<<< This blog post is also available as a YouTube video. >>>

From Jonas Schweizer and Gerd Kommer

A third of the liquid assets of German households are contained in capital-forming life insurance policies (KLVs) - a financial product that is primarily intended for long-term wealth creation and retirement provision. Statistically speaking, each of the more than 40 million households in this country holds more than two KLV policies.

From this “KLV density”, which is probably unique in the world, one could deduce at first glance that the KLV is an important and successful investment product for Germans. Given this magnitude, it is certainly essential; successful too – for the insurers. The success of KLVs for the insured, on the other hand, is likely to be rather modest. This blog post tries to show how modest, why modest and what consequences can be derived from it. [1]

KLVs exist in a “classic” and a fund-linked form. In the classic variant, the policyholder's contributions are invested primarily in long-term bonds from the upper credit segment (primarily government bonds); in the case of unit-linked life insurance, they are almost always invested in expensive, actively managed equity or mixed funds.

The underlying investment in bonds or investment funds (which in turn invest in stocks or bonds) is wrapped in a thick, legally complex “packaging”, the “insurance shell”. It costs a lot of money, introduces a significant additional risk (the counterparty risk or credit risk of the life insurance company), makes an otherwise quite banal capital market investment opaque and – as we will see – does not bring a single real advantage. More on the important counterparty risk below.

From the user's perspective, KLVs can be described as a veritable faulty design. Incorrect construction because, when viewed rationally, a KLV is an economically rather nonsensical coupling of an insurance product with an investment product, namely a term life insurance interlinked with a savings contract. Term life insurance represents death protection - which is generally only necessary for a limited period of time. The savings contract, on the other hand, is an investment product for very long-term wealth creation and retirement provision. Ultimately, these two functions and goals have as much to do with each other as a life jacket and a bicycle. Nevertheless, insurance companies combine them because high costs and margins can be particularly easily hidden in this opaque, illiquid, unnecessarily complex combination.

Anyone who needs death protection can get it tailor-made as pure term life insurance at a fraction of the monthly KLV premium. Later, he can cancel this inexpensive risk insurance immediately as soon as he no longer needs it, e.g. E.g. “when the children are out of the house”. The counterparty risk is not significant with term life insurance.

The savings and investment aspect of a KLV can be achieved better and more reliably using a fund savings contract with significantly lower costs (and therefore higher final assets) as well as more transparency, flexibility and higher liquidity. The same applies to a KLV with a high initial one-off payment, instead of long-term ongoing savings.

KLV policies that were taken out by the end of 2004 (these are almost exclusively “classic” KLVs) had and still have attractive tax advantages. However, these tax advantages gradually disappeared for later policies from 2005 onwards and are now small. This “residual tax advantage” almost never justifies the three structural disadvantages of KLVs. These are: (a) unattractive returns due to the high built-in costs that are difficult for policyholders to fully understand, (b) the counterparty risk (credit risk) of the insurance company and (c) their illiquidity, inflexibility and lack of transparency.

A perfidious legal regulation contributes to the unacceptably low return on average for KLVs, which allows insurance companies to deduct certain ongoing costs of the insurance company, which - and here it comes - will only be incurred for decades in the future, in the first five years or so, i.e. in advance, from the premiums paid by the policyholder. Due to this absurd, customer-hostile method, which does not exist in any other industry, the surrender value (present value) of KLVs in the first few years is usually well below the sum of the premiums paid. This approach, known as “Zillmerung”, has a bad effect on consumers in practice because – depending on the calculation method – over 50% of all KLV contracts are terminated prematurely (Bund der Insured 2019). The shockingly high cancellation rates are a result of commission-driven brokerage in the insurance business and the general deficiencies of the KLV product.

In this context, it can also be mentioned that the approximately 200,000 insurance agents and brokers in Germany are allowed to broker and sell an investment product with KLVs, even though they have no formal qualifications as investment professionals. From a consumer protection perspective, this can be seen as a deficit. As is so often the case with financial services in this country, this is due to regulatory failure on the part of the legislature.

Paradoxically, the insurance industry likes to point out that the above-mentioned trio of characteristics “illiquidity-inflexibility-non-transparency” actually works to the policyholder’s advantage, because the KLV is straight because of this a “positive compulsory savings contract”. This is precisely why it is not dissolved by the policyholder at the “first personal liquidity bottleneck” or in the event of a stock crash, as is often the case with a direct investment.

This argument has more holes in it than Swiss cheese. The cancellation rates mentioned prove that the “theory” of the positive compulsory savings contract simply does not apply to KLVs.

The biggest and strangely often overlooked disadvantage of a KLV is the credit risk borne by the policyholder in relation to the insurance company. If the latter gets into economic difficulties, it is quite possible that the policyholder will suffer drastic financial losses, e.g. B. a significant reduction in his payment entitlement. The money that the policyholders pay into a KLV does not form any Special assets in the sense that is the case with mutual funds, including ETFs.

The term “special fund” does appear in Section 223 of the Insurance Supervision Act (VAG), which is relevant here, but it has a completely different meaning than what is commonly understood by private investors Special assets is understood in relation to investment funds, namely that the assets of the investors in the fund are strictly and effectively separated from the assets of the investment company managing the fund. If it goes bankrupt, it will have no impact on the investors' assets. [2] Even the conceivable bankruptcy of the investor's custodian bank does not play a role in this regard for fund investments, since the custodian bank - which is quite different from a normal account (cash account) - only acts as a custodian of the investor's assets.

In the case of KLVs, Section 314 VAG, which is relevant here, contains the term “security assets” (not “special assets”). According to Section 314, an individual policyholder - unlike an investor in an investment fund - has just none comparable segregation claim for the assets (primarily securities) that were acquired with his money over time should the managing insurance company become insolvent. On the contrary: According to Section 314, the supervisory authority (BaFin) can and will reduce and even completely prohibit payment payments - including the so-called "guaranteed interest" - to individual or all insured persons if the insurance company would otherwise no longer be able to fulfill all of its business payment obligations, i.e. in order to restructure the entire company. This applies both to traditional KLVs and to fund-linked KLVs (Scientific Service 2019). There can be no question of a strict separation of the assets of the insurance company and the assets of the policyholders (i.e. the deposits and the returns generated from them). [3]

The disadvantage of the counterparty risk in relation to the insurance company is particularly significant because a KLV contract typically runs for more than a decade and because the German life insurance industry is already struggling with structural problems that could drive some insurers into serious solvency problems in the next few years. Knowing today that a particular KLV provider has good creditworthiness (as measured, for example, by the credit rating) is largely useless information because it says little about the condition of this company in 12 or 20 years. In our opinion, the disadvantage of the credit risk or the lack of special asset protection alone is so significant that we would never take out a KLV.

The private security scheme of the German life insurance companies called Protector Unfortunately (“Protektor Lebensversicherungs-AG”) doesn’t help here either. Even the bankruptcy of a single large life insurance company would probably exceed Protektor's financial resources. In the event of a systemic crisis that affects several insurance companies at the same time, the protective effect of Protektor would definitely be too low. Such a systemic crisis is particularly possible for German life insurance companies in the future, because the entire industry has been suffering from structural problems for a long time, including declining new business, falling profitability and a “balance sheet asset-liability mismatch”, i.e. insufficient returns from investments that, in the long term, are below the payout obligations to the insured. These structural problems are likely to worsen in the future. One of the largest life insurers on the German market, “Generali”, has already thrown in the towel and transferred a significant part of its KLV portfolio to a liquidation company because a normal sale was no longer possible.

To clear up any misunderstandings: State deposit insurance, as it applies within the EU for bank balances of up to 100,000 euros per bank-customer combination, does not exist for German KLVs.

Given this long list of disadvantages and problems, the question arises as to why there is no other country on this planet with as many KLV policies per capita as Germany. The two answers to this question are: (a) tax advantages (which, as mentioned, are hardly significant for new policies). These tax advantages granted by the state were a gigantic lobbying success for the powerful insurance industry in the post-war period and (b) the curious “craze” of the Germans to have to insure everything all over the place, sometimes even twice. It is no coincidence that the largest insurance company in the world is a German company.

So much for the product KLV, its incurable birth defects and the reasons for its widespread use, despite the obvious defects. Now to practice.

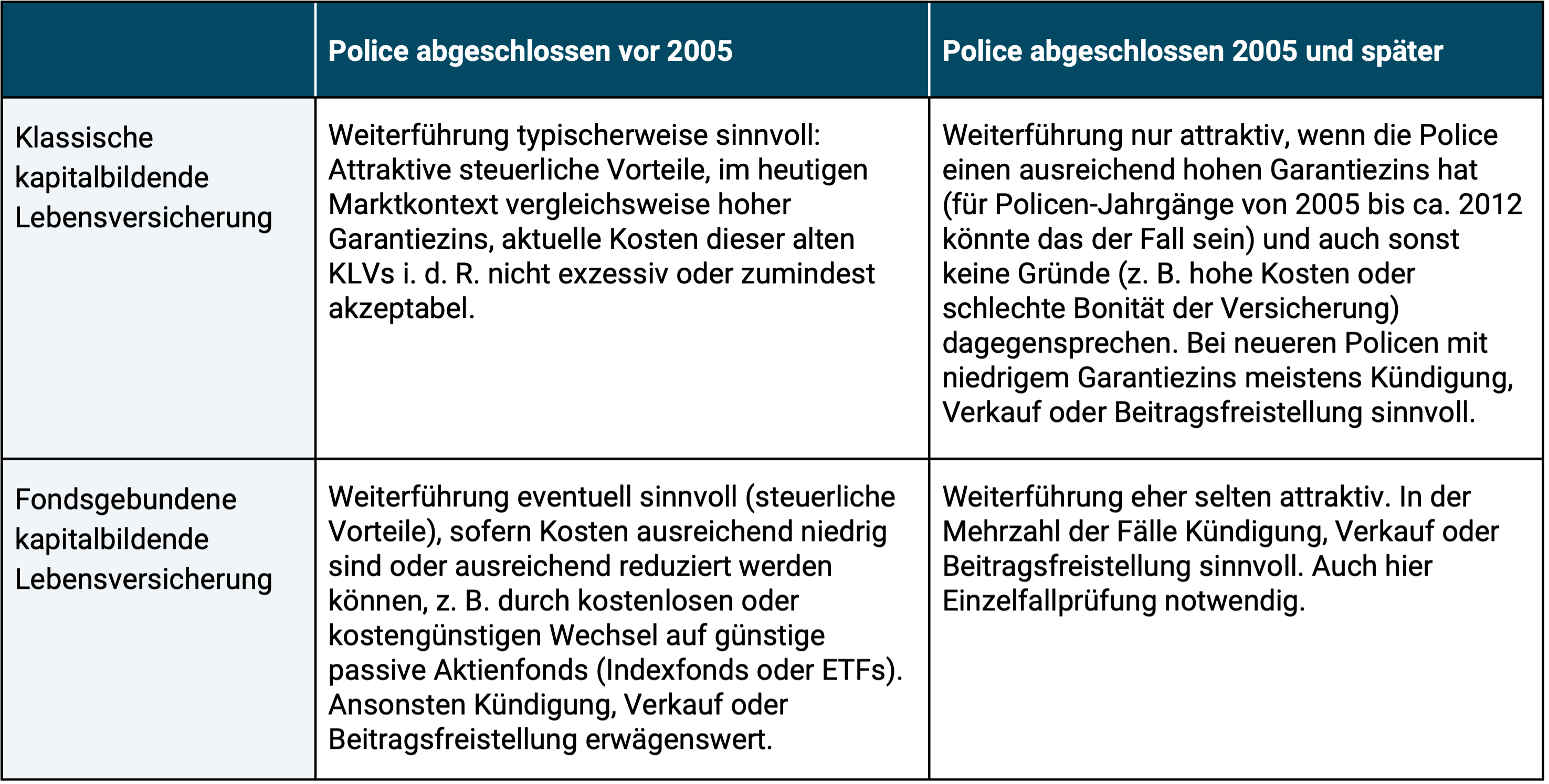

With an existing KLV, there are usually four options for action for the policyholder: unchanged continuation and savings, exemption from contributions, termination or sale on the secondary market. By the way, selling is often more lucrative than canceling.

Which of these options is best in a specific case must ultimately be examined on a case-by-case basis, but some rules of thumb can be formulated in general. This is done in the following table.

Table: Rules of thumb for action-oriented assessment of existing capital-forming life insurance policies

If you have one or more KLVs with non-negligible repurchase values and are unsure about how to proceed, you should contact a consumer advice center Association of Insured Persons or a specialist insurance fee advisor (whom you pay in cash, not through a hidden or indirect product commission).

It is actually always not advisable to take out a new KLV. The only exception we can imagine are fund-linked KLVs on a “net tariff basis” and only if the fund investment is low-cost ETFs/index funds. With a net policy, no or only small commissions initially and continuously flow to the policy broker, as is unfortunately the case with normal policies (“gross policies”). With a net policy, the agent is paid directly in cash by the policyholder - as it should be if you want to minimize the likelihood of bad advice due to conflicts of interest.

On a related topic, private Pension insurance (Annuities) we will publish a separate blog post in the next few months. Kommer discussed the topic of life annuities in May 2019 here Linked lecture already covered in parts.

Conclusion

Capital-forming life insurance is a structurally flawed joint product consisting of an insurance component (term life insurance) and a long-term savings contract on bonds or stocks. Both should be purchased separately. Classic KLV policies that were taken out before 2005 still have significant tax advantages, which, in conjunction with - for historical reasons - high guaranteed interest rates, predominantly suggest that such KLVs should be continued (further savings) - while accepting the associated counterparty risk. In all other constellations described here, it is quite possible that an exemption from contributions, a termination or a sale would be economically more advantageous. In individual cases, only a consumer advice center or a specialized fee-based advisor will be able to help with the specific decision without conflicts of interest. New KLVs only make sense, if at all, as net policies based on ETFs.

Endnotes

[1] The following statements do not apply or only apply to a limited extent to Austria and Switzerland with regard to tax and regulatory statements.

[2] For funds domiciled in Germany, this matter is primarily regulated in Sections 92 ff. KAGB/Capital Investment Code or, for foreign funds, in similar provisions of other EU countries.

[3] In relation to unit-linked KLVs, the insurance industry has commissioned various legal opinions on this matter in recent years, the results of which are intended to prove that - despite the wording of Section 314 VAG - there should be an individual right to exclusion. This seems to indicate that the legal situation is unclear. To date, there has been no real precedent that could serve as a test. All in all, this ambiguity should be enough as an argument: In principle, one cannot safely assume that legally secure special asset protection exists for fund-linked KLVs. With classic KLVs, this non-existence is undisputed anyway.

literature

Association of Insured Persons (without author) (2019): “Most life contracts are canceled”; Internet reference: https://www.procontra-online.de/unkategoriert/artikel/bdv-die-meisten-leben-vertraege- Werden-gekuendigt

Research Service of the German Bundestag (without author) (2019): “Individual question on the Insurance Supervision Act”; Internet reference: https://www.bundestag.de/resource/blob/581272/4f44e5da0d2c2607a8ac4a155f32b56a/WD-4-169-18-pdf-data.pdf