The post “Homeowners are wealthier than renters in old age” – lies with statistics appeared first on Gerd Kommer.

]]>In this blog post we look at a specific old wives' tale about the financial attractiveness of owner-occupied residential properties, which has been re-proclaimed "twice a year" by most media in Germany and by the real estate industry for decades with headlines such as the following:

- „Property owners have significantly more money in old age than tenants“ – Headline of an article in the news magazine Spiegel from January 13th, 2025

- „Pensioners who own their own home are particularly wealthy“ – Headline of an article on the news portal t-online.de from December 17th, 2025

- „Homeowners accumulate more wealth than renters“ –Press release from the Association of Private Building Societies in 2025.

However, the statement “own-occupied home leads to higher wealth in old age than renting” is not far from the truth. The statement is a picture-perfect case of “lying with statistics.” [1]

Lying by concealing essential information

As we know, you can lie in many ways. One of them is that person A (the liar) formulates a statement B correctly, but deliberately omits essential information in order to cause a false understanding or error on the part of addressee C. So A lures C into a comprehension trap by omitting crucial information from statement B. That is the lie. Children can already master this method. In English it has a nice compact name Context Dropping used.

Context dropping – lying by deliberately omitting, i.e. suppressing crucial additional information – happens when the statement “Pensioner with his own home [2] are statistically wealthier than pensioners who rent.”

Below we show how this deception actually works. The claim that home ownership is among older households causal for a higher net worth (as conveyed in the exemplary publications cited at the beginning through manipulative context dropping), we will henceforth call “the real estate lie”. [3]

At first glance - without the correct context - the real estate lie in question appears to be true: homeowners actually have a statistically higher net worth in old age than renter households. This is shown by the relevant data and no one doubts its formal correctness.

But the crux of the matter: the statistical wealth advantage of homeowner households (EHBs) over renter households has nothing to do with owning their own home. It is entirely due to other causes. So here correlation is confused or swapped with causation. Yes, EHB households are generally wealthier as they get older than renter households, but they Caused This asset advantage is not the home.

Here is an illustration of the manipulative swapping of cause and effect Real estate lie: The wealth of the average Ferrari-owning household in Germany (around 14,500 households) naturally exceeds that of the average non-Ferrari-owning household (around 41 million). Now the question: Was the Ferrari the cause of this wealth advantage? Of course not. The Ferrari has statistically reduced this wealth advantage - without it, the wealth advantage of the Ferrari households would be even greater. Either way, Ferrari ownership was the result of the income and wealth advantage, not its cause. It's the same with home ownership. It is the consequence, not the cause, of a number of actual causal factors.

The real causes of homeowners' wealth advantage

The “real estate propagandists” are betting that their recipients will fall for the manipulated statement and misunderstand correlation as causality.

However, as scientific research shows quite clearly, the actual causes of the wealth advantage of EHB households are as follows: [4]

1) EHB households have a higher lifetime income, i.e. h. the sum of their net income over the entire period of earning capacity is statistically higher than for renter households. The proportion of households with two incomes is higher among EHB households than among renter households.

2) EHB households have a higher percentage propensity to save. A higher percentage of their net income, which is already higher in absolute terms (see number 1), goes into wealth creation than is the case with renter households. This higher propensity to save is also expressed in the willingness to submit to a “positive compulsory savings contract” that is linked to the loan-financed purchase of a home. More on that below.

3) EHBs are more risk-averse in their investment behavior and therefore achieve statistically higher long-term returns in their wealth creation away from their own home. This increased willingness to take risks is also reflected in the higher entrepreneurial rate among EHB households than among renter households (starting a business and entrepreneurship are very risky). The higher risk affinity is probably due, among other things, to the proven higher average financial literacy of EHB households.

4) EHBs receive more frequent, larger and earlier wealth transfers from their parents and grandparents through gifts and inheritances. This often happens by “subsidizing” the equity share when the EHB household first purchases property when it is young.

5) EHB households have lower divorce rates than renter households. Divorces often cause serious financial losses for those involved. We show why and how these asset losses happen here.

6) If a home investment fails individually - for example due to a combination of unemployment and excessive debt - the affected households often lose their home through seizure or forced sale and become renter households again. Paradoxically, particularly poor home investments contribute to the “home ownership lie” analyzed here.

Note that in the list and description of the six main causes of the higher wealth of EHB households, we did not say anything about Why These households have higher incomes, higher savings rates, greater willingness to take risks, higher financial literacy or lower divorce rates. Quite obviously, a large part of these wealth-promoting factors lies in the socialization of the people concerned; a small part could also be genetically determined.

Would you compare tenant groups with EHB groups where the six causes listed above no If there were a difference, it would be shown that renters statistically achieve higher or similar levels of wealth in retirement. [5]

Why higher wealth? Quite simply because renting in conjunction with other forms of wealth creation - above all with a simple, broadly diversified stock portfolio on a buy-and-hold basis - leads to a higher net final wealth than an owner-occupied property in the majority of time frames if the financial-mathematically correct comparison is made. Furthermore: The relative final asset advantage of the “rent + capital market investment” constellation will tend to be greater, the higher the loan share (“leverage”) is in the comparison EHB. We at GKI have shown this for Germany and others for other countries - see here and here.

We probably don't need to explain in detail at this point why the real estate lie has been spread again and again by real estate agents, property developers, real estate influencers and banks for decades. These parties earn directly or indirectly from real estate purchases or their financing.

The “compulsory savings contract” for real estate

In connection with the correlation phenomenon of the higher net wealth of EHB households in old age relative to renters, it is often even said that not People with conflicts of interest, i.e. “people without a real estate agenda”, argue that the higher net assets of EHB households are based to a large extent on the phenomenon of the “positive compulsory savings contract”. This means that an EHB household that, for example, has taken out a loan for 80% of the acquisition costs is obliged to pay the corresponding expenses (loan installments, property tax, insurance, maintenance) month after month until it has been completely repaid - typically after 25 years or more. Otherwise there is a risk that the property will be seized by the bank. Above all, the repayment element in debt service contributes directly to wealth creation: with every euro of repayment, the percentage of equity in the property increases.

A tenant household is not under a comparable pressure to save, according to the theory of the positive compulsory savings contract. As a result, tenant households will often save less overall or temporarily interrupt their savings over a 25-year period for consumption purposes.

Here too, the confusion/swapping of correlation and causality probably plays a role. People with a naturally high tendency to save are represented more frequently among EHB households than among renter households. This is probably because their pre-existing strong willingness/inclination to save makes it easier for them to accept the long-term reduction in consumption that comes with the “compulsory home savings contract”. These EHB households would not have been able to purchase their own home for certain reasons [6] or if they had viewed a home as a comparatively unattractive investment, the majority of them would have been just as disciplined and saved for the long term in other asset classes. So if you look behind the façade of formalities, you can't even speak of "compulsion" for most people or households who submit to the supposed "compulsory" savings contract, because they would save even without real estate.

What does the development of the “homeownership ratio” tell us?

If you realize that in almost all countries in the world and especially in Germany, wealth creation through owner-occupied residential real estate is financially supported by the state more strongly through taxation and transfer payments (cash benefits) than any other form of private wealth creation, and if you assume for a moment - incorrectly - that owner-occupied real estate systematically produces high returns on equity, then the homeownership ratio (HOR) in most countries would have to continue to rise over time. [7]

But that is not the case. In the USA, the HOR is now at 65%, the same level as 30 years ago, although every American president during this time announced during the election campaign that his administration would increase the HOR. The HOR average of the 38 OECD countries has essentially moved sideways over the last 20 years. [8] There has also been stagnation in Germany over the last decade (current level 47%). Before that, the HOR had risen moderately - probably due to the special and one-off effect of reunification in conjunction with significantly falling interest rates at the time - since in the eastern federal states the HOR was only 24% before reunification (today around 33%).

Wealthy Switzerland is probably the only economically developed country in which, compared to other forms of private wealth creation, home ownership has not yet been systematically favored or subsidized by the state - neither through taxes nor in any other way. [9] The HOR there is only around 40% - probably the lowest value globally. This is a strong indicator that the “natural” HOR in a rich country with a functioning, deep, liquid rental market and a high level of tenant protection (as is common in Western Europe) is in the 40% to 60% range, but certainly not 80% or higher - where politicians and the real estate industry would like the HOR to be.

In this context, many politicians and of course the entire real estate industry have been claiming for decades that a high HOR is a sign of national prosperity. This is also the view of most citizens. Nevertheless, this idea is probably wrong. Empirically, poor countries have higher HORs than rich countries, with rare exceptions. Romania and Bulgaria are among the poorest states in the EU, but have HORs of 86% and 95%, well above the level of the other, richer European states. In general, poor developing countries worldwide are more likely to have higher HORs than rich industrialized countries. One of the richest countries in the world, Switzerland, has – as mentioned – the lowest HOR globally. [10]

Trying to increase the HOR through state measures “with all financial force” is therefore likely to be – as in most countries over the last 25 years – a waste of taxpayers’ money, which is also economically detrimental to tenant households, and is therefore socially regressive and tends to increase wealth inequality.

The future development of residential property prices in Germany

How will residential property prices develop in the future?

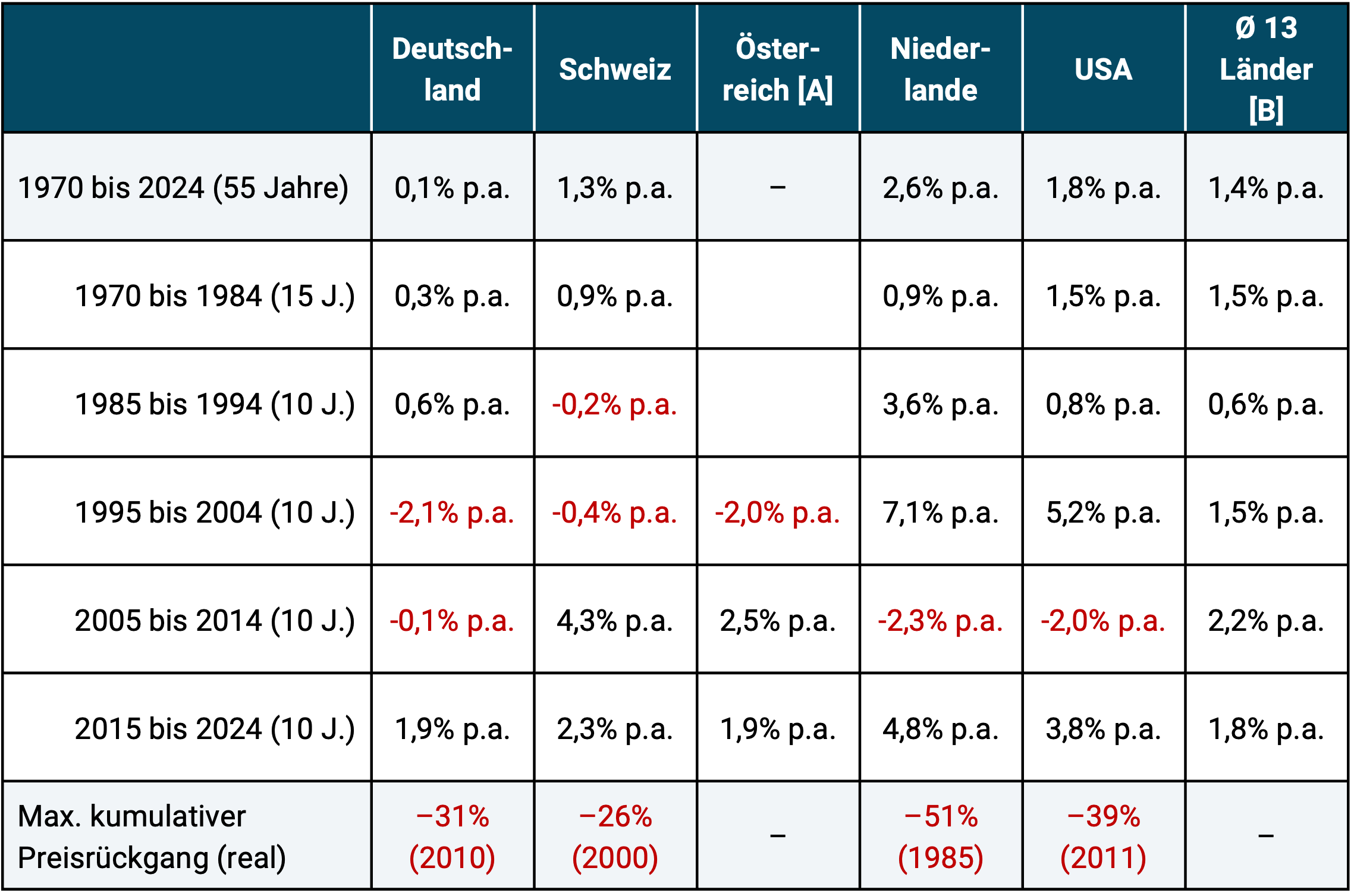

In order to answer this question, one should first look at their development in the long-term past. In the 55 years from 1970 to the end of 2024, residential property prices in Germany rose by a paltry 0.1% p.a., adjusted for inflation. Yes, in the eleven and a half years from mid-2010 to the beginning of 2022, prices had risen sharply, but in the approximately 40 years before that and in the three and a half years since March/April 2022, the increases in value, adjusted for inflation, looked poor - even in the largest cities of Berlin, Hamburg, Munich and Cologne. Since spring 2022, residential property prices in Germany, adjusted for inflation, have fallen from their peak at the time by 26% (Greix index) by September 2025 and by 17% (Europe index) by December 2025 - the most recent figures available. [11] (We show the long-term historical price development in Germany and twelve other western countries since 1970 here.)

We already know with great certainty that the population in Germany will begin to shrink from around 2030. Slowly at the beginning, then faster and faster. This means that a demographic headwind that will continue to affect the development of residential property prices for decades will continue. This demographic “price suppression effect” is further intensified by the fact that those who leave the real estate market due to death occupy particularly large areas per person at this time due to their age and wealth. So we will not only have a decline in population and a resulting dampening effect on demand, but - in addition to the net new construction - an indirect increase in the supply of space, since the owners and tenants who leave the real estate market occupy far larger areas per person than the young people who enter the real estate market after moving out of their parents' house. This increases the supply of space relative to demand.

It is possible that real estate prices in Germany, which have fallen since 2022, are already the front end of this demographic supply and demand effect. Asset markets generally already price in the developments expected for the future in the present.

Another long-term effect on increasing the supply of living space, although its strength is difficult to estimate, could result from the conversion of vacant office space into residential space. (It is also conceivable that in the next few years an AI-related loss of administrative jobs will lead to a second wave of reductions in the need for office space after Corona.)

Government actions to combat climate change will also tend to have a detrimental impact on housing prices and returns in the future. At least that's what Allianz writes in Allianz Global Wealth Report 2024. [12] We consider this assessment to be plausible.

Conclusion

There are many over-optimistic myths circulating about the financial attractiveness of residential real estate as an investment class that do not stand up to a rational comparison with reality - e.g. B. Research results from independent scientists and empirical value increase data from the last 30 to 50 years.

One of these myths is “property owners have more wealth than renters when they get older.” Anyone who formulates this statement “without context” in such a way that the recipient of the statement will probably conclude that real estate ownership has produced this wealth advantage is lying.

Although EHB households are wealthier on average than renter households, the reasons for this wealth advantage are other than the property: (a) higher long-term incomes, (b) higher propensity to save, (c) more risk-taking investments, (d) more wealth inflows via gifts/inheritances (e) fewer divorces.

If the EHB households in question had not invested in an owner-occupied property, but would have remained renters and - without spending a cent more (but not less) on housing and building wealth - they would have invested in more profitable forms of investment such as. For example, if global equity ETFs were invested, they would be invested on a fixed date, e.g. B. the age of 60, was even wealthier.

How beautiful the world would be if everyone who professionally deals with investments for others pursued the goal of spreading as little disinformation as possible in their communication and marketing, including no disinformation through context dropping.

Endnotes

[1] There are numerous books about how this works in general. One of them is “How to lie with statistics” by Prof. Walter Krämer (Amazon link here).

[2] In this blog post, “home” means any type of owner-occupied residential property, including both houses and apartments.

[3] Net worth = Gross worth (total of all assets) minus liabilities.

[4] At the end of this blog post we mention some of these academic studies.

[5] Such studies that neutralize all six causal factors in the study design may not yet exist. They would be very complex and expensive.

[6] For example, because for professional reasons they (have to) live in a place where they do not want to live permanently.

[7] At the end of this blog post in the appendix we show in Table 1 the tax preference for wealth creation through home ownership relative to wealth creation through e.g. B. Shares by the German state.

[8] The OECD is a supranational organization of which, by and large, the 38 wealthiest countries in the world are members. The main task of the OECD is to reach agreement on national tax and economic policies between member states.

[9] The abolition of the so-called Imputed rental value taxation In Switzerland from probably 2028 onwards, this will also lead to state subsidies for wealth creation through one's own home in relation to other forms of wealth creation. For information on imputed rental value taxation, see the keyword “imputed rental value” in the German-language Wikipedia.

[10] Of course, almost all Swiss residential properties still belong to Swiss citizens or Swiss companies (which in turn belong to Swiss citizens), but around 60% do not belong to the households that live there.

[11] It is normal that different property price indices sometimes differ greatly from one another over short periods of time.

[12] "The long-term impact of climate change on housing prices comes mainly through transition risk i.e. the energy consumption of buildings, particularly for heating. Projections of the House Price Index (HPI) in the UK under different climate scenarios up to 2050 show declines between -9.3% and -13.1%. For Germany, cumulative HPI declines could be as high as -24.5%. This would imply per capita losses of EUR32,380. Applied to all markets under consideration, homeowners could face losses of up to EUR30 trillion.” (Allianz Global Wealth Report 2024, p. 5).

appendix

Table 1: The drastic tax incentives for homeownership in Germany compared to Building wealth with capital market investments

► Assumption: Stock ETF is part of private tax assets. ► [A] The current income from a home is the rent saved for the owner. In various countries, this “fictitious” income must be taxed by the owner. ► [B] Stock ETF: 18.5% with 30% partial exemption (70% × 26.375%). ► [C] Inheritance and gift tax exemption for the home. If children or grandchildren are the recipients, then the exemption limit is 200 sqm, for spouses there is no sqm limit. ► [D] Property tax: The effective taxation is property-specific. A rough approximation is given here as a percentage of the current value of the property. ► [E] The stated value results from a property transfer tax of e.g. B. 5% and a holding period of 40 years: 5% ÷ 40 = 0.13% p.a. ► Saver's flat rate of 1,000 euros per person per year for capital market investments is ignored here for the sake of simplicity. It also ignores overall low state subsidies for Riester savings and capital-forming benefits (VL) and the retirement provision portfolio that will exist from 2027.

Literature references

Allianz (without author): Allianz Global Wealth Report 2024; Allianz Insurance Group; Allianz Research; Internet reference here

Birkjaer, Michael et al. (2019): The GoodHome Report 2019 - What makes a happy home?"; Kingfisher plc and the Happiness Research Institute; June 4, 2019; Internet reference here

Bracke, Philippe et al. (2014): “Homeownership and Entrepreneurship: The Role of Mortgage Debt and Commitment”; Working Paper No. 5048; Ifo Institute; Internet reference here

Braun, Rainer (2024): “You build tomorrow’s empty property today”; Interview with Rainer Braun from Emprica in Der Spiegel from July 5th, 2024; Internet reference here

Dräger, Jascha et al. (2024): “The Keys to the House – How Wealth Transfers Stratify Homeownership Opportunities”; German Institute for Economic Research/DIW; October 12, 2024; Internet reference here

Fagundes, Dave (2017): “Buying Happiness”; In: William & Mary Law Review; 58, 2017; Internet reference here

Krämer, Walter (2015): “How to lie with statistics: About the risks and side effects of non-statistics”; Campus Verlag 2015 (book)

Goetzman, William/Matthew Spiegel (2000): “Policy implications of portfolio choice in underserved mortgage markets”; SSRN; 02 Nov 2000; Internet reference here

Moussouni, Oualid et al. (2023): “Does Owning a Home Build More Wealth?” Canada Housing and Mortgage Corporation/CHMC; Internet reference here

Shlay, Anne: (2006): “Low-Income Homeownership: American Dream or Delusion?” In: Urban Studies 43, No. 3, pp. 511-531; Internet reference here

Wong Bucchianeri, Grace (2011): "The American Dream or the American Delusion? The Private and External Benefits of Homeownership for Women"; July 3, 2011; SSRN; Internet reference here

The post “Homeowners are wealthier than renters in old age” – lies with statistics appeared first on Gerd Kommer.

]]>The post Renting or buying – which is more financially attractive? appeared first on Gerd Kommer.

]]>Of the 41 million households in Germany, 43% = 17.6 million own the property in which they live. 57% (23.4 million) are renters. Two thirds of renter households aim to purchase a home (an apartment or a house) in the future. If you ask homeowners aspirants about their motives for purchasing a property, financial motives are mentioned much more often than lifestyle motives, e.g. B. “good retirement provision”, “living rent-free in old age”, “good returns”, “concrete gold”, “material value”, “safe investment” and “inflation protection”.

In Gerd Kommer's book published in 2021 "Buy or rent? How to make the right decision for yourself" The financial and non-financial arguments in a buy-or-rent decision in Germany were compiled and analyzed. The purely economic part of the analysis therein is based on historical data from 1970 to 2020 (51 years). Since then, more than four years have passed, during which a lot has happened in real estate prices, interest rates, rents and capital market returns. Time to bring the financial buy-or-rent comparison in the book up to date with updated figures by the end of 2024.

Due to space limitations, we will not go into this blog post non-financial Arguments, i.e. emotional and lifestyle considerations, which - depending on the argument - speak for either buying or renting. The non-financial arguments are comprehensively covered in the book mentioned above.

Which comparison method leads to truly reliable findings?

Do you want for one? specific Purchase object and one specific Rental situation - i.e. an individual case - to carry out a buy or rent calculation looking into the future, there are numerous useful buy or rent calculators on the Internet. We list links to ten free online calculators at the end of this blog post under point 1 in the appendix. However, such a prognostic case-by-case calculation cannot be used to draw any generalizable conclusions for the purchase or rent consideration.

If you want to formulate generalizable statements about the fundamental economic attractiveness of buying versus renting combined with a simple capital market investment (an ETF portfolio on a buy-and-hold basis) beyond non-representative individual cases, individual case calculations will not help. Structural conclusions can only be reached by calculating with representative statistical data and over sufficiently long, representative periods of time.

If you do that, another basic methodological question immediately arises: Do you want to carry out the comparison on the basis of historical data or on the basis of forward-looking forecasts? Prognostic calculations are inevitably based on subjective assumptions about the future development of home prices, interest rates, rents, capital market returns and taxes. Although forward-looking assumptions for time frames beyond a few months are uncertain and will later turn out to be mostly wrong, the media and real estate finfluencers still predominantly use forecast calculations for their general buy-or-rent analyses. Here are three examples:

- “Buying is cheaper than renting in these seven cities” – Wirtschaftswoche, March 18, 2024, print article

- "Rent or buy? Which strategy is worthwhile in your region" – Handelsblatt, July 5, 2018, print article

- “Is real estate worth it in 2025?” – Finanztip, August 27, 2025, video

The use of forecasts to answer the generalThe question, which is not specific to an individual household, as to whether buying or renting + an ETF portfolio is more financially attractive seems strange when you think about it more closely. To assess the economic attractiveness of Financial market investments - stocks, interest-bearing investments, raw materials, precious metals and cryptocurrencies as well as the financial products derived from them - are practically without exception historical Data series used. So no forecasts, which are based on uncertain, subjective assumptions and will probably not come true as formulated.

Therefore, we base our buy-or-rent analysis in this blog post on this Best practices science and do not calculate on the basis of predictions and assumptions, but on the basis of historical market data. Because we use historical data, because we go back 55 years to 1970, and because we compare our results with academic studies for other countries, our calculated numbers allow fundamental, structural conclusions to be drawn.

What should you consider when making a correct buy or rent comparison?

Here are three basic principles that a reliable comparison of buying and renting + capital market investment must meet:

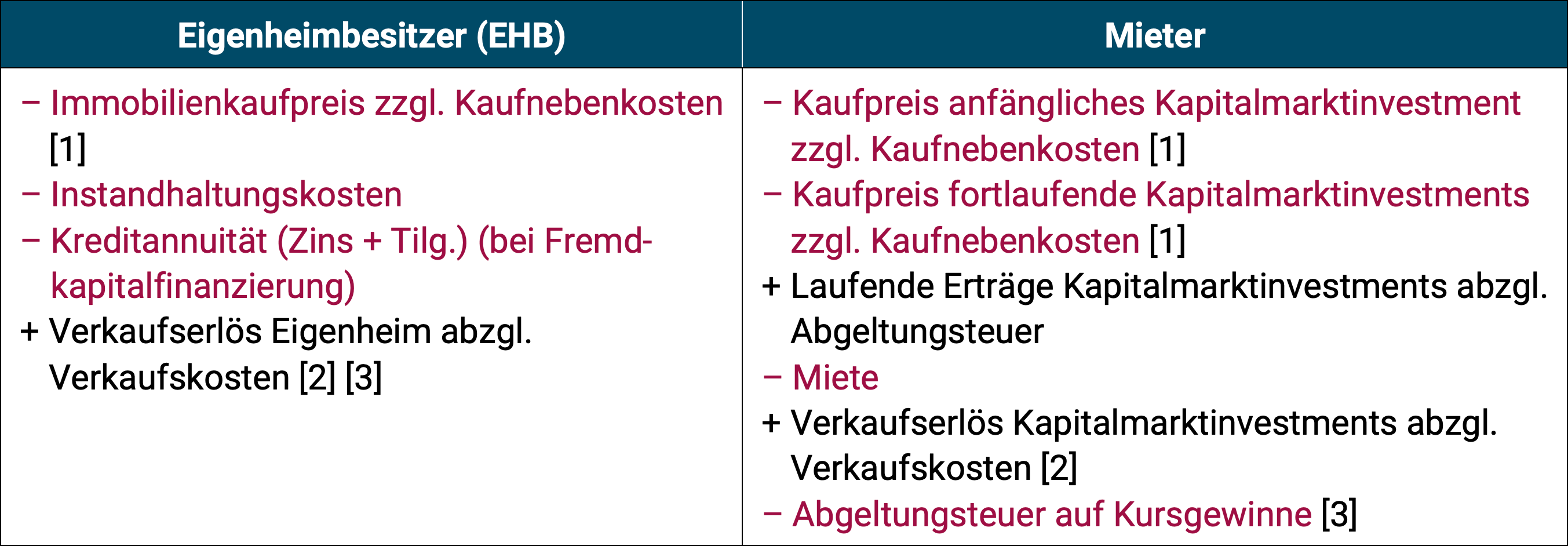

- Buyers and tenants + ETF investors live in an identical property.

- Buyers and tenants have identical “cash outflows” initially and every month, i.e. they invest the same amount in their wealth creation, i.e. they forgo consumption for wealth building purposes are the same. What exactly is meant by “identical cash outflows” becomes clear in Table 1 below. There, the cash outflows in lines 1 and 2 for the homeowner (EHB) and the tenant/ETF investor amount to the same amount. This equality is achieved by the tenant investing the difference between his monthly rent and the EHB's total expenses in an ETF savings plan.

- The observation period (the analysis period) must be sufficiently long, typically longer than 15 years. Shorter time periods are too distorted by random, temporary market conditions. In addition, most real estate financing takes over 20 years to be completely paid off.

Table: Comparison of cash flows between homeowners (EHB) and tenants in an objective rent-or-buy comparison

Reading note: Cash outflows (from the perspective of the EHB or the tenant) are shown in the table in red and with a minus sign, while cash inflows are shown in black with a plus sign.

► [A] Additional purchasing costs for real estate: real estate transfer tax, broker fees, notary fees, land registry fees. ► [B] If the observation period is shorter than the time until the loan is fully repaid, the existing remaining loan debt is deducted from the sales price of the property to arrive at the net final assets. ► [C] It is assumed that all current income (e.g. dividends) minus taxes are immediately reinvested (investment).

If you design an economic buy-or-rent comparison like in the table, then the party with the higher net assets at the end of the observation period (final assets) has the “investment race”. EHB against tenants won.

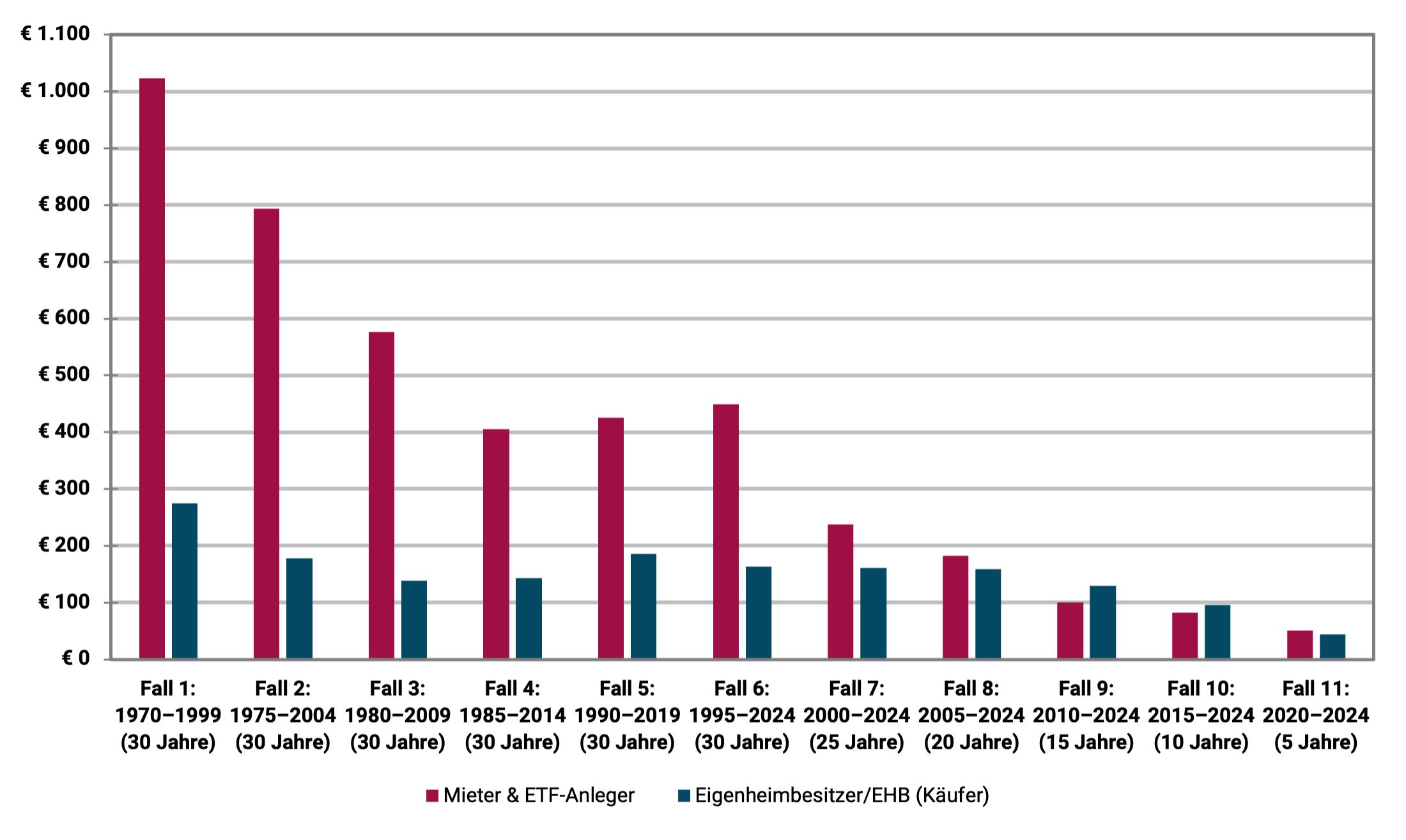

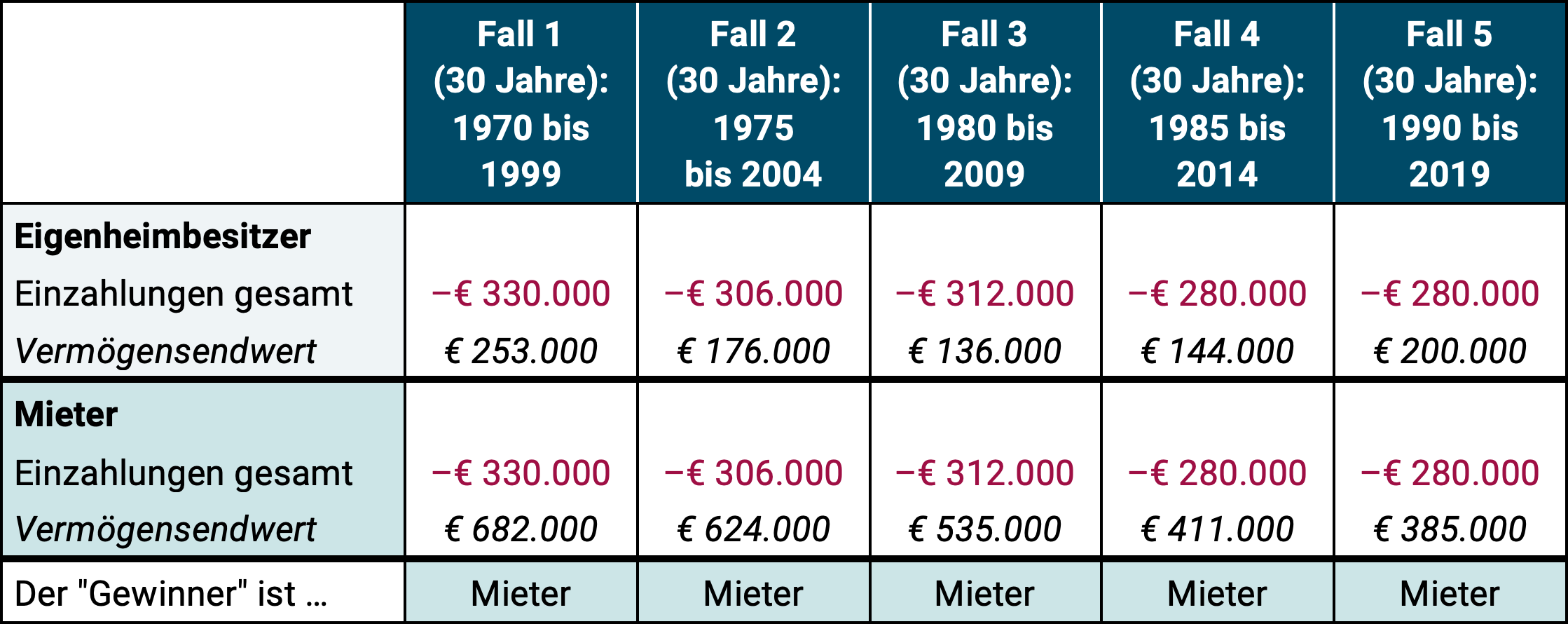

We summarize the results of such a calculation over the entire period from 1970 to 2024 (55 years) in Germany in the following figure. The tenant's capital market investment consists of a simple ETF portfolio on the MSCI World stock index on a buy-and-hold basis. [1] The real estate investment for homeowners is the average residential property in Germany. We accept initial 70% credit financing from the EHB.

We look at eleven different time windows, each lasting a maximum of 30 years, since a typical 70% real estate financing is fully repaid after around 28 years on average. We describe the further assumptions and inputs in the calculation at the end of this blog post in the appendix under point 2 for those readers who want to know exactly how we calculated. Readers primarily interested in the results may ignore the additional explanations in Appendix 2.

Figure: Comparison of the final wealth of homeowners/buyers versus renters/ETF investors in 11 different time windows between 1970 and 2024 (55 years)

► Final assets in EUR thousand.

The interpretation of the results in the figure: Why is the tenant in the lead in the majority?

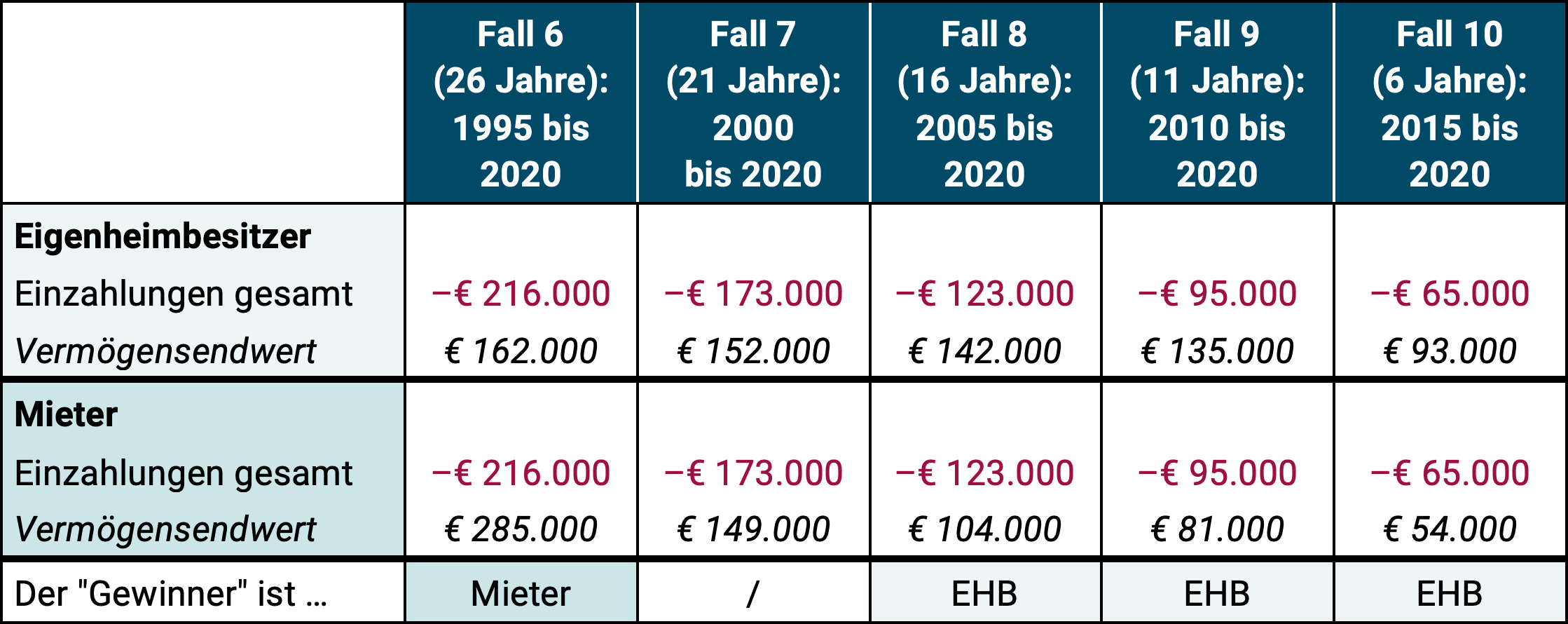

In nine out of eleven cases, the tenant/ETF investor achieved a higher final net worth at the end of the second period under consideration. Only in the two cases 9 and 10 is it the other way around. However, the EHB advantage in absolute monetary units is small in these two cases: only 19 and 14 thousand euros, respectively.

In general, cases 10 and 11 have to be classified as less important for our conclusions compared to cases 1 to 9. Firstly because they only represent relatively short periods of time and secondly because of the rather insignificant absolute differences in final wealth between EHB and tenant. One could therefore speak of “draws” in “yield races” 10 and 11. A clearer result in one direction or the other would probably only emerge after another five to ten years.

The main reason why the tenant + ETF investor wins our buy or rent race nine out of eleven comparisons is that the equity global asset class produces noticeably higher total returns in the long term than the residential real estate asset class. This applies to German residential properties and it also applies to other countries for which corresponding total return data for residential properties is available. Nevertheless, it must be noted that residential property returns in Germany have been particularly low compared to other countries since 1970 to the present day.

But why is the tenant's final asset advantage in cases 1 to 6 so spectacularly high? (In case 1, for example, 748 thousand euros in favor of the tenant.) There are four reasons for this.

Cause #1: Cases 1 to 6 last the full 30 years, cases 7 to 11 do not. Due to the compound interest effect, differences in returns between two investments A and B have a greater impact on the final assets, the longer the observation period is.

Cause No. 2: German residential real estate recorded disastrously low increases in value in the 44 years from 1970 to 2013. At the end of these four and a half decades, the average German residential property, adjusted for inflation, was worth 16% less than at the beginning - the worst value among around 20 western countries for which such data is available.

Cause No. 3: From 1970 to 2013, real estate loan interest rates were significantly higher at an average of 7.4% p.a. than from 2014 to today at 2.2% p.a.

Cause No. 4: Rents and rent increases in Germany were comparatively low from 1970 to around 2015. During this time, this also favored the tenant/ETF investor side (as did causes 1 to 3).

What influence does the amount of the loan share, the “credit leverage” have?

In our calculation for the illustration, we assumed an initial loan financing of 70% for the EHB. If 100% equity financing had been used (i.e. zero credit), nine of the eleven time window cases would still have been in favor of the tenant, although the distribution of winners and losers and the absolute final asset values would have shifted.

A higher credit percentage than 70%, e.g. B. 85% would also have coincidentally resulted in a 9-to-2 overall result in favor of the tenant as shown in the figure, while this modification would in turn have changed the specific winner-loser distribution across the eleven cases.

In general, it can be concluded that it is popular in the real estate fan community Credit leverage [2] On balance, the EHB was rather detrimental to returns. The lack of financial benefit of the credit leverage effect on the final assets and return on equity of real estate investments contradicts the prevailing opinion in the real estate fan community and among those who make money from selling and financing real estate, i.e. brokers, banks and real estate coaches. In our separate blog post “The credit leverage myth in real estate” we show that and why loan financing (leverage) in commercial real estate financing - where there is better data regarding the effect of debt financing - is statistically detrimental to returns.

What impact would variable loan interest rates have had?

In many Western countries, private real estate loans mostly have variable interest rates, while in Germany long-term fixed interest rates of ten years or more dominate. Would variable interest rates have significantly changed the results in the figure? The short answer: Only marginally and more in the tenant's favor. He would have won the final wealth race in the case of variable interest rates in ten out of the eleven cases. Reason: The interest rates, which have risen sharply since the beginning of 2022, had a less favorable effect on the EHB.

Why does the media regularly report that homeowners are, on average, richer than renters in old age?

How do our results fit in with the statement that has been made repeatedly by the real estate industry, journalists and real estate influencers for decades, that pensioner households that own their own home have, on average, higher wealth than corresponding renter households? On the surface, the statement in question is true, but it is still a case of “lying with statistics”. For these households, home ownership is not the cause of their higher wealth, but rather the consequence - more precisely, the consequence of higher income, typically over decades, combined with a permanently higher propensity to save. [3] In addition, there is a statistically larger and/or earlier increase in assets through donations or inheritances for EHB households relative to tenant households.

Here is an illustration of the real estate industry's manipulative swapping of cause and effect in the situation just described: The average wealth of all Ferrari-owning households in Germany naturally exceeds that of non-Ferrari owners. Now the question: Was the Ferrari the cause of this wealth advantage? Of course not. If anything, the Ferrari did damage. Either way, the Ferrari ownership was the result of the wealth advantage. It's the same with home ownership. He is the one Consequence the above-mentioned causes (primarily higher income, higher propensity to save and therefore higher wealth). If one were to compare renters with homeowners who had the same long-term income and the same propensity to save, and if inheritance effects were taken into account, it would be shown that renters statistically achieve higher final wealth in retirement. However, such empirical studies do not exist for Germany.

What about the home ownership advantage of the “positive compulsory savings contract”?

Earlier we mentioned the higher propensity to save among home-owning households. A higher propensity to save can have two causes: (a) A higher income. It falls e.g. B. It is easier to save 20% of 10,000 euros of net income per month than 20% of 2,000 euros. Furthermore, the absolute savings amount in the former case is 2,000 euros and in the latter case only 400. (b) A purely psychologically caused higher “savings affinity”, i.e. if two households A and B have an identical net income, but household A saves 30% of it and household B only 5%, then household A has a purely psychologically caused higher propensity to save. In plain English: Household A is more economical and cuts down on consumption more.

If a home is financed with debt with a debt ratio of around 60% or higher, then this household will have to incur higher real estate-related expenses per month from loan annuity and other real estate expenses (average maintenance, insurance, property tax) than a comparable renter household. This difference exists until the annuity loan is fully repaid, usually 25+ years. Now the crux of the matter: Such an EHB household has no choice in making these expenses month after month until the loan has been fully repaid, otherwise it would lose the property to the bank through a seizure and would also perceive this loss as a social stigma. The comparable tenant household, however, is not under such pressure and risk with its ETF savings plan. He can stop saving every month and instead consume more without any short-term negative consequences. The tenant therefore needs a good deal of self-discipline in order to spend the same amount every month on financial training as the EHB for 25+ years. The latter, on the other hand, “is forced to do so by the circumstances” and is subject to a “positive compulsory savings contract” because of his real estate loan.

This effect - which is nothing other than the statistically higher propensity to save among owner-occupier households mentioned above - contributes to the fact that EHB households are actually statistically wealthier in old age than renters. But again: the statistical asset advantage of EHBs has nothing to do with the high profitability of the property. If anything, it can be said that this asset advantage despite of the home, not because of it. If a renter household has the same saving discipline as a home-owning household, the renter household will statistically have achieved a higher and often significantly higher final wealth by the age of 50, 60 or 70.

What if you don't use a 100/0 stock portfolio for the tenant, but rather a 60/40 stock-bond portfolio?

We based our rent-versus-buy comparison with a tenant on a 100% equity portfolio (an MSCI World ETF) because we believe that a globally diversified equity ETF on a buy-and-hold basis is less risky than a debt-financed investment in a single property. [4] (The fact that it is easier to observe and measure the ongoing fluctuations in the value of an ETF portfolio than the ongoing fluctuations in the value of the equity position in an individual property does not change this basic fact.)

If the tenant were to be based on a 60/40 portfolio consisting of an MSCI World ETF and a bond ETF (medium-term high-quality bonds), the final asset race in the eleven cases would no longer be 9 to 2 for the tenant, but only 7 to 4. The change in the result illustrates what we all ultimately know: stocks produce far higher returns in the long term than interest-bearing investments.

Two biases in favor of homeownership in our calculations

In two ways, our buy-or-rent calculation is biased in favor of buying.

Aspect 1: The calculation assumes that only one property purchase takes place during the observation periods. Although there is no data on the average holding period (median holding period) of a home in Germany, it is likely to be less than 30 years. Such figures are available for the USA. There, the median holding period for a home is around twelve years. In Germany it will be longer, but probably shorter than 30 years. Due to the very high transaction costs (additional costs of buying and selling) in real estate, the return on a home decreases as the holding period decreases. In addition, if a loan-financed home is sold “early,” there may be an expensive prepayment penalty on the loan.

Aspect 2: When taxing the tenant's stock ETF portfolio, the tax advantage that buy-and-hold has under the German withholding tax was not taken into account. We quantified this tax advantage in a separate blog post (“Save taxes through buy-and-hold”).

The academic literature on buying versus renting

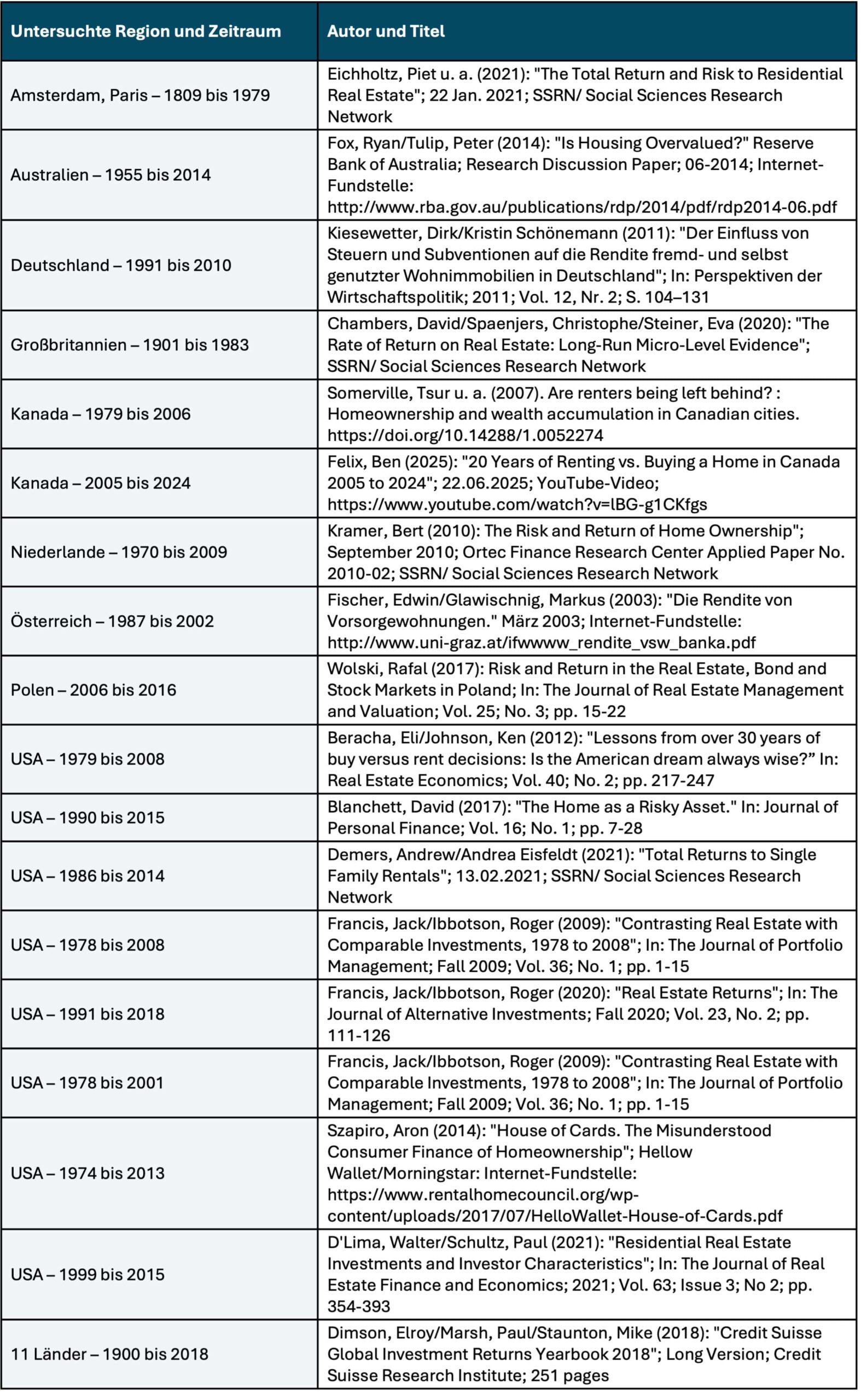

Our buy-or-rent results for Germany presented here are consistent with the basic trend from a number of similar historical buy-or-rent studies or general real estate yield studies for other countries and time periods. At the end of this blog post we list 18 such academic studies in the appendix under point 3.

Conclusion

In the 55 years from 1970 to 2024, renting combined with a simple, broadly diversified stock investment on a buy-and-hold basis was statistically more profitable in Germany than buying a home. This is what our empirical calculation shows and which is confirmed by a large number of comparable analyzes by researchers for other countries and time periods.

These results contradict what most Germans believe about the relative economic attractiveness of buying or renting.

The fact that banks, brokers and real estate influencers claim otherwise can easily be explained by the conflicts of interest of these parties.

The fact that many journalists and media outlets have been repeating the “buying is predominantly more profitable than renting lie” for decades is probably the combined result of “parroting prevailing opinions” and “not wanting to do strenuous research”. In addition, the mainstream media is reluctant to mess with wealthy advertising customers from the real estate and banking industries.

Attachment

Appendix (1): Free Buy or Rent Calculators on the Internet (in alphabetical order)

- Financial flow, independent finfluencer

- Financial tip, consumer protection organization (non-profit)

- Frankfurter Allgemeine Zeitung (daily newspaper)

- Gerd Kommer, author, asset manager (that “Buy versus rent tool” for the book “Buy or rent” by GK can be downloaded free of charge as an Excel file from Campus Verlag under the menu item “Additional material”)

- fmh financial advice, real estate portal (owner: private individuals)

- immoscout24, real estate portal (owner: Scout24 SE)

- real estate world, real estate portal (owner: Axel-Springer-Verlag)

- Dr. Small, credit broker (owner: Hypoport AG)

- Lazy Investors, independent finfluencers

- Stiftung Warentest, consumer protection organization (owner: non-profit foundation)

Appendix (2): The assumptions and data used in the calculation in the figure/graphic

On the real estate side (homeowner/buyer): The property costs 100,000 euros in all eleven cases. (For reasons of simplicity, we use the unrealistically low purchase price of 100,000 euros for a home today, but not in the 1970s, in order to calculate with “round numbers”. If one were to assume 400,000 or one million euros instead, for example, this would have no influence on the relative final result.) The additional costs of the purchase (including property transfer tax) are assumed to be 8%, those of the sale to 8% 1.7%. [5] The purchase and additional purchase costs are financed 30% from equity and 70% from a loan. The loan interest rates are the interest rates for annuity loans to private households with a ten-year fixed interest rate (the interest rate is adjusted every ten years). It is assumed that it will take 30 years for full repayment. The increase in value of the property corresponds to that of the average German residential property during this period. The ongoing additional costs (maintenance, insurance, property tax) correspond to 1.3% p.a. of the current property value. [6] The underlying statistical data comes from the BIS Basel and Bundesbank websites.

On the tenant side (tenant + ETF investor): The tenant initially invests the equity share of 32,400 euros initially spent by the EHB in a world portfolio consisting of an MSCI World index fund (ETF), as such a portfolio is comparable to a debt-financed individual property in terms of its long-term risk. Assumedly he lives in an identical property as the EHB. The rent for this property is based on the historical rental yields for residential properties (apartments) in Germany. Since the tenant's monthly or annual rent is below the EHB's total cash outflow, the tenant saves the difference every month in his ETF portfolio, so that both always spend the same amount on housing and wealth creation. The underlying statistical market data comes from Bulwiengesa and MSCI.

At the end of each of the eleven cases/periods under consideration, both EHB and tenants sell their investments. The tenant pays tax on his ETF investment continuously (dividends) and at the end when it is sold (price gains). Price gains from stock investments were tax-free for private investors in Germany until the end of 2008, after which they will be subject to capital gains tax. [7] Capital gains on homes are tax-free in Germany. In the five cases 7 to 11, the observation period is shorter than 30 years. Therefore, you will have a remaining debt balance with the EHB at the end of the period. To simplify matters, we assume that it will be repaid from the property sale proceeds without any early repayment penalty.

The payments (initial equity deposit and subsequent payments) for the buyer and tenant for the eleven cases are as follows. Case 1: €333 thousand, Case 2: €306 thousand, Case 3: €313 thousand, Case 4: €279 thousand, Case 5: €281 thousand, Case 6: €245 thousand, Case 7: €212 thousand, Case 8: €160 thousand, case 9: 119 thousand euros, case 10: 84 thousand euros, case 11: 54 thousand euros. (Cases 1 to 6 have the same length and should therefore have approximately the same amount of deposits. The existing differences result from different interest levels.)

Appendix (3): List of scientific studies on empirical comparisons of returns from buying or renting

The studies mentioned in the following table come to the conclusion for different time periods and countries that either real estate has lower total returns than stocks or that renting + capital market investment is overall more profitable than purchasing a home with or without debt financing.

Scientific studies on historical returns on residential properties or on buy-or-rent comparisons for different countries or major cities and different time periods

► This literature evaluation primarily took into account scientific studies that cover sufficiently long historical periods, as periods of less than approximately 25 years are only of limited or no significance. ► Not taken into account were (a) publications from the banking or real estate industry that were obviously burdened by conflicts of interest; (b) studies that represent only long-term historical appreciation rather than total returns on residential real estate; (c) buy-or-rent studies that formulate purely model theoretical conditions under which either buying or renting is more attractive; (d) Forward-looking, purely predictive buy-or-rent analyses.

Endnotes

[1] In the 1970s, index funds/ETFs were not yet available for private investors in Germany, but even then a private investor could have easily acquired a broadly diversified stock portfolio on a buy-and-hold basis.

[2] “Credit leverage” = The effect of partial debt financing on the return on equity of an investment (leverage effect).

[3] The propensity to save means the percentage of a household's net income that it does not consume, i.e. invests in wealth creation.

[4] If the property is at construction risk (in the case of a new build or major renovation), the property is even riskier.

[5] The sum of these transaction costs is likely to be at the lower end of what is usual in the market.

[6] In our separate blog post “Maintenance costs – how to calculate real estate investments” let's make this assumption plausible.

[7] We did not take into account the fact that price gains from so-called “old cases” – ETF shares that were acquired up to the end of 2008 – remained tax-free to a limited extent even after 2008, to the detriment of the tenant.

The post Renting or buying – which is more financially attractive? appeared first on Gerd Kommer.

]]>The post The credit leverage myth in real estate appeared first on Gerd Kommer.

]]>In a YouTube video by British finance professor Patrick Boyle about the current crisis in the UK commercial real estate market, Boyle says "No-one loves leverage more than real estate investors" [1] (Video link here). In fact, the crisis in the commercial real estate market in the UK, Germany, USA and other countries since 2022 has a lot to do with too much debt in the commercial real estate sector. Boyle's sarcastic remark about the popularity of debt financing and the credit leverage effect among real estate investors is correct. To illustrate this, here are relevant statements from German real estate finfluencers: [2]

- “Use as little equity as possible” – chapter title in an advice book on investing in residential real estate by Florian Roski and Mario Geiss

- “You won’t get rich without debt” – real estate finfluencer Tobias Claessens in a LinkedIn post from October 2023

- "Building wealth through real estate is possible for everyone. Even for you, without a lot of equity." – Title of a TikTok video from March 2024 by real estate finfluencer “Immo-Tommy” [3]

- “The leverage effect makes real estate investors really rich!” Title of a marketing video on the real estate agent's website Bartz Real Estate

In this blog post we would like to show that the leverage effect in real estate investments is presented alarmingly uncritically by many representatives of the real estate industry, including brokers, property developers, real estate finfluencers, providers of courses on investing in real estate (“real estate coaches”) and authors of advice books in the “Get rich with real estate” category.

We believe this primarily because there is simply no scientific or otherwise objective, hard evidence and figures that show that the credit leverage effect in real estate financing has even a somewhat reliably beneficial effect.

This is the result of our evaluation of the specialist literature from authors without conflict of interest on the effect of leverage in real estate investments. This involves both professional commercial investors and investments by private households - small landlords [4] and owner-occupiers. In Appendix 1 at the end of this article, we list a dozen specialist articles that show that a high proportion of debt capital in commercial and private real estate investments statistically has no financial advantage or is even detrimental to returns, i.e. it worsens either the absolute return on equity or at least the risk-weighted return on equity. The risk of real estate investments (in contrast to their return) always increases through leverage anyway.

As far as we know, there are no independent academic studies on the historically realized returns on equity of small landlords in Germany - with one exception: a study by the German Institute for Economic Research (DIW) from 2014 for the period from 2002 to 2012. With regard to the equity returns achieved by landlord households, this analysis comes to sobering results for small landlords. We have them here summarized in a previous blog post on rental property returns (link to original study here).

For homeowners in Germany, leverage has reduced returns in most long-term time frames over the 54 years since 1970. [5] This is based on figures in Kommer's book Buy or rent presented and more condensed in a blog post (here). Similar results were also found in other countries such as Australia, the United Kingdom, the United States and the Netherlands. Historically, the combination of rents and passive buy-and-hold capital market investments in Germany led to higher final wealth in the majority of cases. And the financial disadvantage of buying compared to renting + capital market investment tended to be greater the more borrowed capital the buyer used to finance his home.

A previous blog post of ours entitled “Leverage stock investments with credit – does it work?” (see here) contains a list of scientific analyzes that show that leverage in companies generally - not specifically in real estate companies - has a statistically negative impact on shareholder returns or company operating returns.

So if there is no hard numerical evidence that leverage has a reasonably reliably positive effect on the returns on equity of real estate investors and companies outside the real estate sector, why are brokers, real estate finfluencers, real estate coaches and the many authors of “get rich with real estate books” the majority of ardent advocates of credit leverage?

The answer to this question should not surprise anyone: The real estate service providers mentioned benefit from the highest possible number of small landlords and owner-occupiers in their business who believe that (a) you can get rich quickly with real estate, (b) that you can do this with little equity and (c) that the additional risk associated with borrowing is not too high.

How does the real estate industry convince private households of the attractiveness of “get rich by buying real estate on credit”, even though there is obviously no hard statistical evidence of success for this? This can be done by real estate service providers using one or more of the following six marketing tricks in their marketing. All six have the direct or indirect purpose of using credit leverage as a “magic tool”, [6] as a species Free Lunch when investing in real estate with little or no equity.

Marketing trick 1: Calculate the credit leverage effect

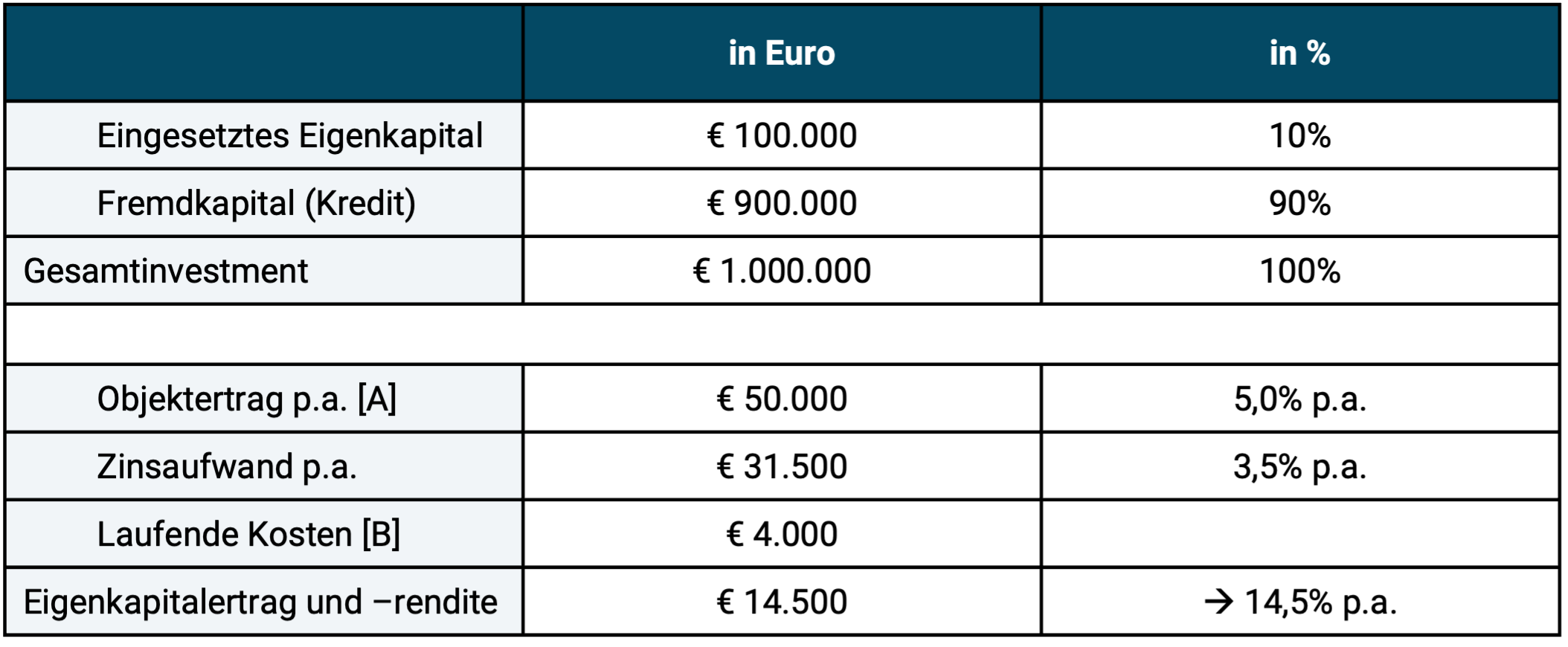

Almost inevitably, a calculation example similar to the following is presented in publications by those who earn directly or indirectly from the sale of loan-financed real estate. These calculations, which are “funny” from a technical perspective, could be titled “Getting Rich on an Excel Sheet”.

Figure 1: Weird example calculation of the credit leverage effect on a real estate investment in “Year 1”

► [A] “Property income” is defined here as gross rent plus increase in value. ► [B] Maintenance, insurance, property tax. 4,000 euros is at the upper end of what the real estate industry would typically state as a percentage, but is still clearly too low. ► The calculated percentage equity return is 14,500 ÷ 100,000 = 14.5%.

Extended calculation examples of the credit leverage effect such as the one in Figure 1 are intended to show that even with relatively low returns from residential real estate investments (net rents and increases in value [7]) attractive double-digit returns on equity result. [8]

You don't have to take such coaster calculations on the leverage effect seriously - not even if you accept that they are intended "for illustration purposes only". They are not to be taken seriously because they are deliberately created from a purely “accounting” perspective, which is ultimately incomplete. If they were complete, they would first of all have to be on one Cash flow basis or “internal rate of return basis”. However, this includes the cash outflow for loan repayment. With small landlords, repayment can never be avoided in the long term - even less so with owner-occupiers. [9] If one were to simplify the example in Figure 1 and take into account a linear loan repayment over 25 years (4% per year = 36,000 euros), the return on equity for the period under consideration would no longer be plus 14.5%, but minus 21.5% (loss of 21,500 euros), since interest expenses and repayment together add up to 67,500 euros.

However, omitting repayment does not mean that the credit leverage wizards' bag of tricks has been exhausted.

In other fables about the "magic of leverage" or about "paying for the property with other people's money and then watching it pay off through the rental income" the loan repayment is included, but in return one or more of the following "tricks" is used: The setting of (a) unrealistically high rental yields (the ratio of rents to acquisition costs or market value), (b) unrealistically low maintenance and management costs (in this blog post more on the assessment of the level of realistic maintenance costs for real estate) or (c) it is simply ignored that with such a “self-paying investment” it takes 20+ years until the cash flow for the investor turns significantly into positive territory because only then does the repayment element no longer apply. In other words, 20 long years to achieve “passive income”.

With the exception of interest rates, the inputs for such calculations are rarely from objective statistics and databases and one conservative Interpretation of the real market conditions derived. They are typically optimistic best-case assumptions for advertising purposes.

Marketing trick 2: Tell the old story of rags to (real estate) millionaire

Many real estate agents and almost every real estate finfluencer or real estate coach have them in their marketing repertoire because they are well received by the public: “Exciting stories” about individual investors who have become “financially independent,” “financially free” or “rich” by purchasing real estate with aggressive leverage – i.e. little equity or even no equity at all – and now live on their “passive income”. In order to make these “rags to real estate millionaire” stories credible, they often contain specific names and often even photos of “successful” real estate investors “who made it at a young age”. It is not uncommon for the narrator himself to be the subject of such a “success story” à la “how I got rich with real estate – and you can do it too!” Because of their specificity (names, photos), the stories seem credible to many recipients.

The unfortunate thing is that this anecdotal evidence can never be verified by outsiders. The majority of these descriptions are likely to be manipulated and some are completely made up.

In addition, the assets of the “successful” real estate investors stated in the stories are almost always properly inflated. In the “personal success story” the property value or the number of properties of the investor is mentioned: “Sebastian already owns nine properties at the age of 29” or “Lisa has a real estate portfolio worth seven million euros after five years”. There is always no information about the debts. [10] This is important because in every other industry outside of real estate and in life in general, “assets”, “wealth” or “net worth” are always referred to as Netassets are stated and understood, i.e. as gross assets minus debts. The general 2,000-year-old rule that “wealth” is the value of all of a person’s (or company’s) assets minus their debts (i.e. equity) applies everywhere except in the real estate industry.

Marketing Trick 3: Repeating the “Inflation will devalue your loan debt” myth

The spread of this “theory” is particularly useful for those who have little capital but want to finally become “rich” because it simply sounds too tempting: “Accrue debt that you only have to pay back in part!” And because this “theory” sounds smart and logical when quickly explained by the “financial experts”, it is believed by probably 90% of those who hear it.

The voodoo logic goes like this: Credit borrowers receive a financial advantage through inflation because their income (e.g. rents collected or their own salary) increases in the long term with inflation, while the amount of their debts and (in the case of fixed interest rates) the interest element are fixed. Both should therefore become less and less or “devalued” over time, adjusted for inflation (in real terms). This makes debts easier to service and pay off from year to year. But this apparently plausible thinking is only half the truth, and in this case the half truth is a complete lie.

The missing half of the economic reality in such fantasy stories: Due to inflation, nominal interest rates are higher than they would be without inflation. Inflation only devalues what the market inflation expectations previously added to the debt service (interest + repayment). We have explained what these economic connections look like in detail in a separate blog post (here). For reasons of space, we will therefore not specifically refute the inflation-devaluation-debt fiction in detail here.

Marketing trick 4: Hide hard figures on the German real estate market

In no other country for which long-term data on increases in the value of residential property are available have these been as low as in Germany since 1970. The increase in the value of residential real estate in this country, adjusted for inflation, averaged 0.1% p.a. from 1970 to 2023 (54 years). The average German residential property was worth a paltry 7% more in real terms at the end of 2023 than 54 years earlier at the beginning of 1970. Even in Japan, residential property prices rose faster. We have this fact, well known among experts here (blog post) and here (YouTube video) documented.

Yes, in the time window from 2010 to 2021 (12 years), the increases in the value of residential properties in Germany were very high. They were that because they were particularly low in the previous 40 years from 1970 to 2009, namely an average of minus 0.4% p.a. in real terms. Due to this return disaster, residential property prices in Germany were 16% below the 1970 level in real terms at the end of 2009. Because of their exorbitantly low valuation in 2009 compared to international standards and interest rates continuing to fall at the time, German residential property prices began to fall at the beginning of 2010 for twelve years until the end to rise sharply in 2021. Since 2022 they have fallen again and in September 2024, adjusted for inflation, they were 17% lower across Germany for existing properties than in February 2022. Ergo: The twelve years from 2010 to 2021 were a positive outlier against the long-term trend that was not representative of the long-term future.

Of course, increases in value are not the total return of a real estate investment, but if the real increases in value are close to zero in the long term, the statistical chances of high leveraged returns on equity are not good from the start.

Occasionally, in this context, one comes across the truly famous statement from some chronic real estate optimists:the There is no real estate market, every property is an individual case." If that were true, then there would be the stock market, the bond market, the raw materials market or the Not the automotive market. There would then actually be no market, just individual investments. Funny! The fact is that the prices of probably over 80% of all individual properties in a city or region correlate highly with the general price trend in the corresponding area and in the minority of properties for which this was not the case in retrospect, we knew it ex ante usually none.

Marketing trick 5: Present real estate as a particularly safe investment class

We have all heard it countless times in our lives from our grandparents, from real estate agents, real estate influencers, bankers, tax advisors and from our buddy who has just bought a condominium: residential properties are “particularly safe” investments. The Sparkasse Pforzheim Calw (Baden) puts it almost comically and bordering on unintentional satire in a marketing publication that is no longer available: “Real estate, probably the safest investment in the world […] Real estate has been one of the safest, most stable investments in Germany for decades - and it will maintain this status.”

However, the reality shines less than the dusty cliché of “stable concrete gold”. Housing prices can crash - just like stock prices, long-term bonds, high-yield bonds, the price of gold, Bitcoin or a private equity investment. However, a crash in real estate usually (but by no means always) occurs more slowly than in stocks and is therefore often not perceived as a crash.

Some crash examples of the decline or collapse of residential property prices (all figures adjusted for inflation): USA over six years from 2006 to 2011: minus 39%, Ireland over seven years from 2007 to 2013: minus 57%, Netherlands over eight years from 1978 to 1985: minus 51%, Japan over 20 years from 1990 to 2009: minus 49%, Germany over 30 years from 1981 to 2010: minus 31%.

In every country in the world for which data of sufficient quality and length is available, there have been declines in the national real estate market over the past 100 years that exceeded 30% in real terms. In France, real property prices fell cumulatively by 84% from 1911 to 1948. It then took the price level another 15 years to return to the level of 1911. Main cause: economic problems in the context of the First and Second World Wars as well as rent controls introduced in 1911, which were only gradually relaxed around 1948.

All of these numbers (a) exclude the loss-increasing effect of leverage and (b) all of the numbers refer to entire national markets. This means that half of all individual properties in these markets performed even worse, and the possible downside is even more extreme than is reflected in these market averages without leverage and transaction costs.

You rarely or never hear statistical data on past slumps in the residential real estate market from credit leverage advocates.

Compare the real estate industry's silence regarding historic droughts and slumps in the real estate market with the situation with equity investments, bonds, raw materials, gold or cryptocurrencies and the financial products derived from these asset classes. Inflation-adjusted historical long-term data, including drawdowns, crashes and duration of recovery phases, are freely available there and have long since been swept under the table by the industry. The reason they won't do this is because anyone who would do so would rightly be seen as a fool or a rip-off. With regard to the “stock crash of the century” from 1929 onwards, the collapse is even regularly overstated (see here).

Anyone who has ever bought a share or a share ETF anywhere in Germany in the last 20 years will inevitably have to click through or literally wade through risk warnings such as “there are high risks associated with investments in securities, including the risk of total loss” before making the purchase. This is transparency and realism.

Of course, total losses are also possible with credit-leveraged real estate investments, especially in severe market crises and in the case of individual unfortunate transactions even in good market phases. Nevertheless, one hears very little about evidence of such risk of loss in credit-financed transactions in the real estate industry and if there are, then they were “isolated cases” or “special cases”.

Marketing Trick 6: Statistics mean nothing because a smart investor only focuses on the best deals

It is the most widespread and probably the oldest of all real estate marketing tricks. It is mainly used when the previous five did not achieve the goal. The trick is the “brilliant” observation that statistics, empirical data and the usual factual logic do not have to apply “if you specifically select particularly financially attractive deals”. With the superior know-how that the respective advice book author or real estate coach imparts, in combination with the “commitment” and “focus” of the investor, this is of course not a problem. This brings to mind the advice of the American comedian Will Rogers (1879 - 1935) on successful investing in stocks: "Don't gamble. Take all your savings and buy some good stock and hold it until it goes up, then sell it. If it doesn't go up, don't buy it." [11] Further comments are unnecessary.

What are rational, sensible reasons for debt-financed investing in real estate?

Of course, there are rational reasons for using debt capital to finance real estate. These include, for example, these two:

- For property for personal use: Without external financing, a typical household would only be able to purchase a home at the end of their working life or even later. Here, debts serve to bring forward “consumption” over time. Bringing forward a consumption or investment decision has been the essential purpose of debt for 3,000 years, not exploiting the credit leverage effect.

- For small rentals: Debt-financed investing and credit leverage can have a positive effect for an investor (a) if he is 100% clear about the considerable risk of leveraged investments and has analyzed its economic and legal consequences thoroughly and competently, (b) if he knows that with fewer than around six to ten residential units the economic logic works pretty mercilessly against him, (c) if he reduces the level of debt to a more moderate level as the company grows and succeeds, lowered to a lower risk level [12] and (d) if he obtains legal notice at the earliest opportunity Firewall between commercial debts on the one hand and his private assets on the other. This means that he then holds a sufficient amount of wealth in the private sphere. With these private assets, he is no longer liable for investment liabilities. But these private assets that have been brought into the security zone can of course no longer be leveraged.

Conclusion

As we have shown here, the impact of credit leverage is naively and optimistically portrayed by much of the real estate industry.

According to academic studies, leverage appears to statistically worsen rather than improve the absolute return on equity or risk-weighted return for large commercial real estate investors, small landlords and owner-occupiers. Even outside the real estate industry, corporate debt statistically has a negative impact on key business metrics or shareholder returns.

Of course, someone who bought a residential property in Germany between approximately 2005 and 2018 and financed a significant portion of the purchase price with debt will have achieved excellent returns on equity after a holding period of five to ten years or more [13] – provided there was no isolated case of bad luck or inability. However, things looked less positive for purchases well outside this time window.

Against this background, the obsession with leverage in much of the commercial real estate sector, as reflected in Patrick Boyle's quoted statement at the beginning of the undying love between real estate and credit leverage, is highly ambivalent. However, it is clear why it exists: without leverage there would be fewer transactions for real estate service providers and therefore less money. And without accepting high leverage, a naive but important dream for many young people would collapse: “Get rich quickly without equity”.

It is high time that the real estate industry, financial journalists and finfluencers practice more honest, evidence-based communication about credit leverage.

Endnotes

[1] Leverage, Leveraging = credit leverage (effect), debt; Lever = lever.

[2] Social media influencers who specialize in the topic of money and wealth.

[3] Over Realty Tommy - according to their own statements, Europe's largest real estate finfluencer - Spiegel and NDR have published several articles and videos about Immo-Tommy's supposedly unfair business practices since August 2024. At the moment (as of November 2024) it is unclear how the matter will turn out for him.

[4] “Small landlord” is the terminology used by the Federal Statistical Office. This refers to landlords who do not operate the rental business full-time (non-commercially), usually with fewer than six to eight residential units.

[5] “Since 1970” because there is sufficiently good data available from that year onwards. How leverage worked beforehand is more difficult to assess due to a lack of sufficiently granular raw data.

[6] Quote from the book “10x for real estate investors – achieve more, grow faster, increase your portfolio tenfold” by Markus Beforth (2024).

[7] Net rent = gross rent less expenses for (average) maintenance, property tax and insurance.

[8] At the end of this blog post there is an Appendix 2 with a more detailed explanation of the leverage effect. Readers who are not yet well acquainted with the mechanics of debt capital leverage can find out more about this in the appendix.

[9] There is a fundamental difference here to large commercial landlords, where the banks accept that there is a permanently constant level of debt at the company level and that there is therefore no net repayment at the portfolio level. This is one of the many structural advantages of large investors relative to small landlords.

[10] For the sake of completeness, it should be mentioned that the numerical information on objects and object values cannot be checked here either. Why should these unverifiable numbers be true if they are obviously for marketing purposes?

[11] "Don't gamble. Take all your savings and buy a good stock. Hold it until it goes up. Then sell it. If the stock doesn't go up, don't buy it."

[12] If René Benko (Signa-Immobilien) had observed this simple risk management principle, he would not now be bankrupt and socially ostracized.

[13] Because the period mentioned includes all or most of the “golden German real estate era” from 2010 to 2021 as well as the zero interest period from 2016 to 2021.

Appendix 1

Below is a list of specialist articles that show that high leverage in commercial and private real estate investments tends to lower the absolute return on equity or the risk-weighted return on equity.

(a) Commercial real estate investments

Alcock, Jamie et al. (2013): “The Role of Financial Leverage in the Performance of Private Equity Real Estate Funds”; In: Journal of Portfolio Management; 39; No. 5; 2013, internet source here

Case, Brad (2017): “Comparing Listed REITs with Private Equity Real Estate: What the Cambridge Associates Data Have to Say”; Aug 16, 2017; Nareit/National Association of Real Estate Investment Trusts; Internet reference here

Giacomini, Emanuela/David Ling/Andy Naranjo (2016): “REIT Leverage and Return Performance: Keep Your Eye on the Target”; August 17, 2016; SSRN; Internet reference here

Haughwout, Andrew et al. (2011): “Real estate investors, the leverage cycle, and the housing market crisis,” Staff Reports 514, Sept. 2011, Federal Reserve Bank of New York

Pagliari, Joseph (2017): “Another Take on Real Estate’s Role in Mixed-Asset Portfolio Allocations”; In: Real Estate Economics, Volume 45, Issue1, Spring 2017

Green Street Advisors (no author) (2009): “Capital Structure in the REIT Sector”; July 1, 2009; Working Paper; Internet reference here

Sagi, Jacob/Zipei Zhu (2022): “Leverage in Private Equity Real Estate”; March 21, 2022; Working Paper; SSRN; Internet reference here

Thomas, Brad (2012): “REITs With Modest Leverage: Separating The Best From The Rest”; July 02, 2012; Wide Moat Investors; Internet reference here

(b) Private/non-commercial real estate investments

Beracha, Eli/Johnson, Ken (2012): “Lessons from over 30 years of buy versus rent decisions: Is the American dream always wise?” In: Real Estate Economics; 2012; 40; No. 2; Internet reference here

D’Lima, Walter/Schultz, Paul (2021): “Residential Real Estate Investments and Investor Characteristics”; In: The Journal of Real Estate Finance and Economics; 2021; 63; Issue 3; No. 2; Internet reference here

Mian, Atif/Amir Sufi (2010): “House Prices, Home Equity-Based Borrowing, and the U.S. Household Leverage Crisis”; April 2010; SSRN; Internet reference here

Jud, Donald/Daniel Winkler (2005): “Returns to Single-Family Owner-Occupied Housing”; Journal of Real Estate Practice and Education; Vol. 8, No. 1; 2005; Internet reference here

Schweizer, Jonas/Alexander Weis (2022): “Buy or rent? – Home vs. global portfolio”; Gerd Kommer Invest; Dec 2022; Internet reference here

Appendix 2: How the credit leverage effect works

First, a case study of how the leverage effect works:

Antonia invests 100,000 euros in an investment project We now imagine two scenarios. In scenario 1, the value of project

What effect does the two scenarios have on the return on Antonia's equity (EK)?

In scenario 1, Antonia's equity return is 30,000 euros ÷ 60,000 euros = plus 50% (profit from equity), in scenario 2 the equity return is -30,000 euros ÷ 60,000 euros = minus 50%. (We ignore the borrowing costs and any tax effects here for the sake of simplicity. Assumedly, there is no loan repayment.)

Without leverage, equity returns would have been plus 30% and minus 30%. (Where there is no leverage, equity return and return on assets, or “property return” in real estate jargon, are the same.)

We see that leverage symmetrically increases both the opportunity (the upside) and the risk (the downside).

In general, leverage results in increased equity returns for a given period, be it six months or 20 years, when the debt expense (absolute or percentage) is lower than the total investment return (absolute or percentage). The general formula for calculating return on equity is:

Explanation of abbreviations: EKR = return on equity, GKR = return on total capital, FKZ = interest rate on debt capital, FKA = share of debt capital in percent or absolute, EKA = share of equity in percent or absolute.

A numerical example. We use Antonia's investment in scenario 1 and a loan interest rate of 3%: EKR = 30% + (40% ÷ 60%) × (30% - 3%) = 48% (rounded).