<<< This blog post is also available as a YouTube video. >>>

From Alexander Weis and Jonas Schweizer

An updated version of this article with current data up to 2024 has now been published: “Rent or buy – which is more financially attractive?”. In contrast, this older article also covers the non-financial (lifestyle) aspects of the buy-or-rent decision.

Is it better to buy or rent? The question of whether you should buy a home (apartment or house) during your lifetime concerns almost everyone in our area at some point. For many households, purchasing a home is one of the biggest financial decisions of their entire lives.

The opinion that it is actually always the smarter and more profitable way to own instead of rent is widespread. We have been hearing this mantra for decades from the real estate industry, from banks, from politicians, from financial journalists and mostly from the people who are close to us: parents, grandparents, siblings, friends and colleagues - and it feels like everyone has a strong opinion on the topic. Over the last 15 years or so, the mantra seemed to be true: real estate prices continued to rise and interest rates fell to historically low levels. There seemed to be great returns on homeownership Nobrainer to be and rent only something for the poor or stupid.

In reality, the mantra “buying is almost always economically smarter than renting” has never been true in this form. And it could be particularly wrong for the decade ahead. This blog post will show this against the background of sober historical data and a bit of factual logic.

Gerd Kommer has published his third edition advice book “Buy or rent – how to make the right decision for yourself“ (“KOM”) launched a guide that answers the question “Buy or rent?” examined in his usual cool, rational and strictly scientific manner. He deals with lifestyle arguments for and against home ownership as well as economic arguments.

In this blog post we have briefly and concisely summarized the most important arguments from KOM. The article is still quite long by our standards, but the underlying facts are also demanding, which justifies the length of this text, and you can get through it quicker than with the book.

The question of whether it is better to remain a renter or “upgrade” to become a homeowner can be broken down into two main aspects: firstly there is the economic aspect and secondly there is that Lifestyle-Viewpoint; you could also say the emotional side. First, let's look at the pure numbers; then the lifestyle arguments.

So, now let's finally get started: Should I buy or rent?

About the returns from buying and renting

If surveys are to be believed, then for the majority of (prospective) homeowners (“EHB”), the financial aspect of their desire to own a home is more important than the lifestyle aspect. This is not surprising given the far-reaching consequences of buying a property for average earners. That's why we're now getting down to business: We're comparing the returns that have been available to EHB and tenants over the last few decades under otherwise identical circumstances. The heart of this comparison is the respective final assets of our two “competitors”, i.e. h. who – EHB or tenant – has achieved how much net assets (gross assets minus debts) at the end of the respective observation period. Based on this, we can make a statement about what was more profitable: buying or renting.

Assumptions of our buy-or-rent comparison

For reasons of space, we limit this blog post to a simplified form of the comparison that Gerd Kommer carried out in KOM. We refrain from describing the historical data sets and indices on which the comparison is based in more detail because that would go beyond the scope of our article. If you are interested in this aspect, you should read the book.

In order to be able to make a fair comparison, the same payment flows must of course be assumed for both households, i.e. h. All the money that an EHB invests in its property is invested by the competing tenant, who rents an identical apartment, in a globally diversified capital market portfolio consisting of stocks and bonds (“global portfolio”) on a buy-and-hold basis. (We show how one is set up in our blog post „Investing passively – the basics“.)

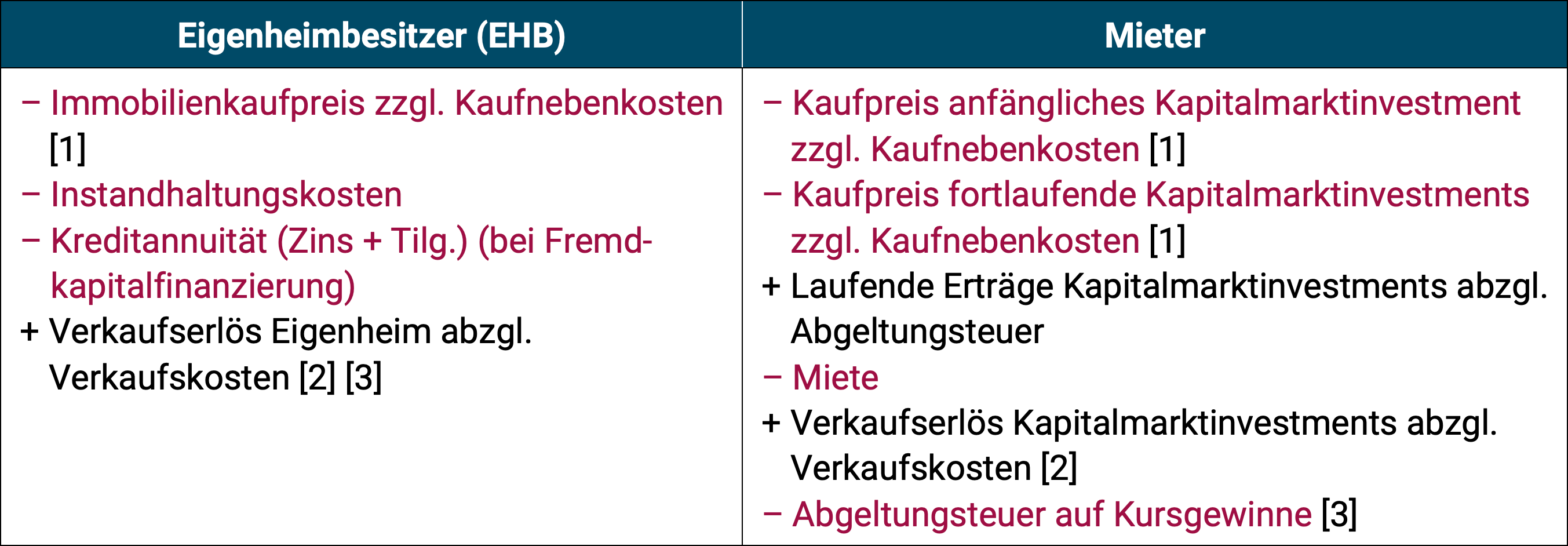

In the following table we have illustrated the relevant payment flows from EHB and tenants. We have placed a minus sign in front of the negative cash flows (expenses) in red and a plus sign in front of the positive cash flows (income) in black.

Table 1: Comparison of cash flows between homeowners and renters

Source: Buy or rent – how to make the right decision for yourself by Gerd Kommer /// [1] Additional purchase costs for real estate are 10 to 20 times higher than for capital market investments via ETFs /// [2] Selling costs for real estate are generally significantly higher than for capital market investments /// [3] In Germany, there are normally no taxes on capital gains for homes that are considered private assets for tax purposes. For capital market investments, price gains are subject to withholding tax - normally 26.4% (and possibly plus church tax).

In prose this means: At the beginning of our 30-year observation period, the EHB buys a property using equity and debt capital, pays off its real estate loan and always invests dutifully in the necessary maintenance in order to sell the home again at the end of the comparison period (a sale is necessary for financial-mathematical comparison purposes). The tenant, on the other hand, initially invests the same amount of equity on the capital market in a 60/40 global portfolio of stocks and bonds, dutifully pays his rent every month and also invests the additional amount that he has left over each month compared to the EHB in his global portfolio. He also sells this at the end of the observation period.

The resulting account balances of the tenant and EHB then allow a conclusion to be drawn about who performed better from an economic point of view with their investment and retirement provision solution. If the EHB still has debts at the end of the observation period, these will of course be deducted, because that's what it's all about Netassets.

But before we take a concrete look at who has historically been ahead in terms of returns, here are a few assumptions that underlie our comparison:

- Tenants and EHB live in an identical property (“apple-apple comparison”);

- the EHB's property costs 100,000 euros and the additional costs amount to 8,650 euros, which it finances 30% from equity (32,595 euros) and 70% from debt (76,055 euros) (we use the unrealistically low amount of 100,000 euros for reasons of simplicity; if one were to assume a million euros instead, for example, this would have no influence on the relative final result);

- the tenant invests the equity share of 32,595 euros initially invested by the EHB in a 60/40 global portfolio consisting of 60% stocks and 40% bonds (we chose the 60/40 split because it is comparable to real estate in terms of risk);

- rent is derived from historical gross rental yields for residential properties (Bulwiengesa data starting in 1970);

- the increase in value of the property corresponds to the house price index for Germany (Bulwiengesa until 2006, then Europace);

- For all other variables (e.g. maintenance costs or purchase/sales costs) we used magnitudes that have been proven in the specialist literature.

Buy-or-rent – the return duel

Now that we have set the stage for our comparison, we present ten historical buy-or-rent comparison calculations in Table 2, including an immediate award ceremony:

Table 2: Comparison of final wealth between homeowners and renters (for ten partially overlapping sub-periods between 1970 and 2020)

Source: Buy or rent – how to make the right decision for yourself by Gerd Kommer /// All numbers nominal, i.e. h. including inflation /// Final asset value in all ten cases at the end of the period specified in the header of the table, i.e. e.g. B. at the end of 1999 in case 1 /// Since a 30-year loan term is assumed until full repayment, in cases 6 to 10 the EHB remains with a remaining loan debt, which is deducted from the market value of the property at the end of the observation period or, in other words: the remaining debt is included in the stated final asset value

The main conclusions from the return and final asset comparison in the table can be summarized as follows:

- In the first six out of ten cases, the tenant was ahead in terms of final assets;

- In the seventh case we have a tie due to the small differences;

- The three out of ten cases in which the EHB was ahead all relate to more recent periods from 2005 to 2020, in which German residential properties recorded unusually high increases in value and loan interest rates were unusually low;

- In absolute numbers, the EHB's lead in cases 8 to 10 is comparatively small compared to the tenant's lead in cases 1 to 6. Although this also has to do with the shorter evaluation periods here, these cases still have to be given less weight in the overall perspective because they are “less significant” due to the smaller absolute difference between the ten cases.

Renting can therefore – from an economic and historical perspective – be just as attractive as buying and has often even been the financially more attractive alternative to owning your own home over the past 51 years. Anyone who is primarily concerned with getting the most out of their money will probably do better by renting than by buying.

But since money isn't everything, as we all know, in the next step we'll look at various lifestyle arguments for the decision to buy or rent, which is so difficult for so many.

About lifestyle aspects of buying and renting

In most cases, the aim of investing is to maximize the return for a given risk, but the resulting wealth gain is ultimately only a means to an end: Basically, it's about how much more life satisfaction you can achieve with the new money you've gained. For this reason, below we look at three arguments for buying or renting from the perspective of a household that wants to maximize its life satisfaction (and not just its return):

Lifestyle arguments for buying 🏠

Pro-buying argument 1: Real estate financing is a “positive forced savings contract”

In our opinion, the strongest argument for buying your own four walls is that, in combination with loan financing, it represents a forced savings contract. Why? After all, a loan has to be paid off – and paid off every single month for a typically damn long period of 20 to 30 years. Anyone who resists this will quickly have problems with the financing bank. This means that you are forced to save month after month for decades, whether you want to or not, and that usually goes hand in hand with a certain reduction in consumption. Tenants also have to pay their rent monthly, but this is usually lower than the EHB's capital service (plus average costs for maintenance, property tax and insurance). The difference could can now be saved and invested in a global portfolio, but can also be squandered for consumption purposes. In contrast to the EHB, saving is voluntary for the tenant. If you consider your savings discipline to be “improvable” and regularly lose the battle against your inner bastard, you will probably do better with a debt-financed property and thus a positive compulsory savings contract than with the combination of a rental apartment and a global portfolio on a “voluntary basis”.

Pro-buying argument 2: Buying offers more social prestige than renting

In our society, purchasing and owning a residential property is often accompanied by an increase in social prestige. Absurdly, this also applies if a property is predominantly debt-financed and, from an economic point of view, belongs to the bank rather than to the EHB. Nevertheless: “100% reputation with 30% deposit” – not a bad deal. The neighbor who rents the identical apartment next door is not only given less respect, but he is also often confronted with pity and well-intentioned advice when he tells friends over dinner how he transfers his hard-earned savings “into his landlord’s pocket” month after month. The fact that this tenant has an ETF portfolio that is worth the same or more than the EHB's apartment minus the debts also rarely earns our tenant admiration from those around him. Over and beyond feel EHB are usually wealthier than tenants, because the human psyche has little use for the concept of debt financing. So if you're concerned about social prestige and perceived wealth, you're probably better off owning an apartment than renting an apartment.

Pro-buying argument 3: Homes offer greater design options

A home can be adapted to personal ideas more easily and to a greater extent than a rental apartment. This fact is trivial and requires no further explanation. However, we would like to point out that tenants also have design options that, with an average rental period of around eleven years in Germany, can not only be psychologically worthwhile, but are also probably economically justifiable in most cases, even for larger sums.

Lifestyle arguments for renting 🌏

Pro-rental argument 1: Renting is less risky than buying

You read that right: Renting in combination with a global portfolio is the lower-risk alternative to buying. Why? First, (normal wealth) EHBs have concentrated a large part of their wealth on a single asset; In economist jargon this is called a cluster risk. Diversification? None. So you literally put all your eggs in one basket. The can of course go well and has been so for the last 15 years, must but it doesn't. It is in the nature of risk that it has to manifest itself from time to time and when it affects my largest asset, that is, euphemistically speaking, not optimal. A tenant with a global portfolio does not have this problem. It can diversify globally across different asset classes such as stocks, bonds, commodities, precious metals and even real estate. Secondly, loan financing significantly increases the risk of an EHB. (If you would like to read this in more detail, take a look at our blog post “The risk of investing in real estate“). And thirdly, an EHB poses a higher risk of being undesirable relative to the tenant Opportunity cost (lost profits). The latter builds a solid bridge to our next pro-rent argument.

Pro-rent argument 2: Tenants are more flexible than homeowners

As its name suggests, real estate is not mobile; they are firmly tied to a specific location. Anyone who buys a property limits their mobility; Every prospective buyer has to keep this in mind and it can also be statistically proven. (Of course, once a property has been acquired, it can also be sold or rented out, but this brings with it a whole range of other problems that we will not go into here for reasons of space.) The negative consequences of immobility can be manifold: Perhaps you cannot take on your “dream job” (or only accept an unreasonable commute time) because it is in another city or even another country. Or you fall in love with another EHB who lives far away and the potential relationship fails because neither one is willing to give up their property for the other. Or you want to start a business, which experience shows is not well compatible with buying a home. And then there was the “dead capital argument”, according to which an EHB lives in a property that is too large for years because its size does not change with his life circumstances (e.g. divorce or children moving out). A tenant, on the other hand, can always choose exactly the apartment size and place of residence that best suits his or her needs (e.g. studies, single or couple apartment, offspring, age-appropriate living or divorce). Renting is undisputedly more flexible than buying - in several dimensions.

Pro-rent argument 3: Renting is less work than buying

A property is a complex physical structure that is continually “worn out” and “damaged” by nature (“wind and weather”) and its inhabitants. In order to compensate or at least slow down this physical depreciation process, someone has to organize the maintenance of a property. In the case of an EHB it is the tenant himself, in the case of the tenant it is the landlord. In other words, renting is a lot less work. In addition, the state, the tax office, the bank and several utility companies for electricity, energy, water, wastewater and garbage constantly confront an EHB with bills, obligations, regulations and new “nice surprises”, all of which mean work. A tenant should only have a fraction of this expense.

Since all of the arguments mentioned above are of a qualitative nature and, in contrast to the introductory return comparison, are difficult or impossible to quantify, everyone has to decide for themselves which arguments outweigh them personally.

If you want to hear more lifestyle arguments when deciding whether to buy or rent, we recommend reading again COM.

Final thoughts on buying or renting

Just over a year ago no one wanted to believe it, but now it's happening: interest rates are rising again. In mid-2021 you still have a real estate loan with a ten-year fixed interest rate for 1.0% p.a. a. now (as of November 2022) almost 4.0% is due again - construction and real estate interest rates have roughly quadrupled in the last year. You don't have to be a mathematician to see that this increase in interest rates cannot work in EHB's favor. Even for those without credit, it is bad because it contributes to the decline in the appreciation potential of all properties.

To make matters worse, residential properties in Germany currently have a higher valuation level than at any time since 1970 (no reliable data is available for the period before that). This makes it unlikely that the increases in value of recent years will continue.

High real estate interest rates and valuations represent an unpleasant combination that can lead to a bad financial deal for prospective EHBs.

Ultimately, the decision to buy or rent of course also depends on the specific property you want to live in, i.e. not only on the conditions under which it is available, but also on whether the desired property is offered for sale or rent.

The common mantra that buying is almost always more profitable than renting in the long term comes largely from the fact that politicians, the media, banks, building societies, real estate agents and our parents and grandparents have been repeating it like a prayer wheel for decades. At the same time, the last 15 years of real estate boom “confirm” the superiority of “concrete gold” and one of many felt The lack of alternatives when it comes to investments and retirement provision reinforce this view.

If you have decided to become a tenant and would like to lend a hand, we recommend our blog post “Investing passively – the basicsIf you don't want to take care of your investments yourself, you could use the Robo Advisor from Gerd Kommer Capital interesting, where you get a world portfolio tailored to your needs and don't have to worry about anything (the minimum investment amount for GKC is currently 25 euros [as of November 2024] and capital investments involve risks).

Conclusion

In this blog post we first showed that renting in combination with a global portfolio has historically been predominantly more attractive than buying. We then examined three lifestyle arguments for buying and renting. Towards the end we offered a number of further food for thought.

The question “Buy or rent?” is probably so difficult to answer because it is a consumer and investment decision at the same time, because the data and the financial mathematics surrounding it are rather confusing, because the financial industry and the media often confuse us with one-sided information and because the whole topic is linked to a lot of emotions. This blog post aims to help make answering this highly personal question a little easier.

(If you are interested in our opinion on real estate in general, we recommend taking a look at the Real estate category on our blog).

literature

Kommer, Gerd (2021). “Buy or rent – how to make the right decision for yourself"; Campus Verlag, 3rd edition, 2021 (first edition 2010); 280 pages

Weis, Alexander; Gschichtmann, Selina (2022): “Passive investing – the basics”; blog post; September 2022; Link: https://gerd-kommer.de/blog/passiv-investieren-die-basics/

Kommer, Gerd; Kanzler, Daniel (2022): “Leveraging stock investments with credit – does it work?”; blog post; November 2022; Link: https://gerd-kommer.de/blog/leverage-effekt/

Kommer, Gerd; Schweizer, Jonas (2018): “The risk of investing in real estate”; blog post; August 2018; Link: https://gerd-kommer.de/blog/das-risk-von-direktinvestments-in-immobilien-besser-verstanden/

Kommer, Gerd; Schweizer, Jonas (2018): “The return on investments in real estate”; blog post; Oct 2018; Link: https://gerd-kommer.de/blog/die-reiz-von-direktinvestments-in-wohnimmobilien-besser-verstanden/