From Gerd Kommer and Jonas Schweizer

One of the “eternal questions” that has plagued private investors since biblical times is how high the risk of direct investments in real estate is. And – related to this – how this risk compares to that of capital market investments, i.e. stocks, interest-bearing investments, derivatives, currencies, raw materials and precious metals.

The question of risk in capital market investments is quite easy to answer. For “stocks and co.” Ultimately, anyone can obtain almost any risk measurement number imaginable for every imaginable historical period and, more generally, also into the future, with little effort. Metrics include, for example, volatility (the intensity of fluctuations in returns), the maximum cumulative loss (“maximum drawdown”) and that Shortfall risk (the probability of falling below a certain minimum return in a certain period). The key figure is also quite well known among financial economists Value at Risk is with that Shortfall risk closely related. Numerous other risk indicators and their characteristics are constantly available and measurable for securities for those who want to take a closer look.

However, when it comes to real estate as an asset class, the issue of objective, modern risk measurement looks different. To put it figuratively and with a wink, the level of development of risk measurement and the availability of data in direct real estate investments is about as far behind the status of securities as the functionality of a Nokia 3310 cell phone from the year 2000 is from that of the current Apple iPhone

For securities, risk measurement is based on market prices, i.e. h. based on continuously updated market prices. You can simply put it this way: There is no risk measurement without market prices. These market prices are determined objectively - in the sense of being unequivocal and binding for every observer - every day through real buy-sell transactions by many hundreds and in some cases even by several hundred thousand market participants. If the share price of the SAP share is 102.50 euros on August 21, 2018 at 12 p.m., everyone - absolutely everyone - knows with 100% certainty what the share costs at that moment and that they can buy or sell at exactly that price at that moment. [1]

One could indeed look at the different “liquidity levels” and their implications for trading the many hundreds of thousands of securities that exist globally ad infinitum but the general conclusion remains unchanged: market prices for capital market investments are redetermined intersubjectively, consensually, continuously, transparently for the market as a whole and beyond doubt between an enormous number of market participants, often with very different levels of information and views about the fundamental value of a security - literally every minute and sometimes even more frequently. Technological progress makes this process even more transparent, even more reliable and even better every year.

None of this applies to direct investments in real estate – both residential and commercial. There is no stock exchange here, nor any over-the-counter trading, as is the case for some less liquid capital market products. For probably 99.9% of all real estate worldwide, no market price is determined through a buy-sell transaction on any given day. Unlike a specific BMW share, Norwegian government bond or a gold bar, every property is unique and typically several years and often decades pass between two transactions (purchase/sale) for such an object. However, this is the only way to determine the objective market price at the time of the trade. This almost permanent lack of confirmed market prices is the reason why a thousand real estate investors have a thousand different opinions on questions about the level of market risk of direct real estate investments.

One might now ask why, given the lack of market price signals, risk measurements are not simply carried out using real estate indices. This method, although widespread in the real estate industry, is misleading. The risk of direct real estate investments cannot be derived from classic real estate indices. There are four reasons why you shouldn't go down this wrong path: Real estate indices

- are based (with very few exceptions) not on market prices, but on expert assessments and other data crutches used as substitutes, such as the information in banks' internal loan applications, because there is a lack of systematically determined market prices in sufficient numbers and frequency; [2]

- Structurally suffer from built-in smoothing tendencies (technical jargon “smoothing bias”) that dampen their upward and downward swings (Geltner 1991);

- do not include transaction costs, which are between 10 and 100 times higher for real estate than for securities;

- are highly diversified and therefore do not represent a single property from the outset, while direct real estate investments are always investments in a single or a few individual properties. [3] An individual object has high “idiosyncratic” (object-specific) risks (e.g. location risk or completion risk); In an index, however, all idiosyncratic risks are diversified away.

At this point one could object: "So what? If there is no solution to the risk measurement and data problem in direct real estate investments, then it simply doesn't exist. Humanity has obviously made real estate investments for the past 5,000 years even without this solution. So why not in the future?"

From our point of view, this resigned, ultimately cynical view would be an intellectual indictment, not least because there is a simple, better solution to determine the market risk of direct real estate investments quite precisely. We describe this solution, which has long been established in research in various variations (example: Lin/Vandell 2007), below.

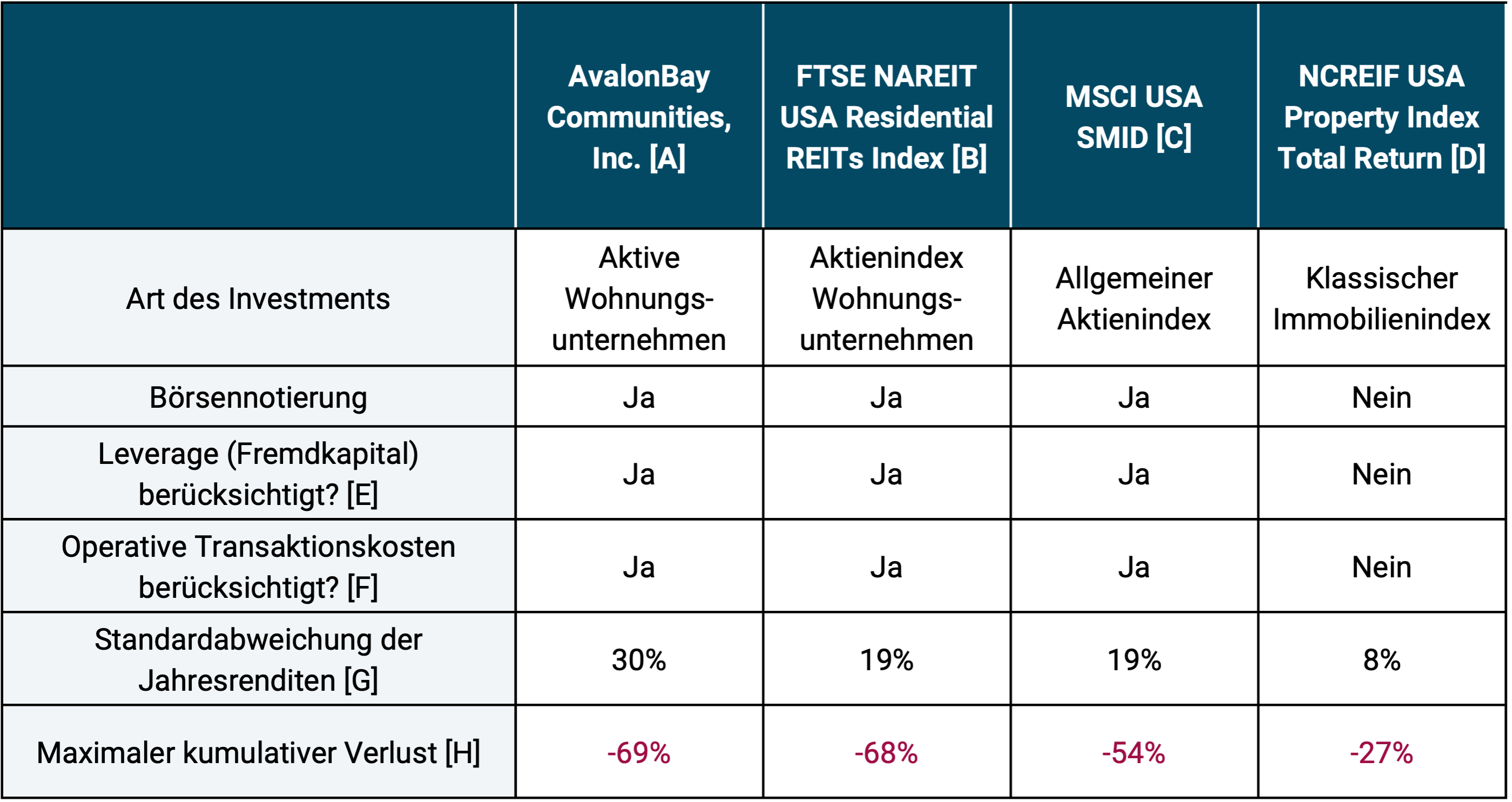

We are looking for a “proxy” in the capital market, i.e. a replacement that comes as close as possible to an unlisted direct real estate investment, but which includes real market valuations of the underlying properties on every trading day and does not rely on expert valuations and other valuation crutches. The aim is to derive the typical, general risk of direct investments in residential real estate from the proxy - just as one derives the general investment risk (market risk) of investments in stocks, corporate bonds, government bonds, gold and raw materials from the analysis of historical capital market returns. The following table makes it clear what is meant by this.

Table: Risk indicators of various listed investments and indices in US residential real estate - period 1995 to 2017 (23 years)

► The 23 years shown are the longest collectively available data period. ► [A] AvalonBay is the largest publicly traded U.S. residential rental company. It owns approximately 77 thousand apartments. ► [B] Real estate stock index that tracks listed real estate companies in the USA that specialize in residential rentals. “REIT” stands for Real Estate Investment Trust, a special legal form of real estate companies. ► [C] General stock index representing small and mid caps in the USA. Small caps and mid caps were chosen because real estate companies are predominantly located in these size classes. ► [D] A “classic” real estate index that is intended to measure the total returns (not just price increases) from direct real estate investments. The property values come from appraisers' valuations (i.e. are not market prices). The index does not include any transaction costs for buying or selling the properties and no debt financing effects. All of these index structure features reduce the reported risk (the fluctuations in value reported in the index). ► [E] Does the property include partial debt financing at the company or index level? Yes No. For real estate companies, the debt capital ratio is on average 25% to 50%, i.e. only slightly higher than the average property financed by private investors. ► [Q] Are the (high) purchase/sale costs for real estate at the company or index level included in the return figures? Yes No. ► [G] Standard deviation of annual returns (volatility): A risk indicator for measuring the intensity of fluctuations in returns. ► [H] The maximum (book) loss that an investor could have suffered during the period under review if he or she had “entered and exited” at the worst possible time. ► Data sources: Yahoo.com, MSCI, NAREIT, NCREIF.

What can be seen from the table? A whole lot.

- Over the 23-year period, an investment in US residential real estate was as risky as or even riskier than a diversified investment in the general US stock market (MSCI USA SMID) - see the bottom two rows of the table. At least that is the opinion of the market, that is, millions of people and thousands of companies who invest their own money.

- If you look at a real estate investment that is based not on market valuations but on individual subjective appraiser assessments - as is the case with the NCREIF Property Index (far right column) - the measured risk miraculously drops to less than half for both risk metrics. A rational investor will not confuse this type of pony farm risk measurement with objective risk.

- In the NCREIF Property Index, four aspects are responsible for the unrealistically low risk reported: (a) Structurally unreliable, conflict-of-interest expert valuations instead of rational stock market valuation of the underlying properties; (b) further smoothing effects in the underlying data (e.g. the use of annual averages rather than year-end values in the underlying property valuations); (c) the lack of (unpractical) consideration of partial loan financing of the properties; and (d) the lack of (also impractical) consideration of the purchase/sale costs for the real estate objects (here referred to as “operational transaction costs”).

- Statistically speaking, a direct investment in one or a few individual properties by a private investor would have to be even riskier than the AvalonBay Communities share or the FTSE NAREIT Residential REITs Index because the latter two are much better diversified than an investment in a single property. With AvalonBay and the NAREIT index there is no idiosyncratic risk (see above) as is the case with individual investments. An analogy: The average individual stock is broadly twice as risky as a globally diversified stock investment, measured e.g. B. volatility and maximum cumulative loss.

The great economist John Maynard Keynes (1883-1946) knew 90 years ago that the situation described here - direct investments in individual properties are not low-risk because the fluctuations in the value of the equity in them cannot be observed every day in the newspaper or on the Internet - is not just gray theory. Keynes is considered the most influential economist of the 20th century. He was a successful private investor himself and managed the endowment fund of Cambridge University in the UK for many years (Walsh 2008). At the time, Keynes mocked the “risk naivety” of the “real estate fans” among his colleagues on the finance committee of the endowment fund. He wrote:

"Some Finance Committee members would, without batting an eyelid, buy unlisted and not immediately marketable properties which, if the members had a price quote for immediate cash sale on each fund audit day, would make their hair stand on end. The fact that one does not know the ongoing fluctuation of such immediate sale quotes does not make these investments safe - as is usually assumed."

Keynes - undoubtedly a super expert - was aware of the widespread confusion between “seeing no risk” and “having no risk” decades ago. Warren Buffett made almost identical comments at the beginning of 2009 regarding the alleged stability of the value of real estate and farmland relative to stocks.

Can the data shown in the table and the insights derived from them also be transferable to Germany? Yes, they are. We only used US data because they go back further than the German ones. If we e.g. B. the share price fluctuations of the housing company Deutsche Wohnen SE [4] use, then the risk is just as great as that of AvalonBay or that of the FTSE NAREIT USA Residential Index.

The Great Financial Crisis began in 2007 in the American residential real estate sector. From there, the crisis spread to the real estate markets of Great Britain, Ireland, Spain, Portugal, Italy, Greece and most Eastern European countries (but not to the German-speaking countries) before spreading to banks and public finances. At that time, the value of the equity of hundreds of millions of homeownership households worldwide collapsed by more than 50% within two or three years. At one point, a quarter of all US households with a home loan had lost 100% of their equity in the property. In France, Holland, Ireland, Spain, Italy, Portugal, Japan and several Eastern European countries, real house prices are still as low as or lower than in 2007.

Direct investments in residential real estate - whether owner-occupied or rented - can be a sensible route to wealth creation and retirement provision for private households and are for many millions of households in Germany and other countries. However, the financial risk of these investments is not low and certainly not low because you cannot see it every day on the Internet or in the newspaper. The equity risk in a credit-financed individual property is at about the same level as that of a globally diversified equity investment and far above the risk of high-quality, interest-bearing investments.

Endnotes

[1] We ignore transaction costs that arise in stock and bond trading and we ignore the short market phases - probably less than 0.1% during a typical twenty-year period - in which the statements just made here only apply to a limited extent for a normal capital market product.

[2] This also applies, for example, to the best-known German real estate index, the Bulwiengesa real estate index. Not only are appraisers' valuations fundamentally an unreliable substitute for market prices, they are also subject to conflicts of interest (the appraiser in real estate funds is paid by the fund management).

[3] Things are different with securities. All investors can easily – e.g. B. with index funds – invest in any diversified segment of the capital market.

[4] As of March 2018, Deutsche Wohnen SE owned around 160,000 apartments, most of them in the greater Berlin area. DW is the second largest listed housing company in Germany and the one whose publicly available price data goes back further than that of the largest (Vonovia SE).

literature

David Geltner (1991): “Smoothing in appraisal-based returns”; In: The Journal of Real Estate Finance and Economics; September 1991, Volume 4, Issue 3, pp 327–345

Justyn Walsh (2008): “Keynes and the Market: How the World’s Greatest Economist Overturned Conventional Wisdom and Made a Fortune on the Stock Market”; Wiley; 2008; 212 pages

Zhenguo Lin / Kerry Vandell (2007): “Illiquidity and Pricing Biases in the Real Estate Market”; In: Real Estate Economics; Volume 35, Issue 3; Fall 2007; pp. 291-330