From Gerd Kommer and Selina Gschichtmann

Germany and Austria have an old-age poverty problem that will only get worse in the future due to the well-known plight of the statutory pension insurance systems. If you as a normal citizen, especially as a person in the first half of life in the wealth accumulation phase, want to individually avoid this problem, wealth creation via the global stock market is the best option. This is particularly true for the lower-income half of the population, as the most common wealth creation alternative to the stock market - the loan-financed purchase of a home (house, apartment) - is rarely available to them due to poor creditworthiness. [1]

The stock market has existed for more than 200 years and has been easily accessible to normal households in Germany, Austria and Switzerland since the 1950s. This accessibility has become even easier and cheaper, particularly in the last two or three decades.

Nevertheless, today only around 15% of all German households own stocks or stock funds, compared to around 66% of American households. This is one of the reasons why the net worth of the median American is far higher than that of the median German. [2]

A main reason for Germans' lack of interest in the stock market is probably their general skepticism towards the market economy, or “capitalism”. The stock exchange is a central element of the market economy. According to a cross-national survey, among respondents in 34 countries, only those in 11 countries view capitalism, the market economy, more critically than the Germans, while people in 22 countries are less anti-capitalist or even pro-capitalist (e.g. Poland, USA). [3]

Anyone who is skeptical about the market economy or generally rejects it is unlikely to acquire either knowledge or practical skills in dealing with market economy forms of wealth creation, e.g. B. Basic knowledge about stocks, investment funds or the stock market.

The lack of interest in the stock market - the most socially effective and at the same time the easiest to implement instrument for preventing or reducing poverty in old age - is often based on toxic beliefs about money, wealth creation, the stock market and the market economy at the individual level.

Opening yourself mentally and practically to stock market investments, even if it is initially just a modest stock ETF savings plan of 20 euros per month, is even more successful when people shed their toxic beliefs and assumptions.

Against this background, in this blog post we analyze eleven harmful beliefs and “poisonous stereotypes” about the market economy, about money, the stock market and becoming wealthy.

Before we begin with the first harmful belief about money, a few words about the market economy, the system that directly and indirectly forms the framework and basis for private wealth creation and wealth protection.

In its current form, the market economy - “capitalism” - emerged gradually from around 1800. At this time, religiously legitimized feudalism (absolutist monarchism), an anti-market social order in key aspects, began to gradually die out in Western countries. Although markets existed before 1800 as places for the exchange of goods and services, the essential legal and institutional basic elements of the modern market economy were only limited to a tiny part of the total population before around 1800: freedom of occupation and freedom of movement for private individuals, freedom of trade, freedom of movement of capital and freedom of establishment for companies. [4] The right to property existed for large parts of the population, e.g. B. women or serfs, also only limited before around 1800.

The gradual withering away of feudalism took place over around 120 years until the end of the First World War. Important milestones in the beginning of the end of this anti-market social order were the American and French revolutions in 1776 and 1789. A few decades earlier, in the middle of the 18th century, the industrial revolution had begun in Great Britain and later spread to continental Europe and North America.

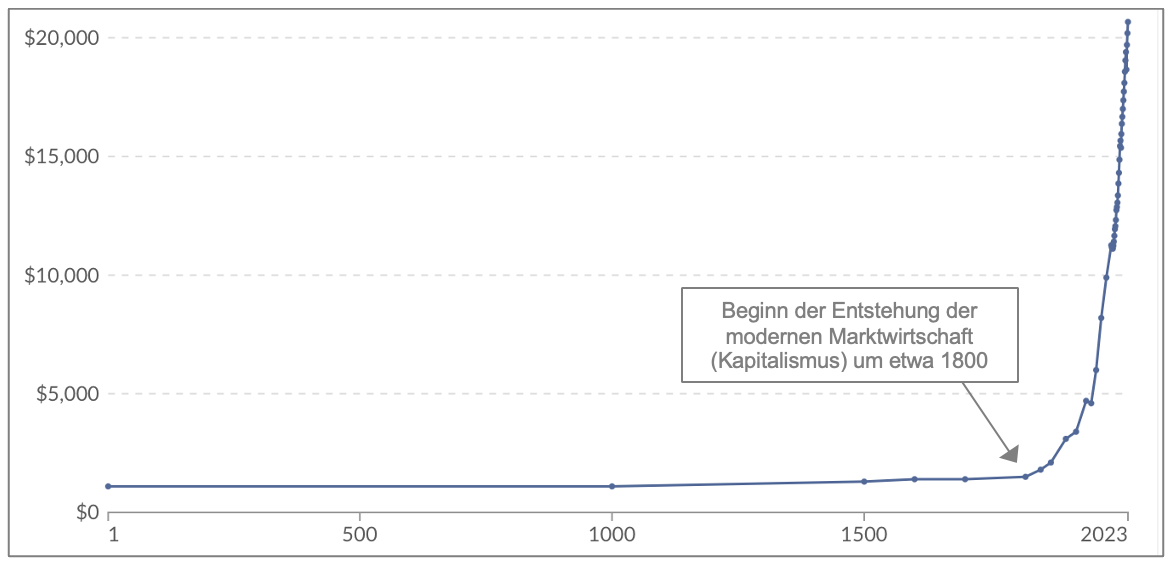

Figure 1 illustrates how enormously the lot of humanity as a whole has improved as a result of the emergence of the market economy from around 1800 onwards using the growth in global gross domestic product (GDP) per capita over the past 2000 years. [5]

Figure 1: The development of inflation-adjusted global gross domestic product (GDP) per capita over the last 2,000 years

► Source: www.ourworldindata.org, Maddison Project Database 2023. ► All figures in 2021 USD = adjusted for inflation

Figure 1 shows that global GDP per capita (approximately comparable to average private household income), adjusted for inflation, increased by about 1,300% from the emergence of capitalism to the present, a fourteen-fold increase.

In the approximately 1,800 years from the birth of Christ until 1800 before the emergence of the market economy, global economic output per capita had practically not grown at all. In view of this, it is hardly surprising that the British philosopher Thomas Hobbes (1588–1679) described existence for ordinary people in his political philosophy treatise in 1651 Leviathan described as “solitary, poor, nasty, brutal, and short”. Only with the emergence of the market economy could parents realistically hope that their children would one day be better off than themselves.

Just as important as the growth in national economic income and thus the strong, lasting improvement in the economic lot of people across all classes was the increase in the life expectancy of the average citizen. This was a paltry 29 years in 1820 compared to 73 years in 2023 - in western countries, where the market economy tends to be established earlier and more comprehensively than in the rest of the world, it is even around 79 years.

These developments illustrate how dramatically the market economy has improved the well-being of people on planet Earth over a long period of time.

Let us now come to the eleven toxic beliefs that prevent many of us on a personal level from trusting the market economy and its important subsystem of the stock exchange and stock market in order to build wealth through market economy institutions and methods.

Toxic Belief About Money #1: “Money is the root of all evil.”

The fact that people's evil actions are often motivated by greed for money as a symbol of wealth is undisputed and banal. However, the belief that money is the root of all evil is simply wrong. The very wording is a meaningless, manipulative modification of a statement from the Bible: “Greed for money is the root of all evil” (New Testament, 1 Timothy 6:10). However, greed and money are two different things.

Money emerged evolutionarily from the uncontrolled, spontaneous interaction of humans around 4,000 years ago in Mesopotamia. [6] It was one of the most important innovations for the development of humanity at the transition from the Stone Age to the Bronze Age. In terms of its cultural and historical significance, money is on a par with other key innovations of the same era (6000 BC to 500 BC): the invention of writing, the formulation of the basics of mathematics, the invention of the calendar, the compass, paper, the use of coal to generate heat, metal processing (bronze, iron), the wheel, concrete/cement and the plow.

Money was necessary in human history in order to replace the inefficient and prosperity-inhibiting barter trade of the Stone Age, which is hard to imagine today, with a more efficient, simpler mode for the exchange of goods and services and thus to dramatically improve the “economic capital allocation”, i.e. to reduce waste and facilitate creative specialization. Efficient, economical capital allocation means directing social capital resources where they provide the greatest collective benefit. Without the invention of money, humanity's civilizational exit from the Stone Age could not have taken place and without money, today's global economy would literally collapse in a short time with catastrophic consequences for humanity. Money is not an evil, but a brilliant cultural-historical innovation.

Money is also morally neutral per se. It is not to blame if individuals crave it, it triggers envy or motivates a minority to commit evil acts, just as it is not to blame for a kitchen knife if it is used to commit murder.

➔ Books/specialist articles:

- Ferguson, Niall (2008): “The Ascent of Money: A Financial History of the World” [Book]

- Rieck, Christian (2025): “Prince’s money, fiat money, Bitcoin – How money is created, gets a value and disappears again” [Book]

- von Mises, Ludwig (1922): “The Impossibility of Economic Calculation under Socialism” (1922); Internet reference here [specialist article]

Toxic Belief About Money #2: “Money corrupts character.”

There is no reliable scientific evidence to support the thesis that rich people are more often and somehow demonstrably of worse character than poor people. Although there are numerous scientific studies on this topic, their results are overall contradictory and ambiguous.

What is not unclear, however, is that violent crime statistically decreases with the level of people's income. The fact that the fiction of the last 500 years and “Hollywood” in their fictional stories very often link wealth with villainy is trivial, but it proves nothing, except that literature and the film industry - as we all know - do not represent reality and that literature and the media have a perfect nose for what sells well.

Unfortunately, similarly foolish statements about the fundamentally “evil rich” can also be found in the Bible. The most famous is: “It is easier for a camel to go through the eye of a needle than for a rich man to enter the kingdom of God.” [7]

In our opinion, behind the common belief that “money spoils character” is ultimately envy of the rich minority, especially in cultures with a high level of general envy. A survey in 13 countries showed that only in France is social envy against the rich stronger than in Germany, while Poles and Japanese, for example, are much less envious (see the following literature). Envy is an emotion that has negative connotations in all cultural value systems. In Christianity, envy is one of the “seven deadly sins”. In order to make our envy subjectively more tolerable to our own conscience, we project bad qualities onto the group of people who are the object of envy, the rich. We do this even though we have no hard evidence of the substance of this projection (“money corrupts character,” “rich people are evil”).

➔ Specialist article:

- Zitelmann, Rainer (2020): “Prejudice and stereotyping against the wealthy”; In: Economic Affairs 40 (2); June 2020; Internet reference here

- Zitelmann, Rainer (2024): “Popular perceptions of the rich in 13 countries”; In: Economic Affairs 44 (2); June 2024; Internet reference here

- Zitelmann, Rainer (2020): “How Hollywood stereotypes the rich”; Internet reference here

- Beig, Stefan (2020): “The Rich – A personally unknown and hated minority”; Internet reference here

Toxic Belief About Money #3: “Capitalism means exploitation.”

Since “exploitation” is a term whose exact definition and interpretation is difficult to reach agreement on, we replace “exploitation” here with the more easily verifiable, related terms “extreme poverty,” “slavery,” and “child labor.” If you do that, the data shows that the market economy has probably contributed more than anything else in the world to the dramatic and largely continuous decline in poverty, slavery and child labor, forms of exploitation, over the last 200 years or so.

Extreme poverty: The proportion of the world's population living in poverty according to the UN definition of poverty extreme poverty lives has declined from 91% in 1820 to 10% in 2024. This is a double victory because, despite the rapidly growing world population, not only the percentage of extremely poor people, but also their absolute number has been falling since 1970.

In 2023, the lowest-income 10% of the population in the 40 “economically freest” of 165 states (countries where market freedoms are least restricted) earned an average annual per capita income of $9,770. The poorest 10% of the population in the 40 economically unfree countries earned an average of just $1,260.

➔ The data listed comes from the websites www.ourworldindata.org and from www.fraserinstitute.org.

slavery: In 1800 there were 50 to 60 states worldwide - depending on the source and definition. At that time, slavery or arrangements similar to slavery (e.g. serfdom) were permitted in all of these states. Today there are around 200 states and slavery is prohibited by law in all of them. The non-profit Australian anti-slavery NGO Walk Free estimates that today - despite official bans - around 50 million people worldwide live in illegal, slavery-like conditions. This corresponds to around 0.6% of the world population. Over 95% of these 50 million people live in Asia and Africa, i.e. in countries where the market economy was introduced later and is now less established than in the West. (The so-called Crony capitalism In many African countries there is a perverted pseudo-capitalism hijacked by the respective corrupt political elite without the rule of law and with severely restricted freedom of trade.)

➔ The data given comes from the website www.walkfree.org.

Child labor: Although the data regarding the development of the global prevalence of child labor is patchy, [8] The available figures show clearly enough that child labor has continued to decline globally over the past 170 years and also in the recent past. In 1851, the child labor rate (KAQ) for boys in Great Britain was 28.3% (global data only exists since 2000). By 1911 it had already fallen to 14.4%. In 2000, the KAQ globally was still 23%, in 2012 it was just under 17% (more recent comparative figures are currently not available). In the “rich” “capitalist” countries of the West, the KAQ has fallen to almost zero.

The lot of children has also improved in other dimensions over the past 200 years: The proportion of children who die in the first five years of life fell globally from 42% in 1800 to 4% in 2020. The proportion of children who have a basic education (as defined by the UN) rose from 17% in 1820 to 87% in 2020. Girls have outperformed boys on this metric in recent years The gap has been caught up significantly over the past 40 years and the gap that still exists is largely due to Islamic, more anti-market countries.

➔ The data given comes from the website www.ourworldindata.org.

Toxic Money Belief #4: “The rich are rich because the poor are poor.”

Behind this socialist thesis lies the false idea that the market economy is a “zero-sum game” and that the wealth of one part of the population is based on the poverty of another. In a zero-sum game, the profit or benefit of one participant must be “financed” (compensated) by the loss or damage of other participants. [9]

In reality, the market economy is not a zero-sum game, but a positive-sum game. The almost breathtaking increase in prosperity for the average person on planet Earth since the beginning of the spread of the market economy, as shown in Figure 1, would not have been possible in a zero-sum world. The fact that this enormous global increase in prosperity from around 1820, relative to the previous millennia, also included the poorer half of the world's population becomes clear in our refutation of toxic belief 3: The global decline in extreme poverty, slavery and child labor. The sharp increase in life expectancy described above in practically all countries on earth can only be explained in a world in which one does not lose when the other wins.

Zero-sum thinking in relation to the market economy is probably the biggest conceptual error in thinking, which contributes to the rejection of the market economy and market-based solutions for wealth creation, which is particularly widespread in Germany.

➔ Books:

- Mokyr, Joel (2018): “A Culture of Growth: The Origins of the Modern Economy”

- Aghion, Philippe et al. (2023): “The Power of Creative Destruction: Economic Upheaval and the Wealth of Nations”

- Zitelmann, Rainer (2022): "The 10 errors of the anti-capitalists. On the criticism of the criticism of capitalism"

- Scruton, Roger (2015): “Fools, Frauds and Firebrands: Thinkers of the New Left”

Toxic Belief About Money #5: "Earth's resources are limited. Therefore, there must be more and more violent conflicts over scarce resources."

The claim that raw materials are inevitably becoming increasingly scarce or are fundamentally finite is an ineradicable false claim that prophets of doom have been spreading for a good 200 years - for the first time in 1798 in a famous essay by the British economist Thomas Malthus (1766–1834), the spiritual ancestor of all professional pessimists.

At the beginning of the 1970s, a group of authors who called themselves the “Club of Rome” published a then-sensational study entitled “The Limits of Growth,” [10] essentially a “Malthus Thesis 2.0”. The main message in "The Limits of Growth" was: "The world's raw materials are finite and will run out in the next 20 years due to the increasing consumption of raw materials due to the 'population explosion'. The result is probably wars over raw materials and famine." A false forecast that was “of course” based on a “new complex computer model”.

Energy raw materials are not finite because the sun radiates gigantic amounts of energy to the earth for free every day. Oil can be produced from coal, which will last at least 300 years. There are no relevant quantitative limits for electricity from nuclear energy. Agricultural raw materials are also not finite.

With regard to the vast majority of other raw materials, we have probably not yet searched for or mined the majority of the quantities available on this planet because this has not yet been necessary or technically and economically possible, e.g. B. Mining at great depths. Mining on asteroids will probably also become possible in the next few decades.

The vast majority of “finite” raw materials can and are substituted by alternatives at correspondingly high prices. This substitutability will become easier and more common to implement over time due to technical progress.

When it comes to global population growth, we now know with a high degree of certainty that the world's population will begin to decline over the next 30 to 70 years. Today no one talks about the “population explosion” as a threat, as was discussed in the 1970s and 1980s. Population growth, which has been falling worldwide for decades and the global population will soon decline overall, together with technical progress, will ensure that humanity's consumption of resources will decline sharply in the future.

In fact (in contrast to purely theoretical considerations), there is no shortage or finiteness of raw materials because the market economy sets in motion the forces and mechanisms that “eliminate” or compensate for finiteness.

Toxic belief about money #6: “Economic inequality is increasing, the rich are getting richer.”

Of the eleven beliefs discussed here, this may be the one whose rejection or relativization is the most controversial and causes some readers to gasp. Reason: Many of us see the constantly growing economic inequality allegedly caused by capitalism as a fact whose clear truth no one should doubt or relativize.

A look at the numbers shows a more differentiated picture:

If one calculates economic inequality not within individual countries such as the USA or Germany, but across more global level, then inequality has clearly fallen in recent decades. The so-called GINI coefficient of disposable income, a mathematical measure of income inequality, shows more economic equality or less inequality at a global level (i.e. including all countries) today than in 1960. Compared to 1990, inequality has fallen particularly sharply. The main reason: household incomes in developing countries have grown faster overall than in industrialized countries. (In Germany, too, the GINI coefficient of income in 2023 was at the same level as in 2009 and only slightly higher than in 1990. So one certainly cannot speak of a “permanent increase”.)

In general, inequality research is overloaded with enormous research problems, problems of data quality and methodological problems and, last but not least, ethical and ideological complexities. This makes it easy for ideologies to “prove” a supposed increase in inequality, and this is exactly what activist journalists, politicians and economists exploit. All you have to do is to selectively pick out individual countries, short periods of time or just very specific inequality indicators from among many possible ones.

Keyword: different measures of inequality or poverty: From our point of view, anyone who talks or reports about inequality without ideological propaganda intentions should make it clear that the development of “extreme poverty” on this planet is measured in absolute Sizes - i.e. how much income the poor have at their disposal in a month or a year - is at least as important and actually more important than development relative Poverty, i.e. inequality. With the more important one absolute Poverty has improved drastically worldwide in the last 100 years and also in the last 50 or 20 years - see our comments on belief 3. Main cause: The market economy reforms in many developing and industrialized countries since the 1980s.

Only in the most anti-market countries, such as North Korea, Venezuela, Cuba and some Islamic dictatorships such as Afghanistan or Iran, extreme poverty is likely to have increased in recent decades.

➔ The data quoted comes from the website www.ourworldindata.org, the website of the World Bank as well as publications by the economist Branko Milanović.

Toxic Belief About Money #7: “An economic system built on growth or compound interest cannot function in the long term.”

This idea is based on the unrealistic interpretation of simple exponential growth functions in economies, e.g. B. interest calculations or other financial mathematical growth formulas and key figures. The basic mistake that those who proclaim the supposedly destructive effect of compound interest in particular, but also the growth rates of individual companies, industries or technologies, make is to “extrapolate” such exponential growth functions/formulas into absurd, unworldly dimensions over unrealistically long periods of time. Time periods and dimensions that have never occurred in human history and the history of the market economy and will not occur either.

This can be illustrated with a simple numerical example. Let's assume that a small German Volksbank has a loan portfolio of a modest 100 million euros in its starting year 1. If the small bank were to succeed in expanding this "credit book" by just 10% annually for 100 years - by acquiring new customers and the infamous compound interest effect, the bank's loan volume after 100 years would be around 70 times as large as that of the ten largest banks in the world today. This calculation shows how absurd it is to extrapolate even seemingly moderate growth rates for more than just a few years into the future. In reality, the average life expectancy of a company, like ours, is only around 20 years here show. Our Volksbank's loan book would at some point stagnate and/or shrink again. Most banks don't exist for 100 years.

Political systems – states, empires – also have much shorter life expectancies than most people assume. States and empires grow and prosper for a limited time. Then they stagnate, shrink or “die” again. The “bankruptcy estate” is absorbed into other, new state structures. Ultimately, every book about the history of the last 3,000 years shows this. This law applies even to the most successful, temporarily rapidly growing civilizations, as the Norwegian historian Johan Norberg shows in his book “Peak Human” (see below).

In addition, the interest rate level in the world's wealthy countries has been falling for around 500 years, which is economically linked to the decreasing level of political risk and increasing levels of prosperity [11] can be explained in the states concerned (Schmelzing 2020). The compound interest effect tends to become weaker and weaker as long as it lasts at all.

Furthermore, there is little doubt that thanks to technological progress, economic growth is becoming increasingly resource-efficient and the “ecological footprint” of this growth is improving. The amount of CO2 emissions per capita has been falling in the group of economically developed countries for about ten years and will also begin to decline in the emerging countries in the next few years. In addition, many indicators show that air and water pollution are already declining on a global scale, despite the world population currently still growing. This in turn – as shown above – will also begin to shrink in the medium term.

➔ Books, specialist articles:

- Norberg, Johan (2025): “Peak Human: What We Can Learn from History’s Greatest Civilizations” [Book]

- McAfee, Andrew (2019): “More from Less: The Surprising Story of How We Learned to Prosper Using Fewer Resources and What Happens Next” [Book]

- Ritchie, Hannah (2024): “Not the End of the World: How We Can Be the First Generation to Build a Sustainable Planet” [Book]

- Pooley, Gale/Tupy, Marian (2022): “Superabundance: The Story of Population Growth, Innovation, and Human Flourishing on an Infinitely Bountiful Planet” [Book]

- Schmelzing, Paul (2020): “Eight Centuries of Global Real Interest Rates, R-G, and the ‘Suprasecular’ Decline, 1311–2018”; SSRN/Social Science Research Network [Article]

Toxic belief about money #8: “Money doesn’t make you happy.” Alternative formulations: “Money creates worries and problems” or “there are more important things than money”.

Of course money doesn't make you directly and immediately happy and of course there are more important things than money, e.g. B. Health, but money in the form of income and assets clearly helps people alleviate worries, problems and deficiencies.

There is extensive scientific research from the last 20 years that shows that poor people are statistically less satisfied with their lives than correctly comparable wealthier (richer) people or people with higher incomes. Nevertheless, journalists and intellectuals are still constantly repeating outdated theses from the 1970s and 1980s that have long been refuted by recent research, which erroneously prove that there is no positive connection between increasing income and increasing subjective feelings of happiness or - the weaker version - that increases in income above a plateau of around 75,000 dollars or euros per year practically no longer have a positive effect on people's subjective feelings of satisfaction would have. Both are wrong, as we now know from science.

➔ Specialist article:

- Stevenson, Betsey/Wolfers, Justin (2013): “Subjective Well-Being and Income: Is There Any Evidence of Satiation?”; in: American Economic Review; Volume 103; No. 3; 2013

- Killingsworth, Matthew (2024): "The Price of Happiness. What is the shape of the relationship between money and happiness, and what are its implications?"; Working Paper, 03 Oct. 2024; Internet reference here

Toxic belief about money #9: “Our times are particularly uncertain and risky.”

“We live in times of unprecedented uncertainty – economically, politically and socially.” This is a claim from a recent newsletter by well-known finfluencer Marc Friedrich. She couldn't be more wrong.

In fact, our security, measured by objective, truly important criteria, has increased globally and in Europe over the last 50 years and over the last 20 years. What are these criteria? These are statistics about the correctly measured percentage frequency of, for example, (a) violent crime, (b) serious accidents in traffic, at work and in the home, (c) most fatal diseases, (d) child mortality, (e) the number of war victims worldwide, (f) poverty measured in absolute financial terms, (g) unemployment, (h) water quality and (i) air quality.

In all of these fields, the available data shows a trend decrease in important uncertainty indicators as soon as sufficiently large regions and sufficiently long time periods are taken as a basis. This development is documented in detail and with hard data, among other things, in the three books mentioned below. The fact that we in Germany are rightly dissatisfied with the economic and political developments of the past 10+ years does not change the basic facts presented here regarding the trend decline in fact-based uncertainty.

➔ Books:

- Rosling, Hans (2018): “Factfulness: How we learn to see the world as it really is”

- Pinker, Steven (2018): “Enlightenment now: For reason, science, humanism and progress”

- Schröder, Martin (2019): “Why things have never been so good for us and we still talk about crises all the time”

Why do we have the opposite impression? Why do we intuitively want to agree so strongly with the above-mentioned quote from Marc Friedrich?

The explanations for this are simple.

— The “Negativity Bias” in the Media: The media, both traditional media and social media, practice a strong, one might say manipulative, bias in their reporting towards negative events. This creates a distorted picture of the world - not because actual reality is so negative, but because it is portrayed in a one-sided, negative and selective way.

— The “diagnostics problem caused by technical progress”: Our information about the existence and extent of many medical, environmental, economic or political problems is now becoming increasingly precise and granular - causing these problems to be perceived as larger than they once were, even though they may or probably are not larger. An example: There are more diagnosed cases of colon cancer in Western countries today than there were 20 years ago. From this fact we erroneously conclude that the frequency or risk of colon cancer has increased. In fact, the probability of dying from colon cancer at a given age, i.e. the risk of colon cancer, has decreased in Western countries over the last 20 years. Our reasoning error: From “more cases found” we incorrectly conclude “there are more cases”. [12] Due to technical progress, this “diagnostic problem” affects almost all socially important fields and leads the majority of us to incorrectly conclude that uncertainty and problems have increased.

— Pessimistic statements tend to sound more credible and “smarter” to us than optimistic statements: There is little doubt about this often confirmed psychological phenomenon. (Here the link to an English-language article on the topic.)

— Our false focus on very short term periods rather than longer term developments and on local areas rather than large areas: Of course, deteriorations in the criteria mentioned at the beginning can be proven with numbers - if you proceed selectively. This “data cherry-picking” typically consists of selecting sub-periods and/or small territories, e.g. B. only the last twelve months instead of the last 20 years or only a single large city instead of the whole of Europe.

— Our egocentric psyche: We have an innate, psychological need to view our own time and our own personal existence as particularly difficult, dangerous, and uniquely significant for the broader history of the world relative to past times and generations. Because we do this, we are “very willing” to overlook or underestimate actual improvements.

But even if the assumption about “our ever-uncertain times” were true, a broad investment in a globally diversified stock portfolio would be one of the most effective means of financially countering this uncertainty.

Toxic belief about money #10: “Money makes the world go round.”

The vast majority of historians and political scientists employed at universities would probably smile at this thesis. If there are social forces and institutions that have historically ruled and dominated the world in a mean way and today rule and control the world in a mean way, then these are primarily fundamentalist religious beliefs, radical political ideologies from the left and right and quite simply real political striving for power in all political shades without exception, but not companies or individual rich people.

Even the largest companies in the world and their boards of directors are now more than ever subject to the control of their respective governments and generally stricter laws combined with more efficient, tougher law enforcement. The last ten years have shown this and it applies to the USA, to China, to Russia, to Germany and to almost every other country. If super-rich corporate leaders in the West can be blamed in this regard, it is that they - even over the last 20 years - have rushed to the obedience of the respective left or right governments and have served them favourably, in order to protect the growth of their companies.

In dictatorships like China or Russia, there is no doubt about the ongoing influence, adaptation and subjugation of large companies and the rich, including billionaires and “tech bosses,” by an overpowering state.

➔ Books, specialist articles:

- Bagchi, Sutirtha/Fagerstrom, Matthew (2023): “Wealth inequality and democracy”: In: Public Choice; 197; 2023 [specialist article]

- McCloskey, Deirdre Nansen/Carden, Art (2022): “Leave Me Alone and I’ll Make You Rich: How the Bourgeois Deal Enriched the World” [Book]

Toxic belief about money #11: “The stock market is gambling and a casino.”

The stock market is not a casino for the rich. It is an indispensable component of the market economy - the economic system that has almost continuously improved the standard of living and life expectancy of humanity for 200 years, including the living conditions of the poorer third of humanity.

Investing in stocks provides companies with equity that they can use to produce goods and services that the eight billion people on this planet need every day for their very survival and also to improve their living conditions. In many respects, listed companies are also far more transparent to outsiders than unlisted companies.

Today's two main alternatives to a market economy - socialism and religious fundamentalism - have a far worse record than a market economy in both improving the economic lot of humanity and protecting the environment.

For people who want to build or maintain wealth, there is hardly a better, easier and more cost-effective option than investing at least a portion of their liquid assets in a broadly diversified global equity ETF.

➔ Books:

- Desai, Mihir (2017): “The Wisdom of Finance – Discovering Humanity in the World of Risk and Return”

- Niemietz, Kristian (2021): “Socialism: The failed idea that never dies”

- Kuran, Timur (2010): “The Long Divergence: How Islamic Law Held Back the Middle East”

Finally, three wise quotes about money and wealth creation:

"There is a kind of snobbery among some elites to believe that money is not necessary to be happy. That is stupid, that is wrong, that is vile." – Albert Camus, 1913–1960, French philosopher, writer and winner of the Nobel Prize in Literature.

"I have been rich and I have been poor. Believe me, rich is better." – Beatrice Kaufmann, 1895–1945, American writer.

“For a miserable life, I recommend you: Don’t waste any thoughts on money.” – Rolf Dobelli, entrepreneur, studied philosopher, best-selling author on lifestyle issues.

Conclusion

Building long-term wealth and securing your retirement provision is difficult enough. However, anyone who makes this task more difficult through negative, toxic beliefs about the market economy, money, prosperity or the stock market reduces their chances even further - and that is unnecessary.

Free yourself from harmful beliefs about money. Make money your friend. You have to treat a friend well. If you do that, the likelihood increases that over the years and decades he will give you back double or triple what you gave him before.

Endnotes

[1] In a recent blog post, we showed that renting combined with a simple ETF stock market investment on a buy-and-hold basis statistically results in higher final wealth than purchasing an owner-occupied property. See Kommer/Jerschensky: “Rent or buy – which is more financially attractive?”

[2] Net worth = assets minus liabilities. The “median” is an alternative “mean” to the arithmetic average. The median is the middle value in a sorting of all values from large to small.

[3] Rainer Zitelmann: “Attitudes towards capitalism in 34 countries on five continents”; September 6, 2023, In: Economic Affairs; 43; Issue 3; Oct. 2023.

[4] These are essentially the so-called “four basic freedoms” for employees and companies within the EU.

[5] The gross domestic product (GDP) of a country is the sum of all domestic income within a calendar year: wages, salaries, entrepreneurial income (e.g. profits) and capital income (e.g. interest, dividends). This avoids double counting. Wages and salaries make up the largest share of GDP.

[6] The area of today's Iraq as well as parts of Syria, Iran and Turkey.

[7] This sentence can be found in three of the four Gospels (Mark 10:25, Matthew 19:24, Luke 18:25), each worded slightly differently.

[8] For many countries there is either no data available or their reliability is limited due to inconsistent definitions and poor data quality.

[9] “Zero-sum game” and “positive-sum game” are terms from mathematical and economic game theory.

[10] “The Limits to Growth”.

[11] This leads to a decreasing “time preference” (also called “present preference”) in individuals – see Wikipedia entry “time preference”.

[12] For most types of cancer and many other diseases, the increase in life expectancy alone explains a large part of the increase in diagnosed cases. However, such diagnoses do not represent an increase in the real risk of cancer - despite an increase in absolute cancer cases or cancer diagnoses.