From Gerd Kommer and Alexander Weis

Note: This blog post was updated in May 2024.

Anyone who follows stock market events even superficially knows them: euphoric media articles, YouTube videos and blog posts about the “amazing” returns of “superstar investors”.

Some time ago we took a look at one of these celebrated stock market gurus in our blog Hedge fund manager Ray Dalio. Although Dalio's best-known and largest fund has underperformed a simple ETF benchmark on a buy-and-hold basis for over 15 years, Dalio has managed to still be lauded as an investment celebrity by the media through clever marketing and, in good years, with the management fees of his hedge fund firm's funds Bridgewater Associates to earn around two billion US dollars for themselves personally.

In this blog post we look at another, less well-known hedge fund guru, but one who is often worshiped even more intensively in the financial scene than Dalio: the American James (Jim) Simons and his hedge fund Medallion. Simons died in May 2024 at the age of 86. He was a mathematician by training. The cult-like adoration that he enjoys in the investment community can be seen in the following quotes about his Medallion fund and himself.

- “The Medallion Fund is the largest money printing machine of all time”

- “The best fund of all time”

- “Medallion has by far the best investing track record of any single investment vehicle in history”

- “Jim Simons has been the subject of amazement, admiration and envy for years due to the incredibly high returns from his flagship Medallion fund.”

- “The performance of the Medallion fund represents the ultimate counterexample to the efficient market hypothesis”

- “A Mathematician who became the greatest trader of all time”

Who Simon's hedge fund company Renaissance Technologies LLCIf you google the Medallion Fund and Simons himself, you will find almost endless other anthemic admiring statements like those listed above. For example, one media article states that the ancient King Midas, who was known to be able to turn things into gold just by touching them, “should be ashamed of Simons' achievement.”

American journalist Gregory Zuckerman wrote in 2019 Bestselling book about Simons, which, in terms of its investment-related parts, is just as well the marketing department of Renaissance could have written (the book is also available in a German translation).

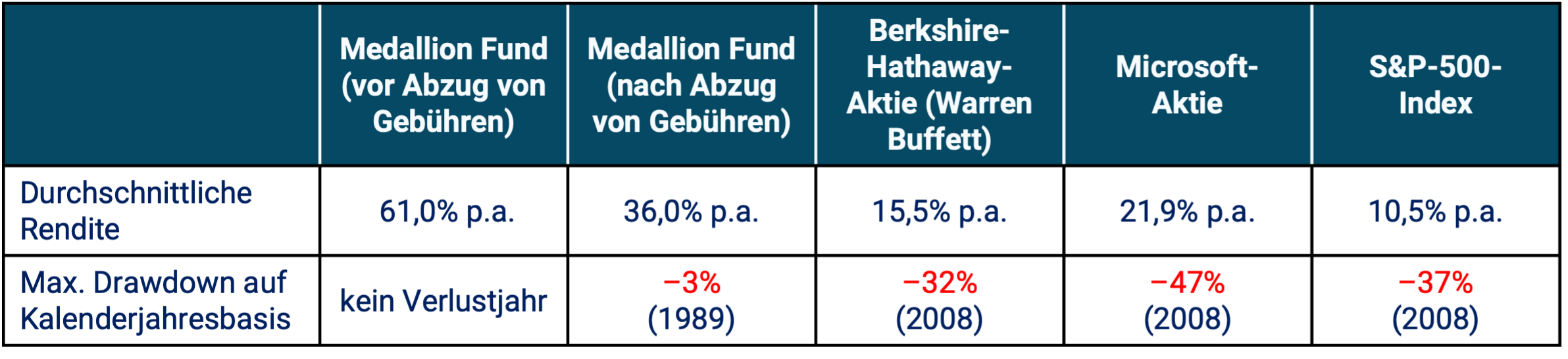

The table below summarizes the return and risk balance of the Medallion fund in the 35 years since the fund was launched in 1988 until 2022.

Gerd Kommer's best fund: The L&G Gerd Kommer Multifactor Equity UCITS ETF. Find out more >

Table: Return and risk of the Medallion hedge fund compared to three benchmarks from 1988 to 2022 (35 years) - nominal in USD

► The Medallion return for the 2023 calendar year is not yet publicly known. ► Data for Medallion from 1988 to 2018 from Zuckerman 2019, then from various media articles. ► Costs not deducted in the case of an S&P 500 ETF. ► Taxes are not taken into account anywhere. ► Maximum drawdown = maximum cumulative (book) loss over the 35 years. Since this calculation is based on full calendar year returns, the maximum drawdown figures are estimated to be 10 percentage points too low everywhere. There are fundamental question marks regarding the risk data for the Medallion fund - see “Argument 5” below in the running text.

The fees for the Medallion fund are exceptionally high, even for a hedge fund. In addition to a fixed fee (fee) of 5% p.a., there is also a profit-dependent fee of between 20% and 44% of the annual return above zero (the profit-dependent fee was 20% in the first few years and then temporarily rose to 44%). However, it is important to note that the fund has no external investors anyway, so those who pay the fees are at least partly identical to those who receive them. Therefore, the pre-fee yield is the more important figure for our analysis purposes.

At first glance, the Medallion Fund's returns before costs and even after fees over this long period of 35 years are literally unbelievable, just as reflected in the quotes mentioned above. The Medallion fund is also phenomenally better off than the three comparable investments when it comes to the reported risk indicator “maximum drawdown”.

We still have serious doubts as to whether this praise is justified and will try to demonstrate the reasons for these doubts using six arguments below:

Argument 1: Lack of publication and transparency requirements for hedge funds

Hedge fund houses are not subject to any publication and transparency requirements like normal investment fund companies. This also applies to Simon's company Renaissance Technologies. Therefore, outsiders cannot know, or can only know unreliably, how many living and “dead” funds (funds that were liquidated in the past due to a lack of good enough returns) that have been currently and historically managed since the company was founded in 1982, i.e. 42 years ago, or are still being managed today. Having said that, media reports – as of the beginning of 2024 – indicate the existence of over 15 Renaissance funds (depending on how you count or “fund definition”, there are only four). The returns of only one, the Medallion Fund listed in the table, are publicly known over a longer period of time and this only accounts for around 20 percent of the investor money currently managed by Renaissance.

Indirectly, one can see from the media that none of the 15+ other funds have produced particularly spectacular returns. We know even less about the dead (liquidated) Renaissance funds, which may also exist. But in order to actually assess the investment performance of Jim Simons or Renaissance, you would have to look at the returns all of its living and dead funds since 1982. The return of a single one of 15+ living funds and probably a few dead ones says practically nothing about the real performance of Simons and Renaissance, especially since the Medallion fund is also a comparatively small fund (more on the important issue of its small size below).

To illustrate, in relation to the founders and CEOs of Microsoft and Berkshire Hathaway – Bill Gates and Warren Buffett – only exists a individual investment, namely the one listed in the table above. Therefore, the investment performance of Gates and Buffett can be reliably and objectively judged from the returns of Microsoft and Berkshire alone. With Simons, however, you cannot derive anything objectively meaningful from the returns of one of over 15 funds, except that one of its 15+ attempts was very successful.

Argument 2: Medallion is not a fund, but a company

The Medallion fund was closed to outside investors in 1993, 31 years ago. [1] Since then, only Simons (or now his heirs) himself and some of his employees have invested in the fund. With only a little exaggeration, it can be said that Medallion is not a “fund” but a “company” that has the word “fund” in its company name for historical and/or marketing reasons. If the terms “fund” and “financial investing” are supposed to have different meanings in contrast to “company” and “entrepreneurial investments”, then Medallion is not a fund, but a company.

Now to the crux of the matter: If you compare Medallion's performance with the return on equity of very successful small to medium-sized companies - not funds - then the Medallion return figures, even from an individual fund perspective, no longer seem so "unbelievable" or "breathtaking", but simply "very good". Thousands of small and medium-sized companies - listed and many more unlisted - worldwide have delivered similarly high or even higher average returns on equity over the past 20, 30 or 40 years.

Argument 3: Lack of scalability of the Medallion strategy

Not only was the Medallion fund closed 31 years ago, it is also quite small because, with the exception of the early years, its profits have always been distributed. According to press reports, the fund has never had a volume of over ten billion US dollars. [2] Relative to a large listed company or a large conventional investment fund, the volume of the Medallion fund is therefore “manageable”. The largest index fund in the world is around 47 times as large, and Microsoft, measured in terms of market capitalization, is 300 times as large (as of April 2024). Why is this relevant? Simply because it is infinitely easier to generate high percentage returns on a small investment than on a large one. Not only that. A low return on a sufficiently large investment is more attractive than a high return on a small investment. What would you prefer? 60% return on $10 billion (i.e. $6 billion) or 15% return on $1,000 billion ($150 billion)?

In this context, one can go one step further and ask why the Medallion fund never had a volume of more than ten billion. Answer: The investment strategy cannot be scaled, i.e. applied to a significantly larger fund volume, without destroying its effectiveness.

This does not apply to investments in large listed companies. Although such companies generate far lower percentage returns than Medallion, they still create much more shareholder value in the unit of measurement that really counts, namely monetary units - not percentage returns based on a comparatively small assessment base. To illustrate: Medallion's average annual return since 1988 is over 60%. [3] With a reference figure of $10 billion, this means the creation of $6 billion per year in new shareholder value. Microsoft generated an average of around $350 billion in shareholder value annually over the past five years. The world's largest index fund generated shareholder value of over $110 billion in 2023.

Argument 4: Questionable calculation of the Medallion return

Because all of the Medallion Fund's profits were always distributed, the final net worth calculations made by its industry admirers are simply wrong: A modest one-time investment of $1,000 was invested in the Medallion Fund in 1988 for 35 years. With the above-mentioned average return of 61% p.a., today that would result in the fairytale final sum of 17 billion dollars before fees or, based on the after-fee return of 36% p.a., 47 million dollars - in each case before taxes. (The big difference is explained by the compound interest effect.)

However, such “funny” calculations, which even a mathematician did in one of the articles listed below (Edesses 2019), assume that all annual profits were always immediately and completely reinvested (accumulated) in the fund. But that wasn't the case with Medallion - if you exclude a few years at the very beginning, no profits were reinvested because that was and is not compatible with the fund strategy.

From a financial mathematical point of view, it would therefore be correct to assume “normal” returns for the distributed profits. However, this would dramatically reduce the corrected actual Medallion investment return. (Note: This technical issue generally applies to a normal distributing investment fund, but you can ignore it with a conventional fund because - unlike Medallion - reinvestments in the fund are permitted and possible without any problems.)

More recently, two scientists have published an article (Guo/Liu 2022) in which, based on a different financial mathematical argument, it is generally questioned whether the “official” average return of the Medallion fund of over 60% p.a. before fees is even correct. The scientists come to the conclusion that the actual pre-fee return is probably only about half as high. The average return after fees (which is not determined in the essay) would then be well below the “official” 36% p.a.

Argument 5: Return Smoothing of Hedge Fund Returns

It has been known and undisputed in the academic literature on hedge funds for decades that the figures communicated by hedge funds to the outside world regarding their risk in the form of volatility and drawdown are often embellished, i.e. smoothed (“return smoothing”). [4] Reason: Because most hedge funds invest more or less extensively in unlisted assets, they must or are allowed to estimate the price changes of these assets themselves and then communicate these own estimates to investors and index providers. Considering that hedge funds are ultimately not subject to supervision, it will come as no surprise that the fluctuations in these estimates are calculated to be “somewhat muted.” In industry jargon this is called “marketing-supportive accounting”. We therefore have to put a big question mark on the nice risk balance of the Medallion fund in the table. Furthermore, only calendar year returns are publicly known for Medallion. We know nothing at all about the daily or monthly fluctuations of the fund.

Argument 6: Medallion returns do not contradict the efficient market hypothesis

The fifth of the praises for the Medallion Fund given at the beginning is “the performance of the Medallion Fund represents the ultimate counterexample to the efficient market hypothesis” (Bradford 2020). This statement is outrageous from a statistical and scientific point of view, even if in this case it comes from a doctor of financial economics. The result of a single investment, even one over 30 years, cannot refute the Efficient Market Hypothesis (“EMH”). The EMH naturally allows for the occurrence of outperformance, even extreme outperformance.

The EMH simply states that with publicly available information it is unlikely to beat a correctly chosen benchmark based on costs, taxes and risk over an extended period of time. The EMH doesn't say anything more, even if further statements and claims are regularly attributed to it. Beating the benchmark by chance is of course consistent with the EMH and is even likely given that there are hundreds of millions of actively managed funds and portfolios worldwide. We clearly cannot rule out this coincidence for the Medallion performance, even if the Medallion track record does not look like a coincidence at first glance. Only if the weighted average return all If 15+ Renaissance funds were far above average over 20+ years, one could or should certainly conclude using the usual statistical methods that the outperformance of Medallion individually and Renaissance Technologies as a whole is not due to luck, i.e. chance.

Conclusion

This blog post wanted to shed more light on the investment track record of the legendary hedge fund manager Jim Simons, which is regularly acclaimed on the Internet. The available data and information seem sobering to us - we just have to evaluate them critically.

The only thing we can say with certainty about Jim Simons financially is that he was a brilliant entrepreneur. Because he was, his personal net worth was over $30 billion as of early 2024. However, Simon's success as an entrepreneur says nothing about his performance as a financial investor and fund manager. Unfortunately, the personal wealth of hedge fund managers is repeatedly misinterpreted by journalists and private investors as a sign of investment success for investors. A surprisingly common mistake made by financial journalists and finfluencers.

Ultimately, we know little that is reliable when it comes to Simon's overall performance as a financial investor and fund manager. What we know about a single, relatively small one of his investments - the Medallion Fund - certainly does not justify the many embarrassingly submissive, often downright fawning praises in the media and on the Internet.

Jim Simons must be praised and thanked for his great philanthropic commitment. According to media reports, he donated six billion dollars to charitable causes during his lifetime. He also made impressive research achievements in mathematics. As a person, as a mathematician and as an entrepreneur, Simons was at the very top and for that he deserves our admiration. Ultimately, we don't know where he stood as an investor.

All in all, Simons, Medallion and Renaissance are a textbook example of how comprehensively the media fails in its responsibility to correctly interpret return data from the financial industry for private investors.

Endnotes

[1] In 2003, some of the existing investors who were not Renaissance employees were “terminated,” meaning their capital in the fund was paid out against their wishes.

[2] According to individual media reports, the fund volume has recently been increased to $15 billion. Other sources still state ten billion.

[3] In the following argument we will address the doubts that researchers have recently expressed about the correctness of this number.

[4] Cliff Asness, head of the fund company AQR, who is well known in the hedge fund scene, has the descriptive term for return smoothing in the reporting of hedge funds and private equity funds Volatility Laundering (from Money Laundering = money laundering).

literature

Celarier, Michelle (2020): “Renaissance’s Medallion Fund Surged 76% in 2020. But Funds Open to Outsiders Tanked;” Internet reference: here

Celarier, Michelle (2021): “Providence’s Troubled Pension System Bet Big on Renaissance Technologies — And Lost”; Internet reference: here

Celarier, Michelle (2021): "The Medallion Fund Is Still Outperforming. Other Renaissance Funds Still Aren't"; Internet reference: here

Cornell, Bradford (2020): “Medallion Fund: The Ultimate Counterexample?”; In: Journal of Portfolio Management, Vol. 46, No. 4, 2020

Edesess, Michael (2019): “Was Renaissance’s Success Luck or Skill – And Was It Behind Trump’s Victory?” Internet reference: here

Fox, Mathew (2022): “Secretive hedge fund Renaissance Technologies reportedly sees $15 billion in outflows”; Internet reference: here

Guo; Shuxin/Liu, Quang (2022): “Is the annualized compounded return of Medallion over 35%?”; July 2022; SSRN/Social Sciences Research Network here

Gränitz, Marko (2020): “The best fund of all time”; Internet reference: here

Lipscomb, Sam (2021): “Renaissance Technologies Review”; Internet reference: here

Maggiulli, Nick (2019): “Why the Medallion Fund is the Greatest Money-Making Machine of All Time”; Internet location: here

Zuckerman, Gregory (2019): “The Man Who Solved the Market: How Jim Simons Launched the Quant Revolution”; Nov 2019; portfolio; 384 pages (the book is also available in German translation)