Tue Gerd Kommer e Alexander Weis

Note: The basis of the data of this article of the blog was integrated in November 2021 with the data in perspective from 2019 and 2020.

The “investimento passive” – over a diversification of a large number of funds with neutral indicators in the market based on Buy and Hold – is likely to be a major success story in the world's investments in the market for the capital of the last 50 years. For this impressive amount of innovation, it is always a good example, even though the front has a great success, even though it is still dominant and still has a beautiful background. Questo is also the case of the “passive investment” with fundi indicizzati neutrali rispetto al mercato negli ultimi vent’anni or giù di lì. (Nella letteratura specializzata, il dates “neutrale rispetto al mercato” è used in modo diverse rispetto al presente articolo del blog e di solito si riferisce a strategy long-short che mirano a eliminare il rischio del mercato totale). The result of the ricerche condotte da various centinaia di economisti finanziari hanno portato no ultimi decenni a una variant dell'approccio all'investimento passiveo, oververo il “factor investing”, also chiamato also “Smart beta investing”.

Cosa sono i “fattori” or “premi di fattore”? I premi di fattore sono fattori di rendimento e di rischio statisticamente identificabili in una classe di asset come ad es. The contracts, the commitments and the real estate. This is a large part of the combination of rischio/rendimento all'interno della classe di asset. Statisticamente, the return and the size of a portafoglio titoli can be seen only by 90% of the value of the identification and the “Factor Exposure” in this portafoglio, over the quanto of a portafoglio è esposto a questi premi di fattore. A confrontation: statisticamente, the number of ore che gli students dedicano allo studio per unesame di matematica spiega a parte considerevole della deviazione dei voti degli students dalla media della della classe. In this sense, the fattore is the “number of the ore”. Altri fattori, come on. The intellectual quorum of one student represents another part of the statistical deviation from the media.

In this primary part of our trilogy of blogs on factor investing in the asset class, the focus is on the basis. Nella seconda parte, che sarà pubblicata il mese prossimo, descriveremo come integrare al meglio i premi di fattore nel proprio portafoglio gli aspetti da tenere presente.

The premium for the fat is not the same as the “premio small size”, but it also means “premio size” or “premio small cap”. In parole povere, si afferma che le piccole società quotate in borsa (piccole in termsini di capitalizzazione del mercato) produced in media rendimenti azionari più elevati rispetto all grandi società or al mercato totale (si veda la table seguente per il periodo 1975-2020).

Attraverso una sovraponderazione Puramente meccanica e disciplinata dei premi di fattore in a portafoglio, è possibile ottenere a rendimento aggiuntivo al net dei costi e delle imposte rispetto al mercato totale; The dates are “premio”. Per quanto riguarda the small cap, “sovraponderare” significherebbe aumentare the loro quota percentuale nel portafoglio oltre la quota che the small cap Hanno in a “portafoglio di mercato totale” neutrale (the percentage of small cap is equal to approximately 15% of the capitalization of the total market of the mondial market). “Sovraponderare” also has a complicated quantity of non-sia, perché tale sovraponderazione può essere ottenuta semplicementee acquisition of a small-cap ETF.

The exposure (exposure) to the prize for the small cap is not the same as the portafoglio small cap in “misura normal”, but only the portafoglio small cap in misura maggiore rispetto all’universo della classe di asset sottostante.

The factor investing is essentially a passive investment, overlooking the role of “stock picking” attribute (selezione mirata di single azioni; in general, “asset picking”) or at “market timing” attivo (entrata e uscita tattica da interi segmenti di mercato).

The factor investing is different from the traditional investment passively for an important aspect. With the factor investing, the title of the portfolio is not included in the capitalization of the market, but the principle of the investment is attenuated, too. attraverso the sovraponderazione di azioni Small Cap.

These are also important in the first two notes, on our side, in order to consolidate the scientific letters:

- Small Size: The piccole società per azioni (“Small Caps”) tendono ad avere rendimenti più elevati rispetto all grandi (“Large Caps”).

- Value: The company values favored volume (“azioni Value”), misurate in base an indicatori come il Price/Earnings ratio, tendono ad avere rendimenti più elevati rispetto alle società con valutazioni elevate (“azioni Growth”).

- Quality or Profitability: The company of high “quality”, based on the indications of redditivity, comes from the report on the use and libri content or the indications of indebitamento – tendono avere rendimenti più elevati rispetto all società di bassa qualità.

- Momentum: The company's recent history has seen a rise in relative speed and a change in the old age for a period of limited tempo and vice versa.

- Political Risk: Le azioni esposte a un elevato rischio politico (soprattutto le azioniq dei Paesi emergenti) tendono ad avere rendimenti più elevati rispetto a quelle che lo sono meno.

- Low Investment or Asset Growth: Le azioni with a crescita del totale di balance sheet relativeamente bassa tendono avere rendimenti più elevati per a periodo di tempo limitato rispetto a source with a crescita del totale di levata.

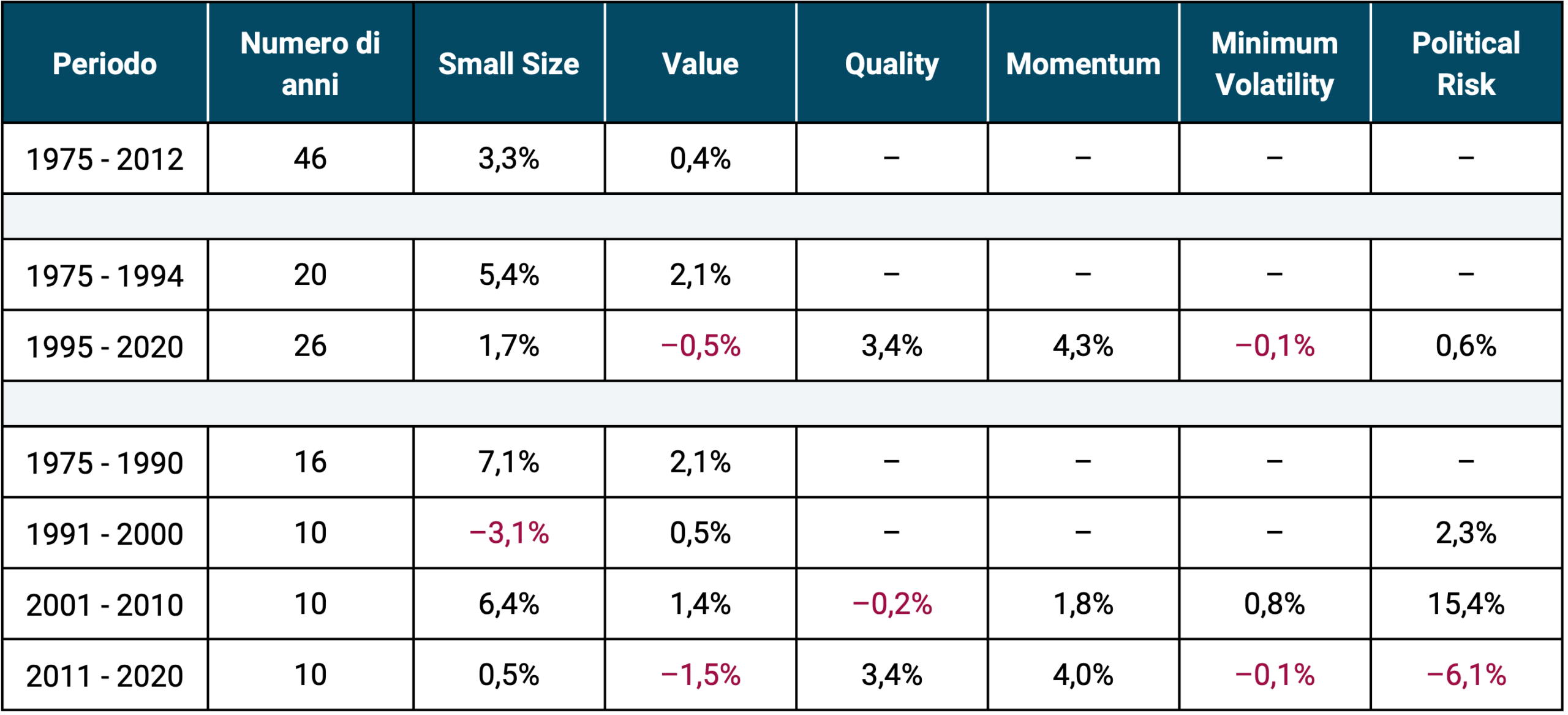

The table seguente mostra la sovraperformance storica degli indici di fattore rispetto al rispettivo benchmark neutrale rispetto al mercato. Questa version della quantificazione dei premium di fattore è particolarmente conservativea e viene chiamata “premi di fattore long-only”. You can see what you're talking about.

Table: Panoramica dell'entità dei diversi premi di fattore annuali dal 1975 al 2020 (46 anni) and dei partial periods in this 46 anni for the global market (“premi long-only”)

Fonte: MSCI, Dimensional Fund Advisors, Deutsche Bundesbank. Vengono mostrate the series of data available in the lungs (per singoli paesi itistono series in the data in the lungs). ► I premi di fattore sono “premi di fattore long-only” (si vedano le spiegazioni di seguito) based on the medium arithmetic. ► This is the Lord of the costs and the impost. ► I rendimenti storici not offrono alcuna guarantee che si ripetano su scala simile in future. ► The scientific studies at the beginning of the historical period give rise to diverse results in the second part of the country or region, the period of time and the method of specific rice.

The letter should be noted immediately that the majority of the fats are not so positive in any single period. This is possible, even if it is probable and necessary, that the price of the fat can be determined negatively for various years or decades, but the price of the fat can also be determined at the same time. In this contest, at least significantly, you can win a positive prize for a long period of time, which will continue to be successful in the short term and in the middle of the term. The award is not based on a forti fluttuazioni imprevedibili nel breve e medio appointments, sarebbe già stato “arbitrato” da tempo, ovvero sarebbe scomparso, perché in caso di elevata stabilità tutti comprerebbero solo queste zioni. I prefer to say that I am unaffected by the certificate and the average date.

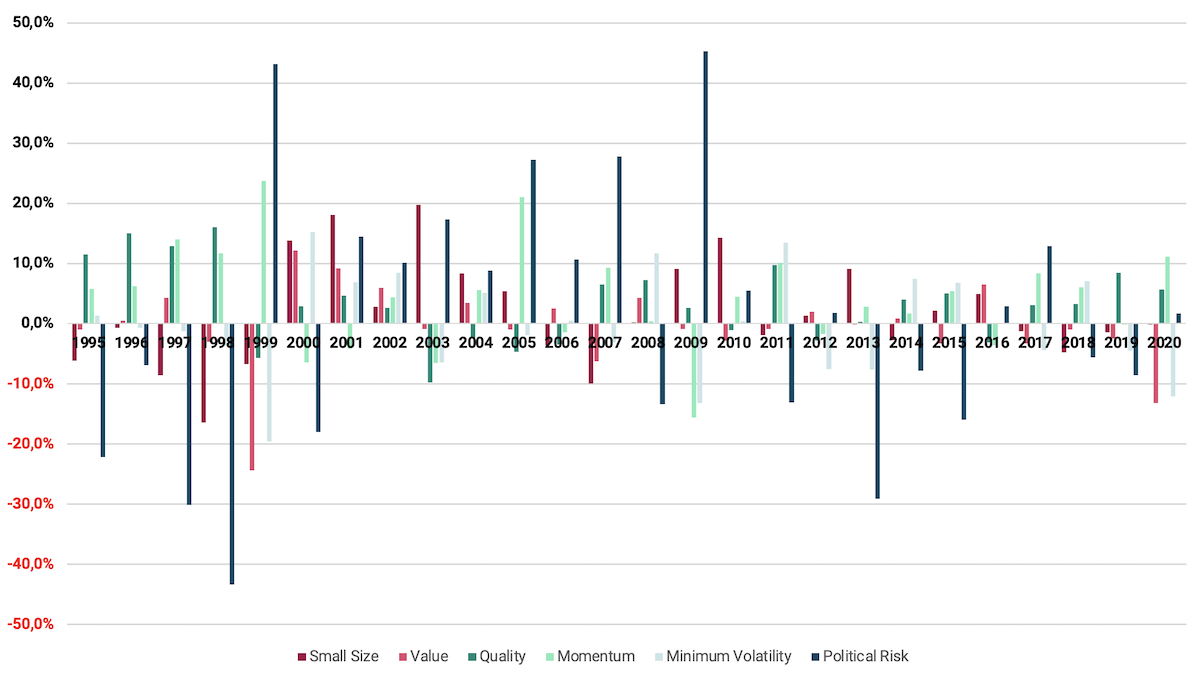

The second graphic illustration shows the potential of flooding. The graphic mostra the realizzazioni annuali the cinque premi di fattore sopra menzionati nel periodo dal 1995 al 2020. The verticale corresponds to all'importo percentuale dei premi in a determinato anno, mentre l'asse orizzontale rappresenta il trascorrere del tempo.

Figure: Andamento annuale dei premium di fattore long-only da 1995 al 2020

Font: Calculation based on the data sizes of Dimensional Fund Advisors and MSCI.

Osservando più da vicino le barre, risulta ancora una volta evidente che singoli premi di fattore possono sottoperformare il loro benchmark nel corso degli anni (barre negative). The stesso vale also per the cosiddetto premium equity, ovvero il rendimento supplementare del mercato azionario rispetto al mercato monetario “privo di rischio” (il “rendimento del libretto di risparmio”). The equity prize is also null or negative for the last year or so. The last date was 120 years old for a large number of people, including Germania and Stati Uniti. To attenuate the “inaffidabilità” of the premiums of fattors, it means that they are diversified in two premiums, but are not punished by a single paniere.

Ancora una parola sul concetto “long-only” di cui sopra: i premi di fattore possono essere calcolati come premi long-only o long-short. With the premi di fattore long-short, the position with a level of incidence of the desired caratteristic (in the case of Small Size) is also available in the same way and the position with an incline of the caratteristica opposta (in this case Large Size) is also sold in the scoperto [1]. I premi di fattore long-only si riferiscono solo alla parte “long” (parte di acquisto) dei premi di fattore; in this case it is not possible to sell it all to the scoperto. The price of the fattore long-short is also higher than the price of the long-only one. This means that the UCITS funds (“fondi comuni”) and the same ETFs are distributed in Germany are not normally authorized to operate on a wide scale, but are concentrated on the long-only fat premium.

For the first time in fat, it is important to note, in other words, the following aspects:

- I have various premi di fattore non sono “additivi”. Since the various premiums of fats are influenza vice-devolmente, the premiums of fats do not have to be taken into consideration. Queste interazioni non solo variano da premio a premio, ma possono essere sia positive che negative. It is significant that the various premiums of fats can be transported or indebolized by a vicenda. The moment is due to the first relationship between Hanno and a correlation [2] Minore di uno, the insertion of the first fattor in the portafoglio consente di ottenere vantaggi di diversificazione che riducono il rischio, the not deve essere considerato uno svantaggio, ma piuttosto an effetto collaterale desiderabile del “raccolto” di più premi di fattore. The same applies to the second part of the new series dedicated to factor investing.

- Another implication of the volatility of the premium fattors is that they can be expected to rotate intrapresa and the premium selection is also negative for a period of tempo prolungato. Come beforehand, first of all, it turns out to be positive. Nella media di lungo periodo, sono positivi in tutti and casi per definition (and also in its history).

- The fruit of the premium fattore costa denaro rispetto a un investmento neutrale rispetto al mercato. Tuttavia, i cost aggiuntivi sono più che compensati dai premi lordi (premi al lordo dei costi).

- I premi di fattore not confutano the nota EMH (Efficient Market Hypothesis, theoria dei mercati efficienti), almeno nella sua forma base, come viene ripetutamente affermato dai media or da Internet. The “Padre dell’EMH”, Eugene Fama, is also likely to be a meritocrat when it comes to the prize of the fattore. The EMH dice only does not have the possibility of a battery system in the “mercato” (rendimento of the asset class) at the net cost and price with the information available to the public. Questa tesi è molto ben supportata dai dati empirici degli ultimi 50 anni è compatibile with the existence of premi di fattore.

- Is factor investing also a “passive investment”? A nostro avviso, this domanda è inutile e troppo “ideologica”. The vero investment “passivo” is not in this community. The investor is also a passive investor who makes a decision and is also “attivo” in a certain misura. This is a global market that is not identical, but the structure of the “sotto-segmenti di rischio-rendimento” is statistically identifiable. I define and describe these two segments. In general, the factor investing is above all “attivo” dell’investimento passive neutrale rispetto al mercato.

Quale andamento avranno in future i premi di fattore e come è possible ipotizzare che i valori empirici storici, se correttamente interpretati, siano applicabili also in the future? Of course, it is not possible to respond to this issue with a 100% certificate, which is almost always a result of the discipline of the social sciences. In line with the principle, this also applies to the level of return “normal” in the class of assets at the top of the list: investments, investments in fruits, real estate, metals, prime materials or arte. In this case it is possible to prevedere with assoluta certezza l'ammontare dei rendimenti assoluti or relativi attesi nei prossimi 20 anni or oltre. I pay the fattore not fanno eccezione in this case.

If in the future the premium of the fats is added to the portfolio, the performance of the investor (and the cosiddetti “cost of opportunity”) will consist only of the cost of the product at an elevation of approximately 0.3 percent of the “fondi Smart Beta” rispetto ai fondi indicizzati neutrali al mercato. Ipotizzando la scomparsa di uno or due to the premi di fattore in futuro, ciò comporterebbe a riduzione del rendimento supplementare, ma non a sottoperformance del portafoglio dei fattori. Nel complesso, the sovraperformance attesa grazie all'impiego dei premi di fattore compensa ampiamente i loro costi aggiuntivi.

Riepilogue: I premi di fattore sono in grado di Spiegare in larga misura il reporto rischio/rendimento di un portafoglio azionario, in misura maggiore rispetto ad altre characteristiche oggettive come l’appartenza al settore, the rendimento da dividendi or characteristiche soggettive come the quality of management o The report from a society with determinati sviluppi macroeconomici (tassi d’interest, inflation, crescita economica, ecc.).

A nostro avviso, una determinata forma di sovraponderazione dei premi di fattore principali consentirà in futuro di ottenere a rendimento supplementare atteso rispetto al mercato totale compreso tra uno e un punto e mezzo percentuale all'anno al net dei costs (storicamente, questa sovraperformance è stata Significativamente superiore – si veda la table in thiso articolo). A new view, the first document that includes Small Size, Value, Quality, Momentum and Political Risk. I singoli premi di fattore non “funzionano” in modo affidabile in ogni anno e hanno una correlazione inferiore a +1, motivo per cui ha senso diversificare su più premium.

Nella second part of the quest series dedicated to factor investing affronteremo the questione di come integrare al meglio più premi di fattore nel proprio portafoglio. In this approfondiremo the various possibilities of implementation of Multifactor Investing.

È convinto del factor investing e desidera un’implementazione semplice e comoda? Abbiamo the solution 1-ETF di Gerd Kommer: l’L&G Gerd Kommer Multi-factor Equity UCITS ETF. Per saperne di più >

Final note

[1] Vendita allo scoperto — in english short selling: the vendita di un titolo (or di asset in generale) che lo short seller (venditore allo scoperto) non possiede ancora al momento della vendita T0, ma che ha preso in prestito a titolo oneroso da una terza parte. The period of the prestige termina is set at the same time, at the moment of T1, the vendor is all scoper to return the title to the prestatore. Per farlo, the vendor allo scoperto deve ora aquistarlo sul mercato libero. The vendor is all scoperto spera che the prezzo di merchandiser del titolo in T1 sia inferiore a quello in T0. There are continuous ebbs and profits. Egli specula quindi sul calo dei prezzi.

[2] The correlation is a misura dell'interazione tra due variabili casuali and può assumere valori compresi tra -1 e +1. A correlation of -1 or +1 is significant in a correlation of perfettamente negative or positive, while a correlation of 0 is significant, which is not a purely casual interaction. An example of positive correlation is the number of calories consumed by a person and his weight body: a number of calories tends to determine the weight of the body.

Letteratura

Baltussen, Guido; Swinkels, Laurens; Van Vliet, Pim (2019): “Global Factor Premiums”; available on SSRN: https://ssrn.com/abstract=3325720

Berkin, Andrew; Larry Swedroe (2016): "Your Complete Guide to Factor-Based Investing. The Way Smart Money Invests Today"; BAM Alliance Press; 358 pages.

Gerd Kommer (2018): “Invest confidently with index funds and ETFs. How to win the game against the banks”; 5° edition; Campus 2018. 410 pages.

Momentum Effect: Dolvin, Steven; Foltice, Bryan (2016): "Where Has the Trend Gone? An Update on Momentum Returns in the U.S. Stock Market"; riferimento Internet: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2813333.

Political risk effect: Pàstor, Luboš; Veronesi, Pietro (2013): “Political Uncertainty and Risk Premia”; in: Journal of Financial Economics; volume 110; edition 3

Profitability/quality effect: Asness, Clifford e altri. (2013): “Quality Minus Junk”; riferimento Internet: https://www.aqr.com/library/working-papers/quality-minus-junk

Effetto Small Size: Shi, Wenyun; Xu Yexiao (2015): “Size Still Matters!”; riferimento Internet: http://www.efmaefm.org/0EFMAMEETINGS/EFMA%20ANNUAL%20MEETINGS/2015-Amsterdam/papers/EFMA2015_0198_fullpaper.pdf

Effetto value: Zhang, Lu (2005): “The Value Premium”; in: The Journal of Finance; vol. 60; edition 1