From Gerd Kommer and Jonas Schweizer

Almost every day in the media you can read about the “overvaluation of the stock markets” and that “now is not the right time” to “enter the market”. In April 2018, the fund manager and “stock market expert” Dirk Müller, also known as “Mr. DAX,” warned in an interview: “The situation on the markets is extremely dangerous; more dangerous than ever before in our lifetime.” Müller expects a “systematic crash from which the stock markets will not recover for decades.”

During Dirk Müller's lifetime there were four major stock market collapses: the first in the 1970s, triggered by the 1973 oil crisis; the fourth in the form of the Great Financial Crisis from the end of 2007. In one of these collapses, the dot-com crisis, the DAX lost almost 70% in the 39 months to March 2003. If you believe Mr. DAX, things that develop from the current market situation will probably be even worse than back then, i.e. h. We are in for an even deeper than the 70% crash of a broad stock index and/or more than a decade of zero returns. Ouch!

Let's ignore for a moment this single one among the dozens of crash predictions that have made the rounds at any point in the past 20 years, including every year since 2014, and focus on what the facts say, which have not been selectively chosen to rationalize a fund manager's individual investment strategy.

- Let's start with the DAX: Although the DAX was not far from its historical high (13,596 on January 23, 2018) with an index level of 12,605 on May 31, 2018, German stocks were not overvalued at that time, as we will see shortly. Index levels like the DAX are from a valuation perspective per se irrelevant. Inflation alone ensures that securities indices continually reach new historical highs in the long term. This could be the case even if the market in question was undervalued for years or decades. A stock index is not a valuation indicator, even if many “experts” in the media and the financial industry apparently haven’t noticed that yet.

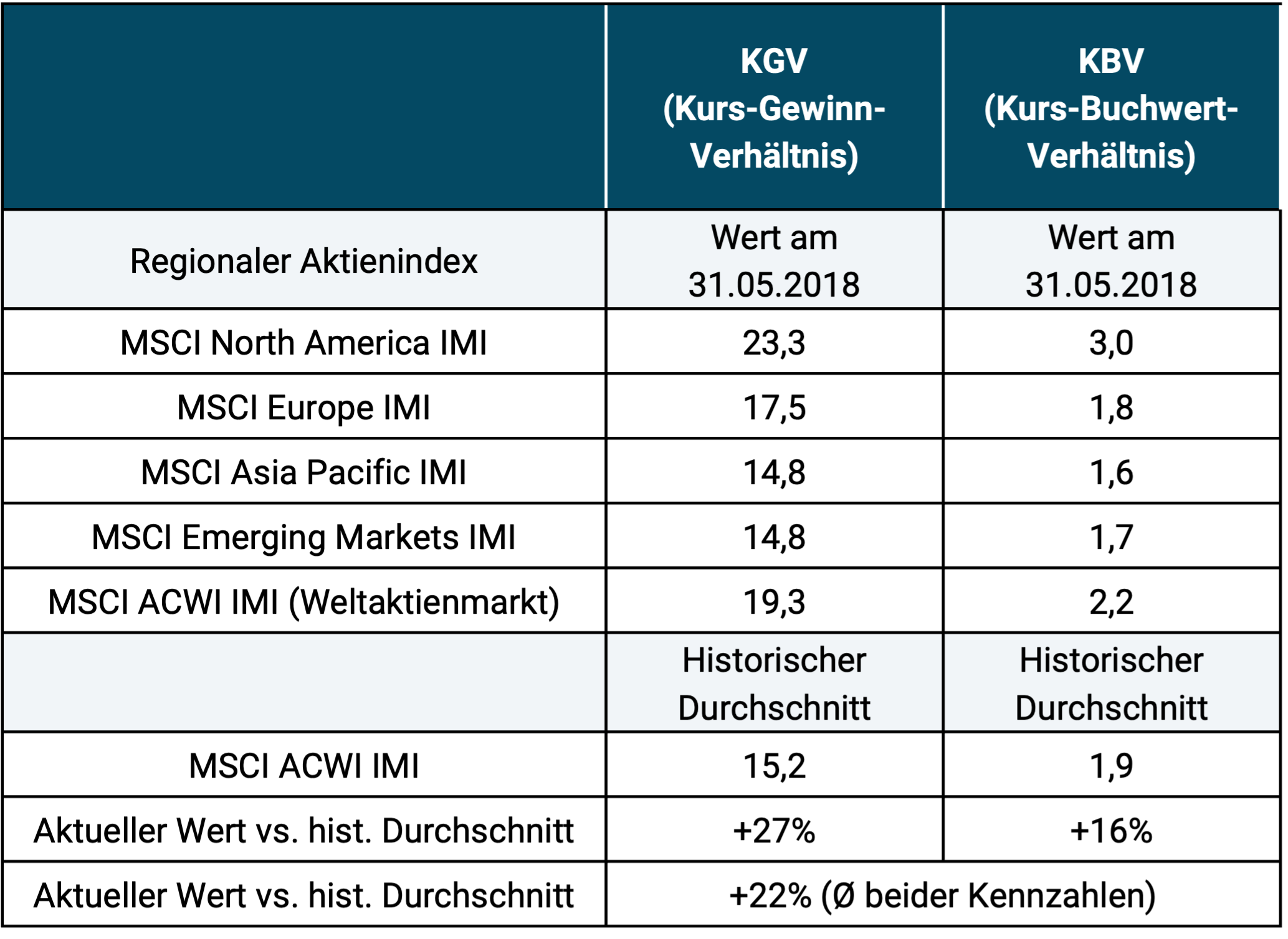

- The most commonly considered and undisputed valuation indicator for a stock market is the market P/E ratio (price earnings ratio). The P/E ratio of the MSCI Germany Standard stock index, which is similar to the DAX, was 15.7 at the end of May 2018, close to its historical average.

- The world stock market measured by the MSCI ACWI IMI index was at the end of May 2018 a P/E ratio of 19.3 and a price-to-book ratio of 2.2. On average, these two best-known valuation metrics resulted in an overvaluation of 22% relative to the historical average (see table). Some would describe 22% as “moderate”, others perhaps as “considerable”, but probably no one as “dramatic”.

Table: Comparison of current stock market valuations for different regions with the historical average valuation level

► Notes on the table: The MSCI ACWI IMI Index (All Country World Index IMI) covers all industrialized and emerging countries (approx. 98% of the market capitalization of the world stock market). ► The historical average was determined from the last ten years.

- Stocks can remain at overvalued levels for years and decades. Overvaluation alone does not lead to an imminent crash. For example, if we use the famous Shiller P/E ratio, also known as the CAPE ratio, [1] The US stock market was overvalued in 290 out of 300 months over the last 25 years from May 1993 to the end of June 2018. That means that 96% of the time over the past two and a half decades – not just the one or two years before a sharp decline – the stock market has been above its historical average valuation since 1881.

- In the long term, shares produce a return that is around six times as high as so-called “risk-free investments” (e.g. government-guaranteed overnight funds, savings account balances or short-term high-quality government bonds). This average return, which is six times higher, naturally includes the losses from the numerous stock market crises over the last 100 years. Even if stocks, e.g. B. measured by the market P/E ratio, were overvalued by a good 250%, their expected return in the future would still be as high as the expected return of the “risk-free” investment, provided it was “fairly” valued. In fact, risk-free investments are also currently highly valued, so their expected return today is lower than our calculations.

- All three main asset classes (stocks, interest-bearing investments and real estate) were “expensive” in mid-2018. h. they were valued higher than their historical average according to the usual metrics used here (interest-bearing investments, including bonds, are valued higher the lower the interest rate level is). Reviews are always relative to see, because investing in “nothing” or “not investing” is literally impossible. Anyone who talks about high valuations and doesn't say in the same breath what they invest their money in instead should have their fool's cap put on.

- From a scientific perspective, there is no evidence that “crash timing”, i.e. the systematic attempt to avoid severe stock market downturns by “in and out”, works reliably enough (example: Boudoukh et al. 2018). Rather, the opposite seems to be the case: practicing this form of market timing is very likely to be wasting money on a buy-and-hold investor in the long term. Anyone who looks at crash timing rationally should actually recognize that it is not a safety measure, but rather a highly risky undertaking.

- Is felt always the wrong time to invest in stocks. 70% of the time, according to one or many well-known experts from the media or the financial industry, stocks are “too expensive” and the remaining 30% of the time, according to the experts, “it is better to wait until the markets have calmed down again and a sustainable recovery or upward trend can be seen”. An example: In March 2009, the global stock market reached its lowest point during the Great Financial Crisis after around 16 months of downward movement. It was of course unclear at that moment whether this would be the final bottom. In the first half of 2009, the guide book “Crash Course” by expert Dirk Müller was published. On page 140 of the book he wrote: “Stocks and equity funds simply do not belong in your portfolio in these uncertain times.” In the twelve months from July 2009 the DAX rose by 24% and in the 24 months from July 2009 by 53%. Today, at the end of June 2018, the DAX is 257% above the July 2009 level. So following Mr. DAX's assessment was a costly undertaking.

- For young investors or - to put it more precisely - any investor who has invested less than half of their lifetime savings up to this point, a crash is a godsend because after the crash this investor can invest much more cheaply and therefore more profitably for many years than before the crash. American financial economist and author William Bernstein put it this way: “If you are a twenty-something in the beginning of your savings phase, get on your knees and pray for the next crash.”

- It is guaranteed that a crash will come at any valuation level, regardless of whether we are at an above-average, average or below-average level. What is not guaranteed, however, is when the crash will come, how deep it will be, how long it will last and which asset classes it will affect; Stocks, interest-bearing investments, real estate, precious metals, raw materials, collector's items or several at the same time. What is also not guaranteed: whether it will be a short, violent, widely visible crash (as is typically the case with stocks, precious metals and raw materials) or a gradual, slow, “less visible” one, as is often the case with real estate, e.g. B. in German residential real estate in the now forgotten 29 “slow-motion crash years” from 1981 to 2009.

All in all, we can sum up: Anyone who stands on the sidelines of the stock market, as most Germans do, will have to pay dearly for this passivity in the long run, in the form of lost asset growth on a potentially hefty scale. Effective retirement planning from the sidelines is impossible.

If the stock markets (or the real estate asset class or any other asset class) seem too risky, you need to make your asset allocation more conservative instead of speculating on short and medium-term market movements.

From our point of view, the wisest thing to do is to always invest the funds that come to you over the course of your life in accordance with the household-specific asset allocation as soon as the funds arrive in your own checking account; completely independent of the alleged or actual market conditions at that moment and the media noise surrounding it. This applies to small amounts that can be squeezed out of your salary every month, medium amounts such as a salary bonus or large amounts such as a large inheritance or a lottery win. Risk management should not be done through market timing, which in most cases is detrimental to returns in the long term, but rather through an asset allocation that is appropriate to your circumstances. For stocks, this includes systematic global diversification, which eliminates a significant portion of the risk of fluctuations in the value of individual stocks in these asset classes.

The following “entry strategy”, which is based on investor psychology, may help anyone who wants to invest a large one-off amount in the stock market for the first time: drawing up an “investment phase plan with self-commitment”. This phase plan could, for example, look like this: (a) You invest a quarter today and another quarter in each of the three following quarters (total duration 9 months). (b) You invest one sixth of the investment amount immediately and then another sixth every six months (total duration 30 months). In any case, you have to implement the originally planned plan consistently and purely mechanically, regardless of which direction the markets move in the short term. With such a plan, an investor can actually only win emotionally: If the market rises after the initial investment, the investor is happy about the increase in the value of his portfolio and about his wisdom in not having postponed the investment. If the market falls, he now has the opportunity to buy at cheaper prices and will feel confirmed in his decision not to have invested everything at once.

However, it should be taken into account that, in retrospect, this entry plan, which is purely psychologically motivated to reduce risk, is always only the second-best solution. If the prices rose on balance during the “extended” investment phase, then it would have been better to invest everything immediately; if they fell, it would have been better to invest everything at the end. With this approach, the investor is never completely wrong in retrospect, but also never completely right.

All in all, we should simply ignore the never-ending barrage of the media about the impending demise of the world, the West or the stock market and stoically, stubbornly and long-term invest a fixed portion of our assets in the global economy, tailored to our personal circumstances, over decades. The best and easiest way to do this is with a globally diversified index fund.

Endnotes

[1] See English Wikipedia, keyword “Cyclically adjusted price-to-earnings ratio”. The Shiller P/E was developed by Nobel Prize winner Robert Shiller in economics.

literature

Boudoukh, Jacob / Ronen Israel / Matthew P. Richardson (2018): “Long Horizon Predictability: A cautionary tale”; Internet reference: here; Accessed May 28, 2018