From Gerd Kommer and Luca Stagnitti

Just over a year ago, the consumer goods inflation rate began to rise in Germany and most countries around the world. In the five months since March of this year, the annualized figure was even over seven percent. For those of us under 60, this is an unusual experience. The inflation rate in the 35 years up to mid-2021 averaged a moderate 1.7% per annum.

The main causes of the strong increase from March 2021 are the expansionary monetary policy of the central banks from 2009, pandemic-related global supply chain problems, government Corona economic support programs in a full employment situation and raw material shortages due to the Russia-Ukraine war.

In this context, the question naturally comes to the fore for investors as to how they can compensate for the devaluation of money with their investments, all the more so as the usual investment recommendations for “how to beat inflation” currently seem unattractive:

- Residential properties in attractive locations in German-speaking countries are now highly valued and real estate financing interest rates have risen significantly since the beginning of 2022. After a thirteen-year real estate boom, there is now widespread talk of the first price declines.

- Since the beginning of the year, gold has hardly confirmed the widespread “theory” according to which the gold price rises noticeably when inflation accelerates and/or a global political crisis sets in. In the longer term, for example over the last ten years, gold returns have been rather poor anyway.

- Cryptocurrencies, often promoted by crypto fans in the past as a “store of value” and “inflation hedge”, have lost some of their previous reputation due to drastic price declines since November 2021, further fraud and hacking scandals and increasing rather than decreasing regulatory risks.

- Stocks have also taken a hit since the start of 2022. From its peak on January 4th to mid-June, the MSCI World in euros fell by around 16%. Although it has caught up a lot since then and was at minus 7% on July 1, 2022, the stock market is currently still portrayed as “particularly uncertain” or “dangerous” in the media. [1]

In such a situation, it does not seem surprising that inflation-indexed bonds (often called inflation-protected bonds) - an asset class that has previously received little attention from private investors - are now coming into focus.

In this blog post we want to explain what inflation-indexed bonds are and whether they actually offer the attractive protection against inflation that their name suggests.

What are inflation-linked bonds and how do they work?

Inflation-indexed bonds (hereinafter “IIAs” for the sake of brevity) are almost exclusively issued by governments and not by companies. Great Britain issued the first IIAs in 1981. [2] Since then, a manageable number of countries including the USA and Germany have been added as issuers. To date, there are no IIAs from Austria or Switzerland. The IIA market share of less than two percent of the global bond volume and the small absolute number of different issuer countries and bonds make it clear that IIAs are still a niche phenomenon.

A few IIA ETFs have also existed for a few years now, making investing in IIAs easier for normal private investors - more on that below.

How does an IIA differ from a corresponding conventional government bond (hereinafter “KA”)?

The key difference between an IIA and a KA is that the risk of unexpected inflation is distributed differently between the issuer and the investor. With an IIA, the issuer, i.e. the government, bears the risk of unexpected inflation; with a KA, the investor bears it.

What is Unexpected Inflation Risk? At any given point in time, there is a collective inflation expectation in the investment community for a given country or currency - the so-called expected inflation. It is already priced into the nominal current yield of a KA at all times. The current yield is the return on a bond from the time of purchase until maturity - assuming that there is no default beforehand. The current yield is known exactly at the time of purchase. For KAs, it contains the market's collective inflation estimate at the time of purchase until the bond matures, be it three years or 30 years later.

Many private investors find it difficult to believe that expected inflation is always already priced into conventional bonds, even though this fact is undisputed in academic financial economics. Some private investors find this concept particularly difficult when the inflation rate has recently been higher than the nominal current yield on government bonds (i.e. the market does not expect full compensation for inflation), as has been the case in Germany and other countries for several years.

Unexpected inflation, like actual inflation, can only be observed in retrospect. Unexpected inflation is defined like this:

Unexpected Inflation = Actual Inflation – Expected Inflation

Unexpected inflation can be negative or positive, i.e. h. the market may overestimate or underestimate inflation for a specific future period. In the case of an overestimation, the unexpected inflation is negative; in the case of an underestimation, it is positive. For a given period, expected inflation and actual inflation are naturally only known looking back (ex post), while expected inflation is known looking forward (ex ante).

IIAs protect the investor from unexpected inflation. They therefore offer protection in the event that the market significantly underestimates inflation over a given period of time - as a shield against so-called inflation shocks (inflation that has not already been priced in).

The inflation priced into the current yields of conventional government bonds for certain remaining terms at any given time - the expected inflation - can be measured by comparing them with the current yields of corresponding IIAs. We return to this fascinating point below. First, however, we have to explain the mechanics of an IIA.

Unlike a KA, an IIA does not have one inherently nominal Coupon (the coupon is the periodic interest payment) and therefore no nominal current yield, just a lower one real Coupon, i.e. a coupon that does not include consumer goods inflation and therefore a real current yield. However, in addition to the lower real coupon, the issuer (the government) adds actual inflation to the investor with each coupon payment. The inflation indexation of the IIA consists in this surcharge. [3] The total interest payment on an IIA therefore corresponds to the real coupon yield, plus an add-on for realized inflation.

For reasons of space, we will ignore how the mechanics of this additional payment work in detail, especially since the IIAs of different countries sometimes differ. However, the economic result is the same for all IIAs, regardless of any small design differences.

If one now subtracts the real current yield of the IIA with the same remaining term from the nominal current yield of a KA at a given point in time, this results in the expected inflation priced in by the market for the remaining term of these bonds.

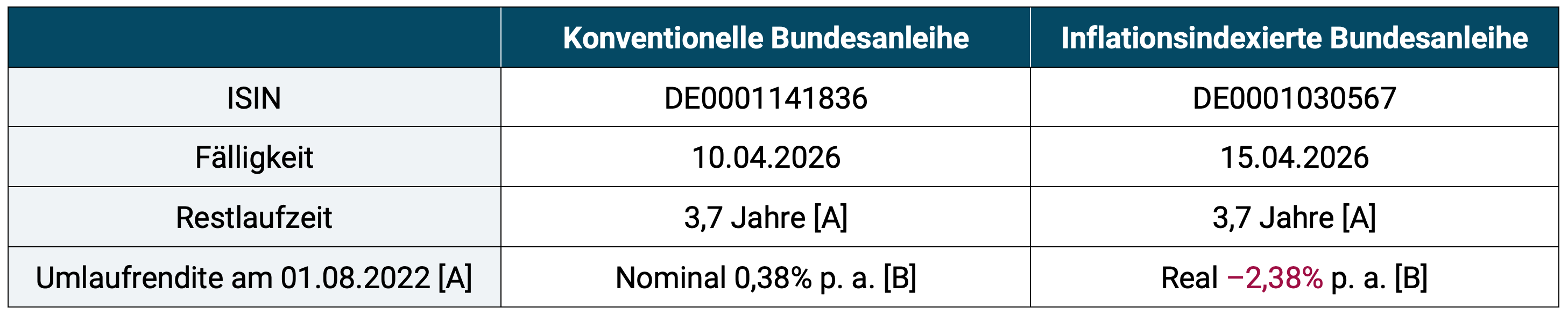

Here is a current numerical example for the next three and a half years - we compare a KA and an IIA that were issued by Germany.

Table 1: Comparison of current yields for a medium-term conventional bond (KA) and an inflation-indexed bond (IIA)

► [A] There are currently only five inflation-indexed federal bonds and none with a maturity date that exactly coincides with the maturity date of a conventional bond. The difference of five days in this case is likely to be the case determined here Breakeven inflation (see ongoing text) but be negligible. ► [B] Current yields via the German Finance Agency website.

We now subtract the real current yield from the nominal current yield, i.e.:

0.38% p.a. a. – –2.38% p.a. a. = 2.76% p. a.

The difference of 2.76% p.a. a. was the consumer goods inflation expected by the market on August 1st, 2022 for Germany on average for the three and a half years from August 1st, 2022. The expected inflation determined in this way is called in financial jargon Breakeven inflation called. It is the inflation priced into KAs for that specific period (the remaining maturity of the two bonds being compared).

For Germany, the breakeven inflation over certain remaining terms is shown on the website of the Federal Finance Agency here displayed for the USA on a website of the Fed (US central bank) here.

If an investor has a reasonable belief that actual inflation will be higher than breakeven inflation (priced-in inflation) for a given future period, then he or she should purchase an IIA. If he doesn't think so, he would be better served with a KA. (In our view, however, there is no convincing evidence that anyone can systematically estimate the level of future inflation better than the bond market.)

Do inflation-indexed bonds have more attractive long-term returns than conventional bonds?

Now that we know how IIAs basically work, the key difference from KAs, and the economic logic behind any preference over KAS, the question is which type of bond is more attractive. To answer this, a rational person would first want to see a long-term historical return comparison. However, this is difficult for IIAs to carry out. This is because there are hardly any data series on IIAs that go back more than 20 years in the past and because with the existing data material it is almost impossible with reasonable effort to keep the (remaining) term (or, more precisely, the duration) of the IIAs and KAs to be compared sufficiently identical - at least for the available data series beyond 20 years. However, if the durations are not close enough to each other, then you are comparing apples with oranges and it may be that the measured differences in return and risk are due to the different durations rather than to inflation indexing. [4]

With this caveat in mind, conventional long-term government bonds in the UK probably produced very similar returns to IIAs for the 37.5 years from January 1985 to June 2022 (longest data series available) - just under 4% p.a. in real terms. a. (although the duration of the two bond types in this data series is not completely identical). If one only looked at the period from January 1985 to March 2021 before inflation rose sharply, KAs would have been clearly ahead in terms of returns. In the short year and a quarter since March 2021, IIAs have outperformed noticeably (see the figure below for US government bonds).

According to economic logic, KAs should have at least a small return advantage over IIAs in the long run, because the return on KAS includes compensation for the risk of unexpected inflation. As mentioned above, this risk component is eliminated for investors in an IIA and is therefore also a source of return.

The small difference between the long-term returns of KAs and IIAs for the UK case from 1985 to June 2022 indirectly confirms that in the long run the ex-ante market estimate (in advance) of expected inflation (priced-in inflation) is close to actual inflation.

The volatility of both asset classes over the entire 37.5-year period was of the same order of magnitude, but the real maximum drawdown, a different measure of risk, was far lower for IIAs at 17% (June 2022) compared to 31% (also June 2022) for KAs. IIAs are therefore empirically lower risk. This also corresponds to the economic logic (keyword: lack of inflation risk – see above).

The correlation of monthly returns with inflation was close to zero for both types of bonds. This is surprising because many investors believe that IIAs have a high short-term correlation with inflation - after all, that's what they are called inflation-indexed Bonds. We explain the reason for the low correlation below. In any case, there can be no question of a return trend for IIAs that is in line with monthly or quarterly inflation. In this sense, they are only a slightly better inflation hedge than KAS in the short and medium term.

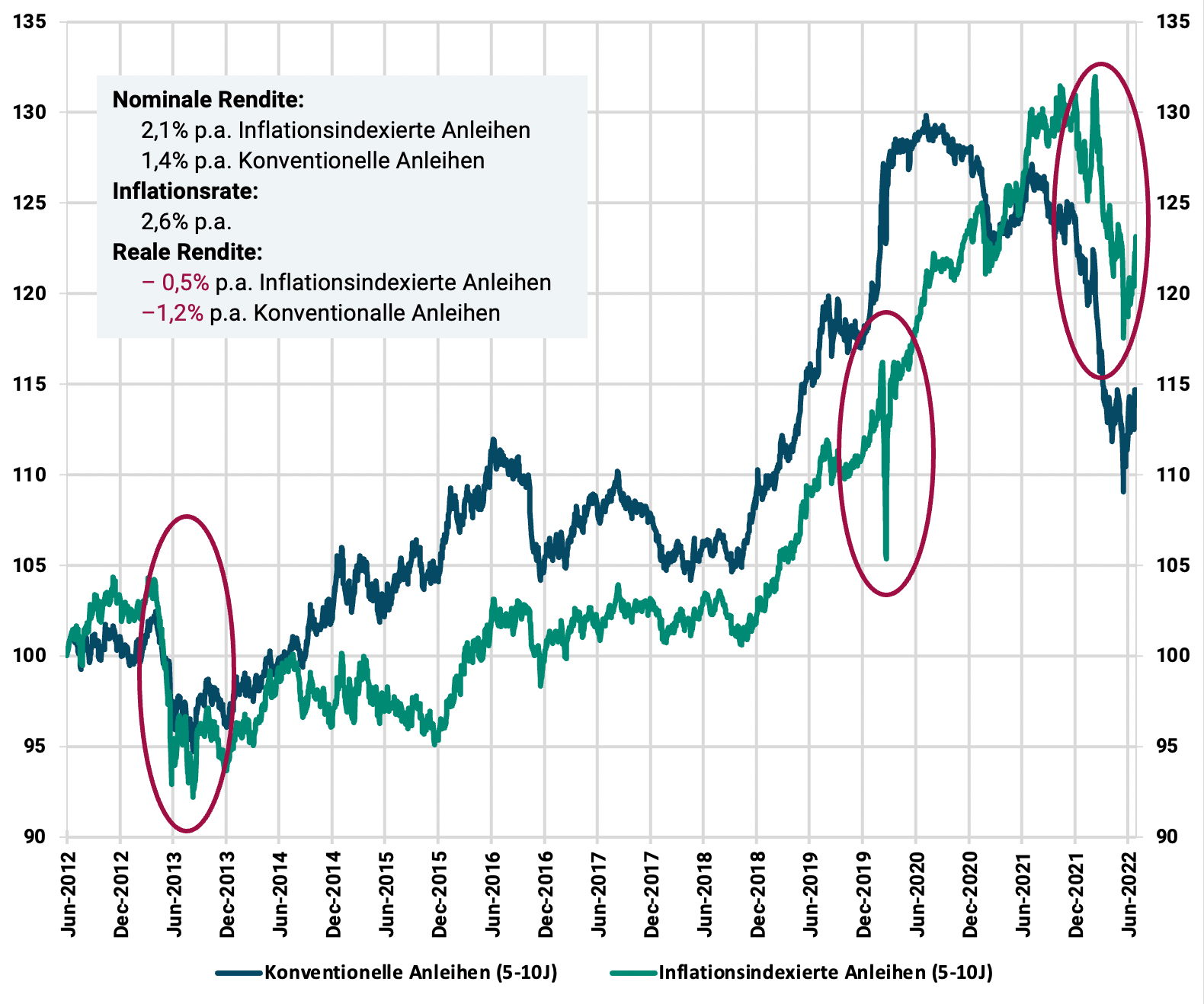

First, the following figure compares the performance of conventional and inflation-indexed US government bonds over the past decade. (This relatively short data series ensures that the duration of the two bond baskets is almost identical at around seven years.)

Figure: Comparison of the development of two bond indices: S&P US Treasury Bonds 5-10 Year Index (conventional US government bonds) and S&P US TIPS 5-10 Year Index (inflation-indexed government bonds)

► Excluding costs and taxes, in USD, nominal. ► Total returns (interest + price changes) ► Effective duration for the two indices as of July 28, 2022 6.4 years and 7.0 years, i.e. sufficiently identical for comparison purposes ► Data: Dimensional Fund Advisors

The graphic reveals some interesting insights:

- Over the past ten years, both the nominal yield on conventional intermediate-term U.S. Treasury bonds and that of IIAs have been below inflation. Real returns were negative in both cases. This makes it clear that with IIAs you do not always “earn at least the inflation” even over periods of several years. Presumably the IIA return over this period is slightly better than that of KAs because at its end there was a strong inflation shock, against which IIAs protect better than KAS (this shock period therefore has a high temporal weight in the relatively short overall period).

- Medium and long-term IIAs are also exposed to interest rate risk. US intermediate-term IIAs lost almost 12% from early December 2012 to early September 2013 during a brief period of rising interest rates in the US (the leftmost oval). From early August 2020 to mid-June 2022 (the rightmost oval), medium-term US Treasury bonds fell 16% due to rising nominal interest rates during this time.

- During the Corona stock crash in March 2020 (middle oval), IIAs briefly fell by almost 10%, while the corresponding KAs remained largely stable. Main reason: In February and March, inflation expectations, which had previously been greatly expanded, narrowed significantly again. Another reason could have been that IIAs are significantly more illiquid than the corresponding KAs because there are so few IIAs and they are traded less frequently. In severe market crises, illiquid securities are sometimes penalized more severely than their more liquid conventional siblings, all other things being equal.

Our main findings

Inflation-indexed bonds do not always offset inflation in the short term or necessarily in the medium to long term.

Even during periods of elevated inflation, such as from mid-2021, inflation-indexed bonds can have negative returns, as has been the case over the past seven months. This will tend to be the more the case the longer the remaining term of the bonds in question is. For long-dated IIAs, the interest rate risk is slightly lower compared to KAs, but it is also significant for IIAs, as the figure shows. In KAs, interest rate risk materializes through inflation shocks and/or increases in real interest rates (increase in risk aversion), in IIAs only through an increase in real interest rates.

Nominal interest rates change primarily for two reasons: when inflation changes, and when general risk aversion and thus the risk premium in the market changes. [5] These two factors influencing nominal interest rates are independent of each other. However, they can and often do coincide in time. The relative contribution of the two factors to a given change in nominal interest rates cannot be distinguished in real time - only retrospectively. Nominal interest rate increases due to increased risk aversion in the market also lead to price declines for inflation-indexed bonds, which increase the longer their remaining term (duration).

If you are an active investor who wants to achieve excess returns with IIAs, you must buy them before an inflation shock occurs (the occurrence of high unexpected inflation). If inflation is already high (as it is now), it is too late. We do not believe that anyone can predict with sufficient confidence the timing and magnitude of inflation shocks.

We have now seen that unfortunately, based on conceptual and empirical arguments, IIAs do not represent the silver bullet against inflation risk in investor portfolios that one might expect based on their name. In practice, they have further disadvantages, especially for investors who prefer to work with ETFs instead of individual bonds for reasons of simplicity.

The problems with ETFs on inflation-linked bonds

First, we would like to briefly discuss the most important and often overlooked difference between investing in an individual bond and investing in bond index funds (ETFs). This difference relates to the duration, which has already been mentioned several times here, which is one of the central factors that determines the return and risk of bonds (see e.g. here or here). The duration of an individual bond decreases by one day for every day it spends in a securities account. This means that the bond gradually changes its basic return-risk character, i.e. it becomes increasingly weaker in return and less risky over time. [6] This phenomenon does not exist with a bond index fund. Because the bond index specifies a certain weighted average duration for the basket of bonds contained in the index (and therefore in the fund), the duration of the investment remains more or less unchanged over time and with it its basic return-risk character. This is an advantage for most private investors because it makes it easier to manage the return-risk of the portfolio and they usually did not consciously plan for the falling duration when purchasing.

Furthermore, the ETF investor, relative to the individual bond investor, saves himself the laborious work and transaction costs of replacing bonds in the portfolio that have matured and where the face value was paid out in cash.

Unfortunately, these fundamental advantages of bond ETFs over individual bonds are ineffective when it comes to asset class IIA. The reason: The range of IIA ETFs available in this country is still measly small and, from our point of view, de facto useless for investors in Germany, Austria and Switzerland - at least in the standard configuration relevant to us of a buy-and-hold investor who does not want to make active, speculative bets.

Of the 31 IIA ETFs currently available, twelve focus on US inflation, one on UK inflation, one on a blended emerging market inflation index and nine on more bizarre global inflation indices. Only eight IIA ETFs on Eurozone inflation remain. From our point of view, they have further disadvantages:

- First, all eight ETFs have durations of over five years. This introduces interest rate risk “into the equation” which can completely “swamp” the inflation risk that we are actually concerned with hedging.

- Secondly, all ETFs contain Italian bonds and some also contain Spanish and/or Greek bonds. Not every German private investor will welcome this due to the comparatively high risk of default on the bonds in question.

- Thirdly, from the perspective of a German household, one could criticize the fact that these ETFs do not track the German consumer price index, but rather that of the Eurozone, i.e. h. the “Harmonized European Index of Consumer Prices” (“HICP”). Eurozone inflation is certainly highly correlated with German inflation, but it is not identical to it and as a German investor you probably want to protect yourself against German inflation.

Conclusion

The initial question was “inflation-indexed bonds – how well do they protect against inflation?”

Inflation-indexed bonds tend to have lower returns than conventional government bonds over the long term, while their volatility is likely to be similar and their maximum drawdown is likely to be slightly lower.

In the short term, the lower their duration, the better IIAs protect against inflation shocks (a sudden sharp increase in the rate of inflation), since inflation shocks are usually accompanied by interest rate increases, which have a negative impact on bond yields.

In our opinion, investing in IIAs with ETFs is not advisable based on the IIA ETFs available today. The durations of the available ETFs on Eurozone inflation are too long (and therefore the volatilities are too high). In addition, the credit risk in most of these ETFs may appear too high for some investors due to their “Southern Europe component”.

Anyone who wants to invest in individual IIAs should only do so if they are firmly convinced that the priced-in inflation (breakeven inflation) is too low for a certain period of time, meaning that the actual inflation will be substantially higher. However, this means that the investor is making an active bet on inflation, which we would not do as supporters of a forecast-free investment approach.

The potentially biggest upside of IIAs for the investor is when they purchase them before actual inflation has increased. If it has already risen and breakeven inflation is then higher, IIAs can be viewed – from a speculative perspective – as “expensive” and less attractive.

Financial instruments that provide reliable short-term inflation protection and offer attractive returns do not exist. Historically, simple money market investments (e.g. money market funds) have offered better short-term inflation protection than medium and long-term IIAs, although money market investments here have also failed to meet historical expectations in recent years.

In the long term, i.e. for periods of more than five to ten years, the equity asset class offers the best protection against inflation. Shares currently also have the advantage that they are normally valued (unlike German real estate).

Endnotes

[1] The global stock market is currently valued normally - in contrast to German real estate and bonds with a high credit rating.

[2] That's not entirely true. The American company issued the first IIAs ever Massachusetts Bay Company in 1780. However, by the first 80 years of the 20th century, this form of bond had disappeared from the scene.

[3] Since the actual inflation for a specific period is only known a few weeks after the end of this period, the actual inflation from the corresponding previous period is used for the inflation adjustment. In this respect, the inflation adjustment takes place with a slight delay. However, this purely logistical, unavoidable technical aspect does not, on average, represent any financial disadvantage or advantage for the investor.

[4] When comparing bonds like this, it is important that the remaining terms or, more precisely, the durations of the bonds being compared (or the basket of bonds in the case of an index) do not differ significantly from one another. Otherwise, the interest rate risk of these bonds would be different and would distort the comparison.

[5] This representation is a simplification. In reality, there are other influencing factors than these two particularly important ones. At the same time, one must add that most of the others flow into the two main factors mentioned and are therefore conceptually on a deeper level.

[6] The statement regarding yield only applies during a normal yield curve when short-term interest rates are lower than long-term ones. This has been present around 90% of the time over the last 50 years. If the long-term interest rates are lower than the short-term ones (inverse interest rate structure), this statement does not apply.

Further videos

Heri, Erwin: "Inflation, what to do? Can you protect yourself against inflation? The example of inflation-protected bonds"; Video; August 17, 2021; Internet reference: https://fintool.ch/videos/5d542a04fefe66725d329b1c/inflation-was-tun?token=0c63d01657a6b42d44396186961a0be2

Kommer, Gerd (2021): “Not all inflation is the same: The meaning of expected and unexpected inflation”; YouTube video; May 16, 2021; Internet reference: https://www.youtube.com/watch?v=60XG1RyKsSg