From Jonas Schweizer and Gerd Kommer

When investors are asked why stocks are riskier than bonds or other interest-bearing investments, the answer often comes: “Because stocks have higher volatility,” meaning their prices or returns fluctuate more. Instead of volatility, other risk indicators are sometimes used in this context, such as: b. maximum drawdown or Value at Risk called. Regardless of the risk indicator chosen, the statement is, strictly speaking, wrong in any case. Volatility and other risk metrics are only an expression of risk, not its cause.

The higher risk of stocks compared to bonds can only be shown and quantified but not explained by their higher volatility or other relevant risk indicators. The explanation of risk requires the description of causality, i.e. h. a logical cause-and-effect relationship. Without the identification of a factual causality, the crucial question of whether historically measured risks or under- or over-returns compared to a sensible benchmark will continue in the same way or in a similar way in the future is difficult or impossible to answer.

So now to what is probably the most important explanation of why stocks are riskier than bonds or interest-bearing investments and why they must therefore have a higher expected return in the future. In the past, they had a higher return in around 90% of all ten-year periods anyway. (It is assumed here that (a) the stocks and corporate bonds relate to the same company; (b) corporate bonds and government bonds have the same duration and currency; (c) the government bonds were issued by the country in which the company has its primary business activities.)

This explanation is based on the concept of the so-called Cash flow cascade. As important as this concept is, it is rarely mentioned in academic financial economics. You won't find it in financial advice books.

The cash flow cascade is a pictorial term for the sequence of legal claims to profits, more precisely the cash flows (payment streams) of a company, which its various “stakeholders” can claim for themselves based on their legal position. Stakeholder can be translated here as “stakeholder group”, for example employees, shareholders, lenders, landlords, suppliers or the state. The term “cash flow waterfall” is sometimes used instead of cascade, but cascade is a more accurate metaphor, as we will soon see.

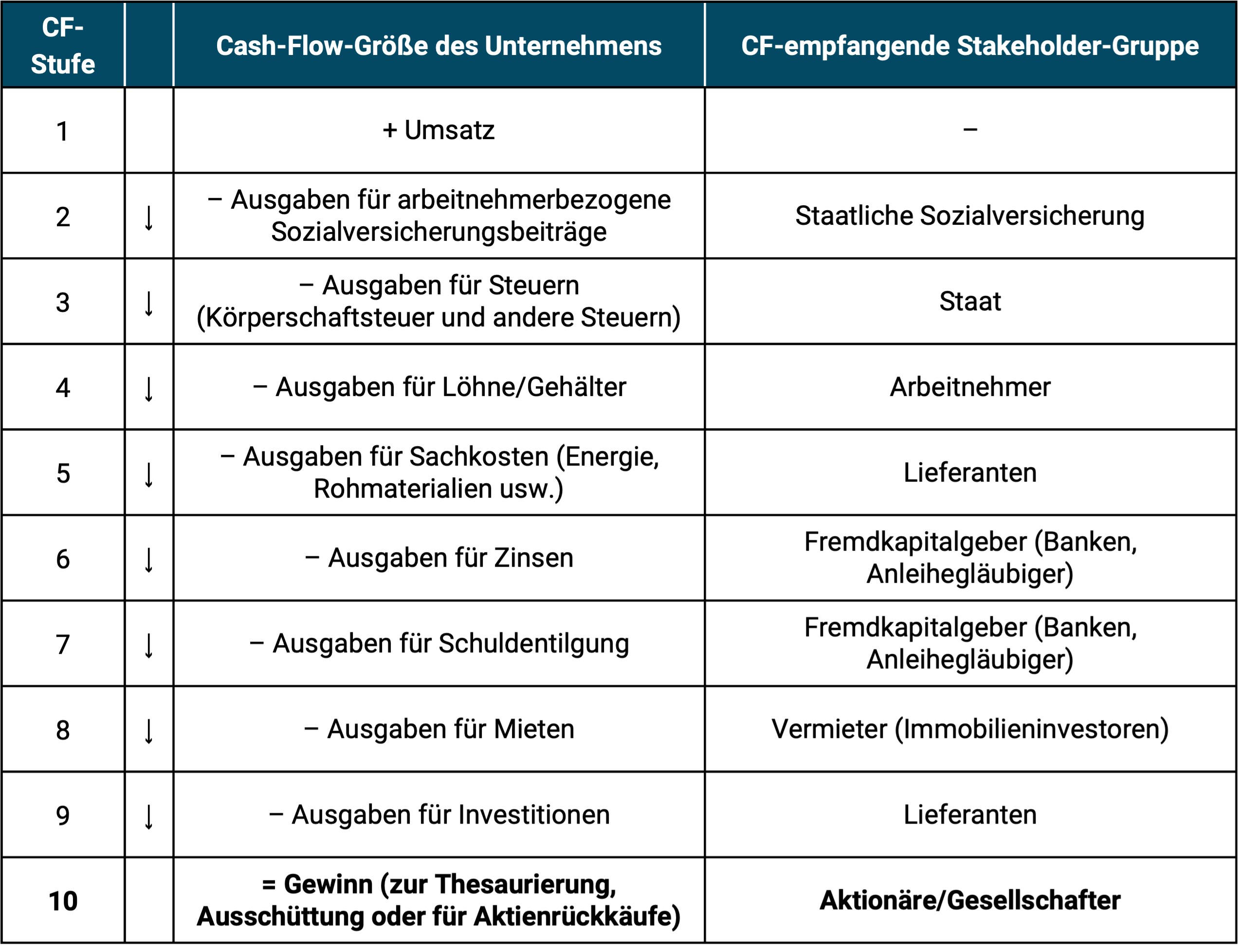

The order of the legal claims (the “ranking” or ranking) that the owners of shares and corporate bonds of an individual company have explains most of the different security or uncertainty of the cash flow claims of the individual stakeholder groups. This uncertainty is expressed, for example, in the volatility of cash flows and ultimately the volatility of stock returns. Insights into why government bonds generally have to be less risky and therefore have lower returns than corporate bonds or bank debt (bank deposits) can also be derived from the cascade concept (see our December 2018 blog post). The following figure illustrates an example of the typical cash flow cascade of a company.

Figure: Simplified cash flow cascade of a typical company

► Source: Own illustration.

At first glance, the illustration is somewhat similar to the traditional structure of a company profit and loss statement (P&L). However, upon closer inspection, there are noticeable differences to a P&L. The operational cash flow cascade is not about reflecting the reporting standards of accounting and bookkeeping or our habitual understanding that often derives from them, but rather about representing legal and economic realities; especially in a scenario where the company cash flow is not enough to generate a significant profit.

The cash flow levels (ranking) largely result from the law of obligations (e.g. loan agreements) in the BGB, corporate law (company law), bankruptcy law, tax law, administrative law and typical contractual arrangements in the general legal transactions relevant here. These legal provisions and principles are likely to be very similar in all market economy countries and have often existed in Western countries since the Renaissance (16th century). A parallel to the cash flow cascade concept exists in mortgage law, where the principle of first-tier, second-tier and third-tier land charges or mortgages in favor of a lender is an essential basis for all real estate financing.

The illustration assumes that there is no pledging or “assignment” of specific parts of the company's assets (assets) to individual creditors (e.g. suppliers or banks). Although such civil law security interests are widespread and in individual cases have an influence on the ranking of an individual creditor, especially in the event of bankruptcy, they do not change the fundamental relevance of the cash flow cascade principle. In general: Payment claims of private creditors (suppliers, banks, landlords) are normally subordinated by law to the claims of social security funds and those of the state (taxes). This often still applies even if individual creditors have civil security interests in certain assets of the company, e.g. B. mortgage liens or account pledges in favor of banks.

Within cash flow levels 4 to 9, the order usually no longer results from the law, but from economic logic. As a rule, a company will or must pay wages, energy and raw materials - even if its liquidity is tight. before to pay for debt servicing, because without these inputs, revenue generation could or would come to a standstill from one day to the next, or at least within a short period of time. This is usually true even if the company is already in receivership. On the other hand, failure to make or delay payment of debt to bondholders, banks or rent payments to landlords often do not lead to the end of production and revenue generation for months, perhaps even years. Ultimately, the respective bank or landlord must first initiate a complex, legally complex and often very time-consuming procedure in order to enforce their payment claims.

Let's look at this with an example. We assume that a company has serious profitability and liquidity problems. This means that its expenses or cash outflows permanently exceed its income (cash inflows). In such a situation, the entrepreneur is not free to decide which stakeholders to pay with their limited funds and which to go temporarily or permanently empty-handed. The order of payment claims of the various stakeholders (order of satisfaction of creditors) is determined primarily by the law and secondarily by contracts and the economic logic just mentioned. The amount of funds available and this order determine the point before which a stakeholder or stakeholder group still receives money and from which subsequent stakeholders no longer see any money.

If the entrepreneur does not adhere to this order, he will probably commit a criminal offense and/or breach of contract - with potentially serious criminal consequences. If the company becomes formally bankrupt and a bankruptcy administrator is appointed within the framework of bankruptcy law, this order of creditor satisfaction now applies to the bankruptcy administrator, who takes the place of the previous managing director.

Anyone who thinks through the concept of the cash flow cascade realizes that debt capital (loans and bonds) is lower risk than equity (stocks and shareholder shares) for the simple reason that it is located higher up in the cash flow cascade.

The constantly observed higher volatility of stock returns and the associated, at times, very poor returns on stocks relative to comparable bonds is not the cause of the higher risk of stocks, but rather its consequence. The real cause of equity risk is the lower position that equities occupy in the cash flow cascade; it produces the many times higher volatility of profits (and therefore equity returns) compared to the capital service (interest and repayment) that goes to bond and loan creditors.

How does this work in detail? Because bonds are higher up in the cascade, the probability that they will actually be “serviced” (the capital service is paid) in a given year is higher than with stocks, which only represent a “residual claim”. Because they are at the bottom of the cash flow cascade, they are only compensated after all other stakeholders have received their compensation. If there is still liquidity left over, then – and only then – the shareholders will receive it. It can either be distributed to them (in the form of a dividend payment or a share buyback) or remain in the company (profit retention). An important consolation for the shareholders: No matter how much is left for them, the amount - unlike all other stakeholders - is not capped. Only the shareholders have – in principle – an unlimited “upside”.

A special feature worth mentioning applies to stage 3 of the cash flow cascade. As is well known, taxes flow to the various levels of the state. In Germany these are federal, state and local authorities. Taxes are the state's main source of revenue. The capital service (interest and repayment) for government borrowing, i.e. for bonds and loans that the public sector issues or takes out, is primarily provided from tax revenue. This means that the state is legally higher up in the cash flow cascade of companies in its role as creditor of tax claims and social security benefits than the company's debt creditors (loans, bonds or supplier debts), as landlord and of course higher up as shareholders. This “seniority” of the government’s creditor position is one of several reasons – and one that is usually overlooked – that government bonds are less risky must as corporate bonds in the same state. We have other reasons for this structural risk advantage of government bonds relative to stocks and corporate bonds Blog post “Sovereign Ceiling” explained.

Overall, the cash flow cascade causally explains a large part of the different risk levels of the different stakeholder claims of a company (stocks, bonds, landlord position, government payment claims, etc.). All of these claims are claims on the same Cash flow, although with different rankings. The risk driver “leverage” (the ratio of debt to equity in a company) is ultimately a consequence of the cash flow cascade. Other factors that affect a company's risk to shareholders and bondholders include: B. the so-called “operating leverage” (the ratio of variable costs to fixed costs), the general industry risk, interest rate developments and company-specific factors such as the quality of management.

The cash flow cascade concept explains why stocks must have a higher return and higher risk than corporate bonds in the long term (even if this higher risk does not materialize in individual time frames) and why these in turn must have a higher return and higher risk than government bonds. Hybrid securities that represent mixtures of equity and debt, e.g. B. Convertible bonds or derivatives (investments derived from stocks or bonds) are merely variations or hybrids of stocks and bonds.

Conclusion

- The ranking of legal claims in the cash flow cascade is perhaps the most fundamental of all risk drivers.

- The cash flow cascade explains why bonds (when correctly compared) are structurally lower risk than stocks and why government bonds must be fundamentally lower risk than corporate bonds.

- The cash flow cascade further explains why rental properties must be riskier than government bonds.

- Volatility and other empirical risk indicators are merely consequences or manifestations of this risk driver, i.e. risk symptoms, but not the causes of risk, with which they are often confused.