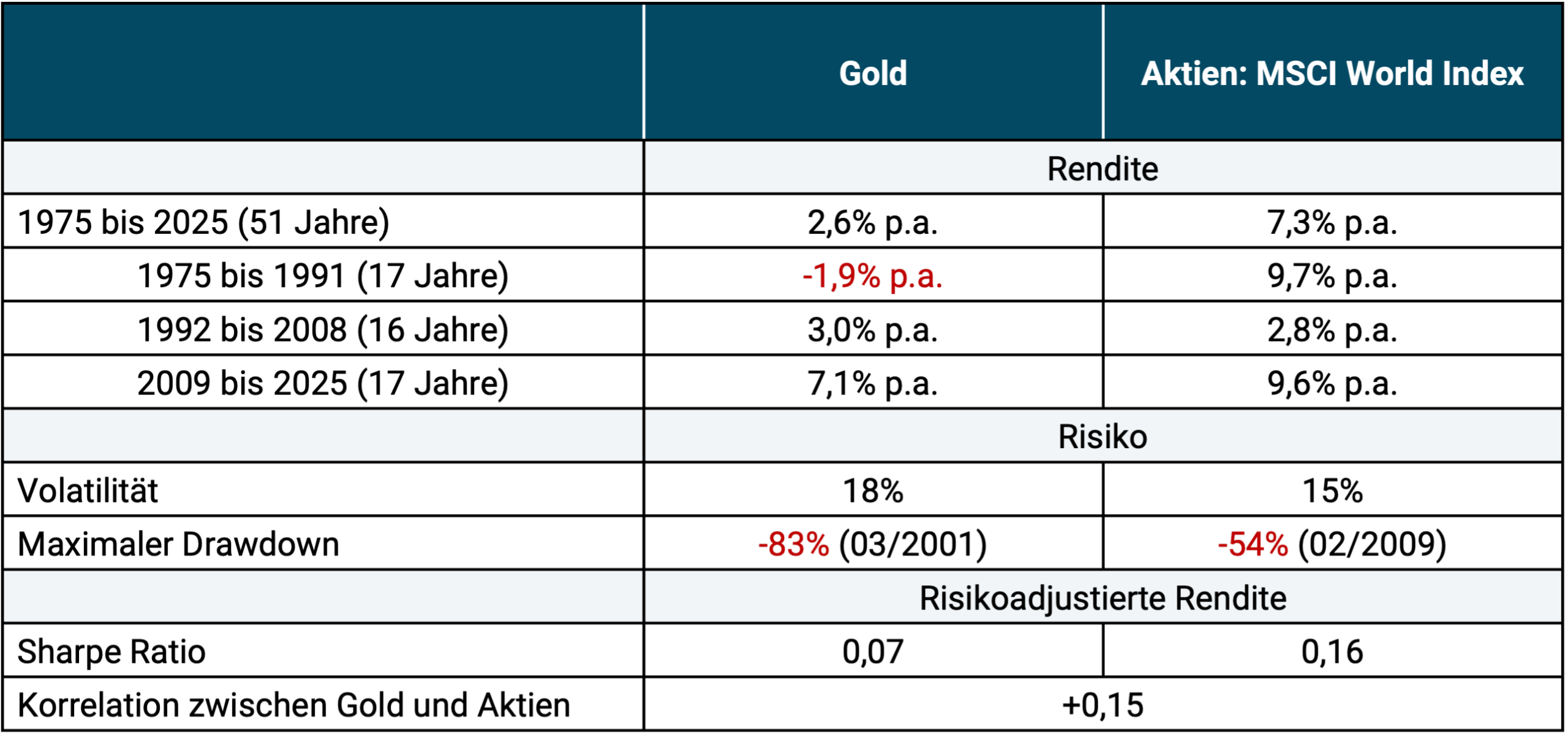

In addition to Figure 1, the following table summarizes some metrics on return and risk compared to stocks.

Table 1: Return and risk of gold and stocks in comparison - in USD, real from 1975 to 2025 (51 years)

► Without taxes and costs. ► Inflation-adjusted returns. ► Volatility = Annualized standard deviation of monthly returns. ► Data: Gold Council, MSCI, Dimensional Fund Advisors.

Some readers may find the gold returns shown in the table surprisingly low, but these are the long-term facts.

We have a historical yield comparison of gold, silver, platinum and palladium in a separate one Blog post employed.

Below we address thirteen other important questions about gold as an investment:

(1) What is the “true” or “fair” value of gold?

(2) Can the price of gold be predicted with sufficient reliability?

(3) Is the price of gold manipulated by central banks or states?

(4) Does gold protect against inflation?

(5) Is it of real relevance that “paper currencies” continue to depreciate relative to gold?

(6) What does it mean that, in gold terms, an upscale suit costs the same today as it did 3,000 years ago?

(7) Is gold a currency?

(8) Could the gold standard be reinstated in the future?

(9) Is gold a “US dollar asset”?

(10) Does gold protect in mega disasters?

(11) Does adding gold to the mix improve the returns of a stock portfolio?

(12) Does gold have tax advantages relative to stocks or bonds?

(13) Are gold mining company stocks a good substitute for investing in physical gold?

Regarding Question 1: What is the “true” or “fair” value of gold?

It is difficult to judge whether the current gold price is high or low, overvalued or undervalued, because unlike stocks, bonds and real estate, gold does not generate any cash flows and therefore has no theoretically determinable “fundamental present value” or – to put it another way – has an “intrinsic value of zero”. For a normal cash flow producing asset, the fundamental value is determined using the so-called discounted cash flow method by discounting future (estimated) cash flows to today. [4] This is not possible with gold. Key figures that are routinely used for stocks, bonds and real estate to roughly assess whether an asset class or an individual investment is over- or undervalued do not exist for gold.

Gold also has no significant industrial use like all other raw materials.

The metrics that some gold bugs (confident gold fans) use to supposedly indicate high or low valuations of gold mostly come from the curiosities of technical analysis and are worthless.

Regarding question 2: Can the price of gold be predicted with sufficient reliability?

No. Anyone who could do that would already be fabulously rich. The gold market, like the stock market, is a very information efficient market. Anyone who tries to predict the price of gold for speculative purposes is entering the world of pure gambling - a game of chance with high participation costs (transaction costs) and an unattractive statistical expected value.

Regarding question 3: Is the gold price manipulated by central banks or states?

This is a conspiracy theory that is so baseless and so simple that there is no need to delve into it. Still, there is a minority in the gold bug community who believe it. In our blog post (here), we will look at this question in more detail.

Regarding question 4: Does gold protect against inflation?

Gold protects poorly against short- and medium-term increases in inflation - just as poorly as stocks, real estate, long-term government and corporate bonds, cryptocurrencies and collectibles. All of these asset classes are bad ones Inflation hedges, d. h. Gold's short-term correlation with inflation (e.g. based on monthly or annual intervals) is close to zero and only marginally higher than that of stocks.

Protect in the very long term all The asset classes mentioned above are ahead of inflation in the sense that they have higher nominal returns than inflation in the very long term.

However, gold would probably be a useful portfolio addition if there were prolonged runaway inflation or hyperinflation. Runaway inflation here means at least a high single-digit annual inflation rate over a period of three years or longer.

In general, commodities (to be precise, commodity ETFs) and inflation-linked bonds with a short remaining term are much better short-term inflation hedges than gold.

Regarding question 5: Is it really relevant that “paper currencies” continue to depreciate relative to gold?

The first thing to note is that all currencies have lost 90% or more of their purchasing power against consumer goods over the last 100 years (if the currency in question has been around that long). This applies to the US dollar, to the Swiss franc, to the British pound, to the Norwegian krone, to the Australian dollar – quite simply to all currencies. Does this play an economically relevant role? No, it doesn't, provided the purchasing power of households increases from their inflation-adjusted household income, and that is exactly what has happened dramatically over the past 100 years.

The per capita economic growth of almost all western countries has been even in the last 100 years after the abolition of the classic gold standard (between 1914 and 1932, depending on the country) higher than in the 100 years before the abolition of the gold standard (see also our separate Gold Standard Blog Post).

The fact that a monetary unit (e.g. a US dollar or a Swiss franc) is now worth considerably less gold units (e.g. ounces of gold) is equally irrelevant from an investment perspective. Exactly the same applies to a monetary unit compared to stocks, bonds and real estate. And even if a particular paper currency had not experienced any inflation in the last 100 years, it would be possible to buy drastically less gold with it today. This is a mathematical side effect of the banal case that the asset in question had a positive real return over the period in question.

Regarding question 6: What does it mean that, calculated in gold, an upscale men's suit costs the same today as it did 3,000 years ago?

This curious phenomenon is referred to in the gold literature as the “Golden Constant” (see e.g. Erb et al. 2017) and is considered by some gold bugs to be somehow very important. The golden constant is probably simply a coincidence. In any case, it has no economic significance. The situation (a constant exchange relation) would not apply to the exchange relationship between gold and other consumer or production goods over the last 3,000 years or the last 150 years. Or the other way around: Such exchange relations, which at first glance seem strangely constant over a historically long period of time, could also be found between a certain amount of real estate or stocks or government bonds (or the annual average income from these) and some consumer or production good X, if you want to waste your time looking for them. The Golden Constant is an economic joke, a funny data artifact with no economic information content. Because this is the case, the golden constant says nothing about the quality of gold as an investment.

Regarding question 7: Is gold a currency?

In an interview in September 2023, Christian Rauch, CEO of Degussa, the largest German gold trading company, said, “Gold is a fantastic currency that retains its value extremely.” The fact that gold is a currency is also claimed on the Internet and in many gold bugs. However, this statement is complete nonsense and no amount of repetition will make it true. Gold was once a currency when the gold standard still existed, but it hasn't been a currency for decades. Today, gold is not legal tender in any of the 195 countries in the world and not a single currency in the world is backed by gold, neither partially nor completely. Gold is also not used for payment transactions. That gold is in a microscopic fraction of all the trillions of payment transactions that take place on this planet every year, the creditor to the debtor voluntarily allowed to settle its debt in gold - i.e. actually and legally entering into an exchange transaction with it - does not make gold a currency. Anyone who says that is also saying that each Barter can create a currency – an absurd thesis. If Mr. Schulze transfers his terraced house worth 400,000 euros to Mr. Maier and Mr. Maier settles his debt by transferring a Ferrari worth 400,000 to Mr. Schulze, the Ferrari is not yet currency. The same applies to gold. It does not become currency because it is used in rare cases in exchange transactions to settle liabilities. Even the fact that central banks hold gold does not make gold a currency. Central banks also hold their assets (their “reserves”) in stocks, bonds and other assets. But none of them become “currency”.

Regarding question 8: Could the gold standard be reintroduced in the future?

In our opinion, the probability of this in the foreseeable future (e.g. the next ten years) is in the subatomic range because the supporters of the gold standard are a tiny minority in politics, science and central banks. And if that were to happen, this reintroduction would probably be accompanied by a previous ban on gold for private households.

Regarding question 9: Is gold a “US dollar asset”?

What is meant is that the dollar exchange rate with other currencies has a structural influence on the gold price, in the sense that a weak dollar tends to cause a rising gold price and a strong dollar tends to cause a falling gold price. This thinking is absolutely wrong, even if this nonsense is spread every day by an “expert” somewhere in the world. Gold and most commodities are economically related to no particular currency at all.

The fact that the price of gold worldwide is quoted primarily in dollars is just a convention, but has no fundamental economic substance; just as distances do not depend on whether they are given in miles or kilometers. Before the Second World War, gold was quoted in British pounds.

Gold would only be a US dollar asset if a very large, dominant share of annual global production and demand came from the US. That is not the case. On average in recent years, the US share of production has only been around seven percent. The No. 1 in production is – by a wide margin – China. When it comes to demand, the USA also ranks far behind China and India.

If a currency always the effect that the price of gold in currency X has a lower return than in the other currencies. This phenomenon has absolutely nothing to do with the US dollar, but is a mathematical triviality. This arithmetic effect would also apply to stocks, iron ore or trouser buttons.

If gold were a USD asset, the volatility of the gold price in dollars would have to be significantly lower than in other currencies. But that is not the case. In reality, gold price volatility over meaningful 10+ year periods is almost identical across different currencies (e.g. USD, Euro, CHF, Yen).

Gold has no specific currency. It is a “global”, currency-independent asset, like Bitcoin, like a mixed commodity index or the MSCI World stock index. Currency-independent assets have their “economic engine” (production, supply and demand) not in a single, specific currency area, but in many currency areas. Global, currency-independent assets can be recognized - in addition to the logic just described - by the fact that their volatility is approximately the same over longer periods of time when measured in different currencies. Nevertheless, the nominal return on gold in different currencies can differ significantly over short and long periods of time (it cannot be predicted).

Regarding question 10: Does gold protect in mega disasters?

The scientific literature has not come to a clear conclusion here (for example, Baur et al. 2010, Bulut et al. 2019, Gomis-Porqueras et al. 2020, Lohre/van Vliet 2024).

In the two greatest catastrophes in the last 120 years, World War I and World War II, the price of gold in US dollar terms fell.

In any case, considerations in this direction could only be convincing if one assigns a relatively high probability to the occurrence of a “mega-catastrophe” in the next few years. Mega catastrophe means, for example, the Third World War, a major war in Western Europe, the national bankruptcy of Germany, the chaotic collapse of the Eurozone or several years of runaway inflation in the Eurozone. From today's perspective, we estimate the probability of these “severe crisis scenarios” to be very low and our knowledge of their conceivable form to be too vague.

Regarding question 11: Does gold as an admixture improve the return of a stock portfolio?

That is unclear. Over the period 1975 to 2025, a 10% gold addition degraded the returns of a globally diversified stock portfolio. In the last 15 years, however, the addition of gold helped with returns and even substantially.

After all: Gold as an admixture (e.g. 10% in a stock-gold portfolio) reduces the risk of the stock portfolio a little (volatility, maximum drawdown), since gold and stocks have a low correlation (see Table 1).

Regarding question 12: Does gold have tax advantages relative to stocks or bonds?

In Germany, yes, if you keep it as a private asset. In most other tax jurisdictions, probably not.

Regarding question 13: Are the shares of gold mining companies a good substitute for an investment in physical gold?

No. Although such stocks have higher long-term returns than gold (like the asset class stocks in general), their returns only correlate comparatively weakly with gold and therefore have a different basic character. Gold mining stocks are “more stocks than gold” (see ours specifically on this topic YouTube video).

Conclusion

Since the gold price began to fluctuate freely on the market around 1975, gold has, all in all, produced a reasonable return, but also a worse return than stocks - with a rather higher risk. Before 1975, the return on gold was lower, but is irrelevant because gold was not an investment asset at that time, but the basis (backing) of legal tender. Accordingly, before 1975 or before 1971 there were completely different conditions for gold price development than today.

There are a surprising number of strange fables circulating among “gold experts” and superficial finfluencers about gold, e.g. B. that it is still a currency today, that it is a US dollar asset, that the price of gold is systematically manipulated by states, that the price of gold can only rise in the long term because the amount of gold on planet Earth is physically limited and many other strange theories.

In our view, gold is not a mandatory component of a retail investor's portfolio, except perhaps (a) for households that believe a "mega-catastrophe" (see discussion above) is significantly likely in the next few years and/or (b) for households that expect inflation in their own currency area to be in the high single digits or higher for three years or more in the foreseeable future.

Endnotes

[1] See article “Bretton Woods System” in the German Wikipedia.

[2] See article “Gold ban” in the German Wikipedia.

[3] In our view, Erb/Harvey are perhaps the world's leading scientific researchers on gold as an investment.

[4] See article “Discounted cash flow” in the German Wikipedia.

literature

Baur, Dirk/McDermott, Thomas (2010): "Is Gold a Safe Haven? International evidence"; In: Journal of Banking & Finance; 34; Issue 8; August 2010

Bulut, Levent/Rizvanoghlu, Islam (2019): "Is Gold a Safe Haven? International Evidence revisited"; January 20, 2019; Internet reference here

Erb, Claude/Campbell, Harvey (2013): “The Golden Dilemma”; In: Financial Analysts Journal, July/August, Vol. 69; No. 42; 2013

Erb, Claude/Campbell, Harvey (2017): “The Golden Constant”; In: The Journal of Investing; Spring 2017

Erb, Claude/Campbell, Harvey/Tadas, Viskanta (2020): “Gold, the Golden Constant, and Déjà Vu”; In: Financial Analyst Journal; 76; No. 4; 2020

Erb, Claude/Harvey, Campbell (2024): “Is There Still a Golden Dilemma?”, May 7, 2024; Internet reference here

Erb, Claude/Campbell, Harvey (2025): “Understanding Gold”, 10 Dec. 2025; Internet reference here

Gomis-Porqueras, Pedro et al. (2020): “Gold as a Financial Instrument”; August 20, 2020; Internet reference: here

Lohre, Harald; van Vliet, Pim (2024): “The golden rule of investing”; In: Journal of Alternative Investments, Volume 26, Issue 3; winter 2024; Internet reference: here