From Alexander Weis

The story begins with a person I have never met - my fiancée's grandmother. For the purposes of this description, let's call the grandmother Dagmar. Dagmar died in 2021 at the age of 83. She was a widow and had a daughter, we call her Britta, my partner's mother. Dagmar lived in a small town in the Ruhr area. Dagmar was what you often imagine an older lady from this generation to be: disciplined and reserved. She had had a long life and, together with her husband, who died in 2010, had built up a considerable fortune through hard work, discipline and thrift. The liquid part of it, several hundred thousand euros, had – “of course” – been with “their” savings bank for decades.

After her death, Britta, the daughter, inherited Dagmar's depot. In it: securities, funds, investments. For someone who is not concerned with financial products and investments - and Britta was one of these people - this portfolio initially looked impressive: valuable, complex and competent.

My fiancée, Britta's daughter, asked me, a financial advisor at Gerd Kommer, to take a look at the whole thing. And what I saw was so typical that it was almost textbook-like: an investment structure that was not built for the customer, but for the bank. A strangely structured portfolio of actively managed funds with high fees and low performance, closed-end investments, high-yield bonds, mixed products with "ambitious" names - the whole thing framed by an asset management mandate that skimmed off painful amounts of fees every year without providing any discernible added value in the form of a sensible risk-return combination. It was not asset management, not financial advice, but a form of creeping asset reduction or, to put it another way, the sneaking transfer of Dagmar's money to the savings bank - the whole thing disguised as "support".

And as luck would have it, the disaster became visible not only through the deposit itself, but also through the reaction of the responsible savings bank employee to a few harmless questions that are completely normal in the context of an inheritance. This reaction activated a red light on my fiancée.

When we asked what fees the depot had generated in the past, the savings bank advisor's initially friendly tone quickly turned into gruff irritation. Instead of numbers, he now came with empty phrases, and instead of transparency, a mixture of justification, appeasement and denial.

So what began as a simple request for self-evident information became a case study about ripping off old people by a public bank, about bank “advice,” about power relations between small customers and a large institution, about fee models and about a business model that thrives on customers simply accepting and dutifully enduring poor returns and high fees.

In this post I tell that story. First we look at the depot, then the fees and then the communication. And finally, how we ended the tragedy and replaced it with a sustainable solution.

The depot

Looks like structure, but it's just sales

Before we get into the details of the individual portfolio positions, let us first provide an overview of the initial situation. I would like to say in advance: The customer advisor did not provide us with documented coordination of specific target figures for expected returns, risk and liquidity.

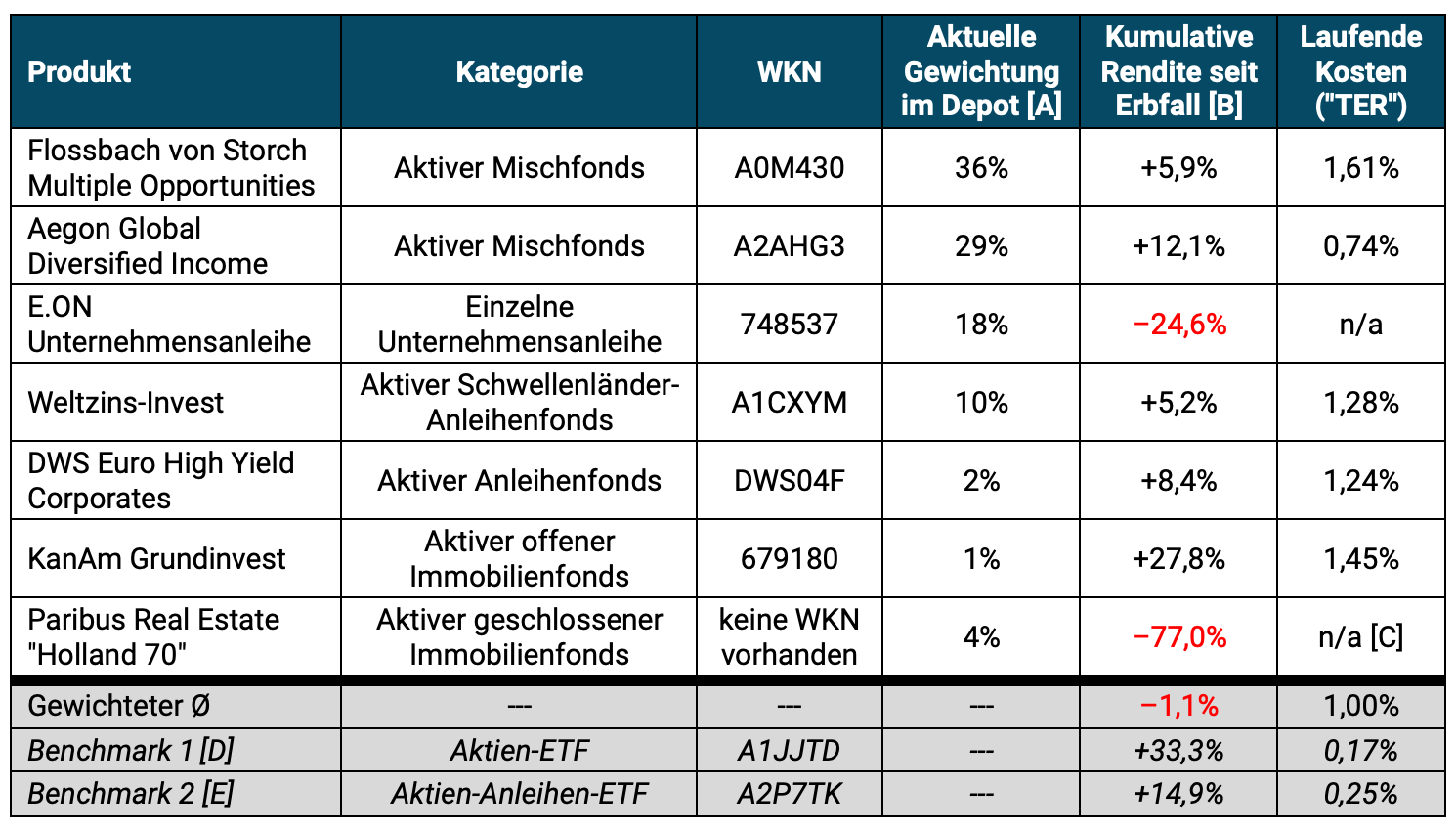

The portfolio consisted of four actively managed funds, an open real estate fund, a closed real estate fund and a corporate bond (see table below). Overall, the composition indicated a portfolio that had grown haphazardly over the years, with new additions and holding decisions and the overall structure clearly not being made on the basis of a consistent investment plan that was suitable for the portfolio holder's specific circumstances.

The documents and reports presented to us by the “advisor” lack meaningful information on the long-term performance of the overall portfolio, e.g. B. since the depot was opened or at least in the last five or ten years. As far as we can tell based on the unsystematic and sparse information presented by the advisor, the return was well below a passive ETF benchmark on a buy-and-hold basis. At the same time, the running costs were in a range that is above average for private investor portfolios.

The reporting provided was limited to static portfolio overviews and individual value statements. There is a lack of aggregated evaluations of performance (return and risk), fluctuation range or portfolio structure, as well as indications of rebalancing, reallocations or strategic adjustments.

During the course of the analysis, there was a fairly extensive email exchange with the consultant. We asked questions about costs and the composition of the depot. The answers were evasive and formalistic and became more and more pat with each new email. There was no open discussion about the structure or purpose of the portfolio.

Since the consultant did not provide any comprehensive, systematic documents and no such documents were found in Dagmar's estate, our subsequent analysis must be limited almost exclusively to the current portfolio status and the associated portfolio overview for the period between the portfolio transfer to Britta as part of the execution of the will, September 8th, 2021, and today, the end of July 2025. But even this almost four-year period speaks volumes. The securities account statement also showed that there have been no reallocations, product swaps or rebalancing since the securities account transfer in 2021 to date, i.e. h. The savings bank no longer managed the deposit but left it untouched.

For these reasons, the following assessments relate exclusively to current parameters such as ongoing costs, liquidity or the role of individual positions in the overall structure. Even though the analysis is based on a limited period of just under four years, we can assume that the identified structural weaknesses - particularly with regard to diversification, cost efficiency and portfolio architecture - probably already existed before the start of the analysis period.

The following table summarizes the structure of the depot:

Table: Britta’s savings bank deposit as of July 21, 2025

Return data: comdirect.de /// All information on returns and costs without the separate, additional mandate fee (see ongoing text below). /// Returns including any distributions (total returns) from the portfolio transfer on September 8th, 2021 after the deceased grandmother's inheritance until July 21st, 2025 (~3.9 years); only return on the “Holland 70” position due to a lack of data availability since subscription. /// [A] Current weighting in the overall portfolio as of July 21, 2025 /// [B] Cumulative return since portfolio transfer after inheritance (September 8, 2021) to today (July 21, 2025) /// [C] The fund is being wound up/liquidated, therefore no information on ongoing costs is available; In general, the running costs of closed real estate funds are above 5% p.a. a. of the invested equity. /// [D] Passive Benchmark 1 (stocks): SPDR MSCI All Country World Investable Market UCITS ETF /// [E] Passive Benchmark 2 (stocks and bonds): Vanguard LifeStrategy 60% Equity UCITS ETF /// All information to the best of our knowledge and belief, but without guarantee.

This overview suggests what characterizes many managed bank deposits: diversification on paper, inexplicable complexity or lack of transparency and high-priced financial products. There seems to be a lack of a well-thought-out structure tailored to the specific circumstances, living conditions and investment goals of the portfolio holder.

The largest individual positions and a brief return assessment at a glance:

- Flossbach von Storch Multiple Opportunities: An equity-heavy, actively managed mixed fund. Cumulative return of the fund over the period under review (3.9 years): 5.9% compared to the return of a passive ETF benchmark with a similar equity allocation, the Vanguard LifeStrategy 80% Equity UCITS ETF (WKN: A2P7TF) of 24.9%. Ongoing annual costs of the Flossbach fund: 1.61% vs. 0.25% for the benchmark.

- Aegon Global Diversified Income: Also a mixed fund, but slightly less stock-heavy than the Flossbach fund. Cumulative return over the period under review was 12.1% compared to the return of a passive ETF benchmark, the Vanguard LifeStrategy 60% Equity UCITS ETF (see table) of 14.9%. Ongoing annual costs of the Aegon fund: 0.74% vs. 0.25% for the benchmark.

- World interest rate investment: A medium duration global bond fund investing in foreign currency bonds of emerging market countries. Cumulative return over the period under review: 5.2% compared to the return of a passive ETF benchmark, the L&G Emerging Markets Government Bond (USD) 0-5 Year UCITS ETF (WKN: A2QFQ5) of 9.8%. Ongoing annual costs of the Weltzins fund: 1.28% vs. 0.25% for the benchmark.

- DWS Euro High Yield Corporates: A bond fund that invests in Eurozone companies with low credit ratings. Cumulative return over the period under review was 8.4% compared to the return of a passive ETF benchmark, the iShares EUR High Yield Corporate Bond UCITS ETF EUR (WKN: A2DUCZ) of 9.9%. Ongoing annual costs of the DWS fund: 1.24% vs. 0.50% for the benchmark.

- E.ON corporate bond: As an individual position with a relatively large portfolio share of 18%, this bond represents a strange foreign element of risk in the portfolio. The return of -24.6% speaks for itself. Only the gods know what this bond is supposed to do in the portfolio of an 80-year-old widow.

- KanAm Grundinvest: An open-ended real estate fund that stumbled after the turbulence of the financial crisis and the Euro crisis in 2011. It has been in liquidation ever since. Surprisingly, the fund achieved a cumulative return of 27.8% over the period under review - significantly better than its passive counterpart, the iShares European Property Yield ETF (WKN: A0HGV5), which lost 18.7% in value over the same period. It is difficult to say whether this was a temporary recovery or a late recovery. However, it remains unclear why the fund was included in the portfolio with less than 1% weighting - this mini position hardly made strategic sense.

- Paribus Holland 70: A closed real estate fund that has also been in liquidation for years due to large losses. A return of the shares is not possible. On the secondary market, the fund is trading at a 77% discount to the last reported share value. Putting such a highly complex, structurally illiquid financial product - a company investment - in an old lady's portfolio seems downright negligent.

The relative underperformance of the portfolio would be of a similar magnitude if one had not looked at the last 3.9 years (the period from which the portfolio was transferred to Dagmar's daughter Britta) as in the table, but rather the longer period of five years. We didn't calculate any further back because, due to a lack of information from the savings bank, it was not clear whether there were any significant portfolio changes in the period before Dagmar's death.

What is striking about the portfolio is that, with the exception of the E.ON corporate bond (which is a problematic component of the portfolio for risk reasons), it was all high-cost products. They were not bought into the portfolio because they fit each other, but because they bring high commissions to the custodian bank. The fact that apparently neither issuing surcharges nor excessive trading were charged is a small consolation - but it does not change the basic problem: the product selection was not independent.

The obvious solution would be a compensation system that is completely independent of specific product selections - and therefore free of sales interests and harmful conflicts of interest. In this case, product selection was only half the story. In addition to the funds' internal cost burden, there was another layer of fees on top - the bank's mandate fee.

The fees

“There are no costs” – said the “advisor”, and meant: “no costs other than the ones I’m not telling you”

In addition to the internal costs of the funds - which were already around one percent in weighted average - Dagmar's portfolio added a second layer of fees: the mandate fee. An administration fee that goes directly to the bank for supposedly ongoing management of the portfolio. According to the price list, between 0.7% and 1.5% per year based on the portfolio volume - in addition to the ongoing costs (TER) of the funds.

Our question to the savings bank advisor was simply: “What ongoing costs arise from the depository mandate?”

His answer was:

"There are no custody fees and half of the mandate fees are offset against tax. With the exception of the Storch Flossbach, all positions are charged at 0.7% (see also the list as a PDF). This is a special condition as part of the support for the entire family group."

Sounds caring – almost like a loyalty bonus. But something crucial is missing between the lines. The largest position in the portfolio, the Flossbach from Storch Multiple Opportunities, is priced according to the model with a mandate fee of 1.5% per year - in addition to the fund's already high TER of 1.61%. This number does not appear in the email text, but only in the attached PDF. If you don't open the attachment, you get the impression: "0.7% for everything". Anyone who opens it will see that more than a third of the depot is being charged twice as much as claimed.

The mentioned “tax credit” simply means that the actual fee is a quarter lower than the stated fee due to tax credit. Three quarters of the fee still remains with the investor.

This selective transparency is no accident. It is method. And it follows a familiar pattern: first simplify, then trivialize, then keep quiet.

Similar with the issuing premiums, which the bank advisor lovingly refers to as “premium”, probably because that sounds less negative. For several funds, additional fees were charged upon purchase, which were then fully refunded. That sounds like a fair deal - and that's how it was communicated by the consultant:

“The issue surcharges were fully credited back to the customer, so that she did not incur any costs.”

That sounds generous. In reality, it is a rhetorical trick: an unnecessary and high fee is charged, only to then waive it again as a service. You could also say: you trip up the customer and then help him up again.

The whole thing was crowned by the following passage:

"If you then take into account the fact that no custody fees are charged, half of the mandate fees paid are counted as a tax allowance and all of your own transaction costs are not calculated, we would actually be in the black with this model. So we are talking about no fees."

A remarkable sentence. The bank charges product costs of around 1% on average, plus mandate fees of between 0.7% and 1.5% (depending on the product) - and then claims that the customer pays "no fees" but that the bank adds money.

It becomes particularly bitter when you ask what was actually paid for all these fees. The depot has not been adjusted for years. No reallocation. No rebalancing. No recognizable controls. Just a return that was significantly below that of a passive benchmark, at least during the period under review.

The advisor

Communication as a defense and concealment tactic

Products can be expensive. Fees can be concealed. But in the end, it's the tone that decides whether you're dealing with a service provider - or with a system that doesn't tolerate any questions. In this case the latter was clearly noticeable.

We asked politely: about the running costs, about the structure of the mandate, about the background to the composition of the portfolio. The answers did not really help in assessing whether the savings bank had met its customer's legitimate goal: to achieve a return-risk combination that was at least at the same level as that of a passive ETF benchmark on a buy-and-hold basis.

The advisor's defensive, defiant attitude became clear when he defended his "non-communication" and poor portfolio performance by pointing out that he had "been looking after clients for decades." In reality, the length of the customer relationship is of course no quality criterion, especially in such a case. This became even clearer in the next sentence - a kind of oath to one's own infallibility:

“For decades, it has been our obligation for the entire family group to ensure the security of investments, value development and trusting cooperation, and this also means that everyone can rely on us to ensure the best possible option, also with regard to advice and the associated costs.”

Full of pathos, full of self-assurance - but empty of content. What is “the best possible option”? Who decides what “trustworthy” means? And what’s left of “performance” if the portfolio has made poor returns?

In truth, it's not about advice, but about interpretative sovereignty. Criticism is not answered, but rather framed morally. And when we finally asked for concrete figures, for documents and for plain text, there was an attempt to stall the conversation:

“I hope that we can finally answer this annoying topic with this email.”

“Sore topic” – this is not how we talk about transparency, but rather about disruption. It's framing that turns a legitimate question into a problem. It's not the fees that are the problem - it's the fact that someone wants to know them. And the word “final” is not a factual conclusion. It's a rhetorical cover.

At this point you finally understand that it's not just about costs, but about fear and control. Not about numbers, but about the power over their interpretation. It's not about service, but about sovereignty in interpretation. And it's about who makes the rules - and who has to tacitly accept them.

The solution

Get out of the high-priced lack of transparency

Since neither the communication nor the portfolio structure or performance were right, we decided together within the family to sell all positions and put an end to this tragedy.

We invested the proceeds in a simple, globally diversified 60/40 portfolio of stock and bond ETFs. Specifically: For the equity part we chose the L&G Gerd Kommer Multifactor Equity UCITS ETF (WKN: WELT0A), for the bond part we chose the iShares EUR Ultrashort Bond UCITS ETF (WKN: A3DJQJ) made of short-term corporate bonds with a high credit rating and no currency risk.

Outro

Dagmar's unspeakable deposit was not the mistake of her individual advisor, but the almost inevitable result of a bank business model with a decades-old remuneration system in which conflicts of interest are structurally embedded. As long as banks and consultants are controlled by product commissions, in-house products, margin targets and commissions, the result for their customers in the long term will most likely look like Dagmar's Depot: high-priced, non-transparent and with lousy returns.

If you want to avoid this, you have two options: invest in do-it-yourself mode without an “advisor” or asset manager or choose a service provider who consistently avoids commissions, in-house products, sales charges and income from unnecessary back-and-forth in the form of trading. Everything else would be bogus solutions.

Dagmar's case seems particularly bitter because the bank was a savings bank. A publicly funded institute. Although savings banks do not have a public welfare mandate, for obvious reasons they are even less likely to be seen as ripping off their customers.