From Gerd Kommer and Tobias Jerschensky

In a YouTube video by British finance professor Patrick Boyle about the current crisis in the UK commercial real estate market, Boyle says "No-one loves leverage more than real estate investors" [1] (Video link here). In fact, the crisis in the commercial real estate market in the UK, Germany, USA and other countries since 2022 has a lot to do with too much debt in the commercial real estate sector. Boyle's sarcastic remark about the popularity of debt financing and the credit leverage effect among real estate investors is correct. To illustrate this, here are relevant statements from German real estate finfluencers: [2]

- “Use as little equity as possible” – chapter title in an advice book on investing in residential real estate by Florian Roski and Mario Geiss

- “You won’t get rich without debt” – real estate finfluencer Tobias Claessens in a LinkedIn post from October 2023

- "Building wealth through real estate is possible for everyone. Even for you, without a lot of equity." – Title of a TikTok video from March 2024 by real estate finfluencer “Immo-Tommy” [3]

- “The leverage effect makes real estate investors really rich!” Title of a marketing video on the real estate agent's website Bartz Real Estate

In this blog post we would like to show that the leverage effect in real estate investments is presented alarmingly uncritically by many representatives of the real estate industry, including brokers, property developers, real estate finfluencers, providers of courses on investing in real estate (“real estate coaches”) and authors of advice books in the “Get rich with real estate” category.

We believe this primarily because there is simply no scientific or otherwise objective, hard evidence and figures that show that the credit leverage effect in real estate financing has even a somewhat reliably beneficial effect.

This is the result of our evaluation of the specialist literature from authors without conflict of interest on the effect of leverage in real estate investments. This involves both professional commercial investors and investments by private households - small landlords [4] and owner-occupiers. In Appendix 1 at the end of this article, we list a dozen specialist articles that show that a high proportion of debt capital in commercial and private real estate investments statistically has no financial advantage or is even detrimental to returns, i.e. it worsens either the absolute return on equity or at least the risk-weighted return on equity. The risk of real estate investments (in contrast to their return) always increases through leverage anyway.

As far as we know, there are no independent academic studies on the historically realized returns on equity of small landlords in Germany - with one exception: a study by the German Institute for Economic Research (DIW) from 2014 for the period from 2002 to 2012. With regard to the equity returns achieved by landlord households, this analysis comes to sobering results for small landlords. We have them here summarized in a previous blog post on rental property returns (link to original study here).

For homeowners in Germany, leverage has reduced returns in most long-term time frames over the 54 years since 1970. [5] This is based on figures in Kommer's book Buy or rent presented and more condensed in a blog post (here). Similar results were also found in other countries such as Australia, the United Kingdom, the United States and the Netherlands. Historically, the combination of rents and passive buy-and-hold capital market investments in Germany led to higher final wealth in the majority of cases. And the financial disadvantage of buying compared to renting + capital market investment tended to be greater the more borrowed capital the buyer used to finance his home.

A previous blog post of ours entitled “Leverage stock investments with credit – does it work?” (see here) contains a list of scientific analyzes that show that leverage in companies generally - not specifically in real estate companies - has a statistically negative impact on shareholder returns or company operating returns.

So if there is no hard numerical evidence that leverage has a reasonably reliably positive effect on the returns on equity of real estate investors and companies outside the real estate sector, why are brokers, real estate finfluencers, real estate coaches and the many authors of “get rich with real estate books” the majority of ardent advocates of credit leverage?

The answer to this question should not surprise anyone: The real estate service providers mentioned benefit from the highest possible number of small landlords and owner-occupiers in their business who believe that (a) you can get rich quickly with real estate, (b) that you can do this with little equity and (c) that the additional risk associated with borrowing is not too high.

How does the real estate industry convince private households of the attractiveness of “get rich by buying real estate on credit”, even though there is obviously no hard statistical evidence of success for this? This can be done by real estate service providers using one or more of the following six marketing tricks in their marketing. All six have the direct or indirect purpose of using credit leverage as a “magic tool”, [6] as a species Free Lunch when investing in real estate with little or no equity.

Marketing trick 1: Calculate the credit leverage effect

Almost inevitably, a calculation example similar to the following is presented in publications by those who earn directly or indirectly from the sale of loan-financed real estate. These calculations, which are “funny” from a technical perspective, could be titled “Getting Rich on an Excel Sheet”.

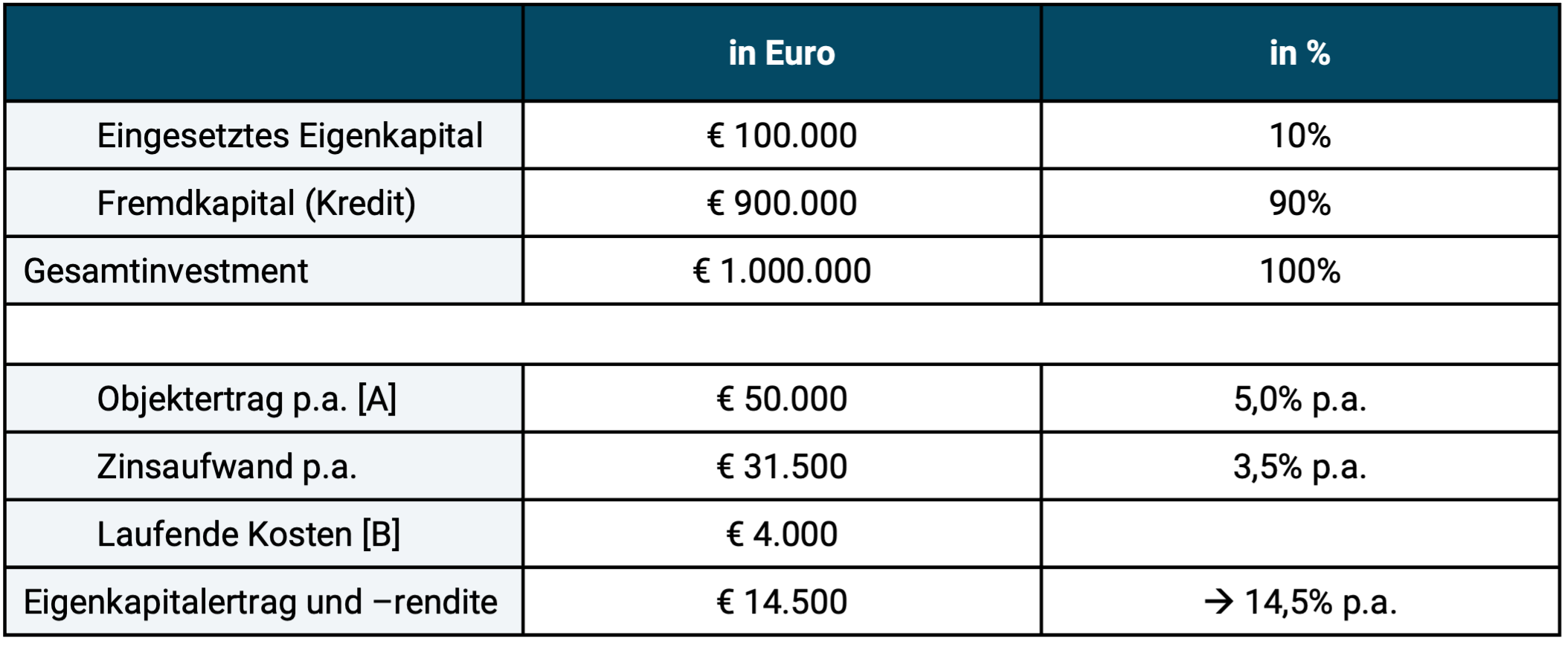

Figure 1: Weird example calculation of the credit leverage effect on a real estate investment in “Year 1”

► [A] “Property income” is defined here as gross rent plus increase in value. ► [B] Maintenance, insurance, property tax. 4,000 euros is at the upper end of what the real estate industry would typically state as a percentage, but is still clearly too low. ► The calculated percentage equity return is 14,500 ÷ 100,000 = 14.5%.

Extended calculation examples of the credit leverage effect such as the one in Figure 1 are intended to show that even with relatively low returns from residential real estate investments (net rents and increases in value [7]) attractive double-digit returns on equity result. [8]

You don't have to take such coaster calculations on the leverage effect seriously - not even if you accept that they are intended "for illustration purposes only". They are not to be taken seriously because they are deliberately created from a purely “accounting” perspective, which is ultimately incomplete. If they were complete, they would first of all have to be on one Cash flow basis or “internal rate of return basis”. However, this includes the cash outflow for loan repayment. With small landlords, repayment can never be avoided in the long term - even less so with owner-occupiers. [9] If one were to simplify the example in Figure 1 and take into account a linear loan repayment over 25 years (4% per year = 36,000 euros), the return on equity for the period under consideration would no longer be plus 14.5%, but minus 21.5% (loss of 21,500 euros), since interest expenses and repayment together add up to 67,500 euros.

However, omitting repayment does not mean that the credit leverage wizards' bag of tricks has been exhausted.

In other fables about the "magic of leverage" or about "paying for the property with other people's money and then watching it pay off through the rental income" the loan repayment is included, but in return one or more of the following "tricks" is used: The setting of (a) unrealistically high rental yields (the ratio of rents to acquisition costs or market value), (b) unrealistically low maintenance and management costs (in this blog post more on the assessment of the level of realistic maintenance costs for real estate) or (c) it is simply ignored that with such a “self-paying investment” it takes 20+ years until the cash flow for the investor turns significantly into positive territory because only then does the repayment element no longer apply. In other words, 20 long years to achieve “passive income”.

With the exception of interest rates, the inputs for such calculations are rarely from objective statistics and databases and one conservative Interpretation of the real market conditions derived. They are typically optimistic best-case assumptions for advertising purposes.

Marketing trick 2: Tell the old story of rags to (real estate) millionaire

Many real estate agents and almost every real estate finfluencer or real estate coach have them in their marketing repertoire because they are well received by the public: “Exciting stories” about individual investors who have become “financially independent,” “financially free” or “rich” by purchasing real estate with aggressive leverage – i.e. little equity or even no equity at all – and now live on their “passive income”. In order to make these “rags to real estate millionaire” stories credible, they often contain specific names and often even photos of “successful” real estate investors “who made it at a young age”. It is not uncommon for the narrator himself to be the subject of such a “success story” à la “how I got rich with real estate – and you can do it too!” Because of their specificity (names, photos), the stories seem credible to many recipients.

The unfortunate thing is that this anecdotal evidence can never be verified by outsiders. The majority of these descriptions are likely to be manipulated and some are completely made up.

In addition, the assets of the “successful” real estate investors stated in the stories are almost always properly inflated. In the “personal success story” the property value or the number of properties of the investor is mentioned: “Sebastian already owns nine properties at the age of 29” or “Lisa has a real estate portfolio worth seven million euros after five years”. There is always no information about the debts. [10] This is important because in every other industry outside of real estate and in life in general, “assets”, “wealth” or “net worth” are always referred to as Netassets are stated and understood, i.e. as gross assets minus debts. The general 2,000-year-old rule that “wealth” is the value of all of a person’s (or company’s) assets minus their debts (i.e. equity) applies everywhere except in the real estate industry.

Marketing Trick 3: Repeating the “Inflation will devalue your loan debt” myth

The spread of this “theory” is particularly useful for those who have little capital but want to finally become “rich” because it simply sounds too tempting: “Accrue debt that you only have to pay back in part!” And because this “theory” sounds smart and logical when quickly explained by the “financial experts”, it is believed by probably 90% of those who hear it.

The voodoo logic goes like this: Credit borrowers receive a financial advantage through inflation because their income (e.g. rents collected or their own salary) increases in the long term with inflation, while the amount of their debts and (in the case of fixed interest rates) the interest element are fixed. Both should therefore become less and less or “devalued” over time, adjusted for inflation (in real terms). This makes debts easier to service and pay off from year to year. But this apparently plausible thinking is only half the truth, and in this case the half truth is a complete lie.

The missing half of the economic reality in such fantasy stories: Due to inflation, nominal interest rates are higher than they would be without inflation. Inflation only devalues what the market inflation expectations previously added to the debt service (interest + repayment). We have explained what these economic connections look like in detail in a separate blog post (here). For reasons of space, we will therefore not specifically refute the inflation-devaluation-debt fiction in detail here.

Marketing trick 4: Hide hard figures on the German real estate market

In no other country for which long-term data on increases in the value of residential property are available have these been as low as in Germany since 1970. The increase in the value of residential real estate in this country, adjusted for inflation, averaged 0.1% p.a. from 1970 to 2023 (54 years). The average German residential property was worth a paltry 7% more in real terms at the end of 2023 than 54 years earlier at the beginning of 1970. Even in Japan, residential property prices rose faster. We have this fact, well known among experts here (blog post) and here (YouTube video) documented.

Yes, in the time window from 2010 to 2021 (12 years), the increases in the value of residential properties in Germany were very high. They were that because they were particularly low in the previous 40 years from 1970 to 2009, namely an average of minus 0.4% p.a. in real terms. Due to this return disaster, residential property prices in Germany were 16% below the 1970 level in real terms at the end of 2009. Because of their exorbitantly low valuation in 2009 compared to international standards and interest rates continuing to fall at the time, German residential property prices began to fall at the beginning of 2010 for twelve years until the end to rise sharply in 2021. Since 2022 they have fallen again and in September 2024, adjusted for inflation, they were 17% lower across Germany for existing properties than in February 2022. Ergo: The twelve years from 2010 to 2021 were a positive outlier against the long-term trend that was not representative of the long-term future.

Of course, increases in value are not the total return of a real estate investment, but if the real increases in value are close to zero in the long term, the statistical chances of high leveraged returns on equity are not good from the start.

Occasionally, in this context, one comes across the truly famous statement from some chronic real estate optimists:the There is no real estate market, every property is an individual case." If that were true, then there would be the stock market, the bond market, the raw materials market or the Not the automotive market. There would then actually be no market, just individual investments. Funny! The fact is that the prices of probably over 80% of all individual properties in a city or region correlate highly with the general price trend in the corresponding area and in the minority of properties for which this was not the case in retrospect, we knew it ex ante usually none.

Marketing trick 5: Present real estate as a particularly safe investment class

We have all heard it countless times in our lives from our grandparents, from real estate agents, real estate influencers, bankers, tax advisors and from our buddy who has just bought a condominium: residential properties are “particularly safe” investments. The Sparkasse Pforzheim Calw (Baden) puts it almost comically and bordering on unintentional satire in a marketing publication that is no longer available: “Real estate, probably the safest investment in the world […] Real estate has been one of the safest, most stable investments in Germany for decades - and it will maintain this status.”

However, the reality shines less than the dusty cliché of “stable concrete gold”. Housing prices can crash - just like stock prices, long-term bonds, high-yield bonds, the price of gold, Bitcoin or a private equity investment. However, a crash in real estate usually (but by no means always) occurs more slowly than in stocks and is therefore often not perceived as a crash.

Some crash examples of the decline or collapse of residential property prices (all figures adjusted for inflation): USA over six years from 2006 to 2011: minus 39%, Ireland over seven years from 2007 to 2013: minus 57%, Netherlands over eight years from 1978 to 1985: minus 51%, Japan over 20 years from 1990 to 2009: minus 49%, Germany over 30 years from 1981 to 2010: minus 31%.

In every country in the world for which data of sufficient quality and length is available, there have been declines in the national real estate market over the past 100 years that exceeded 30% in real terms. In France, real property prices fell cumulatively by 84% from 1911 to 1948. It then took the price level another 15 years to return to the level of 1911. Main cause: economic problems in the context of the First and Second World Wars as well as rent controls introduced in 1911, which were only gradually relaxed around 1948.

All of these numbers (a) exclude the loss-increasing effect of leverage and (b) all of the numbers refer to entire national markets. This means that half of all individual properties in these markets performed even worse, and the possible downside is even more extreme than is reflected in these market averages without leverage and transaction costs.

You rarely or never hear statistical data on past slumps in the residential real estate market from credit leverage advocates.

Compare the real estate industry's silence regarding historic droughts and slumps in the real estate market with the situation with equity investments, bonds, raw materials, gold or cryptocurrencies and the financial products derived from these asset classes. Inflation-adjusted historical long-term data, including drawdowns, crashes and duration of recovery phases, are freely available there and have long since been swept under the table by the industry. The reason they won't do this is because anyone who would do so would rightly be seen as a fool or a rip-off. With regard to the “stock crash of the century” from 1929 onwards, the collapse is even regularly overstated (see here).

Anyone who has ever bought a share or a share ETF anywhere in Germany in the last 20 years will inevitably have to click through or literally wade through risk warnings such as “there are high risks associated with investments in securities, including the risk of total loss” before making the purchase. This is transparency and realism.

Of course, total losses are also possible with credit-leveraged real estate investments, especially in severe market crises and in the case of individual unfortunate transactions even in good market phases. Nevertheless, one hears very little about evidence of such risk of loss in credit-financed transactions in the real estate industry and if there are, then they were “isolated cases” or “special cases”.

Marketing Trick 6: Statistics mean nothing because a smart investor only focuses on the best deals

It is the most widespread and probably the oldest of all real estate marketing tricks. It is mainly used when the previous five did not achieve the goal. The trick is the “brilliant” observation that statistics, empirical data and the usual factual logic do not have to apply “if you specifically select particularly financially attractive deals”. With the superior know-how that the respective advice book author or real estate coach imparts, in combination with the “commitment” and “focus” of the investor, this is of course not a problem. This brings to mind the advice of the American comedian Will Rogers (1879 - 1935) on successful investing in stocks: "Don't gamble. Take all your savings and buy some good stock and hold it until it goes up, then sell it. If it doesn't go up, don't buy it." [11] Further comments are unnecessary.

What are rational, sensible reasons for debt-financed investing in real estate?

Of course, there are rational reasons for using debt capital to finance real estate. These include, for example, these two:

- For property for personal use: Without external financing, a typical household would only be able to purchase a home at the end of their working life or even later. Here, debts serve to bring forward “consumption” over time. Bringing forward a consumption or investment decision has been the essential purpose of debt for 3,000 years, not exploiting the credit leverage effect.

- For small rentals: Debt-financed investing and credit leverage can have a positive effect for an investor (a) if he is 100% clear about the considerable risk of leveraged investments and has analyzed its economic and legal consequences thoroughly and competently, (b) if he knows that with fewer than around six to ten residential units the economic logic works pretty mercilessly against him, (c) if he reduces the level of debt to a more moderate level as the company grows and succeeds, lowered to a lower risk level [12] and (d) if he obtains legal notice at the earliest opportunity Firewall between commercial debts on the one hand and his private assets on the other. This means that he then holds a sufficient amount of wealth in the private sphere. With these private assets, he is no longer liable for investment liabilities. But these private assets that have been brought into the security zone can of course no longer be leveraged.

Conclusion

As we have shown here, the impact of credit leverage is naively and optimistically portrayed by much of the real estate industry.

According to academic studies, leverage appears to statistically worsen rather than improve the absolute return on equity or risk-weighted return for large commercial real estate investors, small landlords and owner-occupiers. Even outside the real estate industry, corporate debt statistically has a negative impact on key business metrics or shareholder returns.

Of course, someone who bought a residential property in Germany between approximately 2005 and 2018 and financed a significant portion of the purchase price with debt will have achieved excellent returns on equity after a holding period of five to ten years or more [13] – provided there was no isolated case of bad luck or inability. However, things looked less positive for purchases well outside this time window.

Against this background, the obsession with leverage in much of the commercial real estate sector, as reflected in Patrick Boyle's quoted statement at the beginning of the undying love between real estate and credit leverage, is highly ambivalent. However, it is clear why it exists: without leverage there would be fewer transactions for real estate service providers and therefore less money. And without accepting high leverage, a naive but important dream for many young people would collapse: “Get rich quickly without equity”.

It is high time that the real estate industry, financial journalists and finfluencers practice more honest, evidence-based communication about credit leverage.

Endnotes

[1] Leverage, Leveraging = credit leverage (effect), debt; Lever = lever.

[2] Social media influencers who specialize in the topic of money and wealth.

[3] Over Realty Tommy - according to their own statements, Europe's largest real estate finfluencer - Spiegel and NDR have published several articles and videos about Immo-Tommy's supposedly unfair business practices since August 2024. At the moment (as of November 2024) it is unclear how the matter will turn out for him.

[4] “Small landlord” is the terminology used by the Federal Statistical Office. This refers to landlords who do not operate the rental business full-time (non-commercially), usually with fewer than six to eight residential units.

[5] “Since 1970” because there is sufficiently good data available from that year onwards. How leverage worked beforehand is more difficult to assess due to a lack of sufficiently granular raw data.

[6] Quote from the book “10x for real estate investors – achieve more, grow faster, increase your portfolio tenfold” by Markus Beforth (2024).

[7] Net rent = gross rent less expenses for (average) maintenance, property tax and insurance.

[8] At the end of this blog post there is an Appendix 2 with a more detailed explanation of the leverage effect. Readers who are not yet well acquainted with the mechanics of debt capital leverage can find out more about this in the appendix.

[9] There is a fundamental difference here to large commercial landlords, where the banks accept that there is a permanently constant level of debt at the company level and that there is therefore no net repayment at the portfolio level. This is one of the many structural advantages of large investors relative to small landlords.

[10] For the sake of completeness, it should be mentioned that the numerical information on objects and object values cannot be checked here either. Why should these unverifiable numbers be true if they are obviously for marketing purposes?

[11] "Don't gamble. Take all your savings and buy a good stock. Hold it until it goes up. Then sell it. If the stock doesn't go up, don't buy it."

[12] If René Benko (Signa-Immobilien) had observed this simple risk management principle, he would not now be bankrupt and socially ostracized.

[13] Because the period mentioned includes all or most of the “golden German real estate era” from 2010 to 2021 as well as the zero interest period from 2016 to 2021.

Appendix 1

Below is a list of specialist articles that show that high leverage in commercial and private real estate investments tends to lower the absolute return on equity or the risk-weighted return on equity.

(a) Commercial real estate investments

Alcock, Jamie et al. (2013): “The Role of Financial Leverage in the Performance of Private Equity Real Estate Funds”; In: Journal of Portfolio Management; 39; No. 5; 2013, internet source here

Case, Brad (2017): “Comparing Listed REITs with Private Equity Real Estate: What the Cambridge Associates Data Have to Say”; Aug 16, 2017; Nareit/National Association of Real Estate Investment Trusts; Internet reference here

Giacomini, Emanuela/David Ling/Andy Naranjo (2016): “REIT Leverage and Return Performance: Keep Your Eye on the Target”; August 17, 2016; SSRN; Internet reference here

Haughwout, Andrew et al. (2011): “Real estate investors, the leverage cycle, and the housing market crisis,” Staff Reports 514, Sept. 2011, Federal Reserve Bank of New York

Pagliari, Joseph (2017): “Another Take on Real Estate’s Role in Mixed-Asset Portfolio Allocations”; In: Real Estate Economics, Volume 45, Issue1, Spring 2017

Green Street Advisors (no author) (2009): “Capital Structure in the REIT Sector”; July 1, 2009; Working Paper; Internet reference here

Sagi, Jacob/Zipei Zhu (2022): “Leverage in Private Equity Real Estate”; March 21, 2022; Working Paper; SSRN; Internet reference here

Thomas, Brad (2012): “REITs With Modest Leverage: Separating The Best From The Rest”; July 02, 2012; Wide Moat Investors; Internet reference here

(b) Private/non-commercial real estate investments

Beracha, Eli/Johnson, Ken (2012): “Lessons from over 30 years of buy versus rent decisions: Is the American dream always wise?” In: Real Estate Economics; 2012; 40; No. 2; Internet reference here

D’Lima, Walter/Schultz, Paul (2021): “Residential Real Estate Investments and Investor Characteristics”; In: The Journal of Real Estate Finance and Economics; 2021; 63; Issue 3; No. 2; Internet reference here

Mian, Atif/Amir Sufi (2010): “House Prices, Home Equity-Based Borrowing, and the U.S. Household Leverage Crisis”; April 2010; SSRN; Internet reference here

Jud, Donald/Daniel Winkler (2005): “Returns to Single-Family Owner-Occupied Housing”; Journal of Real Estate Practice and Education; Vol. 8, No. 1; 2005; Internet reference here

Schweizer, Jonas/Alexander Weis (2022): “Buy or rent? – Home vs. global portfolio”; Gerd Kommer Invest; Dec 2022; Internet reference here

Appendix 2: How the credit leverage effect works

First, a case study of how the leverage effect works:

Antonia invests 100,000 euros in an investment project We now imagine two scenarios. In scenario 1, the value of project

What effect does the two scenarios have on the return on Antonia's equity (EK)?

In scenario 1, Antonia's equity return is 30,000 euros ÷ 60,000 euros = plus 50% (profit from equity), in scenario 2 the equity return is -30,000 euros ÷ 60,000 euros = minus 50%. (We ignore the borrowing costs and any tax effects here for the sake of simplicity. Assumedly, there is no loan repayment.)

Without leverage, equity returns would have been plus 30% and minus 30%. (Where there is no leverage, equity return and return on assets, or “property return” in real estate jargon, are the same.)

We see that leverage symmetrically increases both the opportunity (the upside) and the risk (the downside).

In general, leverage results in increased equity returns for a given period, be it six months or 20 years, when the debt expense (absolute or percentage) is lower than the total investment return (absolute or percentage). The general formula for calculating return on equity is:

Explanation of abbreviations: EKR = return on equity, GKR = return on total capital, FKZ = interest rate on debt capital, FKA = share of debt capital in percent or absolute, EKA = share of equity in percent or absolute.

A numerical example. We use Antonia's investment in scenario 1 and a loan interest rate of 3%: EKR = 30% + (40% ÷ 60%) × (30% - 3%) = 48% (rounded).

With leverage you can also lose more than 100%. A numerical example: Antonia once again invested 100,000 euros in project A using leverage, this time with only 30,000 euros equity and 70,000 euros FK. Now the value of Project A collapses by 40% within a few months. Antonia has now lost her entire equity of 30,000 euros and owes the bank another 10,000 euros. In percentage terms, your loss is –40,000 ÷ 30,000 = –133%

So we have seen that leverage symmetrically increases both upside potential and downside potential.

In an essay in 1958, two American economists, Franco Modigliani and Merton Miller, provided theoretical evidence that corporate leverage does not produce a systematic advantage in terms of risk-weighted return on equity (at least if one ignores possible tax advantages). Modigliani and Merton Miller received the Nobel Prize in Economics in 1985 and 1990, respectively, for this groundbreaking research work (Modigliani, Franco/Merton Miller (1958): “The cost of capital, corporation finance, and the theory of investment”; In: American Economic Review; Vol. 48; 1958).