From Gerd Kommer and Jonas Schweizer

This post was updated in August 2025.

In our consulting practice, we often encounter a financially questionable constellation with private households: “negative interest differential transactions”. Behind this terminology, which sounds like a dubious financial construction, there is something that is simple in theory, whose harmfulness is usually not recognized and, fortunately, has nothing to do with illegality.

A household has a negative interest differential transaction (hereinafter abbreviated as “NZDG” for the sake of simplicity) if it holds a significant amount of low-yielding “cash assets” while at the same time having liabilities, i.e. debts. The cash investment - interest-bearing and non-interest-bearing bank deposits - will produce lower returns than the loan interest rate will be, not only in the short term, but also in the long-term average, almost without exception, after inflation, taxes and costs.

It is obvious that it is economically a gamble if, on the one hand, you invest your own money with a very low or zero return and, on the other hand, you take out a loan that costs more than the cash investment earns. In most cases, this “money-bleeding constellation” – the NZDG – should be ended as quickly as possible. Of course, a small personal liquidity reserve for the uncertainties of life is excluded from the NZDG logic [1]. Every household should have this, even a household with debt.

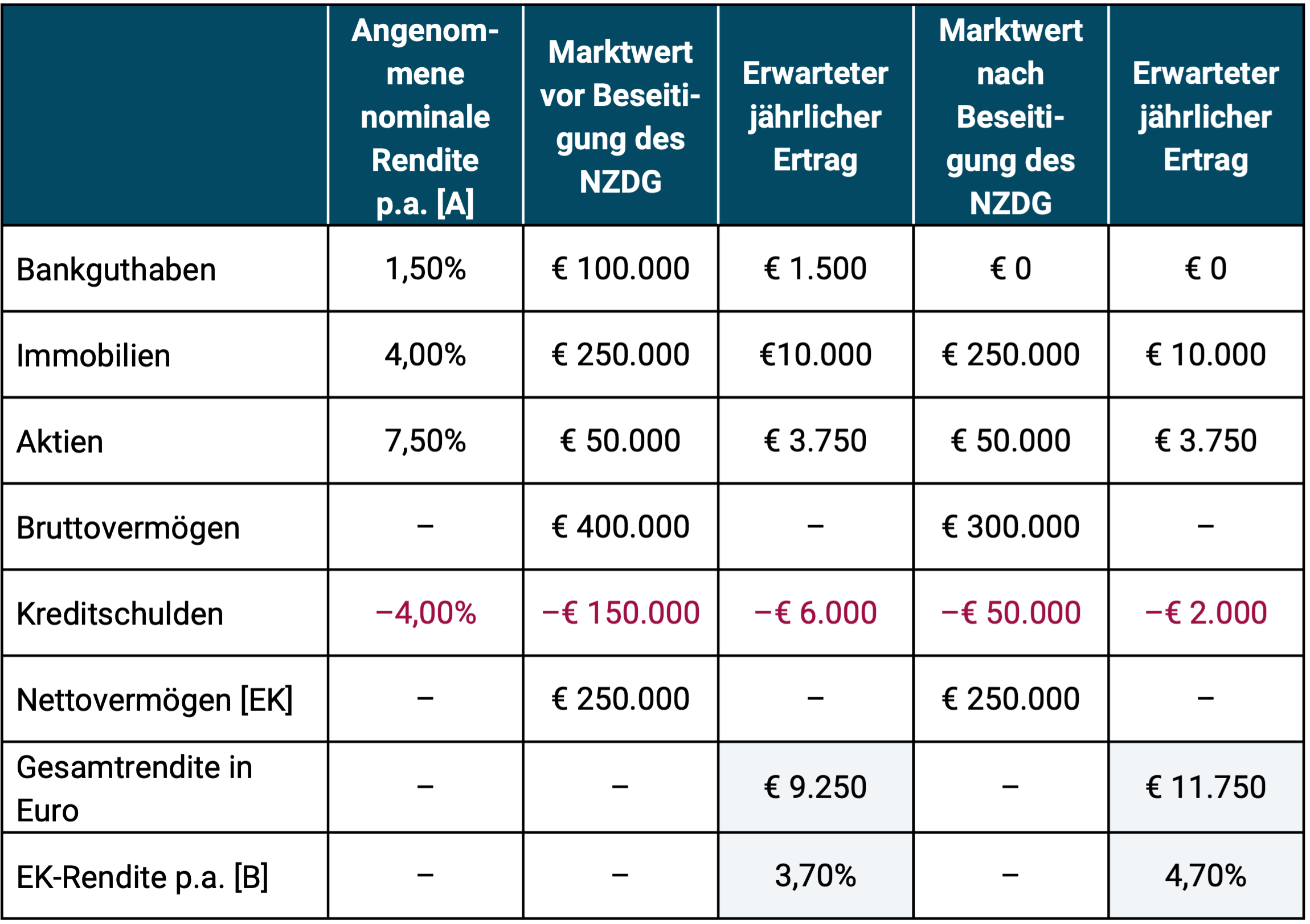

In a nutshell, ending a typically adverse NZDG involves using free cash to pay down debt as much and as soon as possible or investing cash in assets that have a higher “expected net return” than the loan interest rate. The following table illustrates the NZDG situation numerically using the Schneider couple's household balance sheet as an example. The free cash resources are invested in loan repayment.

Table: Illustration of the effect of eliminating a negative interest differential transaction (NZDG) using the example of the Schneider couple household

► [A] This refers to the total return: current income and price or value increases after deducting costs and taxes. ► [B] Return on equity (equity return) = total return in euros ÷ net assets. ► The personal liquidity reserve is not taken into account here (see ongoing text for PLR).

The table shows that in this sample calculation, the Schneiders reduce their costs by 2,500 euros annually by ending the NZDG or increase their total income in euros by 2,500 euros (11,750 euros minus 9,250 euros). This improved profitability is also reflected in the increased return on equity.

Terminating the NZDG as a measure to improve economic efficiency in absolute and relative terms is usually easy to implement and its positive effect is ultimately guaranteed. In the field of investment, there are not many measures that have a return-increasing effect without also having obvious or hidden disadvantages such as: B. involve more risk or more complexity. Eliminating an NZDG by repaying the loan is one of the rare options for improving returns that does not come with any disadvantages and is very simple - a Free Lunch, if you want. What else is there to say about this?

- The benefit from eliminating NZDG has nothing to do with low or zero interest rates. The logic and benefits of eliminating NZDG would apply even if (nominal) interest rates were significantly higher than today; The loan interest rates would then also be higher.

- As mentioned above, every household should have a sufficiently generous personal liquidity reserve (PLR), the famous nest egg for emergencies. In terms of amount, this should be around six times the long-term average monthly expenses. If you want to be particularly careful and conservative, you can set twelve times that amount. The PLR is always left out of the considerations for eliminating NZDG, even if this slightly reduces the benefit from this elimination.

- If the loan in question cannot be repaid early or can only be repaid to a limited extent due to repayment restrictions, then it is obvious that the advantages from the elimination of the NZDG cannot be used to this extent. Such a household should then make up for this at the earliest possible opportunity (keyword: special repayments).

- The repayment of a loan is economically equivalent to a completely risk-free investment in the amount of the repayment, the return of which is the interest expense saved. Otherwise, risk-free investments that provide such returns don't actually exist on this planet. This economic intuition should convince them of the attractiveness of ending NZDG if the other arguments have not already done so.

- The normal, most obvious elimination of an NZDG by paying off the loan increases the (expected) profitability of a household portfolio, but does not influence its risk (or only minimally in a positive sense) and thus represents a “free lunch” that is very rare in economics.

- Maintaining low-yield liquidity, even though there are liabilities that cost more than the liquidity brings in, can make economic sense if you believe that an “investment opportunity” will arise in the short or medium term, an opportunity into which the low-yield liquidity will then flow - instead of into loan repayment. The investment opportunity must then have a higher expected return after costs and taxes than the loan costs after taxes.

- The logic described in the previous point can also be applied analogously to an immediate (already known) investment, i.e. without “waiting for the opportunity”. In this case, the low-yielding liquidity is invested in an existing or known investment, e.g. B. invested in broadly diversified stock ETFs. If the termination of an NZDG does not occur by way of loan repayment, but rather through an investment with an expected return above the loan interest rate, then in principle this also leads to the aforementioned cost advantage, but at the same time the household in this constellation increases its overall risk (and its overall return opportunity) because - compared to the original starting point - the proportion of the risky part of the portfolio in the entire portfolio has now increased. However, if an investor believes that he has identified an investment that has a higher expected net return than the loan interest rate in question and that is at the same time risk-free or almost risk-free, then of course our argument does not apply. However, we view such considerations as naive Alice in Wonderland fantasies.

If you haven't heard from your bank, financial advisor or asset manager about eliminating NZDG, it may not be because that institution - unlike you - makes money directly or indirectly from the continued existence of NZDG.

One could therefore summarize that the pivotal point in dissolving an NZDG is the decision as to how the low-yielding cash resources should be used: in debt repayment or in an investment with an expected return above the cost of the loan. In any case, the following statement applies: Holding cash-like, low-yielding assets while simultaneously having credit debts is - subject to the exceptions mentioned above - economically irrational. The rational path is either to repay the loan or to expand risky investments. The loan repayment route definitely improves profitability while maintaining the same risk (there is no uncertainty about the effects). The expansion of risky investments increased the expected return and the expected risk (there is uncertainty about the effects).

Conclusion

What needs to be done in practice for private households? You should check your investments for the presence of negative interest rate differential transactions. This also includes small loans such as overdrafts and consumer loans. If an NZDG exists, then in most cases it will be financially worthwhile to put an end to this return killer as soon as possible, by repaying debts (provided the corresponding loans can be partially or completely repaid early) or by expanding risky investments with an expected return above the loan interest rate.

Endnotes

[1] The purpose and recommended level of personal liquidity reserves are explained below.