From Gerd Kommer and Jonas Schweizer

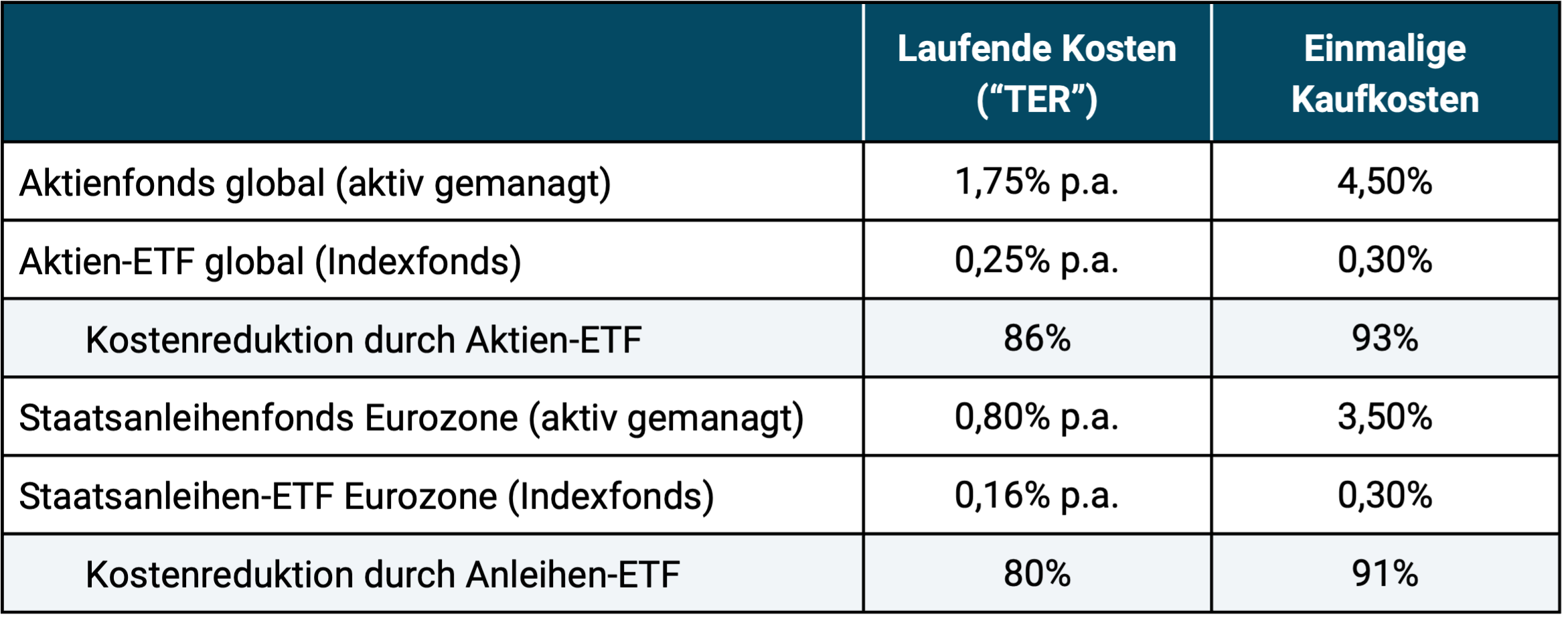

With the onset of the Great Financial Crisis of 2008/2009, low-cost index funds including ETFs experienced a surge in popularity worldwide. The market share of index funds in the investment fund segment for private investors has grown significantly in recent years. Overall, however, the correctly calculated global market share of “passive investing” is still likely to be less than 2% (see here, especially calculation on slide 10). This market share growth is putting pressure on margins in the financial sector - something that investors can also be happy about. Table 1 illustrates how high the product costs of traditional, actively managed fund products still are compared to those of index funds.

Table 1: Comparison of typical costs between actively managed investment funds and index funds (ETFs) in Germany and Austria

► All information in the table should be understood as average values of a range that is considerable in practice. ► For proof of information on actively managed funds, see e.g. B. “FMA market study on fund fees for Austrian mutual funds – deadline December 31, 2018”. The purchase costs of actively managed funds are the issue premium (this can be partially reduced by purchasing through a direct bank). ETFs are concerned with the bid-ask spread and other transaction costs. ► “TER” = Total Expense Ratio (“Ongoing Costs”).

The differences in running costs that may appear small visually between e.g. B. 1.75% and 0.25% for equity funds (see Table 1) produce enormous differences in final wealth in the long term due to the negative compound interest effect in this case, has now become accepted by large parts of the private investor community. Nevertheless, it doesn't hurt to keep reminding yourself of this fact with concrete figures: Assuming a nominal gross return of 8% p.a. for stocks. a., costs of the same amount as those in Table 1, a tax rate of 27% on the annual gross return and an investment horizon of 30 years, then the passive ETF investment in stocks leads to a final value that is 43% higher than an investment in the active fund; For bonds, the cheaper ETF alternative leads to a final value that is approximately 19% higher, assuming a nominal gross return of 3% p.a. a. accepts. (It would be wrong to assume a higher gross return for active funds because the pre-cost return of the average active fund is known to be very close to that of index funds, as proven by an innumerable number of scientific studies over the last few decades.)

Given the fact that more and more private investors are discovering the advantages of cost-effective passive products and investment strategies, it should come as no surprise that the established financial industry - banks, asset managers and fund companies - is taking “creative” countermeasures here. One of the many measures that marketing experts have come up with in recent years is to reduce the ongoing management fee of asset management portfolios and/or actively managed funds and, in return, to introduce a new additional fee with a hip name: so-called “performance fees”.

From the perspective of their creators, performance fees (hereinafter abbreviated to “P-fees”) have three advantages: (a) They allow the provider to reduce the normal management fee without actually having to become cheaper. (b) Probably 99% of all private investors cannot quantify the real costs of P-Fees. This means they are left out of total fee estimates and comparisons for potential new customers - exactly what the provider wants. (c) P-fees even sound kind of good at first, because they make it seem as if the financial company is only paid “if the performance is right”. And who wouldn't want to pay for good performance?

With regard to issue (b), we have quantified some actually existing P-fee clauses from banks and asset managers in Table 2. (The calculation methodology is explained in the following text.) Fact (c) - the P-fee only applies if the performance is correct - turns out to be wishful thinking on closer inspection. A P-fee is de facto payable even if the bank, the asset manager or the fund underperforms its benchmark in the medium and long term, i.e. it does not generate any additional performance at all, but the investment only returns poorly or even poorly.

Table 2: Quantification of performance fees from various providers in the form of a long-term average cost ratio

► See current text for calculation methodology. ► All four cases are based on the original formulas of the banks and the asset manager, including a “high watermark regulation” in three of the four cases. ► Performance fees apply almost without exception additionally at normal administration fees.

In Table 2, we have transformed four standard P-fee clauses from real asset management contracts from three anonymized banks and a bank-independent asset manager into a long-term annual average fee. To do this, we have taken an example of the annual returns of the FONDAK A fund (ISIN DE0008471012) since the earliest possible point in time, i.e. h. from 1962 to 2018 (57 years) and then calculated what the annualized P-fees would have been based on these returns. FONDAK A is the oldest surviving German equity fund. It belongs to the Allianz insurance group. The fund invests in German standard stocks. FONDAK A has outperformed the DAX index by 1.3 percentage points p.a. over these 57 years. a. under-performed (6.4% p.a. for the DAX and 5.1% p.a. for the FONDAK A - without taking into account the FONDAK issue premium of (regular) 5%. Despite this poor performance, the FONDAK A was actually an above-average actively managed fund in its segment during the period under review - otherwise it would not have survived so long. The FONDAK A charges its investors with ongoing costs of 1.7% (“TER”). However, for the purposes of the simulation in Table 2, we have mathematically reduced this fee to 1.3% because we estimate that it would have been 0.4 percentage points lower if there had been a P-fee.

The bottom line of this evaluation: Even with a long-term return that is below the benchmark (reference size), P-fees fall between approximately 0.50% and 0.80% p.a., depending on the specific P-fee formula. a. to. There can therefore be no question of any reward or remuneration for the particular performance or outperformance of the asset manager or fund manager. In fact, the investor pays even if there is underperformance and mediocrity. This absurd result comes about because P-fees are constructed the way they are constructed: due to their design, their level is in reality determined more by high volatility (fluctuation in annual returns) than by attractive long-term returns.

P-Fees originally come from the “posh world” of hedge funds and private equity funds. The “2/20 cost model” (2% management fee + 20% P-fee) that is common on the market there [1] combined with a so-called High Watermark) would result in an average P-fee burden of 1.28% p.a. based on the raw return figures in Table 2. a. - excluding the normal administration fee of 2% p.a. a. Ouch!

However, actual hedge fund P-fees in recent years may have been lower because the 10,000 or so hedge funds worldwide as a group delivered catastrophic returns well below the broader stock market over the past 15 years. The results for typical private equity investments were somewhat better, but were also well below an adequate equity benchmark (see, for example, Kommer, Invest confidently with index funds and ETFs, 2018, Section 2.18).

In addition to their unpleasant cost and return impact, P-fees smuggle another foul player onto the field: unnecessary conflicts of interest. The reason lies in the special construction of P-fees, which are almost always calculated on the basis of calendar year or half-yearly returns. If a fund manager is significantly “behind” in terms of returns – let’s say at the beginning of October – he only has a chance of earning a P fee if there is a strong “turnaround” in the last three months, which will incentivize him to take particularly high risks for these three months. This is the only way he will – with a bit of luck – get his “bonus” in the relevant calendar year. However, this irrelevant behavior has nothing to do with the actual fund strategy and is ongoing ex ante against the interests of investors. The fund manager is therefore paid additionally for taking on a higher, unrelated risk.

In the end, the question arises as to whether P-fees, which arise in the medium and long term even in the event of mediocre or poor performance and which promote disastrous conflicts of interest, should always be rejected. The answer is Yes. The only conceivable exception to this conclusion would be “symmetrical” P-Fees, i.e. P-Fees that can fundamentally benefit both sides in the same way, not just the asset manager or the fund company, as is the case with normal “asymmetrical” P-Fees. With a symmetrical P-fee, fund companies or asset managers pay money from their own pockets to the investor in the corresponding amount in every calendar year in which the return is below the reference figure (benchmark), since the fund manager or administrator is responsible for the poor performance. That would be a fair arrangement for a change.

In the USA - a country in which investor protection is much more developed than in German-speaking countries - only symmetrical P-fees are legally permitted for investment funds for private investors. But because no US fund company wants to commit to so much fairness, there are no P-fees in the US mutual fund market. In Germany, however, they are becoming more and more numerous. This shouldn't be surprising, as the legislature in this country has been in a vegetative state for decades when it comes to real, effective private investor protection.

Conclusion

Performance fees are a double deception because they actually apply even if the bank, fund or asset manager only delivers an average return or even a return that is below the reference value (benchmark). Additionally, they create ugly conflicts of interest. Anyone who agrees to anything other than symmetrical performance fees is making a serious mistake that will probably pay dearly in the long run.

Endnotes

[1] The 20% number refers to the calendar year return. If the value of the portfolio including current income (interest, dividends) at the end of the calendar year is higher than in all previous years since the investor's investment began, the following applies: P-Fee in the relevant year = 20% × annual return.

literature

Andrew Clare / Nick Motson / Richard Payne / Steve Thomas (Oct. 2014): "Heads we win, tails you lose; Why don't more fund managers offer symmetric performance fees? Internet reference: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2525545

Henri Servaes / Kari Sigurdsson (Dec. 2018): “The Costs and Benefits of Performance Fees in Mutual Funds”; AQR Capital Management); Internet reference: https://ecgi.global/sites/default/files/working_papers/documents/finalservaessigurdsson.pdf