The ETF is available from the piano by accumulo presso the major part of the fornitori.

The post The global portfolio of Gerd Kommer: invest with security with the ETF appeared first on Gerd Kommer.

]]>What is actually a “global portfolio”? Chiunque si occupi di investimenti passivei No other language document is available in the first place or in the “global portfolio”, introduced by Gerd Kommer on 20 years ago. What are you doing in real life? Are you presenting a concrete global portfolio? E another lei ne ha bisogno? Troverà le risposte a queste domande in questo articolo del blog.

Prima di iniziare, diamo un'occhiata alla terminologia: The global portafoglio is not a single portafoglio composto da ETF or indici specifici, ma a concetto di portafoglio with cui ogni investitore può constructuir a global portafoglio personalizzato in base alle proprie esigenze e preferenze personali.

In this article of the blog the quality of the principles is based on the concept and comes into practice.

(1) I am one of the scientific pioneers based on the global portfolio concept

The conoscenze scientifiche fundamentali da cui deriva il concetto di portafoglio global provengono da quattro economisti americani, tutti vincitori del Premio Nobel per l'economia (in momentsi diversi) per i loro contributi rivoluzionari all'economia finanziaria or alla macroeconomia:

- James Tobin (1918-2002). Ha formulato the “Theorem of Separation of Tobin”. The theory relates to the “portafogli ottimali” sono composti da due soli elementsi fundamentali: a part of the portafoglio “priva di rischio” (a basso rischio) and a soggetta a rischio.

- Harry Markowitz (1927 – 2023). Ha dimostrato per la prima volta come constructuire a “portafoglio ottimale” composto da singoli asset which rappresentano the migliore combinazione possibile dal point di vista matematico tra rendimento e rischio.

- William Sharpe (NATO nel 1934). The ricerca has portato alla distinction between rischi “sistematici” and “non sistematici” (or “idiosincratici”). I have idiosyncratic characteristics that are “diversified” and that there are no statistical compensations from the capital market that attracts additional returns. Solo i rischi sistematici do not have the possibility of being more diversified. Pertanto, dal point of view statistico, gli investitori possono aspettarsi dal mercato una compensazione del rendimento solo per i rischi sistematici e quindi dovrebbero includere nel proprio portafoglio solo questi rischi.

- Eugene Fama (nato nel 1939): The efficiency of the market, secondly the quality of the market and in other financial markets, a cause of “efficienza information”, is probably impossible to achieve a benchmark passivo in termini di costs e rischi in modo systematico (non solo casuale) use only the information available to the public. Fama is also a pioneer of factor investing (in the 9th section).

To use the scope of the Quattro Superstar dell'economia and the other ricers of the Alto Livello come private investors, it is not necessary to compare the details of the mathematical and statistical elements of the modern cosidency of the portfolio. È sufficiente conoscere the conclusions concettuali principali. Questo post del blog si propone di fornire aiuto in tal senso.

(2) The global portfolio of Dott. Gerd Kommer: una breve definition

The global portfolio is based on the results of the ricerca sopra citati and the other in a concept of investment “complete” and “completely integrated”, ie

- gli investitori privati normali (a difference between the investitors established)

- possono mettere in pratica effettuando investimenti in regia propria

- with investment products available on the retail market

- a basso costo

- with importi d’investimento piccoli or grandi

- e with a dispendio di tempo minimo

- for the constitution of the patrimony in a long term or the preservation of a patrimony of the past

existed.

This is a schematic diagram based on the concept of the global portfolio, which is realistic and realizable in a long-lasting manner (per day of life) for normal investors in familiar nuclei. In terms of the quality of investors in global portfolios, it is not necessary to have fanatics about the wallet, which means that the ore of all the financial questions.

The portafoglio does not have to be integrated and adapted in a fashionable way, come raccomandato dalla scienza, alla reddituazione reddituale e patrimoniale di un investitore nucleo familiare, durante tutta la adult vita con tutti i suoi cambiamenti e also durante the critical crisis.

Comer has name and description for the first voltage of the global portfolio concept in 2001 in this book“Investing worldwide with funds” (Solo Edizione Tedesca). A year ago, in 2002, it was published as the first edition of this successful bestseller“Invest confidently with index funds and ETFs” (Solo Edizione Tedesca). All'initio il libro è rimasto sugli scaffali delle librerie come un mattone. Tuttavia, with the introduction of the Grand Financial Crisis in 2007, the book was sold by Hanno iniziato ad aumentare. In 2016 the book received the financial book award from Deutsche Börse AG and Citibank.

Ad oggi sono state sells around 300,000 copies di Invest confidently e di versioni semplificate più brevi. This edition of the book, which was published around the same time in 2017, is also a blog that dates back to 2017, and has continued to expand the concept of the global portfolio in a modern and evolving way.

In Invest confidently (Investire with security), the concept of the global portfolio is derived from the science and description. This can be used to define the global portfolio with the most important keys:

The term of the global portfolio indicates a portfolio of investment components due to the principal components: a part of the portfolio “ad alto rischio”, responsible for the generation of the total portfolio (the “motore di rendimento”), and a part of the portfolio “a basso rischio”, which funge principalmente Ancora di stability and security in the total portafoglio. Entrambe the part of the portfolio sono altamente liquide. Altri aspetti and characteristics fundamentali sono: (a) global diversification and elimination of the individual assets and default assets, (b) Buy and Hold discipline and coercion, integrating the rebalancing based on the regulation to eliminate the delay in rendiment and the cost of opportunity (utili persi) derivanti dal timing, nonché l'onere fiscale effettivo, (c) riduzione dei costi attraverso l'uso di fondi indicizzati ed ETF a basso costo e (d) riduzione dei rischi di contraparte ad es. The part of the bank, the other parts of the financial services and the financial products are in a level that is not as long as possible.

Le parti (a) e (b) della definition implicano l'importanza di evitare investimenti attivi basati su previsioni, poiché questi, dal punto di vista scientifico, producono combinazioni rischio/rendimento poco interestingi. The investment in the market of the capital is based on the selection of titoli, the market timing or a combination of entrambe le cose. The investment attivo, nelle sue infinite forme individuali, “è ciò che fanno tutti”. The global market quota is superior to 95%.

Nella parte restante di questo post del blog, esamineremo i requisiti di vero portafoglio global secondo Gerd Kommer e mostremo, sulla base di prodotti e concreti solutions, come potrebbe essere a portafoglio di questo type nella sua più semplice.

(3) The southern division of the portafoglio in a part of a rischio and a basso rischio (“allocazione level 1”)

As a prospettiva aerea, the global portfolio is divided into a quota of portafoglio rischiosa (“RBT”) and a quota of portafoglio “priva di rischio” (a basso rischio) (“RFT”). The quota di portafoglio rischiosa is il motore di rendimento Responsibility of the generation of the return of the portafoglio, according to the quota of the portafoglio priva di rischi funge the “ancora di sicurezza or di stability” nel portafoglio. Chiamiamo questa dicotomia allocation level 1.

Per quanto riguarda the ripartizione tra quota di portafoglio rischiosa and quota di portafoglio priva di rischi, sono possible to combine the 100% quota di portafoglio rischiosa/0% quota di portafoglio priva di rischi (“portafoglio 100/0”) fino a 0% quota di portafoglio rischiosa/100% quota di portafoglio priva di rischi (“portafoglio 0/100”). A global portfolio of 100/0 has the return at the highest level, but also for certain fluctuations (which are volatile) at a rapid pace. Contrary to this, a portfolio of 0/100 ha is available at low speed, but also has a minimum flooding at a minimum speed. Nella pratica, for the maggior parte degli private investors la musica suona da qualche parte nel mezzo, poiché solo buti preferiscono the allocazioni marginali.

In a version of the global portfolio, the quota of the global portfolio is constituted by one or more funds indicizzati/ETF that belongs to the global market. The class of investment (class of asset) is the class of asset with the return on a long term basis, superior to the corresponding returns on real estate, obligatory, material prime, metallic prices or oggetti in the collection or products of financial derivatives of this class of assets or products of financial products correlati, come ad es. depositi bankcari fruttiferi, assicurazioni sulla vita a capitalizzazione or hedge fund. (Le partecipazioni in private equity hanno rendimenti statisticamente simili a quelli delle azioni, sono più rischiose and illiquid)

It is not the case that the quota of the private portfolio of Rischi contributes to a significant return over a long period of time, as the net cost, the impost and the inflation, but also have a cap on its main function ancora di stability. Really positive returns are significant in the net cost and imposition of the same status in passing and potranno essere ottenuti in the future.

The quota of the private portfolio of Rischi is constituted by the obligations of the state and the obligatory societies of altamente liquide with (a) breve durata residua (e quindi poco rischio di variazione del tasso d’interest), (b) basso rischio di credito (e quindi rischio di default difficilmente riducibile) e (c) nessun rischio di cambio.

Per the quotation of the portfolio of the bank with a value of 100,000 euros, you can also use a current account in a bank account, but this is imported by a combined bank-client and is also guaranteed by legal deposits (statal).

(4) Libertà di previsione and massima diversificazione global

A vantaggio essential del concetto di portafoglio global è che, a difference of the strategy d'investimento attive or the products finanziari gestiti attivamente, non richiede previsioni, ossia non richiede previsioni sul corso del titolo, sulle variabili economiche (ad es. tassi d'interest, inflation, crescita economica) or su Other sviluppi della società, della politica e dell'economia che influenzano il mercato azionario.

The science in this regard, in the major part of the capital, is not possible in the economic previsions, which are fruitful in the market of the capital. The then-derivante dal seguire the major parte delle previsioni guess supera il beneficio derivante dal seguire the minoranza delle previsioni corrette.

The previsions of investments are definitely considered in one or two of the following phases of investments:

- azioni singole (stock picking);

- singoli Paesi, settori o argomenti;

- singoli gestori del fondo o “guru”;

- singoli periodi di tempo (market timing);

- l’andamento dell’economia o dei tassi di interest; oppure

- la politica monetaria delle bankche centrali

If you want to be able to see the bottom of the article in the blog “The motivation behind these investments is non-functional“.

In breve: tali scommesse rappresentano rischi negativi perché evitabili (“diversificabili”) che non vale la pena correre in assenza di una compensazione prevista (sotto forma di rendimento atteso). Pertanto, è opportuno rinunciare a previsioni di qualsiasi type, soprattutto when si tratta di importanti questions come la previdenza per la vecchiaia. Questo obiettivo può essere raggiunto concentrandosi sull’intera Economia di mercato, vale a dire sulla massima diversificazione globale sul Buy and Hold. Per quanto riguarda le azioni, it is possible to realize the acquisition of a fund of indicia/ETF and also the rifletta il mercato azionario global.

(5) Buy and Hold & Rebalancing

The Buy and Hold (B&H) is a principle of the basis of the concept of the global portafoglio altrettanto importante quanto l'assenza di previsioni e la diversificazione global. Il B&H (a) ridduce il carico di lavoro e i costi (in particolare riducendo al minimo i costi di acquisto e vendita), (b) abbassa l'onere fiscale effettivo in un sistema fiscale come quello tedesco e (c) eliminate il potentiale theno ai rendimenti derivante da decisioni di timing sbagliate and guide the emotions. Queste sono particolarmente probabili tra gli investori privati, come hanno dimostrato più volte the ricerca sulla finanza comportamentale (economia comportamentale) and the ricerca empirica sui mercati finanziari.

As part of the global portfolio, the B&H is collegato with rebalancing. The rebalancing is the ripristino, secondo regole prestabilite, the ponderazioni percentuali desiderate (ponderazioni target or teoriche) di butte le positions in a portafoglio nel corso del tempo, dopo che queste si sono “allontanate” dalla struttura target precedentemente scelta consapevolmente a causa degli effetti del mercato. Questo “allontanamento” is verificherà inevitabilmente prima or poi nella pratica and not contraddice il concetto di buy and hold. The motivation is the sense of rebalancing, the composition and the conseguenza of the combination of rischio/rendimento in a portafoglio cambierebbero nel tempo a causa delle oscillazioni di mercato, allontanandosi the reali preferenze of the investors. The rebalancing is also a special form of investment anti-cyclic (“contrario”) second to the principle “sell high/buy low”.

(6) Riduzione dei costsi

A parità di condizioni, i costi riducono il rendimento net rendimento di an investment, ovvero il rendimento che conta davvero. I cost Hanno an effect simile a quello dell'effetto dell'interest composto negativo.

The estimated value is: with an initial capital of 5,000 euros, a return in the middle of the year of 10% and the cost of 0.5% all year, the final value of the patrimony being 30 years old and 76,000 euros. The annual cost is 1.0%, the final value of the patrimony is approximately 66,000 euros, over 10,000 euros in meno, pari a quasi il 15%.

At the moment, the cost of the investment is just one of the most influential investments in the world, and it has a high degree of certainty e controllo, vale particolarmente la pena esercitare tale controllo.

Inoltre, the vecchia regola generale secondo cui “una superior quality costa di più” non si applicagli investimenti. The opposite is true: the investments are made at low cost, including the hedge fund, and the funds for the life of the capital, but also with low returns.

(7) Eliminazione dei rischi di controparte legati in processi e ai products finanziari

A part of the total voltage trascurata del concetto di portafoglio global è the coerente elimination of the rischi di counterparty legati in processi e ai prodotti finanziari che accompagnano the maggior parte delle forme di investimento attivo. Cosa intendediamo con questo?

Molti prodotti finanziari, ad es. The investments in the life of the capital, the pensionable private investments, and certificates, several investments in private equity, the investments in hedge funds, the investments in the funds, the investments in the Alcune stock exchange of cryptocurrencies and the investments in P2P credit, as well as the associations counterparte (tipicamente trascurati). In other words, there is a contradiction in the question of whether there is a difficult economic situation or additional fallout, the investor's interest is in part or complete. The value of the bank deposits is also superior to the guaranteed deposits of up to 100,000 euros per combination of the bank client.

In line with the principle, the concept of the global portfolio, the opposite is not the case, but (a) in the indices/ETF, a difference between the products and the financiers mentioned above, which constitutes the giuridicamente of the cosiddetti patrimony speciali e (b) the case of a bank deposit, the bank agisce solo come depositario e non come debitore, come the case of a bank deposit.

(8) A simple graphic representation of the concept of the global portfolio

The seguente panoramaica mostra a semplice graphic illustration of the general structure of the base of a global portafoglio.

(9) Optional: The global portfolio in the variant of factor investing

Come components are optionally worth considering, in the construction of a global portafoglio it is possible to account for the cosiddetti premium di fattore. I premi di fattore sono characteristic of the titoli che consentono di aumentare il rendimento atteso (ovvero il rendimento medio statistico) di a portafoglio rispetto al mercato totale. At the end of 100 years approximately, with the factor investing (used due to the premium of the fattore) it is intended to have a higher return on the percentage of the entire year, with a source from the “normal” market (the total market), with a similar term in terms Volatilità (fluttuazioni di rendimento).

I premi di fattore più noti sono

- The prize is Small Size: Le piccole imprese, misurate in base alla loro capitalizzazione del mercato, tendono ad avere rendimenti migliori rispetto alle grandi imprese.

- The premium value: Le imprese con valutazioni favorevoli (ad es. misurate in base a indicatori quali il P/E) tendono ad avere rendimenti migliori rispetto all imprese con valutazioni elevate (“costose”).

- The premium quality: The imprese with a basso indebitamento and an'elevata redditività (ad es. margine di profitto operativo) hanno rendimenti medi a longo appointments migliori rispetto alle imprese all'altra estremità dello spettro (aziende di bassa qualità).

- The Momentum Prize: The action of Hanno avuto rendimenti nettamente superiori alla media negli ultimi dodici mesi tenderanno a continuare così per altri tre-sei mesi prima di tornare alla media or al di sotto di essa.

- The premium low investment (chiamato anche premio Low Asset Growth): the imprese che nel recente passato hanno registrato una crescita del totale di balance inferiore alla media (“parsimoniose”) tendono a generare rendimenti azionari più elevati rispetto alle imprese con una crescita del totale di balance sheet elevata (“spendaccione”).

The premium of the fattore diventano is clearly visible in the long term and the period of preservation or the period of investment. The title is illustrative: in the period of storage during the year, the market has a statistic and a return superior to zero at 53% of the cash (years). The period of storage is this year, the indicator “percentuale di rendimenti superiori allo zero” is at 93%. A regulation similar to this is also per i rendimenti supplementari derivanti from the first fattors.

For the purposes of factor investing, it is important questo post del blog.

(10) Possible solutions for global portfolios

In this case, a global portfolio is realized with an ETF for the part of the portfolio in a rischio and a part in the lower part of the rischio. For an investor who wants to allocate a level of 1 100/0 or who wants to use the current account's ambition for the guarantee of state deposits per the quota of the private portfolio of Rischi, it is sufficient for a single ETF.

Nella in this form is a simple example, a portafoglio di questo type potrebbe apparire come segue (aggiornato a luglio 2023):

- Quote from portfolio rischiose – Azioni globali: L&G Gerd Kommer Multifactor Equity UCITS ETF (ISIN: WELT0A) o SPDR MSCI ACWI IMI UCITS ETF (ISIN: A1JJTD)

- Quotation of the portafoglio prive di rischi - obbligazioni a breve appointment with elevated rating creditizio and senza rischio di cambio: L&G Corporate Bond ex-Banks Higher Ratings 0-2Y ETF (ISIN: A40E7Q) e/o Xtrackers II Germany Government Bond 0-1 UCITS ETF 1C ISIN: DBX0T8). Come accennato in precedenza, the part of the portafoglio a basso rischio può essere rappresentata in alternative also tramite a current account presso una bank, a condition che the importo d'investimento in conto current rientri nella guarantee sui depositi statale di 100,000 euros per combination cliente-banca.

| Disclaimer importante: This is not an indication of the investments made, but only an illustration comes from it potrebbe Facilmente attuare il concetto di portafoglio global. The quota of the private portafoglio of rischi is not “priva of rischi” in the sense of the letter of the dates. Autonomous information and detailed information on the product documents before making a decision on the investment. |

Conclusions

The global portfolio is an approach to fully integrated investments, derivato dalla scienza, che consente agli investitori di effettuare investimenti patrimoniali orientati al longo appointments e based sul mercato dei capitali per the constitution of patrimonio and its conservation.

The global portfolio concept is implemented in an autonomous manner or with delegated investments. A fine use of Gerd Kommer's books, his blog was published in 2017, his YouTube channel and other publications, collegiate and Gerd Kommer's newsletter.

Further information on the concept of the global portfolio

Post of the blog:

Kommer, Gerd; Weis, Alexander (2019): “Factor Investing – the Basics”; post on blog; maggio 2019; link: https://gerd-kommer.de/it/blog/factor-investing-le-basi/

Kommer, Gerd; Weis, Alexander (2020): “The motives for investing in investments do not work well”; post on blog; February 2020; link: https://gerd-kommer.de/it/blog/dieci-motivi-per-cui-gli-investimenti-attivi-non-funzionano-bene/

Weis, Alexander; Gschichtmann, Selina (2022): “Passive investing – the basics”; post on blog; September 2022; link: https://gerd-kommer.de/it/blog/investimenti-passivi-le-basi//

The post The global portfolio of Gerd Kommer: invest with security with the ETF appeared first on Gerd Kommer.

]]>The post The ETF by Gerd Kommer appeared first on Gerd Kommer.

]]>If you use the ETF in the same language area, you don't have to deal with a person in particular: Dr. Gerd Kommer. For 23 years, the guide has been written on the topic “Investments with funds indicated by ETFs” and for 30 years it has been operating in financial terms. Gerd Kommer is not only a retailer of private investors in the area of lingua tedesca l'investimento senza previsioni and based on the regulation of the foundation of scientific consolidation, coniando a tal fine il termine “portafoglio global”. Questo approccio d'investimento, realizzabile with gli ETF, è diventato semper più popular negli ultimi anni tra gli private investitors of the paesi di lingua tedesca grazie al suo concetto convincingnte, al suo rendimento atteso interesting a long appointments and all a sua facile implementation, also with denominazioni simili come “Weltdepot” or “Welt-AG” and in the form of implementation of leggermente modificate.

The global portfolio is not a combination of ETFs or specific titular indications, which is a global coercion of the investors that can be adapted in a flexible manner to all the properties and specifications specific to Victorinox. Tuttavia, from the point of view of an investor, this flexibility can also be achieved with completion or great carico di lavoro.

In June 2023, a solution for DIY investors will be launched:L&G Gerd Kommer Multifactor Equity UCITS ETF, which in this article of the blog was written “Gerd-Kommer-ETF” per brevità. This is how important the characteristics of the Gerd Kommer ETF are.

Questa pubblicazione ha finalità di marketing. You should read the prospectus of the background and the information provided by the investors before making a final investment decision.

1 Characteristics of the base

The Gerd-Kommer-ETF is an ETF that is purely based on the part of the portfolio that is part of the global portfolio concept in a unique fund, called a “soluzione 1-ETF”. Per “componente rischiosa del portafoglio” si intendede qui il “mercato azionario global”. This is why we want to invest in a “level allocation of 1 100/0” for the future (100% in rischio / 0% in basso rischio) without the previous ETF or the Gerd Kommer ETF. The aim is to adopt a conservative approach (orientated towards safety), with a level allocation of 1 di “90/10”, “80/20”, “70/30” etc. fino a “10/90”, you can combine the Gerd-Kommer-ETF with an ETF obbligazionario or take the part of the bottom of the portfolio with a current fruit bank account. The ETF is obligatory to be used by the owner, including the duration of the residual debt, with an elevated credit rating based on the local value of the investor. For the reasons of the loan, the balance of the current account is not above 100,000 euros, the maximum limit of the guarantee on deposits in Germany.

2 Società d’investimento (KVG)

The Gerd Kommer ETF is the foundation of the ETF Legal & General Investment Management (“L& G “). L&G part of the British Legal & General Group (“L&G”), one of the largest companies in Europe. L&G is one of the principal asset managers (patrimonial managers) of the world. In December 2022, the patrimony of L&G was worth approximately 1,300 billion euros. A metà del 2023, L&G offers almost 50 diversi ETF sul mercato tedesco.

3 Indice azionario sottostante

The indication based on the Gerd Kommer ETF is the same as Dott. Gerd Kommer and his team in collaboration Solactive AG e L&G November 2022 and 2023. Solactive It is a fornitore di indici tedesco based on Francoforte. The indication of the riferimento is based on the indication and denomination Solactive GBS Global Markets Investable Universe USD Index NTR (ISIN: DE000SL0EM79) and the index is based on the Gerd Kommer ETF in chiama Solactive Gerd Kommer Multifactor Equity Index NTR (ISIN: DE000SL0G219). [1] The index is from the global market, the “Welt-AG”, and it is also directly paragonable to an ETF from the noto index MSCI ACWI. Tuttavia, the Gerd Kommer ETF is discosta consapevolmente e in modo significativo da an ETF MSCI World in alcuni punti importanti descritti di seguito. [2]

4 “Principio All-Cap-All-Market”

A difference in an ETF MSCI World, the Gerd-Kommer-ETF also includes other aspects of the emerging landscape in different dimensions regional e small cap (azioni secondarie) nella dimensions. This is the same as the “All Cap All Market ETF”, which is part of the international market. The MSCI World, however, does not take into account the actions of the emergent countries and the small cap.

5 ponderazione per paese

The Gerd Kommer ETF costs almost 50 paesi (rispetto ai 23 dell'ETF MSCI World [al giugno 2023]). The ponderazione di a single Paese nell'indice è determinata per il 50% dalla sua capitalizzazione del Mercato e per il 50% dalla quota del Paese nel prodotto interno lordo global (performance economica global). In this case, in this case, the focus of the concentration is not on the Stati Uniti, which is the indication of MSCI World (situated in June 2023 with a higher US rating of 67%), although it is worth noting. Controversially, the emerging countries and the major part of the industrialized countries are not static but have a higher elevation.

6 Forma di replica dell’indice

The Gerd Kommer ETF is an ETF a replica fisica, but not an ETF on swap (ETF sintetico). This guarantees that the indication of the situation is as good as possible and that it is not sussista alcun rischio di contraparte sotto forma di banca. The replica technology is based on the Optimized Sampling (Optimized Sampling) approach and has a fine limit on the number of possible costs in the background.

7 Utilization of dividends

The ETF is available in a class of quote a capitalization (ISIN: WELT0A; ISIN: IE0001UQQ933) and in a class of quote a distribution (WKN: WELT0B; ISIN IE000FPWSL69), al fine di soddisfare le diverse esigenze degli investors.

8 factor investing

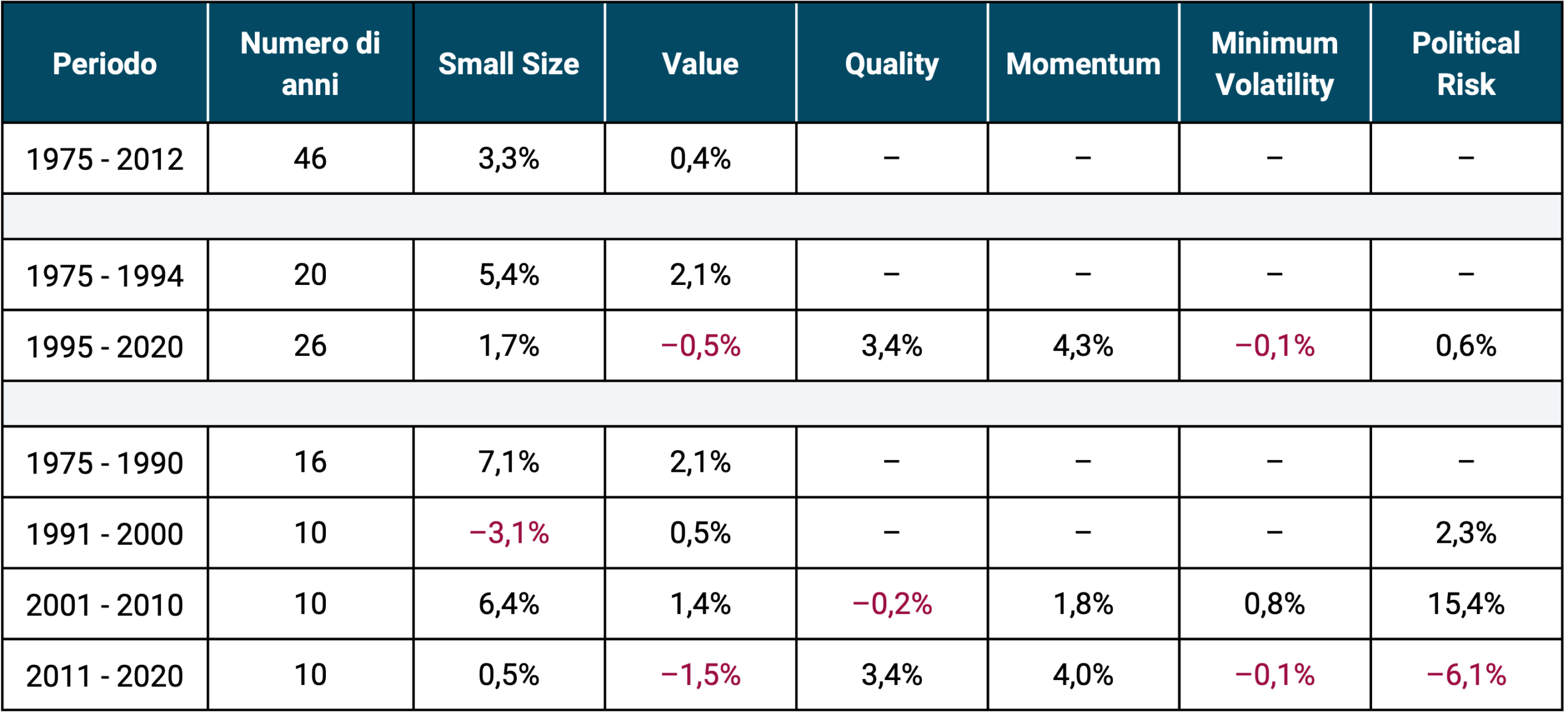

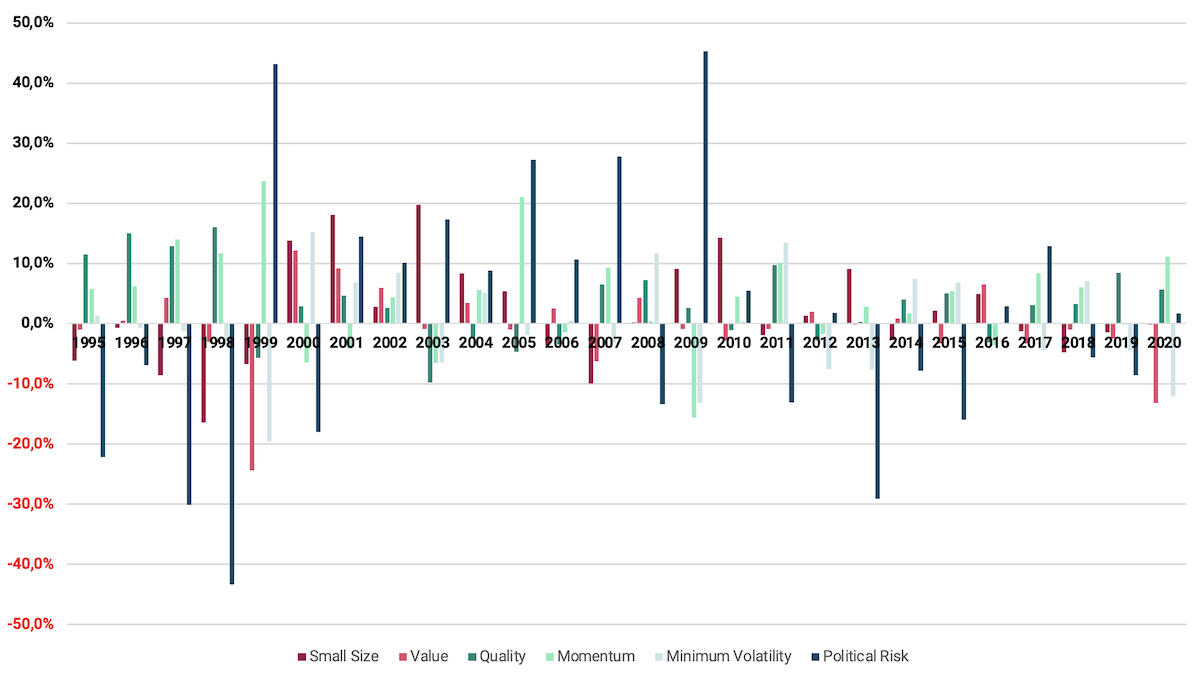

The Gerd Kommer ETF is one ETF multi-fattore The sovrapondera i cosiddetti “premi di fattore” rispetto a un indice azionario passive neutrale rispetto al mercato (“plain vanilla”). [3] The factor investing is also another factor Smart beta investing. I premi di fattore sono characteristic delle azioni identificate dalla scienza che hanno a correlazione sistematica e statistica with the rendimento e il rischio and the cui sovraponderazione in a portafoglio azionario dovrebbe generate a rendimento supplementare a longo appointments rispetto a un portafoglio neutrale rispetto al mercato. I premi di fattore presenta nel Gerd-Kommer-ETF sono:

- Size: The images of the imprint, based on the capitalization of the market, have a rendimento atteso statisticamente più elevated rispetto all the azioni di grandi imprese.

- Value: The values of the cui prezzo è basso rispetto a determinati indicatorsi aziendali (ad es. utili or patrimonio netto contabile) Hanno a rendimento atteso statisticamente più elevato rispetto ad zazioni altrimenti identiche in cui ciò non si verifica. In other words: the “Economic” (Value) value has a higher value than the “cost” source (elevated value), the Growth or Crescita value.

- Quality: The analysis with a redditività superiore alla media, a crescent rotation of the capital and/or a low level of indebitamento Hanno and rendimento atteso statisticamente più elevato rispetto ad zazioni altrimenti identiche che non presentano these characteristics.

- Investment: The results with a total amount of the balance sheet content can be returned at the same time in an elevated statistical manner.

- Momentum: The results are not recorded at the end of the month and are registered in a superior way in the media, according to a short period of time and return at the same time in statistical terms, with a high level of rispetto of all the items recorded by Hanno in the same period.

- Political risk: The actions of the emergent countries, participatory in the “politico world”, are now a rendimento atteso statisticamente più elevato rispetto a quello of the actions of the Paesi industrializzati.

The purchase of the premium of the fats has the opportunity to generate a supplementary return (including the net cost) and an ETF neutral risk in the market in long dates.

The case of the Gerd Kommer ETF is part of Multifactor Investing integrate, in quanto all this premi di fattore presi in considerationazione sono rappresentati in us singolo Indice anziché in più indici individuali. In this case, the theory is that it is possible to interact with each other in the first place of the fattore. In other words, the fat should determine the premi di fattore hanno and the effect will be strong in combination with other piuttosto che “da soli”. Questo vale ad esempio per Size e Value O Size e Quality.

For more diversification, I get the better fat Size, Value e Quality vengono ottenuti adeguando the rispettive ponderazioni delle azioni. The aim of the rebalancing trimestrale, in which the fattori vengono considerati in modo equamente ponderato.

Per quanto riguarda i premium Momentum e Investment, using a special technology for screening to ridurre al minimo the rotation of the titoli (turnover) associata all'utilizzo di questi due premi and i costi di transazione da so generati.

The prize for political risk deriva dall'adeguamento delle ponderazioni dei paesi al prodotto interno lordo già prima dell'ottimizzazione.

I premi di fattore sono volatili, ovvero flutuano nel tempo, proprio come i rendimenti azionari in generale. In other words: I give the fat to you non-permanently (it is not verified this month or year), but I can also change the “bonus” to the “malus” in the period of tempo prolungati. Be the first of the fattors fossero continui (cioè “garantiti”), sarebbero stati da tempo arbitrati, ovvero resi soì “costosi” dalla forte domanda da non offer più alcun vantaggio di rendimento.

For the purpose of approving the argument of the factor investing, the following is written in this article of the blog: “Factor investing – the basis”.

9 Elevata diversificazione (“ultradiversificazione”)

Nonostante si tenga account of the premiums of fattors and the filters ESG, which tends to be ridurre of the universe of investment, the index is around 5,000 titoli singoli (su around 10,000 shares in each segment of the Prime Listing Standard of the stock market of the quasi 50 paesi considered). There are approximately 5,000 single entries, the Gerd Kommer ETF selects over 4,000 single items in an optimized sampling procedure (optimized sampling procedure). With the volume of the fund in the ETF, this number is also available. The ponderazione massima di una singola azione nell'indice è limitata a value massimo dell'uno percento in ogni data di adeguamento, in modo da evitare a “eccesso di ponderazione” (a quota superiore al 10% delle dieci azioni più grandi, which is in molti altri ETF su indici azionari globali). Thanks to the special method of considering the two descritto sopra, there is also a great diversification in the past and the ETFs are traditional.

10 filters for sostenibility leggeri

The Solactive index based on the Gerd Kommer ETF includes an ecological filter (screen) centered on the elimination of CO emissions2. This is fine, including 3% of the emissions from CO2 più elevate negli undici “settori principali”. Sono inoltre escluse the aziende che violano the norm of the Nazioni Unite, which commettono the più grave violazioni della sostenibilità (“Severe ESG Controversies”), which produced armed controversy and i producers di carbone. [4]

11 Ulteriori criteria di exclusionee specifici delle aziende

The scientific researcher has dimostrato che determinati tipi di azioni or costellazioni di azioni presentano combinations rischio/rendimento statisticamente poco attraenti. The figure of the company's actions is based on the company's initial public offer (IPO/Initial Public Offering) only recently and the quality of the prestige title is quickly raised to the market. [5]

12 Prestito titoli

At the moment (a year 2023) the Gerd Kommer ETF does not work in its title with the content of the ETF.

13 Data for ricostituzione dell’indice and rebalancing

In three months, the rical data and components of the loro ponderazione dell'indice sottostante and the azioni che non soddisfano più i criteri dell'indice vengono sostituite con quelle che ora li soddisfano. Laddove gli ulteriori requisiti dell'indice non sono più pienamente soddisfatti, this rebalancing based on the regulation guarantees that this is new.

14 Vigilance and protection of investors

The Gerd Kommer ETF is a cosiddetto fundo UCITS, over a fundo d'investimento liberamente authorizzato alla distribution agli investitori privati all'interno dell'UE. I found the investitors present a special patrimony, separating the point of view of the financial and infrastructure of the patrimony of the Società d’Investimento (L&G). A fallimento della società d’investimento non avrebbe alcun effetto negativo sui fondi degli investitori. Allo stesso modo, the investor does not corre alcun rischio di insolvenza bancaria in relazione al deposito in cui the quote dell'ETF sono custodite presso the banca dell'investitore, dal momento che la banca svolge solo il ruolo di depositaria per i valori in deposito (which is an'importante differencea giuridica rispetto a un accountto bancario and a un deposito bancario). Inoltre, si applicano all i requirements normativi in materia di gestione del rischio e protection degli investitori previsti da normativa UCITS.

15 costs

The cost of the ETF (“TER”) is always 0.45% all year, which includes the return of the ETF and also compensates for the return, but the automatic use is guaranteed.

The cost of the Gerd Kommer ETF is also paragonabili to the other ETF multi-fattore or portfolio portfolio and is drastically inferior to the conventional funds. It is possible to confront a single part of the ETF, based on the MSCI World index, at the moment the Gerd Kommer ETF offers both functionality and completeness.

Siamo convinti di offer a prezzo equo per il Gerd Kommer-ETF, dal momento che oltre a un approach multi-fattore integration e a un'ultradiversificazione, offering a ponderazione per paese innovativea che tiene conto della performance economica, cosa unica in Germania.

16 Availability

Gerd Kommer's ETF is in quota on XETRA from 21/06/2023 and is available from the main bank and broker in Italy.

17 Idoneità al piano di risparmio

18 Importo minimo dell’investimento

Not è previsto a minimum import of the investment.

19 Ultimate information

All marketing information is available on the web of the ETF (https://gerd-kommer.de/it/etf/). The legal information is available from the background and the information provided by the investors (KID), also available on the website sito web of the store of the fondo L&G. Before you leave this document you have to make a final investment decision. This is interesting in all the technical structures of the index in detail methodology of the index (Index Guideline) in lingua inglese.

Conclusions

L'L&G Gerd Kommer Multifactor Equity UCITS ETF It is a solution that is comfortable and efficient to implement the Dott global portfolio concept. Gerd Kommer in a unique solution ETF, possibly in this case a deposit from a bank fruit bank or an ETF obbligazionario to represent the part of the bass portfolio of the global portfolio, which is desidera.

With the Gerd Kommer ETF, the investor is responsible for the initial rice and selection of the single ETFs, but also for the initial impostation, the rebalancing periodically. The investor has inoltre la certezza che il concetto di portafoglio global nella variant del factor investing sia stato implementato da esperti.

With the Gerd Kommer ETF it is possible to initiate with qualified import of investment and/or structure containing a male patrimony with a piano accumulo ETF.

Final note

[1] “GBS” by Global Benchmark Series, “NTR” by Net Total Return, “ISIN” by International Security Identification Number.

[2] The confrontation and returns of the funds or other indices are based on the value of the USD (USD on the index, the EUR on the ETF of the Euro area) and are identical to the data on the return of the confrontation. All of this modo, it is necessary to ensure that the dividends are considered in the same way as the total return (indici total return) and to verify the dividend in the same state, if any, in the font (variant of the index of total return net rispetto all the variant of the index of total return of Lord). The Solactive index is a total net return indicator. The ETF is based on certain information.

[3] The dates “neutrale rispetto al mercato” are not used in the sense that they have an accademic economy, but also have a neutral orienting sense in the ponderazione delle azioni, which deriva esclusivamente dalla loro capitalizzazione del mercato.

[4] “ESG” sta per Environmental, Social, Governance nel contesto dei criteria di sostenibilità.

[5] In this case, based on this criterion, the Wirecard system is definitely an indication of the primary value of the card.

The post The ETF by Gerd Kommer appeared first on Gerd Kommer.

]]>The post Investimenti passivi: le basi appeared first on Gerd Kommer.

]]>Questo articolo del blog è a breve introduzione all’investimento passiveo. You offer a panoramic sintetica sull'investimento con ETF and this desidera orientarsi rapidamente sull'argomento.

The article is presented in a conoscenza di base del mercato azionario. It is significant that it is necessary to have a general idea of the same language, a commitment and an ETF and also have a conoscenza di base di concetti come rendimento e rischio. (Chi desidera rinfrescare le proprie conoscenze in materia può consultare il nostro Glossary, in what we see in technical terms that are important in the field of patrimonial investments).

In a first phase there is a panoramic view of the principal forms of investment, in a second phase there is an illustration of the return and the investment. Successivamente affronteremo the domanda cruciale dell'investimento ("voglio essere un investitore attivo or passive?") and mostreremo perché l'investimento passiveo è l'alternativa migliore agli approcci attivi. Infine, presenteremo a “ricetta” for a portfolio passive composto da soli due ETF: this is exactly what it is.

This is familiarity with the basis of the passive investments, consigliamo il nostro articolo del blog un po’ più avanzato “Factor investing – the basis”.

Lei è convinto dell’investimento passive e vuole metterlo in pratica in modo semplice e comodo? Abbiamo the solution 1-ETF di Gerd Kommer: l’L&G Gerd Kommer Multi-factor Equity UCITS ETF. Per saperne di più >

Iniziamo!

Classi di asset – una panoramica

Per evitare malintesi, ecco una premessa: in this articolo ci occuperemo esclusivamente di attività liquide, ovvero escluderemo tipi di attività come il capitale humano, the partecipazioni societarie or i diritti pensionistici. The ragioni sono due: in primo luogo, the dibattito attivo-passivo è irrilevante per la maggior parte dei tipi di patrimonio illiquido, perché alla fine possono essere gestiti solo attivamente, and in secondo luogo, ciò andrebbe oltre lo scopo della nostra piccola introduzione.

What is the asset class? The classi di asset (classi d'investimento) also has a logic for attività and is also relatively similar in terms of return, balance and liquidity.

This is a panoramic view of the most important asset classes:

- Azioni: partecipazioni azionarie in società quotate in borsa

- Obligations: credit negotiations in the stock exchange of Stati or Società

- Real estate: residential and commercial properties

- Matter prime: natural sources come from petroleum, metal base or prime agricultural matter

- Metallic prizes: sotto group of the prime matter (come gold, silver or platinum)

- Other collections: art, luxury cars, luxury watches, vintage wines, etc.

- Criptovalute: Bitcoin, Ethereum, Tether, ecc.

Queste sono the classi di asset in cui è possibile investire come privato investor with a sforzo accettabile and a costi ragionevoli.

Contrariamente a quanto si crede, the deposito bankcario is not a class of asset, ma a prestito non garantito dal depositante all'istituto di credito.

The financial products also come with a capital insurance policy, real estate assets, private equity, hedge funds, investment funds and ETFs that are not in the same class of assets as they are, but only “imballaggi” per vere and ownership of the asset class. Questi “gusci” not sono di per sé negativi and si difference principalmente per il loro spessore, con gli hedge fund (spessi e costosi) a un'estremità dello spettro e gli ETF (sottili ed economici) all'altra. For many finanziari products, the confezionamento comporta non solo costi e perdita di trasparenza, ma also rischi aggiuntivi che the classe di asset non ha nemmeno all'interno del prodotto finanziario stesso.

Andiamo advance!

Rendimento e rischio – Quali sono the classi di asset migliori?

To take a risk in all aspects of the asset class, it is necessary to have the first opportunity to ensure effective investment. Di norma, the risposta sarà: “Ottenere il massimo rendimento possibile with il minimo rischio possibile”. Pertanto, nella Tabella 1 diamo uno sguardo al rendimento e al rischio delle nostre classi di asset principali (le criptovalute non sono incluse nella table a causa della loro storia troppo breve; i mercati da Collezione non sono inclusi a causa della mancanza di dati disponibili):

Table: 1: Returns on long dates according to the inflation of the principal asset classes (in USD) from 1900 to 2021 (122 years)

► Data: Dimson, Marsh, Staunton (2022); Morningstar; David S. Jacks (oro, matter prime) ► Senza costi e tasse (considerati i costi di mantenimento degli immobili) ► Tutti i rendimenti in dollari USA (ad eccezione degli immobili residenziali - vedi sotto) e rendimenti totali (somma dei redditi correnti + aumento del valore) e corretti per l'inflazione ► Rendimenti degli real estate residenziali: periodo di scostamento dal 1900 al 2017 e media ponderata in base alla population dei rendimenti di nove paesi occidentali in valuta locale (motivo: mancanza di dati disponibili), esclusi i costi di transazione che riducono il Rendimento in caso di acquisto e vendita ► “Tempo necessario per raddoppiare”: numero di anni necessari affinché an investimento initial una tantum si raddoppi al rendimento medio dato (senza costi e tasse) ► “Rischio”: deviazione standard dei rendimenti dell’anno solare (volatilità) from 1975 to 2021. For the real estate is not indicative of high value, although the real assets are not available, “ones” and comparisons in the same way with the other asset classes.

If you can't wait in the table? Innanzitutto, if you note that the number is so probabilmente that the lower quantity of the major part is not supported. One of the motives is what the real returns are, over the net dell'inflation. Another motivation is the media, the Internet and the library in general that Hanno has finished with an idea of the realization of realistic results. The number and crudi of the table are the same as in the market for the capital Hanno, which has been produced since the end of 120 years, in terms of performance, illusion and fantasy. If you are still there, you will continue to live with this real thing, but you will not be able to see it further.

In the second luogo, è chiaro che the azioni offrono di gran lunga and rendimenti più elevati tra tutte the classi di asset: the double rispetto agli real estate, due voltage and mezzo rispetto ai titoli di Stato a lungo appointments e sei volte rispetto all'oro e ai libretti di risparmio.

In the third place, the fat of the title of the Stato emerges in accordance with the class of the asset with the lowest weight in assoluto, also in this case with an ample margin.

Is it possible for you to do this? The reason for this is that the massive return to the proprio denaro does not prescindere the azioni. Tuttavia, poiché the major part of the investitors is not in grade or not desidera convivere with the forti oscillazioni delle azioni, an investimento azionario dovrebbe essere integration da un'aggiunta meno volatile. Due to the high intensity of the flooding, the obligation to meet the deadlines of high quality or deposits of fruit banks (purchase the import of the loor without the guarantee of the deposits statale) is also suitable for this purpose.

Questo per quanto riguarda le schermaglie preliminari – ora è il momento di passare all’azione!

Investimenti attivi vs. passivei – la domanda cruciale

The aim is to invest in the property in terms of funds or obligations in the wallet, primarily from the front of all the property, which is in this sense an approach to investing attitudinally or passively. Does this consist of investment assets and passive assets? (Per semplificare il più possibile la questione, ci limiteremo di seguito inclusive all azioni, tralasciando il mercato obbligazionario).

In parole povere, a passive investor acquires the “mercato” (nel nostro caso il mercato azionario). All the best of the year there are quindi il rendimento del mercato (al net of the costs of investment) and it è quindi complete esposto all oscillazioni di mercato. (“Acquistare il mercato” is possible attraverso l’acquisto di uno or più ETF). As you can see in the precedent, the retail market is able to get a 5% annual return on the net inflation, with the control of the impost and cost.

An investitore attivo, invece, not si accontenta del rendimento del mercato e ritiene che sia possibile battery sistematicamente il mercato. Si può cercare di Farlo acquire the azioni che si ritiene avranno andamento migliore rispetto al mercato (“stock picking”) or “entrando” nel mercato ogni volta che è al minimo e ‘uscendo’ poco prima del prossimo presunto crollo (“market timing”). The investment attivo is inevitabilmente always in the form of stock picking, market timing or a combination of entries. It is possible to invest at the same time as an investor in the regia propria with the formula fai-da-te (“DIY”) or have access to a consultant (as a bank or a patrimonial manager).

The crede nell'investimento attivo e non vuole essere un investitore fai-da-te può affidarsi a un gestore del fondo, un patrimonial administrator or a bank, pagando commissioni relativamente elevate, sia aperte che nascoste (difficili da individuare).

For each color, this is also the case in this metafore, which creates the table 2, in which the difference between the investment and the passivo is also illustrated in a very concise and coherent way:

Table 2: The major differences between investments and passives

►Fonte: The easy entry into the world of ETFs by Gerd Kommer

Allora perché investire in modo passiveo?

La risposta breve è: perché è più redditizio.

Questa affermazione non è nostra, ma proviene dal world scientifico. Last year, 60 years ago, the state published a letter from the study of Hanno to improve the statistical superiority of passive investments.

Tuttavia, poiché dal punto di vista di fornitore di servizi finanziari è possibile guadagnare molto di più with l'investimento attivo che con quello passive, the settore finanziario traditional - scienza o meno - offre quasi esclusivamente investimenti attivi.

Also through the traditional media and Internet, the investment investment is much more redditizio, but the story is based on all the investment investments and all the speculative consent of other people, with a high-altitude adjustment or a high-click key, without the voice of the speakers Pubblicitari generate dai fornitori di prodotti finanziari gestiti attivamente.

Le prove scientifiche che dimostrano la superiorità dell'investimento passive rispetto a quello attivo sono in ogni caso letteralmente schiaccianti. Tuttavia, without limitarci a supposizioni, nella nostra argumentation ci riferiamo a un argumento teorico e un empirico tratti dalla scienza e lasciamo che siano i numeri a parlare.

Theoria: L'aritmetica dell'investimento attivo

The calculation of the investments is based on the fact that the devon investors generally complicate the return of the market, according to the definition of the constitution of the market. It is significant that the 50% of the imported investments are generated by an inferior return and the other 50% and a superior return on the returns from the market. È importante sottolineare che si tratta di una necessità matematica che non può essere contestata. It is therefore not necessary to have additional information on the costs, the imposte and the composition or the comportamento of the operators of the market.

Torniamo all’argomento: this is significant – al lordo dei costs (!) – the 50% of the investment investments deve Sovraperformare the market and, vice versa, the 50% deve sottoperformare il mercato. Supponiamo inoltre che l'investimento attivo comporti costi più elevati rispetto all'investimento passiveo - vedi “Costi correnti” nella Table 2 - la percentuale di investitori attivi che battono il mercato deve essere compresa tra lo 0% e il 50%. Pertanto, the probabilità puramente statistica di sovraperformare the mercato è netamente inferiore al 50% and è quindi inferiore alla probabilità di Vincere in a duello a testa o croce. To look at the percentage in real practice, in a collegamento and diamo un’occhiata alla nostra argumentazione empirica.

Empirismo: the outperformer is also affidabili quanto lo zero alla roulette

The practical part of our argument is based on a studio of S&P Dow Jones Indices, one of the major fornitori di indici al mondo, the title is also complicated.Standard & Poor's Index Versus Active", o in breve "SPIVA". The studio confronted the performance of the fond gestiti attivamente with a benchmark passivo equo, consentendo di trarre conclusioni sul successo dell'investimento attivo in diversi periodi di tempo e aree geographical. (Esistono numerosi studi comparabili che giungono a risultati similarili, ma abbiamo The SPIVA studio is one of the most popular versions of the same genre, which has been working for several years since 20 years and is accessible to the public free of charge).

Dallo studio SPIVA can do the main thing due to the conclusion:

- The outperformer is also a minor figure: the percentage of the funds used is at the highest level in the loro benchmark passivo è state in the media of 40% around the region (in industrial areas and in the south) between the end of three years, from 2019 to 2021, and only the 10% around the end of 20 anni, dal 2002 al 2021 (the entity and the number of the fondi sottoperformanti aumenta with the allungarsi del periodo di osservazione). This is the result of all the non-investment in this minor issue, which is the port of the second conclusion.

- Raramente gli outperformer restano tali: the composition of the fondi che riescono a superare the proprio benchmark cambia da an all'altro period in modo più or meno casuale. The greater 25% of the backgrounds were produced in 2017, only 62% and a further 25% in the year 2018; In 2019 the percentual era was 37%; The 2020 era was only 28% and the 2021 era was 1.7%, but it was also individual with a little influence. (Nel caso dei fondi obbligazionari, la percentuale è scesa allo 0% già nel terzo anno successivo, il 2020). The popular method of investing solely in the background of Hanno's history will result in positive positive results that are destined to fall.

Let's just say this conclusion, a view that is largely significant, and concludiamo così the nostra argument against the investment attivo and a favore di quello passive. This is not a part of the convinti of the vantaggi of the passive investments and/or desidera leggere ulteriori arguments against the investment attivo and a favore di quello passive, è invited a leggere il nostro articolo sul blog “The motivation behind these investments is non-functional“.

The abbiamo già convinta, ne siamo lieti e, come ringraziamento, abbiamo in serbo per lei una chicca davvero speciale: a semplice ricetta for a portafoglio passive gustoso e succulento composto da soli due ETF.

Come funziona l’investimento passive?

The investment passivo is simply in line with the principle of the investment of the funds indicated in the years ’70 and the ETF come as a variant of the funds indicated in the years ’90. In sostanza, that's it fare due cose:

in the first place, determine the ripartition percentage of the proprio portafoglio tra la parte a rischio e quella a basso rischio (ad esempio 60/40) e, in secondo luogo, riempire the due parti del portafoglio con ETF specifici.

Questa asset allocation statica implementata su una rigorous logica Buy and Hold (“comprare e detenere”). The Buy and Hold is part of the investment passive and the amount of global diversification attributable to the use of funds indicizzati ed ETF.

Questo is the concept of the global portfolio of Dr. Gerd Kommer, derivato dalla scienza. In this case, it is sufficient to have an ETF product for the part of the portfolio and also for the part of the rischio. The illustration is in seguente graphic.

Grafico: Rappresentazione schematica del portafoglio global

►Fonte: The easy entry into the world of ETFs by Gerd Kommer. ► (*) Conto current account only se l’importo rientra nella garanzia sui depositi statale di un paese con un rating di credito di almeno AA.

The quota of the portafoglio rischiosa (“RBT”) is the motor of the rentimento responsabile della generation of the rentimento of the portafoglio”, which is the quota of the portafoglio priva di rischi (“risk-free”) (“RFT”) funge da “ancora di sicurezza”. Chiamiamo questa dicotomia allocation level 1. In line with the principle, it is possible to allocate 100% of the quota of the rischiosa portafoglio (“portafoglio 100/0”) to 0% of the rischiosian portafoglio’s quota (“portafoglio 0/100”), so the sole solution is optimally si trova da qualche parte nel mezzo, poiché solo Pochi investors prefer the extreme allocations.

The position specific to determine the balance sheet of investments in the RBT-RFT spettro (quota di portafoglio rischiosa - quota di portafoglio priva di rischi) differs principally from quattro variabili: rendimento atteso, propensione al rischio, fabbisogno di liquidityità e orizzonte di investimento. Maggiore è l'incidenza di queste variabili (ad eccezione del fabbisogno di liquidità), più rischiosa (“aggressive”) potrà essere the composition of a portfolio. Viceversa, if the variables are as small as the mark, they should be initiated with a level allocation of 1 meno rischiosa (“più conservativa”).

The variables differ from each other in the terms of intensity, based on the orientation, even initially, on the other hand, in a conservative way, not in successive years, a personal voltage acquisition with the portafoglio, in the final and gradual process.

A voltage decision is made to allocate level 1, it is necessary to decide on the ETF specification: the question is the same allocation level 2. In this simple form, it is realized with an ETF for the RBT and one for the RFT. The RBT can also be used by the global market, the ETF RFT should contain only obbligazioni i) with a scadenza residua breve, ii) with an elevated rating of credit and iii) in the national value of the investors, al fine Aspire to all the functions of removing the rischio.

Nella in this form is simple, a portafoglio di questo type potrebbe presentarsi come segue:

- Quota di portafoglio rischiosa (“RBT”): Vanguard FTSE All-World UCITS ETF (ISIN: IE00BK5BQT80) [a partire da: settembre 2022] o L&G Gerd Kommer Multi-fattore Equity UCITS ETF (ISIN: WELT0A)

- Quota di portafoglio priva di rischi (“RFT”): Lyxor EuroMTS Highest Rated Macro-Weighted Govt Bond 1-3Y (DR) UCITS ETF (ISIN: LU1829219556) [set 2022]

Alternatively, the part of the portafoglio a basso rischio potrebbe is also presented as a current account or an account for deposit on a termina presso una banca, a condition that the import of investment is rientri nella guarantee on deposits statale di 100,000 euros per or combinazione cliente-banca.

If you are notified by notaries, you are not required to accept the investment, but only in a way that you can easily attribute an approccio to the passive investment. The global portafoglio is extremely perfect for a picture (as it is combined with cosiddetti premium di fattore; tuttavia, reflect the theory and practice on the basis of the cosiddetto factor investing andrebbe oltre lo scopo di this article).

A voltage that defines the portfolio and acquires the ETF, it is possible to verify a regularly scheduled allocation interval of 1 without the additional discount of the target allocation that is also desired at a long period of time. The motivo is the ricercarsi inlle fluttuazioni di mercato a cui un portafoglio (in particolare the RBT) è esposto giorno.

Conclusions

In this article it is possible to achieve the same quality as the class of activity and the quality of the device as well as present in the portafoglio. Per the strategic direction of the private investors, a mix of actions come from “motore di rendimento” and obbligazioni come “ancora di sicurezza” nel portafoglio dovrebbe essere adeguato. Successfully abbiamo affrontato il dibattito sull'investimento attivo e passiveo, esaminando the difference tra i due approcci e dimostrando, sulla base di argomenti teorici e pratici, perché l'investimento passiveo è l'alternativa migliore rispetto a quello attivo. Infine, abbiamo esaminato l'attuazione pratica di un portafoglio passiveo (spesso denominato che “concetto di portafoglio global” by Dott. Gerd Kommer) and abbiamo sottolineato the importanza of the principle of ribilanciamento.

Invest in a globally significant portfolio that meets the needs of the global economy and its capital. With the capital of the company, the company's quota of 10,000 is in stock, in fact the world has the right to be saved and serviced by the people on the left side of the piano tenore di vita rispetto alla generation dei loro genitori. Per the fornitura di capitale di rischio sotto form di azioni e obbligazioni, the investor of the global portfolio viene ricompensato with a rendimento adeguato al rischio.

Letteratura

Dimson, Elroy; Marsh, Paul; Staunton, Mike (2019): “Credit Suisse Global Investment Returns Yearbook 2018”; versione lunga; Credit Suisse Research Institute; 256 pages

Kommer, Gerd (2018): “Invest confidently with index funds and ETFs. How private investors win the game against the financial industry”; Campus Verlag, 5° edizione, 2018 (prima edizione 2002); 415 pages

Gerd Kommer (2022): “The easy entry into the world of ETFs: Uncomplicated provision – a starter book for financial beginners”; FinanzBuch Verlag, 1° edizione, 2022; 180 pages

Kommer, Gerd; Weis, Alexander (2019): “Factor Investing – the Basics”; post on blog; maggio 2019; link: https://gerd-kommer.de/it/blog/factor-investing-le-basi/

Kommer, Gerd; Weis, Alexander (2020): “The motives for investing in investments do not work well”; post on blog; February 2020; link: https://gerd-kommer.de/it/blog/dieci-motivi-per-cui-gli-investimenti-attivi-non-funzionano-bene/

S&P Dow Jones Indices LLC (2021): “Standard & Poor’s Index Versus Active”; December 2021; link: https://www.spglobal.com/spdji/en/research-insights/spiva/

The post Investimenti passivi: le basi appeared first on Gerd Kommer.

]]>The post The motivation behind these investments is non-functional appeared first on Gerd Kommer.

]]>This is a promising investment, in reality it is only due to the formation of the foundations of investments: investments “attivi” and “passivi”. The maggior parte delle persone associa quasi automaticamente l'investimento e la constitution di patrimonio solo agli aspetti che riguardano l'investimento attivo. The investment attivo è “ciò che fanno tutti”, ovvero lo stock picking, the market timing or a combination of entrambe le cose.

Investire in modo attivo significa investire denaro with l'obiettivo, consapevole or inconsapevole, di effettuare un investimento particolarmente interesting rispetto al mercato or alla classe di asset di riferimento. From the point of view of a private investor, it is significant to invest at the denaro autonomously or commission a banker, a patrimonial manager or a sponsor of the fund for the payment of a commission. Secondly, according to the calculation, the quota of the global market for investments is at least 98% (Kommer, 2019). A passive investor does not have a battery in the market, it invests in a market based entirely on the Buy and Hold basis, using fundi indicizzati or ETF (Exchange Traded Fund) at a lower cost.

One of the motives for investing in investments is based on a quota from the market that is elevated and corresponds to a fundamental characteristic of the psychological environment that is imprinted on our DNA from the last 10,000 years of evolution: Quasi all is alive migliori degli altri. When you invest, you also go to the market. Investire attivamente è normal, naturale and soft. Tuttavia, ciò comporta un problema importante: funziona piuttosto male.

A nice maggioranza di all gli investitori attivi (secondo alcuni studi oltre iltre iltre il 90%) sottoperforma il proprio benchmark passive per una determinata finestra temporale (ad esempio l’anno solare 2019, gli ultimi cinque anni o i 20 anni dal 1970 al 1989), ovvero un Indice comparable dal punto di vista scientifico che si limita a seguire il mercato o la classe di asset su base Buy and Hold.

The minor group of investitors have taken up the benchmark passivo nell'arco di tempo considerato, probabilmente lo ha fatto per caso. The conclusion is that the successive arc temporal equivalent can be achieved through the minor achievement of the outperformer. Because of this, the composition of the minors is not the end of the future. The scientific students have studied in modern times and are convinced that they are around 60 years old in number.

The conclusion of 60 years of empirical research on financial markets: ponderato in base alla probabilità, the investment attivo è a gioco a perdere.

In this regard, the cosiddetta theory of the Mercati Efficienti (“EMH”) viene citata come motivo della migliore combinazione rischio/rendimento dell’investimento passiveo. Si tratta di un'affermazione corretta, ma troppo myope: oltre all'EMH, infatti, esistono numerose altre cause e argomentazioni che, nel loro insieme, rendono l'investimento passiveo l'approccio più redditizio.

Con this post you have presented all the arguments, the loro in sieme, determines the superiority of the investment passivo.

The result is that these arguments are based on the investment passive genera and a better combination of rischio/rendimento rispetto all'investimento attivo.

(1) Teoria dei mercati efficienti (“EMH”)

Come accennato in precedenza, this is the argument più citato against the investment attivo. The EMH depends on the prezzi of the titles in a current moment when the information is available to the public; in other words, this information is also available beforehand. Questo fenomeno è noto come efficienza informativiva dei mercati dei capitali (Brown, 2011). The use of public information, the source of the majority of investors, is not available, but is not available in the form of an affidable rendiment (in Gergo tecnico “Alfa”) rispetto all the media of the Mercato. In an efficient market from a point of view of information, the deviation from the return of the market to a single investor is casual. The American economist Eugene Fama, winner of the Nobel Prize, is considered the “father” of the EMH (Efficient Market Hypothesis, theory of efficient markets).

(2) “The Arithmetic of Active Management” (AAI)

The title of a famous Nobel prize for economics is William Sharpe. L’AAI afferma che l’investitore attivo medio deve sottoperformare un investitore passivo equivalente per necessità matematica (Sharpe, 1991). The precise value is: up to 50% of the unit of monetarie invested in investments that have an inferior return on the source of the unit of monetization invested in liabilities. Questo perché tutti gli investitori insieme formano il mercato. Quindi, the Lord of the Costs, is one of those who have a second half of the market and the other half of the old one. By definition, the investors passivi ottengonono esattamente il rendimento del mercato al lordo dei costs. Because the costs of the investitors are therefore necessary to increase the sources of the investitors passively, the value of the investitors attracted also has a “net” inferior risk to the investitors passively. Questa affermazione non presuppone né the validity of the EMH né other conditions. In definitive, it is based on a logic of the market and fattuale molto semplice, in combination with i costi da cinque a dieci volte superiori dell'investimento attivo rispetto and quello passive.

(3) Il vantaggio fiscale intrinseco del Buy and Hold

Quasi tutti gli investitori pagano le tasse gli investitori attivi pagano più tasse degli investitori passive. Perche? By definition, the investment is rich in acquisitions and sales risk from all passive investments, which requires a Buy and Hold approach. Poiché the realization of the plus value on the title and the conseguente pagamento delle imposte vengono rimandati nel futuro, the Buy and Hold produce a cosiddetto vantaggio in value attuale fiscale rispetto all'investimento attivo (in cui ciò not si verifica, or si verifica in misura minore, per la posizione media), vale a dire che l’onere fiscale effettivo diminuisce. Questa correlazione esiste praticamente in ogni regime fiscale. A parità di altre condizioni, più alto è the livello di tassazione, maggiore è the vantaggio fiscale del Buy and Hold. The fiscal regime is relative to all'imposta sui redditi da capitale, this effect porta a aumento del rendimento netto di circa un punto percentuale all'anno per le azioni in circostanze altrimenti identiche, ipotizzando a periodo di Buy and Hold di 30 anni (Kommer, 2018).

(4) Distribution of returns from the campaigns

The distribuzione destra (or asimmetria positiva) is a terme statistico e in parole povere significa che ci sono alcuni outlier extremely molto “a destra” rispetto alla media. The product is located in the “market section” and in the “longitudinal temporal section”. In the first place, according to the quanto riguarda la distribution of the nella section of the market: the section of the market is constituted by the action that is based on the same period in a determined period of time (from 50 years ago). The crucial point is: only 4% of the purchase price is responsible for the return of the retailer to the interest of the retailer (“risk-free return”) (Bessembinder, 2018). The remaining 96% of the “loser” generation is only the “rendimento of the libretto di Risparmio”, which is the net dell’inflation è prossimo allo zero. Since the positive return of the market is concentrated in the final analysis in a number of straordinariamente ridotto of “azioni superstar”, this means that it is difficult to identify in a permanent and sufficient manner to ensure stock picking. Come già accennato, in a determinata finestra temporale ciò riesce solo a una piccola minoranza di stock picker e probabilmente per caso. A description of the “distribution of the destra” is completely diverse, in a similar way, it is verified in a long period, but the market is not returned for a long period of time (this year, the same year). As an example, from the beginning of 1970 to the best of 2019 (50 years or 600 years) the year after 20 years was the index of the MSCI World Standard index, but only 3% in the last 50 years, the total return was 7.9% annuo (nominal e in euros) the drastic price of the metal, passed to 3.95% annuo. Se si perdessero i 49 mesi migliori, ovvero solo l’8% di tutti i mesi, the rendimento risultante per tutti i 50 anni scenderebbe a zero. Se this calcolo fosse based on two years ago, the effect of distruzione del rendimento dovuto alla mancanza di piccole porzioni dell'arco di tempo totale sarebbe ancora più extreme. Based on the “distribution of the positive (or asimmetria positive)” motivation, the market timing is quite unrealistic, precise and successful.

(5) “The Paradox of Dropouts”

Secondo questa teoria dell'economista Steven Thorley, il mercato dei capitali (ad es. il mercato azionario or il mercato obbligazionario global) è inteso come un gioco con partecipanti di diverse abilities - un'ipotesi plausibile (Thorley, 1999). This is the same, with the passing tempo, soprattutto i giocatori (operatori di mercato) with a basso level of ability (skill) ad bandonare il gioco, poiché prima or poi si renderanno conto della loro mancanza di successo (rendimento). The result is the medium level of ability of the rest of the players. Diventa quindi più difficile per un determinato giocatore restante superare il livello medio di abilità ora più alto (the nel gioco della “borsa” è il rendimento del mercato). The paradosso of the dropout implies the increase in the quota of the market for passive investments in the last year (and the result of the diminution of the quota of the market for the investments in assets), contrary to the quantity of the investment quota, which is likely to be non-portable to the rest of the investors, Bensi a uno svantaggio.

(6) “The Paradox of Skill”

Questa tesi è state formulata originariamente dal biologo americano Stephen Jay Gould. In this case there is a quanto segue: it is presumed that the borsa is a competition with the cui result (the distribution of the Alfa to the operators of the market, over the access or the difetto di rendimento rispetto alla media of the market) è determinato in parte dall'abilità e in parte dal caso. This means that the ability of the operators of the market can be achieved at a very rapid pace in the progress of science and technology combined with a better form of investment and the ability to gradually distribute in the same way as the operators of the market, also Perché la percentuale di investitori privati tra tutti gli investitori diretti (investitori in regia propria) sta effettivamente diminuendo (come dimostrato dal mercato azionario statunitense). In a tale of competition, the contribution of the caso rispetto all'abilità nel determinare the result of the competition (the distribution of Alfa tra gli operatorsi di mercato) also in tempo perché the ability of the operators di mercato saranno più simili tra loro (Mauboussin & Callahan, 2013). Questo fenomeno è a paradosso, perché nonostante l'aumento assoluto dell'abilità della maggior parte dei giocatori, aumenta l'influenza del caso sul risultato individuale. Quanto maggiore è the influence of the case, tanto minore è the attrattiva dell'investimento attivo.

(7) Berk-Green's allocation to alfa

In 2004, in a small studio, the economists Berk and Green Hanno dimostrato che in a mercato in cui sono presenti investitori professionali in gradeo di generare alfa in modo affidabile (ossia un mercato Not efficient at the point of view of the information). Secondly Berk e Green, i gestori di investimenti di successo (ad es. gestori di fondi comuni, hedge fund or amministratori patrimoniali) with an alfa positivo aumentano the loro commissioni assolute attraverso l'aumento del volume di denaro gestito e in alcuni casi also attraverso an aumento della commissione percentuale fino a quando il net returns from investors from the market. Questa tesi è perfect in linea with the data preserved. The application of Berk-Green also has a real ability to operate the market, without the final investment being a benefit.

(8) Inasprimento della regolamentazione

In a commercially strettamente regolamentato it is very difficult to keep the retailer in a retailer without regulation. The regulation tends to contribute to the elimination of “special opportunities” for the individual investors and to create a greater opportunity for the mass of investors. Negli ultimi decenni, the densità normativa dei mercati finanziari è aumenta in modo significant in all the world, in particolare negli ultimi dodici anni dopo the Grande crisis finanziaria del 2007-2009. The vigilanza is diventata più rigorous and professionale e l'azione punale in caso di reati sui mercati finanziari è diventata più efficace. It is likely that this tendency will continue in the future. Basti pensare al drastico inasprimento delle sanzioni nei Paesi occidentali and ai procedimenti penali per insider trading, a fonte storicamente importante di sovraperformance.

(9) Technological progress

La crescente diffusione il miglioramento delle tecnologie informatiche e di Internet fanno sì che, nel longo periodo, più investitori osservino e analizzino il mercato con informazioni e strumenti semper migliori. The “anomaly of the market” has a long duration (titoli with prezzi errati, but the opportunity for supplementary returns) can also be arbitrated very quickly and in a very long time, but the opportunity for sovraperformance is rare. Questo technological progress continues in the future.

(10) Volume di alfa limitato rispetto all'aumento del numero di cacciatori di alfa

The pool of opportunities for additional rendimenti rispetto al mercato (pool di alfa) è in ultima analisi limitato dall'economia global, ovvero dall'economia reale. In parole povere, si potrebbe also dire è limitato dal numero di aziende e progetti di investimento. The global economy reaches a pace of around 3% all year. Tuttavia, the number of “cacciatori di alfa”, ovvero di tutti gli investitori attivi, sta aumentando più quickly. One of the indicators of this fence is the number of the hedge fund: Nel 2000 or 900 in the world, or even 15,000 (with a medium annual crescita of approximately 16%). Also the number of graduate students in the financial markets is in the last decade. Do the lupi si riproducono più velocemente degli agnelli, rimane semper meno per il singolo lupo (Berkin & Swedroe, 2015).

Conclusions

Abbiamo dimostrato che non solo la theory dei mercati efficienti (l'efficienza informativa dei mercati finanziari) è responsabile della superiorità statisticamente osservabile degli investimenti passivei, even in old nove fattori raramente menzionati dai media finanziari. A new view is also given in part to the fat of the controversial arguments that are now destined to continue in terms of force and imprint in the future. Nella misura in cui ciò si verificherà, aumenterà ulteriormente l'attrattiva relativa degli investimenti passivei nei prossimi anni.

Letteratura

Berk, Jonathan; Green, Richard (2004): “Mutual fund flows and performance in rational markets”; in: Journal of Political Economy; vol. 112; n° 4.

Berkin, Andrew; Swedroe, Larry (2015): “The Incredible Shrinking Alpha: And What You Can Do to Escape Its Clutches”; Buckingham.

Bessembinder, Hendrik (2018): “Do Stocks Outperform Treasury Bills?”; in: Journal of Financial Economics; vol. 129; n° 3.

Brown, Stephen (2011): “The efficient market hypothesis: The demise of the demon of chance;” in: Accounting and Finance; vol. 51.

Gerd Kommer (2018): Invest confidently with index funds and ETFs; Campus Verlag (5° ed.); page 235 e segg.

Gerd Kommer (2019): “The most important arguments of the ETF critics – what’s wrong with them?” Press Conference by the Federation of Organizing Consumers of Tedeschi; https://gerd-kommer.de/medien/2019-01-VZBV-Kommer-V9-L.pdf

Mauboussin, Michael; Callahan, Dan (2013): “Alpha and the Paradox of Skill”; Credit Suisse.