<<< This blog post is also available as a YouTube video. >>>

From Gerd Kommer and Alexander Weis

This blog post is the first part of our trilogy on factor investing (Smart Beta Investing). We recommend that interested readers read the articles published in June 2019 and May 2020 “Integrated multifactor investing" and "The Pains of Factor Investing“ .

Note: The data basis in this blog post was expanded to include the years 2019 and 2020 in November 2021.

“Passive investing” – i.e. very broad diversification with market-neutral index funds on a buy-and-hold basis – is probably one of the world’s biggest success stories in capital market investing in the past 50 years. But no matter how impressive an innovation is, there will always be someone who, even in the face of its great success, asks more questions and digs deeper. This has also been the case with “passive investing” with market-neutral index funds over the past twenty years. (In the specialist literature, the term “market neutral” is used differently than in this blog post and usually refers to long-short strategies that aim to eliminate overall market risk.) In recent decades, the research results of a few hundred financial economists have led to a variant of the passive investing approach, namely “factor investing”, often also “smart beta investing”.

What are “factors” or “factor premiums”? Factor premiums are statistically identifiable drivers of return and risk in an asset class such as E.g. stocks, bonds or real estate. They explain a large part of the risk-return combination within the asset class. Statistically, over 90% of the return and risk of a securities portfolio can only be explained if the “factor exposure” in this portfolio is identified and measured - i.e. how strongly a portfolio is exposed to these factor premiums. A comparison: The number of hours that students study for a math exam statistically explains a significant portion of the deviation in student grades from the class average. In this example, “number of hours” is the factor. Other factors such as B. a student's IQ explains other parts of the statistical deviation from the average.

In this first part of our blog trilogy on factor investing in the equity asset class, we will first focus on the basics. In the second part, which will appear next month, we will describe the smartest way to add factor premiums to your portfolio and what you need to keep in mind.

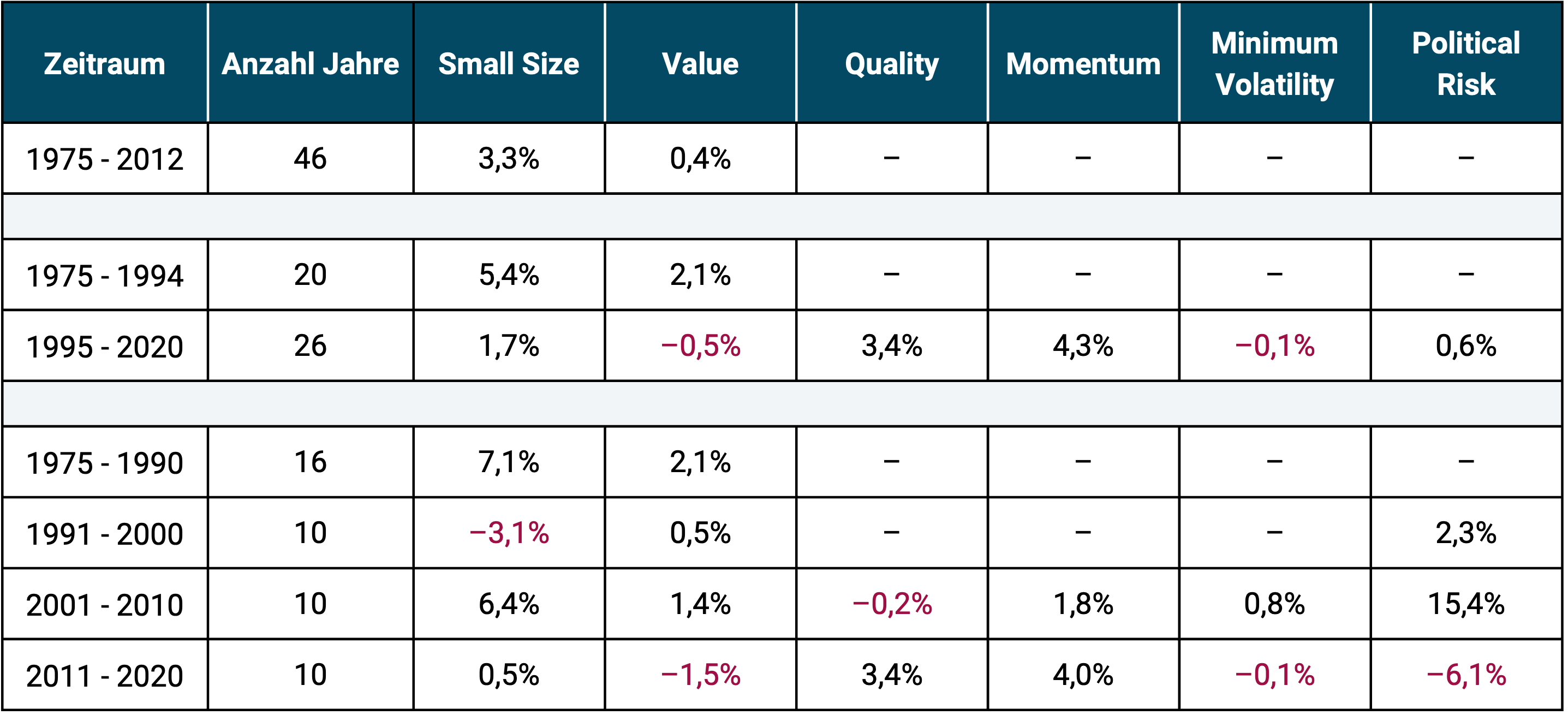

The best-known factor premium for stocks is the “small size premium,” often just called the “size premium” or “small cap premium.” It states, actually quite banally, that small listed companies (small, measured in terms of their market capitalization) produce higher stock returns on average than large companies or the overall market (see table below for the period 1975 to 2020).

Through purely mechanical, disciplined Overweight Factor premiums in a portfolio make it possible to generate additional returns after costs and taxes compared to the overall market; hence the term “premium”. In relation to small caps, “overweight” would mean increasing their percentage share in the portfolio beyond the share that small caps have in a market-neutral “total market portfolio” (the share of small caps is around 15% of the total market capitalization of the world stock market). “Overweighting” sounds more complicated than it is, because such overweighting can be achieved quite easily by purchasing a small-cap ETF.

Exposure to the small cap premium is therefore not for those who have small caps to the “normal extent” in their portfolio, but only for those who have small caps in them stronger dimensions in the portfolio than is already the case in the underlying asset class universe.

Factor investing is essentially passive investing, i.e. the avoidance of active “stock picking” (targeted selection of individual stocks; more generally “asset picking”) or active “market timing” (tactical “in-out” related to entire market segments).

Factor investing differs from traditional passive investing in one important way. With factor investing, the individual securities in the portfolio are not weighted purely according to their market capitalization, but this weighting principle is softened, e.g. B. by overweighting small cap stocks.

We list the most well-known premiums and, in our opinion, the best established ones in the scientific literature:

- Small Size: Small stock companies (“small caps”) tend to have higher returns than large ones (“large caps”).

- Value: Cheaply valued companies (“value stocks”) – measured by key figures such as the price-earnings ratio – tend to have higher returns than highly valued ones (“growth stocks”).

- Quality or profitability: Companies of high “quality” – measured by profitability indicators such as the profit-to-book value ratio or debt ratios – tend to have higher returns than companies of low quality.

- Momentum: Companies that have had relatively high returns recently tend to have higher returns for a limited period of time and vice versa.

- Political Risk: Stocks that are exposed to high political risk (primarily emerging market stocks) tend to have higher returns than stocks that are less so.

- Low Investment or Asset Growth: Stocks with relatively low growth in total assets tend to have higher returns for a limited period of time than those with high growth in total assets.

The following table shows the historical excess return of factor indices compared to the respective market-neutral benchmark. This version of quantifying factor premiums is particularly conservative and is called “long-only factor premiums”. We will explain what this is all about below.

Table: Overview of the magnitudes of several factor premiums per year (p.a.) from 1975 to 2020 (46 years) and sub-periods in these 46 years for the global market (“long-only premiums”)

Source: MSCI, Dimensional Fund Advisors, Deutsche Bundesbank. The longest data series available are shown (longer data series exist for individual countries). ► The factor premiums are “long-only factor premiums” (see explanations below) based on arithmetic averages. ► All data before costs and taxes. ► Historical returns provide no guarantee that they will be repeated to a similar extent in the future. ► Scientific studies on historical factor premiums come to slightly different results with regard to their amount, depending on the country or region, time period and specific research methodology.

The attentive reader will immediately notice that many factor premiums were not positive in every single period. It is therefore quite possible, even probable and necessary, that a given factor premium will be negative over several years or decades, since factor premiums are statistically expected premiums. In this context, expected means that although a positive premium can be assumed over a sufficiently long period of time, it fluctuates greatly in the short and medium term. If the premium didn't fluctuate unpredictably in the short and medium term, it would have been "arbitrated away" long ago, i.e. disappeared, because if there was a high degree of stability, everyone would only buy these shares. The premiums must therefore be unreliable in the short and medium term.

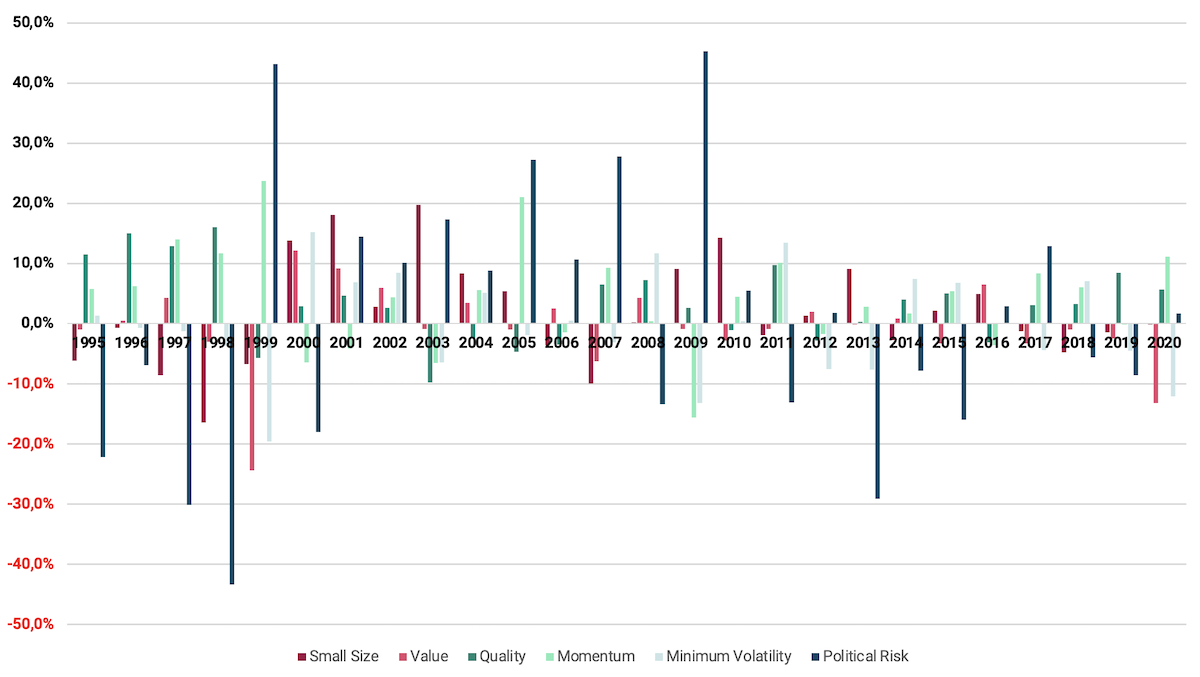

The following figure graphically illustrates this potential for fluctuation. The graphic shows the annual realizations of the five factor premiums mentioned above in the period from 1995 to 2020. The vertical axis represents the percentage of premiums in a given year, while the horizontal axis represents the passage of time.

Figure: Annual development of long-only factor premiums from 1995 to 2020

Source: Own calculations based on raw data from Dimensional Fund Advisors and MSCI.

A closer look at the bars makes it clear once again that individual factor premiums can underperform their benchmark for years (negative bars). The same also applies to the so-called Equity premium, i.e. the excess return of the stock market compared to the “risk-free” money market (the “savings book return”). The equity premium can also be zero or negative for ten years or more. This is shown by data from the last 120 years for a large number of countries, including Germany and the USA. In order to mitigate the “unreliability” of factor premiums, it is therefore advisable to diversify across several premiums, i.e. not to put all your eggs in one basket.

A word about the “long-only” term mentioned above: factor premiums can be calculated either as long-only or as long-short premiums. Long-short factor premiums involve overweighting stocks with a high level of the desired characteristic (such as small size) and shorting stocks with a high level of the opposite characteristic (in this case, large size). [1]. Long-only factor premiums refer only to the “long side” (buy side) of the factor premiums; They are not assumed to be short selling. Long-short factor premiums are accordingly higher than long-only premiums. Since UCITS funds (“mutual funds”) – and therefore all ETFs sold in Germany – are not normally allowed to engage in short selling, we concentrate on long-only factor premiums.

If you want to understand factor premiums, the following facts, among others, are important:

- Different factor premiums are not “additive.” Since different factor premiums influence each other, the returns of multiple factor premiums cannot simply be added up. These interactions not only vary from reward to reward, but can be both positive and negative. This means that different factor premiums can reinforce each other, but can also weaken each other. Since two given premiums usually have a correlation [2] of less than one, risk-reducing diversification benefits can be realized by including several factor premiums in the portfolio, which is therefore not viewed as a disadvantage but rather can be welcomed as a desirable side effect of “harvesting” multiple factor premiums. But more on that in the second part of our factor investing series.

- A further implication of the volatility of factor premiums is that you should stick to the course you have chosen even if the selected premiums are negative over a longer period of time. As expected, these will turn positive again at some point. In the long-term average, they are positive in all cases by definition (and also in the historical data).

- Taking advantage of factor premiums costs money compared to market-neutral investing. However, the additional costs are more than offset by the gross premiums (premium before costs).

- Factor premiums do not refute the well-known Efficient Market Hypothesis (EMH for short), at least in its basic form, as is repeatedly claimed in the media or on the Internet. The “father of EMH”, Eugene Fama, is also probably the most deserving researcher when it comes to factor premiums. The EMH only says that you cannot systematically beat the “market” (asset class return) based on cost and risk using publicly available information. This thesis can be very well supported by empirical data from the past 50 years and is compatible with the existence of factor premiums.

- Is factor investing still “passive investing”? In our view, this question is pointless and too “ideological” for us. Real “passive” investing doesn’t exist anyway. Even the most passive investor has to continually make decisions and is therefore “active” in a certain sense. It is obvious to us that the global stock market is not a completely homogeneous stew, but rather consists of a few “risk-reward sub-segments” that are statistically identifiable. Factors define and describe these sub-segments. In general, factor investing is of course more “active” than market-neutral passive investing.

How will factor premiums develop in the future and can we assume that historical experience values – understood correctly – can also be transferred to the future? Of course, this question cannot be answered with 100% certainty - as is almost always the case in social science disciplines. In principle, this also applies to the level of “normal” returns of all asset classes without factor premiums: stocks, interest-bearing investments, real estate, precious metals, raw materials or art. Nowhere can the level of expected absolute or relative returns over the next 20 years or beyond be predicted with complete certainty. Factor premiums are no exception.

If all the factor premiums that have been added to the portfolio fall to zero in the future, the investor's loss (the so-called "opportunity costs") would only consist of the currently approximately 0.3 percentage points higher product costs of "smart beta funds" compared to market-neutral index funds. If one or two of the factor premiums disappear in the future, this would mean a reduction in the excess return, but not an under-return of the factor portfolio. Overall, the expected outperformance from the use of factor premiums more than offsets their additional costs.

In summary: factor premiums are able to explain the risk-return ratio of a stock portfolio to a large extent, to a greater extent than other objective characteristics such as e.g. B. Industry affiliation, dividend yield or subjective characteristics such as quality of management or the relationship of a company to certain macroeconomic developments (interest rates, inflation, economic growth, etc.).

In our opinion, through a certain form of overweighting the key factor premiums, an expected additional return compared to the overall market of one to one and a half percentage points per year after costs can be achieved in the long term (historically, this outperformance was noticeably higher - see the table in this article). In our view, the best documented premiums are Small Size, Value, Quality, Momentum and Political Risk. Individual factor premiums do not “work” reliably in any given year and have a correlation of less than +1, which is why it makes sense to diversify across multiple premiums.

In the second part of this series on factor investing, we will address the question of how best to get multiple factor premiums into your portfolio. In it we will discuss the various options for implementing multifactor investing (see our blog post Integrated multifactor investing).

Are you convinced of factor investing and want a simple and convenient implementation? We have Gerd Kommer's 1 ETF solution: The L&G Gerd Kommer Multifactor Equity UCITS ETF. Find out more >

Endnotes

[1] Short selling: The sale of a security (or asset in general) that the short seller does not yet own at the moment of the sale T0, but has borrowed from a third party for a fee. If the loan period ends a few weeks or months later at time T1, the short seller must return the security to the lender. To do this, the short seller must now buy it on the open market. The short seller hopes that the market price of the security will be lower in T1 than in T0. That would give him a win. He is therefore speculating on falling prices.

[2] Correlation is a measure of the interaction between two random variables and can take values between -1 and +1. A correlation of -1 or +1 means perfect negative or positive correlation, respectively, while a correlation of 0 means there is no or only random interaction. An example of a positive correlation is the number of calories a person consumes and their body weight: a higher number of calories tends to lead to a higher body weight.

literature

Baltussen, Guido; Swinkels, Laurens; Van Vliet, Pim (2019): “Global Factor Premiums”; available at SSRN: https://ssrn.com/abstract=3325720

Berkin, Andrew; Larry Swedroe (2016): "Your Complete Guide to Factor-Based Investing. The Way Smart Money Invests Today"; BAM Alliance Press; 358 pages.

Kommer, Gerd (2018): “Invest confidently with index funds and ETFs. How to win the game against the banks”; 5th ed.; Campus 2018. 410 pages.

Kommer, Gerd; Weis, Alexander (2019): “Integrated Multifactor Investing”; blog post; June 2019; Link: https://www.gerd-kommer-invest.de/integrated-multifactor-investing/

Kommer, Gerd; Weis, Alexander (2020): “The Pains of Factor Investing”; blog post; May 2020; Link: https://www.gerd-kommer-invest.de/pains-of-factor-investing/

Momentum Effect: Dolvin, Steven; Foltice, Bryan (2016): "Where Has the Trend Gone? An Update on Momentum Returns in the U.S. Stock Market"; Internet reference: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2813333.

Political risk effect: Pàstor, Luboš; Veronesi, Pietro (2013): “Political Uncertainty and Risk Premia”; In: Journal of Financial Economics; Volume 110; Issue 3

Profitability/quality effect: Asness, Clifford et al. (2013): “Quality Minus Junk”; Internet reference: https://www.aqr.com/library/working-papers/quality-minus-junk

Small-size effect: Shi, Wenyun; Xu Yexiao (2015): “Size Still Matters!”; Internet reference: http://www.efmaefm.org/0EFMAMEETINGS/EFMA%20ANNUAL%20MEETINGS/2015-Amsterdam/papers/EFMA2015_0198_fullpaper.pdf

Value effect: Zhang, Lu (2005): “The Value Premium”; In: The Journal of Finance; 60; Issue 1