From Gerd Kommer and Maximilian Bartosch

This blog post was updated in September 2025.

In the eight years since our company was founded, our consulting practice has often shown that our clients - a probably representative sample of wealthy private households in German-speaking countries - overestimate the long-term increases in value of the residential real estate asset class. The fact that this tendency to overestimate also exists in the general population has been confirmed in academic studies and opinion surveys. It applies to both property owners and tenants.

Against this background, this blog post aims to compare “facts and fictions” regarding the long-term price increases of residential real estate.

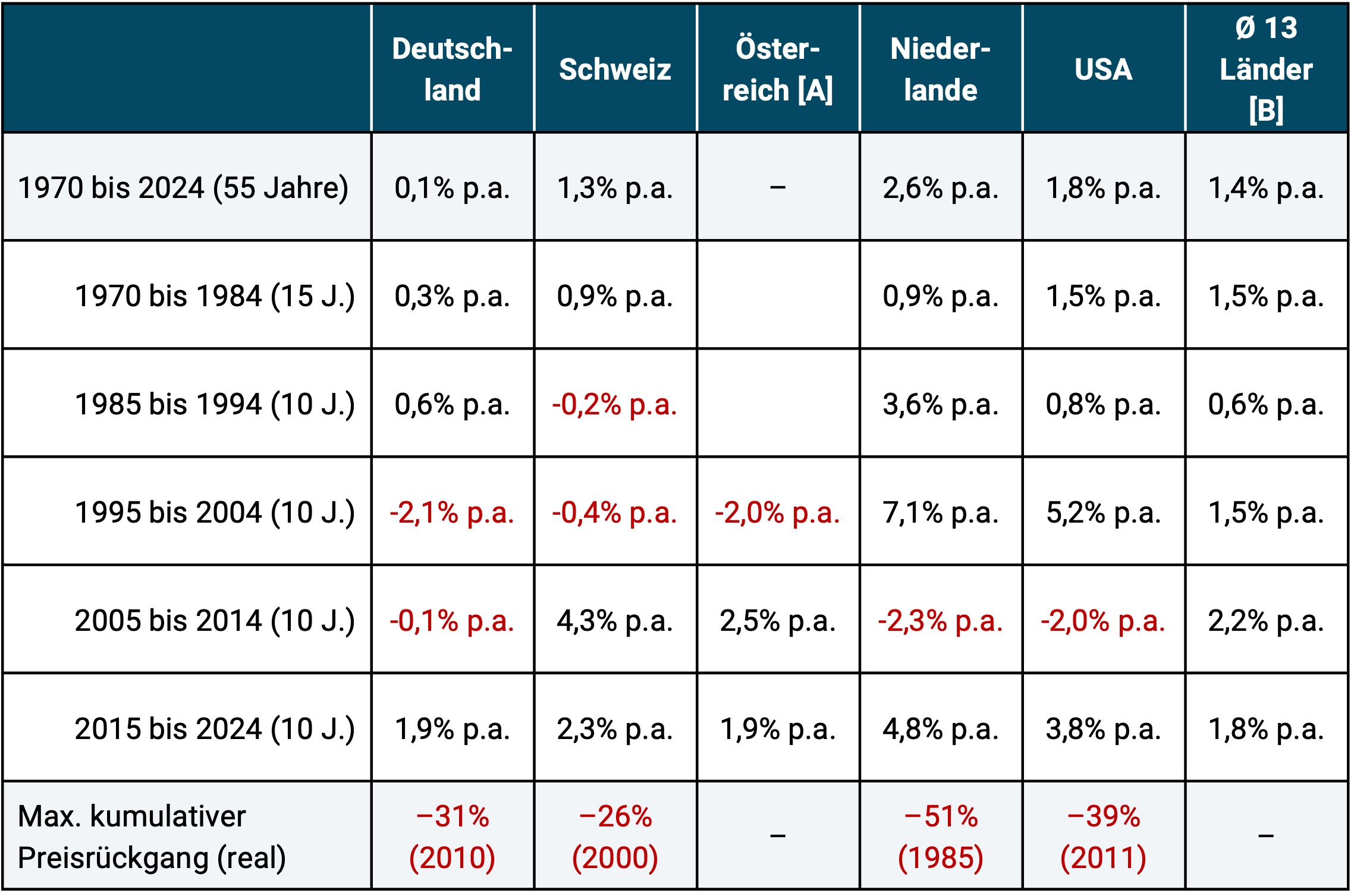

The following table shows the inflation-adjusted (real) increases in the value of residential property in 13 Western countries from 1970 to 2024 (55 years). Five countries (DE, CH, AT, NL and USA) are highlighted individually in the table and the population-weighted average for all 13 countries is also shown.

Table: Real increase in the value of residential properties in 13 countries, 1970 – 2024 (55 years) and maximum cumulative loss in value

► No transaction costs for buying and selling. ► All returns in local currency. ► German inflation over these 55 years was 2.7% p.a. ► [A] Data for Austria only available from 1987. Therefore, no maximum cumulative loss is shown here. ► [B] Weighted average from the countries DE, CH, AT, NL, USA, France, Italy, Spain, Great Britain, Sweden, Australia, Japan, South Africa. Individual countries weighted by population share of the total population of all 13 countries. ► Data source: Bank for International Settlements (BIS) in Basel.

The following insights can be derived from the table:

- Over the long term, residential property value appreciation is lower than many of us believe. We will explain below why we tend to overestimate increases in the value of residential real estate.

- Among the 13 countries on which the table is based, Germany held the red lantern with an average price increase of 0.1% p.a. over these 55 years - less than Japan with 0.4% p.a.

- In all countries, the increases in value over these five decades were not uniform, but varied considerably over time. The data shows that national real estate markets can easily decline in real terms for ten years or more (individual properties will show even more extreme upward and downward trends). By far the best decade for Germany since 1970 was the decade from the beginning of 2012 to the end of 2021. From the beginning of 2022 to March 2025 (last available data point), residential property prices across Germany fell by 27% in real terms.

- Increases in the value of real estate are subject to what is known as “regression to the mean”. Phases of particularly high price increases tend to be followed by phases of lower increases or even price declines. Conversely, phases of particularly low price increases tend to be followed by larger price increases. This statistical phenomenon (regression to the mean) can be seen with the naked eye in the table. It can also be demonstrated more formally using sophisticated statistical techniques (Glaeser 2013).

- The single most important reason why value increases in Germany in the twelve years from 2010 to the end of 2021 were exorbitantly high by historical standards was that they were exorbitantly weak in the previous 40 years from 1970 to 2009. This actually banal fact is regularly ignored in the discussion about price increases in Germany. At the end of these 40 years of actually disastrous performance on an international scale, residential real estate in Germany was simply “incredibly cheap”. At some point, things had to go back up significantly from this historic low; the only question was when and how quickly. The fact that interest rates continued their falling trend from 2010 onwards (which had already started many years before) also helped, of course, but was of secondary importance in relative terms.

- Housing prices can crash - just like stocks. However, a crash in real estate typically occurs more slowly than in stocks and is often not perceived as a crash because of this slowness. Some crash examples (all figures adjusted for inflation): USA over six years from 2006 to 2011: minus 39%, Ireland over seven years from 2007 to 2013: minus 57%, Netherlands over eight years from 1978 to 1985: minus 51%, Japan over 20 years from 1990 to 2009: minus 49%, Germany over 30 years from 1981 to 2010: minus 31%.

Below we put the historical data we have just summarized into an explanatory context by briefly addressing 14 questions relating to the topics of “long-term increases in the value of residential property” and “structural factors influencing residential property prices”.

(1) Is the index data shown here reliable?

Yes, the data is reliable. They come from the most reputable and well-known data providers in the respective countries and are documented by the Bank for International Settlements (BIS) in Basel and are freely accessible on their website. The figures shown in the table are likely to distort the actual increases in the value of residential properties upwards by around half a percentage point per annum because quality improvements and growth in living space in the properties on which the indices are based have not been completely filtered out over time (Dimson et al. 2018). Also important: These numbers do not include transaction costs (costs of buying and selling), which are approximately 50 times higher for real estate than for stocks.

(2) What were the increases in residential property values before the 1970s?

Significantly lower than from the 1970s. The main reason for the global increase in price increases from the early 1970s was the emergence of the international ecology movement at that time. It led to a shortage of building permits and thus to an important price-increasing effect that had not existed before.

(3) Are increases in value in large cities systematically higher than increases in value in rural areas?

No. Many people believe this, but it cannot be proven by long-term data. In some five years or decades in a given country or region, increases in value in large cities are higher than in rural areas (such as in the decade just ended in Germany), but they are just as often lower. The fact that real estate prices in large cities are always noticeably higher than in rural areas does not mean that they generally rise faster. Rental yields in large cities are structurally lower than in rural areas because the rental risk is lower in large cities.

(4) Is urbanization (greater population growth in large cities than in rural areas) the norm?

No, in developed countries “urbanization” is decreasing in the very long term if urbanization is defined or calculated correctly. So is e.g. B. the proportion of the population living in large metropolises is lower today in most developed countries than it was 30 or 50 years ago. A lasting urbanization trend can only be observed in developing countries - until these countries have reached a certain level of prosperity. Then the structural urbanization trend ends there too.

(5) Are increases in the value of high-quality properties systematically higher than the increases in the value of simple, low-value properties?

No, if anything the opposite is the case. Anyone who adheres to this misconception confuses expensive with profitable.

(6) Are the general statements in this blog post qualified by the fact that each property is an individual case?

No. For every property that performed better than the averages shown here, there is another that performed even worse. The vast majority of individual properties are priced very similarly to the market. We estimate that less than ten percent of all properties have a significant price increase or decrease from the overall market.

(7) Is it possible as an investor to systematically (i.e. reliably) pick out attractive properties and avoid unattractive properties?

Possible, yes, but not likely. In any case, professionals don't seem to be able to do it systematically. As an example, consider the poor development of the share prices of well-known listed real estate companies in Germany over the last five years (Vonovia, Deutsche Wohnen, LEG, TAG, Adler and others). And believing that the implementation of a profitable real estate project in Germany over the approximately 15 years up to the end of 2021 is sufficient proof of competence and ability is not itself a sign of cognitive competence. In these 15 years, almost everyone in Germany was able to earn well with real estate. Skill was not a necessary prerequisite for this. Just like you didn't need skill to triple your money in stocks in four years from 1995 to 1999.

(8) Are value increase data that go back further than, for example, 25 years relevant at all for today and the future?

Yes, they are. Looking only at data from, say, the last 20 years would be unwise. Over the past two decades, real estate in most Western countries has experienced exceptionally favorable, “abnormal” macroeconomic conditions. The global decline in interest rates, which will last until the end of 2021, has never occurred before in a similarly strong and extended manner in the last 100 years.

Only house price data from around 1970 may no longer be representative today. As already mentioned in point 2, long-term residential property price increases were significantly lower before the 1970s than after. The reason for the increase in price increases from the beginning of the 1970s was the emergence of the global ecology movement at that time. It led to a structural shortage of building permits and thus to an important price-driving effect that had not existed before.

(9) Why has Germany had lower residential property price increases in the 55 years since 1970 than the 12 other countries included in the table?

The four most important factors are probably: (a) The almost uniquely high level of tenant protection in Germany. (b) The government building regulations with regard to energy, fire protection, accessibility and environmental protection, which are unprecedented in Germany. Overall, they lead to particularly expensive construction. (c) Compared to many other countries, social housing construction by the state or by private individuals with state subsidies is more extensive and of higher quality. [1] (d) The public consensus in Germany, which existed until the noughties, that the statutory pension was sufficient as a retirement provision. Such a view has hardly existed in any other country.

(10) Why do so many private households – perhaps most – overestimate the long-term increases in value and returns of residential real estate?

This has the following main causes: (a) The confusion of uninformative nominal increases in value with really relevant real increases in value. (b) The conflict-of-interest “real estate propaganda” of those institutions that earn money from the sale and financing of residential real estate and services related to real estate investments: banks, brokers, property developers, real estate book authors, providers of courses on investing in real estate. (c) The lack of daily visible, real market prices for real estate. Unlike securities, these are not listed on the stock exchange. For a given year or decade, this allows the owner to have almost any idea about the returns and stability of their investment - without a reality check. (d) In no other investment class are emotions and facts as closely intertwined as in real estate. Apart from gold, they are the only important financial investment that one can “touch” and to which normative categories such as “beauty” or “family connection” can be applied. (Try to imagine a “nice” bond, stock, or “nice” commodity ETF.) However, the mixing of emotions and facts often prevents a purely fact-based assessment of reality.

(11) Could it be that Germany has “catch-up potential” in the long-term appreciation rate of residential real estate to get closer to the international average?

Unlikely. Residential real estate markets are not internationally integrated, as is the case for capital markets. Each national real estate market has its own laws: real laws, economic laws and cultural peculiarities. In addition, there is hardly any cross-border “arbitrage” between national residential real estate markets. A Londoner or Stockholmer who finds property prices there too high will still not buy anything in Berlin or Cologne, where prices may be lower.

(12) In the media, day in and day out, you read about “housing shortages” and even “housing shortages” in Germany. Shouldn't this lead to rising residential property prices in the medium and long term?

The term “housing shortage” is more of a political battle term than reality. The fact is that 99.7% of all people in this country have an apartment. In addition, the average living space per citizen in Germany is higher than in the vast majority of countries on the planet (this living space per resident has almost quadrupled since 1950). Germany also ranks high in the world when it comes to the physical quality of living space.

Those who fantasize about “two million missing homes” or the need to “build at least 400,000 new homes per year” almost never substantiate how they derive these figures. Such numbers are often simply copied or parroted from somewhere else.

In the long term, perhaps starting in just a few years, the demand for living space in Germany will fall due to demographic factors and the supply will grow at the same time. The latter even without increased new construction activity, since the baby boomers - those who are now between 55 and 70 years old - are exposed to ever increasing death rates due to age. These age groups now live in above-average living spaces due to their wealth and biography. These areas will then gradually come onto the market – slowly at the beginning, then faster and more extensively.

Economist Andreas Beck recently provided interesting insights into the “housing shortage”, the supposed lack of construction activity and the demographic factors influencing the real estate market this interview expressed.

(13) Do the skyrocketing construction costs ensure that real estate prices will rise in the long term?

No. What primarily determines prices in a reasonably functioning market is supply and demand backed by purchasing power, but not production costs. If the production costs are above the equilibrium price of the market, then prices do not rise, but supply falls. Exactly what we are currently observing in the market.

(14) What will have the greatest influence on the short and medium-term development of the German residential real estate market?

Here we will not surprise any reader by naming the level of loan interest rates as the most important single influencing factor. Currently (August 2025), the interest rates for ten-year fixed interest rates are around 3.7 percent p.a. This is almost three percentage points higher than the corresponding interest rates at the end of 2021, but is still low and has some potential for further increase for two reasons: Reason No. 1: The average loan interest rate level from 1970 to today was 6.2% p.a. In other words, the current interest rates are historically low. Reason No. 2: Due to the high global government debt ratios, as well as the debt ratios of companies and private households, a structural increase in long-term interest rates cannot be ruled out.

The fact that valuations (as mentioned above) are still in the upper range, at least in large cities and attractive locations, could also have a negative impact on the development of property prices in the short and medium term.

(15) If one were to consider total returns on residential properties, not just increases in value as in this blog post, would a fundamentally different picture emerge?

Total returns on real estate are those that take into account all factors affecting returns: increases in value, additional costs of purchase and sale (including real estate transfer tax), maintenance costs, insurance costs, property tax and gross rent. In the case of real estate that is partially financed by credit, the debt service for the loan is added; also income taxes, if there is a tax liability.

Although there is a serious data problem when it comes to rental yields and maintenance costs that go back further than just a few years, one can deduce from the available data that the long-term total returns on residential real estate are significantly below those on stocks and slightly above those on long-term government bonds. The fact that real estate is easier to purchase does not change this basic fact.lever(leverage) can be better than other investments. We go into detail about the total returns on residential real estate in our blog post “The return on investments in real estate” (see link below).

We have highlighted further economic aspects of real estate investments in the previous blog posts linked below.

- “Maintenance costs – how to calculate real estate investments”

- “The return on investments in real estate”

- “The risk of investing in real estate”

- “Are rental properties attractive investments?”

- “Open-ended real estate funds – illusion and reality”

- “Rent or buy – which is more financially attractive”

From a self-user perspective, total returns over the past 50 years for Germany and other countries are in the book Buy or Rent (2021) presented by Gerd Kommer.

Conclusion

In the long term, the increases in the value of residential real estate are lower than many private households assume and promote than those who earn from financing and selling real estate. The high price increases in the German residential real estate market in the 12 years from 2010 to 2021 were an upward outlier, a historical anomaly.

In the long term, demographics in Germany will act as a structural headwind, dampening the development of residential property prices. The market will begin to price them in several years before these demographic factors become clearly felt in the real economy.

literature

Dimson, Elroy/Marsh, Paul/Staunton, Mike (2018): “Credit Suisse Global Investment Returns Yearbook 2018”; long version; Credit Suisse Research Institute; 251 pages

Glaeser, Eduard (2013): "A Nation of Gamblers. Real Estate Speculation in American History"; In: American Economic Review; 103; No. 3; May 2013; pp. 1-42

Kommer, Gerd (2021): “Buy or rent – How to make the right decision for yourself”; Campus Publishing; 3rd edition; 2021; 285 pages

Endnotes

[1] There is also extensive social housing construction with affordable rents in a number of other Western countries, but these properties are probably significantly worse than in Germany in terms of their combination of location, size and construction quality.