From Gerd Kommer and Jonas Schweizer

In the context of passive investing, rebalancing is the periodic restoration of the originally selected portfolio structure (asset allocation) after this has shifted due to different return developments of the individual portfolio components - a situation that inevitably occurs and is normal over time. Below we explain the most important aspects of rebalancing. We do this by answering eight questions about rebalancing.

In this blog post we present the standard rebalancing method. In addition to the standard approach, there is also a modified RB approach that is rarely discussed in the specialist literature, but which can be an attractive RB alternative for many investors. We call this modified approach “Safe Asset Floor Rebalancing” (SAF-RB). We will discuss this in a separate blog post (see here). In our opinion, anyone who is dealing with the theory and practice of rebalancing for the first time should first read this text on the standard method and only then deal with the SAF-RB variation.

(1) Why is rebalancing useful?

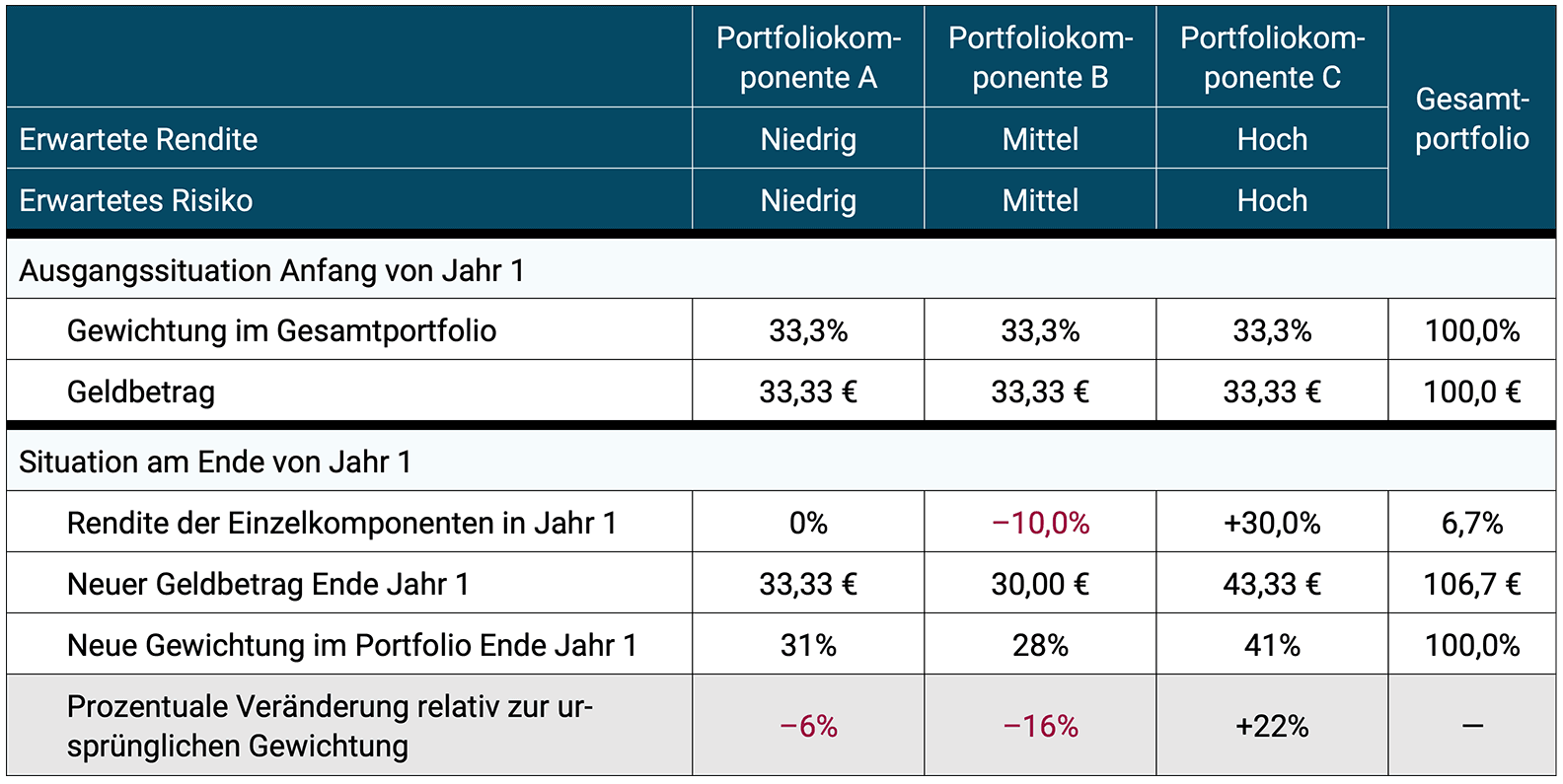

The following table shows a one-period example for a simple portfolio with three equally weighted individual components and a total investment amount of 100 euros. The different individual returns of the three portfolio components in the observation period lead to a significant shift in the asset allocation between the beginning of the period and its end.

Table 1: Illustration of the need for rebalancing

► Numbers rounded commercially.

The numerical example in Table 1 illustrates that at the end of the year all three portfolio components are underweighted or overweighted compared to the original portfolio structure. For component A, the relative change is still within relatively moderate limits. However, the significant shifts in weighting, at least for B and C, should be viewed critically as they materially change the risk profile of the overall portfolio. The riskiest portfolio component now has a weight of 41% (previously 33.3%) - an increase of more than a fifth (22%). In return, the weight of the two lower-risk components together fell by 22%.

Since high-risk asset classes have higher long-term returns than low-risk asset classes, if rebalancing (hereinafter “RB”) is avoided, the risky parts of the portfolio will assume an increasing weight in the portfolio over a longer period of time - as in the calculation example in Table 1. This will result in the portfolio without RB a la longue increasingly risky – and more profitable.

The crux of the matter in such situations is that the investor registers the “evolution” of the portfolio away from the initial structure that was once consciously chosen, but is often inclined to tolerate this because he assumes that it cannot be right “now of all times” to sell some of the investments that have done well in the immediate past and to increase the ones that have done poorly. Even harder for some to bear: now having to pay taxes on realized profits due to rebalancing.

In the short or medium term, the opposite could of course happen: the high-risk portfolio components produce losses, i.e. significantly worse returns than the low-risk components - for example in a stock market crash. (The classification “high-risk” is no coincidence.) In this case, the portfolio has become less risky/safer and has lower returns due to the negative market impact moving forward.

In this scenario - when the high-risk/high-return portfolio components had severely negative returns - many investors lack the courage to sell low-risk portfolio parts and reallocate them to the risky components that have just collapsed. This also implies that RB does not always mean making the portfolio less risky, it can also mean the opposite, more risky and more profitable.

Rebalancing generally means restoring the original third-tier target structure, because it is this original structure that correctly reflects the investor's preference in terms of the expected return-risk combination.

(2) What are the advantages and disadvantages of rebalancing?

The most important reason for and advantage of RB is what is already indicated using the numerical example in Table 1: RB ensures that the risk level of a portfolio does not stray too far from the level consciously chosen by the investor. RB is therefore primarily a risk management tool and this risk management aspect should ultimately be the sole or at least the main reason for carrying out RB.

In addition, RB also offers a return advantage - depending on how you look at it, as we will see shortly. Within asset classes with approximately the same expected return, i.e. asset classes with similar risk, RB increases the annual return at portfolio level between 0.1 and 0.4 percentage points in the long term, while the risk hardly changes or even decreases minimally. This effect is called the “rebalancing bonus” or “diversification return” in the literature. Over an “investor life” of around 35 years, 0.4 percentage points more return means an increase of around 15% in the final asset value.

How is the RB bonus explained? With regard to the possible improvement in returns, it results from the fact that it... Regression to the mean [1] exploited, and possibly also in a mild form the value and size effects. RB is an application of the buy low, sell high principle. Some also speak of “countercyclical investing” in connection with RB (Contrarian investing). However, this is somewhat ambivalent because contrarian investing (a form of active investing) not only has similarities with RB but also has many differences.

Almost every fundamentally advantageous investment decision also comes with at least one disadvantage. This also applies to RB. (The famous only exception to the “no free lunch” principle in investing is diversification.) The three main disadvantages of RB are:

(a) Between portfolio components with significantly different expected returns (e.g. stocks and short-term high-quality bonds - i.e. the high-risk and the low-risk part of the portfolio), RB reduces the portfolio return in the long term compared to pure, "radical" buy-and-hold. If you think about it for a moment you will see why. Regardless, in this case too, RB tends to increase the risk-weighted return in the form of the Sharpe ratio. [2]

If you look at two opposite “shift scenarios” in asset allocation, the following applies: In a stock crash situation, RB will significantly increase returns in the short to medium term. Over the period of a stock crash and its immediate recovery, RB is usually particularly profitable in the medium term, as it allows you to buy shares in the cheaply valued asset class before the recovery begins. [3] At the same time, RB requires a lot of discipline and nerve strength at this moment. Most private investors lack both in this situation. “Rebalancing in a crash” mentally overwhelms many investors and is therefore unfortunately not done.

In a long bull market (which is the other shift scenario), RB will lower the return versus doing nothing.

In the “total period” (25+ years), the subsidence effect probably predominates. (Nevertheless, there are numerous publications on the Internet by “practitioners” - not scientists - who claim that rebalancing generally increases returns. Unfortunately, this is incorrect. Behind such claims there is either ignorance or the desire to win customers in this way.

(b) Costs and taxes: RB, to the extent that it occurs through reallocations (more on this below), incurs transaction costs for selling and buying investments that a “radical buy-and-hold approach” without RB does not have. Fortunately, these costs are low if you do it right. RB also produces a small tax disadvantage because it is overlooked by too many private investors Tax present value effect through buy-and-hold minimally reduced.

(c) Workload: RB naturally also causes workload. Although this disadvantage is worth mentioning, it should rarely be very significant, as the effort is, all in all, manageable. Unless it's a do-it-yourself portfolio, the argument doesn't apply at all.

You can make RB work easier by using a web-based RB calculator. There are several free RB tools on the Internet with which you can easily determine what the target amounts are for a given portfolio structure in a given situation. (Of course, you can also find out with a home-made Excel spreadsheet.) Just google the words “extraETF rebalancing calculator” or “financial flow rebalancing calculator”.

(3) Which rebalancing methods exist?

Basically there are three different RB techniques or methods. A fourth consists of combining the three individual techniques.

(a) Calendar-based RB: Here, RB is carried out by reallocating (sales and purchases) at a fixed point in time, for example every twelve or every 24 months.

(b) Band-based RB: A numerical example: For a given asset allocation, in the event of shifts in the asset allocation, as shown in Table 1, one remains inactive until at least one asset class exceeds or falls below its target allocation, for example by 20% (percentage, not percentage points) (see bottom row of Table 1) - so the RB band has a width of plus/minus 20%. For example, if a portfolio component is to have an initial weight (target weight) of 40%, this would mean that this portfolio component can range between 32% and 48% (40% × 20% = 8%). Only a shift beyond the band triggers a reallocation.

Calendar-based and Band-based RB are the two variants of “Reassignment RB”. They are opposed to cash flow-based RB.

(c) Cash flow-based RB: Most households are in one of two states with regard to their portfolio: either they add new funds to the portfolio on a regular or irregular basis over time (portfolio construction phase) or they withdraw funds from the portfolio over time (portfolio use or reduction phase). The former tends to be the case with young households, the latter tends to be the case with retirees. In other words, the majority of all portfolios are “dynamic” in this sense as opposed to “static”. From a rebalancing perspective, it's encouraging because these cash flows can be used to run free, tax-neutral RB. When making portfolio additions, by always directing the new funds to the most underweighted portfolio components; When withdrawing from the portfolio, always sell components whose weight has increased first. Here, unlike the two methods mentioned above (calendar method and tape method), no Reallocations are required with the associated disadvantages (costs, taxes). The CF method, if it is possible in the specific investor case, is in principle compared to the two above-mentioned. Reallocation methods are always to be preferred because CF-based RB does not incur any transaction costs or tax payments (on sales) that would not occur anyway. In this specific sense, RB is free here and tax neutral (on sales). Fund savings plans and fixed payout/withdrawal plans (if one or the other exists for an investor) should also always be used for CF-based RB, for example by changing the plan every twelve months to achieve the RB effect.

(d) Mixed method: All three methods mentioned above can be combined with each other. In a portfolio in which funds are added or withdrawn regularly or irregularly over time, CF-based RB can be combined with either or both of the two switching methods. However, priority is always given to CF-based RB because it is de facto free and tax-neutral. However, if the portfolio is very large relative to the monthly savings or portfolio withdrawals and/or in a stock market crash situation, it may be that the foreseeable cash inflows or cash outflows are not sufficient to realistically bring the portfolio back close enough to the target allocation over a maximum period of 36 months. In this case, one of the two reallocation methods must be used, even if this has unfavorable consequences in terms of transaction costs and possibly tax liquidity. This suggests that RB via cash flows can be, and usually is, somewhat “gradual” rebalancing, not full RB “all at once.”

In a sense, there is a fifth, fundamentally different method that we call Safe Asset Floor Rebalancing (SAF-RB). We will not go into this in this blog post because SAF-RB is not “standard in the market” and is fundamentally different from the universally used standard RB approach presented here. We will deal with SAF-RB in a separate blog post here.

For all three individual methods presented above, one could still differentiate between “rebalancing exactly to the target” or “rebalancing to the nearest outer edge of the band”. (If you want to practice calendar-based RB, you also have to define a band in this case.) If you only rebalance to the nearest outer edge of the band, instead of "exactly to the target", then you can perhaps reduce the transaction costs somewhat again because smaller investment volumes are bought and sold.

Furthermore, you still have to differentiate, at least mentally, between two different important RB levels - Level 1 and Level 2. Level 1 is the highest asset allocation level between the high-risk, high-return portfolio part and the low-risk, low-return part. Level 2, below, is asset allocation within of these two parts of the portfolio. RB at level 1 is more significant and has higher priority than at level 2. At level 2, in the interest of minimizing transaction costs, you can wait longer (calendar method) or define wider bands (band method), provided you are not afraid of this additional complexity (differentiation between these two levels) in your own RB approach.

For retail investors who invest in do-it-yourself mode, calendar-based RB may be easier to implement than band-based RB.

To complete the numerical example in Table 1, below are the respective rebalancing amounts assuming one of the two reallocation methods and immediate, full RB (no cash flow RB).

Table 2: Reallocation amounts for the numerical example from Table 1

► Numbers rounded commercially. ► Without taking any tax effects into account.

(4) What does science say about the advantages and disadvantages of each rebalancing method?

One could fill a small library with the academic literature on RB. The bottom line from probably several hundred academic studies on RB: The benefits and advantages of RB are sufficiently clear and large that RB is recommended for all investors.

Where CF-based RB is possible, this method should always be used to the maximum because it does not cause any relevant transaction costs or tax disadvantages.

Which of the two reallocation methods or which combination of methods after It is not possible to clearly determine whether the CF method is the best. In each specific historical time window, a particular method or combination of methods delivers the best results. However, the differences in returns between the individual methods are usually rather moderate. In exceptional cases, large differences can occur during short periods of time, which will probably level out again later and in the long term.

In any case, the science says that the overall differences in effectiveness between the two rebalancing methods are too small and unpredictable to make a clear favorite between the two methods. This includes two key aspects of the rebalancing methods: in the calendar method, how frequently RB should occur; in the band method, how narrow the bands should be. Ultimately, you would need 500 or 1,000 years of historical capital market data to reliably determine the “one best method”. However, we only have around 100 years of data of sufficient quality. Ergo, it doesn't matter which specific method you use, as long as you choose a specific one and implement it fairly cleanly.

(5) How frequently should rebalancing take place?

In general, the following applies to the two reallocation methods: Just so often that transaction costs and work effort on the one hand are in a sensible relationship with the risk management effect of RB on the other. With the calendar method, this means probably once a year at most and perhaps even every 24 or 36 months (always in the same month if possible). With the band method, the bands are chosen so that transaction costs and risk management effects are in a healthy relationship. Pragmatically, from a private investor perspective, you could say 20%. With a 30% portfolio component, this would correspond to plus/minus six percentage points. With the CF-based method, the question of frequency does not arise because you simply use any sufficiently large cash flow for RB purposes, no matter when it occurs.

All in all, it becomes clear that one should not make a religion out of the choice of the specific RB method and its concrete implementation in the sense of a single, single, blissful approach and its highly precise implementation. It is less important that one slavishly adheres to the formulated rules than that (a) one carries out RB at all and (b) that one does not misuse RB for active speculation through the back door. RB should be a rules-based, mechanical, emotionless, forecast-free, disciplined process - not speculative market timing or active countercyclical investing.

(6) How does rebalancing fit in with the buy-and-hold principle?

Of course, RB represents a deviation from “pure, radical buy-and-hold”. Buy-and-hold represents a central core element of forecast-free passive investing, but completely passive investing in the literal sense does not exist anyway. Buy-and-hold should never be understood as a narrow-minded “I am never allowed to make adjustments in my portfolio – not even in a rule-based and intelligent manner.” (Some critics of buy-and-hold, desperate to find flaws in this smart investment philosophy, fire back at this unrealistic caricature of buy-and-hold.)

(7) Does rebalancing always mean returning to the original asset allocation?

No, that's not what it says. If the risk tolerance or, more generally, the preferred return-risk combination of a passive investor/household changes, then its Level 1 asset allocation will normally also change. The change in risk tolerance can have many causes and will probably happen several times over the course of an investor's life. Here are a few typical triggers: The investor's assets and/or his intention to continue working (i.e. his human capital) change either suddenly or very gradually due to inheritance, gifts, lottery winnings, real estate financing, company sales, marriage, divorce, unemployment, illness, accident, life crisis, ideological reorientation, emigration abroad, government measures, the very banal aging process and, and, and.

Rebalancing should of course take such changes to the current target asset allocation into account. This also implies that there is no need to necessarily rebalance to the immediately previous asset allocation.

(8) Does rebalancing also make sense for actively managed portfolios?

No, ultimately not. Although the word is often used, especially in the Anglo-Saxon world Rebalancing or to rebalance When used in the context of active investment strategies, RB, as presented in this article, has little or nothing to do with active investing. In principle, an active investor decides his asset allocation continuously and “opportunistically” or “tactically” depending on the ongoing change in circumstances and his assessment of them. In such a setting, RB would be absurd in the sense of a rule-based process.

Conclusion

Rebalancing is an integral part of the rational passive investing approach. RB can be carried out on the basis of a few simple, pragmatic rules or - if you want - according to a fairly sophisticated algorithm, as long as it covers every eventuality in advance. In both cases, however, the magic word is the same: discipline. RB should be seen primarily as risk management, not as an attempt to increase returns in the short or medium term. CF-based rebalancing is free rebalancing and is therefore particularly attractive. From an investor's perspective, rebalancing is an expression of "I'm in the driver's seat, not the market with its short and medium-term capers that swing in all conceivable directions."

We deal with a modified RB approach – Safe Asset Floor RB – in a separate blog post (here).

Endnotes

[1] Regression to the Mean: In relation to investment returns, the statistical tendency that above-average returns in a sub-period (e.g. two years) are followed by a sub-period return that is closer to the average (conversely for below-average sub-period returns). Formulated casually and somewhat vaguely: the tendency towards the mean (see article “Regression to the middle” in the German Wikipedia).

[2] Sharpe Ratio: A ratio that expresses the “risk-weighted” or “risk-adjusted” return of an investment. In its simplest form, the Sharpe ratio is calculated by dividing the average return (arithmetic average) over an entire period (e.g. ten years) by the standard deviation of the individual period returns. To put it bluntly: the return per unit of risk.

[3] When this recovery will begin sustainably after the RB is of course unclear at the moment.

Literature references

Arnott, Amy (2020): “Why Rebalancing (Almost Always) Pays Off”; June 6, 2020; Morningstar; Internet reference: https://www.morningstar.com/articles/990564/why-rebalancing-almost-always-pays-off

Chambers, Donald/John Zdanowicz (2014): “The Limitations of Diversification Return”; In: The Journal of Portfolio Management; 40; No. 4; 2014

Dichtl, Hubert/Wolfgang Drobetz/Martin Wambach (2014): “Testing Rebalancing Strategies for Stock-Bond Portfolios Across Different Asset Allocations”; In: Applied Economics; September 2015; 48; No. 9; pp. 1-17

Ilmanen, Antti/Thomas Maloney (2015): “Portfolio Rebalancing, Part 1 of 2: Strategic Asset Allocation”; Dec. 2015; AQR; Internet reference: https://www.aqr.com/Insights/Research/White-Papers/Portfolio-Rebalancing-Part-1-Strategic-Asset-Allocation

Kiskiras, John/Andrea Nardon (2013): “Portfolio Rebalancing: A stable source of alpha?”; January 23, 2013; Internet reference: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2202736

McNamee, Jenna/Thomas Paradise/Maria Bruno (2019): “Getting back on track: A guide to smart rebalancing”; April 10, 2019; Vanguard; Internet reference: https://advisors.vanguard.com/insights/article/IWE_InvResBkOnTrkGdeSmrtRblncng