The post Portfolio Evaluation for Passive Investors: Eleven Simple Rules appeared first on Gerd Kommer.

]]>In this blog post, we formulate eleven simple rules of thumb to help a private investor evaluate the performance (return and risk) of his or another passively managed portfolio. Such an evaluation is often referred to in financial jargon as: Benchmarking referred to when a comparison is made with a reference size, e.g. B. with an index (market return, asset class return) or with another objectively comparable investment.

Some of the following basic evaluation and benchmarking rules do not apply to actively managed portfolios/portfolios or only apply with additional assumptions.

(1) Short periods of time are usually useless and often even misleading for evaluating the performance of a portfolio

Periods of less than three to four years are not meaningful if you want to draw reliable, robust conclusions from the observed portfolio performance (return, risk). When looking at shorter periods of time, there is a risk of drawing conclusions that are harmful for the future.

Judgments derived from history tend to become more reliable the longer the data series being analyzed. The returns of listed and unlisted investments over short periods of less than three to four years are heavily influenced by “statistical noise”. These are influencing factors that are often random in nature or are in any case beyond the control of the portfolio holder or his advisor and their specific characteristics could not be predicted (expected) ex ante. Because this is the case, little or nothing can be derived from “noise-influenced results” for the future. Drawing decision-making conclusions from short series of data can actually be downright harmful.

An example: A depot has existed for six years. Over this period, the performance is satisfactory from the portfolio holder's perspective. But isolated only in the last twelve months, it is significantly worse than an underlying benchmark and also less satisfactory than over the entire period. What can be inferred from the poor performance over the immediate past twelve months? Most likely nothing, even if that seems unsatisfactory to the portfolio holder.

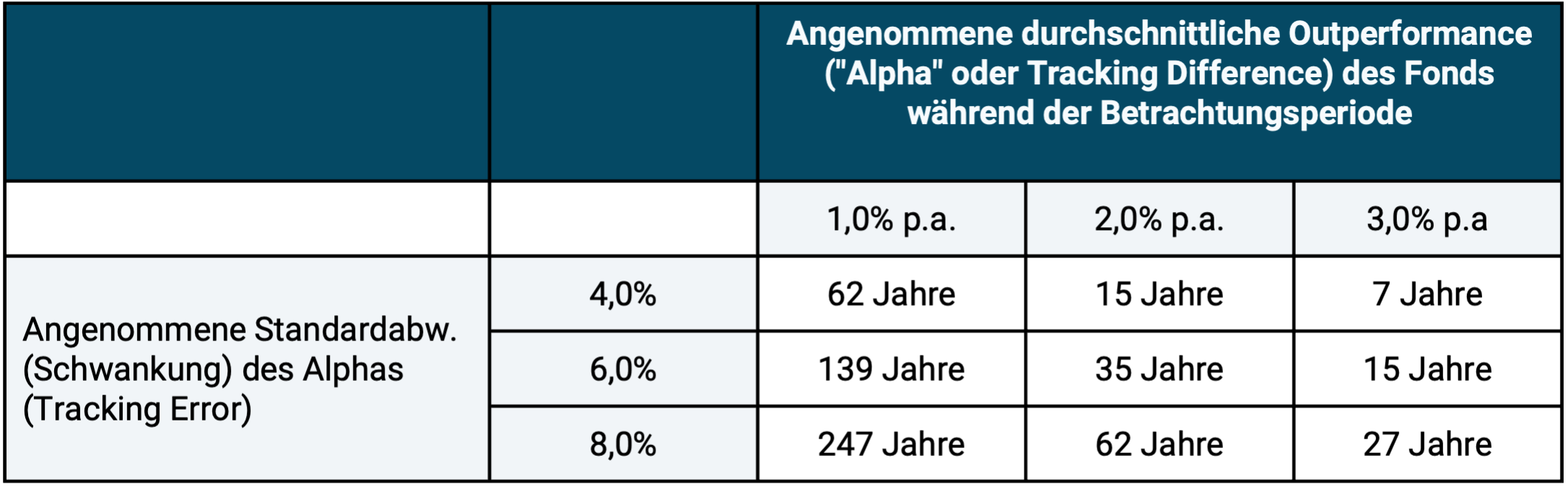

In the following table we show how long it would take, from a purely statistical point of view, until under normal circumstances one no longer has to consider a given outperformance (excess return) of an actively managed fund or other portfolio relative to its correctly chosen benchmark to be “possibly coincidental”.

Table: How long does it take until you can reliably distinguish random outperformance from non-random outperformance (excess return) in an actively managed investment fund?

► “Alpha” or tracking difference is the average return difference of an investment A compared to a benchmark B over a sufficiently long measurement period. This return difference will fluctuate around its mean from year to year with some volatility. Three typical example values for this fluctuation intensity are given in the second column from the left. An alpha of an average of one percentage point p.a. after all costs over a period of ten years is generally considered to be a significant performance for active portfolios (e.g. investment funds). ► "Tracking error is the volatility of the periodic tracking difference in an overall period. This is highly dependent on the active strategy and is usually higher, the higher the desired "outperformance" compared to the benchmark is. ► The calculated annual figures are based on a significance level of 95%. After this number of years, the probability that the “alpha” was just a coincidence is only 5%.

Also, the return of a portfolio or investment Anyone who, without a hard, objective reason, gives greater weight to performance in the recent past in the analysis than to performance in the more distant past is subject to the common, dangerous error of reasoning: “recency bias”. [1]

(2) Return alone is not meaningful

The fact that two portfolios A and B should not be compared solely on the basis of their (hopefully correctly measured) return, but that the comparison must also take risk and liquidity level, taxes and costs into account, is a trivial statement that no one will dispute. Nevertheless, according to our observation, “one-dimensional” portfolio or financial product comparisons are constantly made solely on the basis of the return and often enough on the basis of the return in far too short periods of time, e.g. B. 12 or 24 months. We will address the common mistake of not taking into account the different degrees of liquidity between two investments being compared in the next rule of thumb.

(3) Illiquidity or liquidity should be taken into account in the ex post evaluation of the individual components of a portfolio

The parallel/comparative evaluation of the performance (return, risk) of liquid and illiquid investments (e.g. stocks, bonds, gold, cryptos as liquid investments on the one hand and real estate or private equity as illiquid investments on the other) during a period of time There are two insights to consider:

A rational assessment of the risk, especially the risk of fluctuations in the value of illiquid investments over a given historical period, is complex because these investments are not listed on the stock exchange, i.e. there are no daily updated market prices for them. Concluding from the absence of daily updated market prices and the resulting apparent stability of value that the illiquid investment in question has relatively stable prices over time will often be an incorrect and potentially very damaging conclusion. When evaluating a portfolio, an investor should ask himself at what price he could sell the illiquid investment at that moment in a maximum two-month window. In the majority of cases you will find that immediate sale is not possible or only via a “secondary market” with a presumably considerable discount compared to the “reported price” from the provider.

The illiquidity disadvantages of individual investments should be underestimated or even ignored in their performance assessment because they ex post - as will usually be the case in a specific case and even statistically has to be the case - did not play a role is a common mistake among private investors that can have a very damaging effect at some point.

(4) The individual components in a consciously and systematically diversified portfolio should not be evaluated purely individually in isolation

If a depot consists of several individual components, e.g. B. several ETFs and other financial investments, which were originally consciously chosen as part of the definition of the overall structure of the portfolio, then the portfolio performance should primarily be evaluated “as a whole”, so to speak as a “team performance”.

So it usually happens not on the individual return of an individual investment in isolation, but on the portfolio structural role of this individual investment “in the team”, in the overall portfolio. For example, it is a mathematical necessity that even among ten individually excellent, but also different, individual investments within a portfolio, there must necessarily be one that produces the worst individual return among these ten in a given period of time (whether 12 months or 12 years).

The analogy of a Bundesliga soccer team: what counts in terms of its success in an individual game or in a season (34 games) is primarily the team's game result, the collective performance of all eleven players, i.e. how these eleven players played together in different roles and tasks. For example, a defender

(5) When evaluating a portfolio, one should avoid hindsight bias

A not uncommon mistake when evaluating the performance of a portfolio during a period of time This is called “hindsight bias” in technical jargon. [2]

In most situations, one should judge the past performance of a portfolio or the performance of the person managing the portfolio based primarily on only the information that one had before the start of the period. This approach ensures that there is no “confusion between strategy and result”, which means: the quality of a strategy - including an investment strategy - can ultimately only be meaningfully assessed on the basis of the information and goals that were known/available at the time the strategy was chosen and defined. The result of the strategy alone - regardless of whether it is pleasant or unpleasant - is an inadequate and often even very poor quality criterion for a strategy.

The following simple example should make this clear. The goal is to get from Berlin to Munich by train in the shortest possible travel time. Therefore the Sprinter is chosen, which is supposed to be around half an hour faster than the normal ICE. In statistical terms you should be faster. In fact, on the specific journey, this Sprinter train is delayed by an hour, while the normal ICE arrives on time. Nevertheless, hardly anyone can doubt that it is ex ante The right strategy was to book the sprinter, even if the specific result was disadvantageous.

(6) The valuation level of an investment at the end of the evaluation period should be taken into account

Here is an example to illustrate what is meant: Two stock portfolios A and B generated the same, satisfactory return over a period of eight years (i.e. an evaluation period that tends to be sufficiently long). They also had similar fluctuations in value (volatility) during this time and there were no serious differences in other risk types (e.g. maximum drawdown, diversification contribution in the portfolio, etc.). However, at the end of the observation period, stock portfolio A is now valued significantly higher (more expensive) than portfolio B - measured by a common and reliable valuation indicator, here the P/E ratio.

What are the conclusions? Portfolio B was or is now the better investment because it has a higher expected return in the future (all other things being equal). The superiority of Portfolio B exists even if the assessment of the valuation of the two investments is based on an (identical) uncertainty factor.

(7) Non-materialized cluster risks should be taken into account when evaluating the portfolio return

A good portfolio is structured in such a way that it does not contain any concentration or default risks, except for those that the investor has recognized, understands and is aware of - e.g. B. temporarily – were accepted. Typically, the materialization of cluster risks is a rare black swan event. Black swan events may only occur once every 20 to 50 years. [3]

It can be assumed that such a cluster or default risk did not occur in a given evaluation period. This is exactly what was to be expected ex ante. However, this “normal non-occurrence” does not mean that these unmaterialized cluster risks should be ignored in the ex post evaluation of a given portfolio.

From a conventional, so to speak “vulgar” risk perspective, which consists in basing risk evaluation solely on volatility, a portfolio A in which cluster risks have been well diversified away cannot be directly compared with a portfolio B in which a cluster risk exists.

Here is an example: Portfolio A consists of 100 different high-yield bonds from 100 different issuers from different industries and countries, so it is well diversified in terms of default risk. Portfolio B consists only of one high-yield bond. The two portfolios are identical in all other important characteristics (current yield, currency, duration). Portfolio B is very likely to outperform over a normal long period of time (e.g. one year or five years) because the probability of this one bond defaulting is low for these periods. In Portfolio A, on the other hand, one of the 100 bonds is almost guaranteed to default, which lowers the A portfolio return. Only if the small risk of default for the individual bond in B occurs will A perform better (and then dramatically). Therefore, if B outperforms as expected, one cannot conclude that it was the better portfolio (investment). The B investor was simply lucky, but luck that will occur in the majority of cases. However, if luck does not occur, the consequences for Portfolio B are extremely negative.

Examples of further cluster risks include the decades-long under-return of assets in a country (stocks, bonds, real estate) due to political factors. Examples of such default risks include the bankruptcy of an account-holding bank or the provider of capital-forming life insurance.

(8) The benefit of a mediocre investment may have been ex post to prevent an even worse investment

The financial benefit from an investment A - in addition to its return - often also consists in the fact that the investment A prevented the investor from making a worse investment B. This statement is not sophistry.

When evaluating the past performance of a given investment, an investor should always ask himself, "If I'm being honest, did Investment A stop me from making an even worse Investment B?" Investment success is not only the result of smart, positive decisions and actions, but also the result of avoiding harmful, negative decisions/actions.

We have this unusual evaluation perspective in a separate blog post entitled “Via Negativa – an unknown concept for more success when investing” shown. The via negativa concept is based on the obvious, but often overlooked, insight that the economic success of most wealthy households relative to less wealthy households is due in large part to the fact that they have made fewer investment mistakes than other households over a long period of time. One such avoided mistake could be avoiding a “disaster investment” by making another investment that may be individually suboptimal.

(9) When evaluating a portfolio, you should also think about “negative parallel universes”.

A portfolio should be structured to provide a minimum level of financial resilience even in “negative future worlds”. Here are some examples of negative “future worlds”, negative “future scenarios”:

- The general level of interest rates in the Eurozone is rising noticeably above the current level. As a result, real estate prices fall sharply and the real estate market “freezes”: the transaction volume (purchases/sales) shrinks by more than half. Sellers no longer want to sell at the sharply reduced price. Buyers do not want to buy as they wait for further price declines. I won't be able to implement my short-term wish to sell for two years and after that only at a lower price than expected today.

- The German state is tightening the existing rent cap. As a result, the value of rented and owner-occupied residential properties only increases below inflation over 13 years, i.e. falls in real terms.

- The USA is experiencing a national debt crisis due to its high national debt. US dollar interest rates (as well as bond interest rates in other countries) are therefore rising sharply. As a result, bond prices fall by 40% in a short period of time. There are reports in the media about a possible haircut on US government bonds. The US dollar is depreciating sharply. My daily money in US dollars experiences a drawdown of 35%.

- There is a systemic banking crisis in the Eurozone. At the same time, many banks are running into serious liquidity problems and are restricting their customers' account withdrawals. [4] According to media reports, my bank, where I hold 700,000 euros in a current account, is potentially insolvent and will no longer allow withdrawals until further notice. It has been unclear for months whether there will be a bailout by the state for my bank above the statutory deposit protection limit of 100,000 euros.

- Due to their high valuation today, tech stocks will significantly underperform the general stock market over the next ten years, as was the case for around ten years from the beginning of the noughties. Tech stocks have a weight of around 60% in my portfolio. This pulls the portfolio return below the general market return for years.

- My own company, which I own, is in crisis. Its estimated value is halved and no distributions are possible for several years. My financial peace of mind as an entrepreneur and as a person decreases significantly because of this.

The structure and distribution of a household's assets, if they have already accumulated significant assets, should ideally be designed in such a way that no such black swan scenario has an individually catastrophic financial impact on the household, i.e. that the household assets will suffer, but "the very worst" is still prevented, even if that costs return points "in good times". This is called “financial resilience.” The question of the correct asset allocation and portfolio structure should be addressed by the household at greater intervals.

(10) When evaluating the performance of a passively managed portfolio, one should consider which goals can be achieved rationally and realistically and which cannot

From our point of view, the primary financial goal of a passively managed portfolio is to be in the top quintile (the top 20%) of all comparable investor households in terms of final assets achieved or the average return measured correctly in financial mathematics after ten, 20, 30 or 40 years. A secondary but also very important goal is to avoid disaster performance, i.e. not to be among the worst - let's say - fifth of all meaningfully comparable investors (see previous point).

“Factually comparable” requires taking into account the risk taken during the period in question (e.g. volatility risks, counterparty risks, cluster risks, liquidity risks, default risks).

For an investor with a passively managed portfolio, a rational, realistic goal with regard to the portfolio cannot be “to have the most profitable investment” or to “be among the most successful 2% of all comparable investors”. By definition, this cannot be realistically achieved with a passively managed portfolio in periods of less than, say, 20 to 30 years (it is possible for longer periods). If it is not achievable, then later introducing the claim “why did I underperform the best investment Y in the ten years this portfolio has existed?” makes no sense in performance evaluation.

(11) For a portfolio managed by a service provider: Be careful when comparing your own portfolio with the portfolios of other asset managers or banks

When asset managers and banks want to acquire a new customer B. based on a securities account statement. Then they benchmark this portfolio Naturally, strategy Y has paid better in the past than portfolio on average were no better or even worse than X.

In this case, does the historical outperformance of Y compared to X prove that the new asset manager/bank has more investment skills than the one who managed the previous portfolio X?

No, because to do this you would have to compare all existing strategies of the new asset manager/bank with portfolio But this will not happen on the part of the new asset manager/bank.

Conclusion

Successful investing is a long-term process, a marathon. In order to be able to judge for every kilometer covered during this marathon whether or not one is sufficiently promising in terms of the desired performance, evaluation criteria are needed. We have formulated eleven simple criteria or rules of thumb here. Anyone who uses them during the annual portfolio review (much more often will not be necessary) increases the likelihood of actually achieving the marathon goals they have set for themselves.

Endnotes

[1] See article Recency effect in the German Wikipedia or article Recency Bias in the English Wikipedia.

[2] See article Hindsight bias in the German Wikipedia or article Hindsight bias in the English Wikipedia.

[3] What is characteristic of black swan events is that they have a very low probability of occurrence, which is often not even quantifiable, but which cause particularly great damage if they occur.

[4] Depots (as opposed to accounts) cannot and must not be blocked for legal reasons.

The post Portfolio Evaluation for Passive Investors: Eleven Simple Rules appeared first on Gerd Kommer.

]]>The post From rich to poor happens more often than you think appeared first on Gerd Kommer.

]]>The book The Missing Billionaires – A Guide to Better Financial Decisions by two American asset managers Victor Haghani and James White contains a fascinating calculation on the subject of “The rich become poor again much more often than we think”. We reproduce this calculation below in a slightly modified form.

In 1900, there were around 4,000 people in the United States with assets of $1 million or more. In the absence of more precise data, Haghani/White simply assume that a quarter of these 4,000, i.e. around 1,000 people or households, had assets of at least five million dollars. Inflated with the average US inflation rate over the 122 years from 1900 to 2022, five million dollars from 1900 in money in 2022 (the end date of the calculation in the Haghani/White book) corresponds to about $180 million, and when inflated with the growth of the American economy (and thus roughly the growth of US household incomes) corresponds to around $6 billion. The correct inflated value of this “truth” is probably somewhere in between (see the following info box “Inflation”).

Infobox: The correct method of inflating historical amounts of money

Typically, prices, incomes or assets from the long-ago past are transformed (“inflated”) into today’s monetary values using the average consumer goods inflation rate. It is doubtful whether this is correct. There is much to be said for using the generally higher nominal growth rate of household income instead, or, as a replacement that is easily available to everyone, the nominal growth rate of gross domestic product per capita (Williamson et al. 2026). This method results in higher values in today's money.

It is on these 1,000 people – just over 0.001% of the then US population of 78 million – that we focus. We call this wealth elite our “MB Group” for “Missing Billionaires” based on the Haghani/White book. Why we talk about Missing Billionaires will become clear immediately.

Let us now make the following simple, obvious assumptions: The 1,000 people were each part of a couple, i.e. a family. To date, these families have continued to grow in membership at the same rate as the entire U.S. population. In 1900, all members of the MB Group invested their total assets in a broadly diversified portfolio of US stocks (a representative sample of, for example, 40 stocks). Families withdrew 2% of their assets each year in real terms for subsistence purposes. [1] Given the high level of wealth, this is a generous assumption. This rate of withdrawal would have allowed for a standard of living that would have been many times more demanding than that of the average American, without any further professional activity on the part of the people concerned.

“Real withdrawal” means that the corresponding absolute withdrawal amount from year 1 (i.e. 1900) was increased every year with the inflation rate, so that the consumer goods purchasing power of the withdrawal remained unchanged. Over time, the families paid taxes on dividends and any realized capital gains, taking a buy-and-hold approach, taking into account their withdrawals, that helped effective To reduce the tax burden significantly below the statutory (legal) tax rate. (We explain how this works - in practically every national tax system - in a separate Blog post)

At the end of 2022, the original 1,000 families would have become around 4,300 families, each with an average Minimum assets of around 2.3 billion dollars. Minimum assets because we expected a starting value of five million for all families, whereas in reality this value was probably only the lower limit of the wealth of the 1,000 families in question.

In their book, Haghani/White even come up with 16,000 families for the year 2022 with a minimum wealth of one billion dollars per family, because their calculation was overall less conservative than ours when it comes to the assumed effects of costs, taxes and withdrawals.

In fact, in 2022 there were only 730 families in the USA with assets of a billion dollars or more. Haghani/White write that presumably not a single one of these families is closely related to the original MB group. In other words: Probably none of the 1,000 super-rich families in our MB group from 1900 managed to stay in the top group of super-rich over these five generations.

Asset collapse among the super rich

The apparently surprisingly universal and rapid decline in wealth of the super-rich can also be illustrated with other figures. The first Forbes 400 list of the super-rich in the USA was published in 1982, over 40 years ago. [2] Of the 400 families in the 2022 issue of Forbes magazine, less than 10% were included in the first list in 1982, according to Haghani/White.

The short “half-life” of the wealth of the super-rich in the USA is analyzed even more comprehensively and clearly in the scientific study “The Rich get poorer – The Myth of Dynastic Wealth” by Arnott/Bernstein/Wu 2015.

To our knowledge, there are no such complex studies on the extent of the wealth collapse of “normally rich” families with assets of “only” a few million euros, but we see no reason why these wealthy, but not super-rich, families should be subject to other rules.

Why do we regularly read “the rich are getting richer” in the media and in populist books on economic inequality? This has two main causes. The first is that there is a lot of cherry-picking in the underlying time frames and regional units (e.g. a single country versus the entire world) in order to get to the sensationalistic desired result of many journalists: “Economic inequality is increasing and the rich are getting richer.”

Research on economic inequality is incomplete

The second main cause: Practically all academic research on the distribution of income or wealth over time, i.e. on the question of economic inequality, which is important in socio-political discourse, is methodically based on viewing “rich” as an abstract statistical Aggregate to be viewed as a small percentage group at the upper end of the income or wealth distribution, e.g. B. 10%, 1% or 0.1%. However, this way of looking at the rich population segment must be distinguished from the completely different analytical approach “rich people as a non-abstract group of specific natural persons” - a difference of importance that can hardly be overestimated.

If inequality research were to be carried out systematically on the latter methodological basis (rich people as specific natural persons) in addition to the “conventional method” (rich people as an abstract percentage group), the resulting headline would almost invariably be: “The rich from 10 or 20 or 30 or 50 years ago have become relatively and often enough even absolutely poorer” or “the rich families of today are hardly the rich families of 20, 30 or 50 years ago years”.

This is the case because the... composition According to all we know, the group of rich people changes surprisingly strongly and quickly over time. There is a constant migration into this group (“from bottom to top”) and out of this group (“from top to bottom”). It is not a “closed club of rich people” or rich families who are, so to speak, forever at the top financially and everyone else is forever at the bottom.

Back to the traditional, conventional and, in our opinion, incomplete or even misleading measurement of inequality (riches as a statistical aggregate): Despite the different impression that the media has been giving us about it for years, even this form of economic inequality is in the respect that matters most, namely global level, decreased in the relevant past. The so-called GINI coefficient of disposable income, a mathematical measure of income inequality, shows more economic equality or less inequality at a global level (i.e. including all countries) today than in 1960. Compared to 1990, inequality has fallen particularly sharply. The main reason: household incomes in developing countries have grown faster overall than in industrialized countries. This is primarily due to market economy reforms in China, India and other large and small emerging countries.

If one looks at after-tax income and not - as is usually the case in most such inequality statistics - pre-tax income and income including state transfer payments ("social assistance", unemployment benefits, etc.), then income inequality has also decreased or moved sideways in most western countries (i.e. not just at a global level) since 1990.

Fake news in the media about “The rich are getting richer”

A considerable part of the reporting on the alleged increase in economic inequality (with the implication “the rich are getting richer”) even cites figures and developments as “evidence of increasing inequality” that clearly do not say or can say anything about inequality, e.g. B. the increase in absolute Number of billionaires in a single country or worldwide over time. Such an increase would occur over a given extended period even if the inequality would remain unchanged or fall simply because it is the necessary consequence of the combined effects of population growth, economic growth and inflation.

Interim conclusion: The fact that economic inequality is increasing and, by implication, the rich are getting richer and the poor are financially stagnating or becoming poorer are clearly false statements in this generalization. (a) Globally, economic inequality has trended down relatively consistently over the last 50+ years, (b) it has also fallen in rich Western countries since a peak in the early 1990s, especially when after-tax income and government transfers are taken into account. (c) Specific Rich families don't always get richer, but as a group they probably get poorer (relatively and/or absolutely) in the long term. At least that is what the few available data and studies that inequality research has provided so far indicate.

Another cognitive deception at the level of the individual observer plays a role in this complex and ethically and sociopolitically charged topic: Why do we hear in the media and in our personal social environment much more often about specific people becoming rich than about rich people becoming poor? Because the former are proud of it, some even brag about it, while the latter almost always keep it quiet because they see their financial decline as a defeat and/or shame.

But whatever. What is crucial here is that the composition of the richest 10% or 1% changes surprisingly dramatically over time. It is not always the same people or families who are in this top group today as they were ten years, 25 years or 50 years ago. Not clearly communicating this factually and socio-politically important fact, barely researching it empirically, and literally keeping quiet about it can be seen as a systematic failure of sociological and economic inequality research. [3]

The reasons for this failure are obvious. By using the narrative “inequality is increasing and the rich are getting richer,” you as a researcher will receive much more attention in the media, in the public and in politics, you will be more likely to increase your own research budget and, moreover, you will not encounter any opposition anywhere. The same applies to journalists who, of course, achieve more circulation and clicks with the clickbait headline “inequality is increasing” than with the actually correct headline “according to the most important criteria, inequality is decreasing and most of the rich from 20+ years ago are poorer today”.

At the level of the individual household, the false narrative reinforces the false belief: “Once rich, always rich” and complicates the fundamental mind shift that a household that has become rich needs to transition into a truly functioning asset protection mindset.

What novels tell us about the collapse of wealth

Perhaps instead of relying on obviously incomplete or activist statistical methods and data, academic wealth and inequality researchers should evaluate the fiction literature of the last 200 years. It probably tells more “rich-to-poor” than “poor-to-rich” fates – the fates of specific people. Of course, these are initially fictional fates, but we can confidently assume that they are based on the real life reality in their society observed and experienced by the authors. Here is an example from the novel The green Henry by Gottfried Keller (1819-1890): [4] "The division of property [in the small Swiss town where the novel is set] changes a little from year to year and with every half century almost beyond recognition. The children of yesterday's beggars are today the rich in the village, and tomorrow the descendants of these are struggling to get around in the middle class in order to either become completely impoverished or rise up again." [5]

Thomas Manns (1875-1955) Buddenbrooks (Publication 1901), the most important social novel ever in the German language, is another example of a specific super-rich family that becomes poor again in two generations through a combination of materialized cluster risk (too little diversification), incompetence, wastefulness and laziness. (The laziness in the second generation of the family is glorified in various euphemistic terms, for example as “sensitivity” or “artistic inclination”.)

Otto von Bismarck (1815-1898) is said to have once said - in politically incorrect terminology from today's perspective - "the first generation creates wealth, the second manages it, the third studies art history and the fourth goes to waste." There are many popular variations of this observation. The Anglo-Saxon proverb “from rags to riches and back again in three generations” expresses the same point. [6]

The question now arises as to why rich families are apparently so bad at the discipline of “long-term asset protection”. Anyone who takes a closer look at this interesting question is likely to come to conclusions similar to ours. Seven possible individual causes of becoming poor are particularly striking in relation to rich people in Western countries:

(a) distribution of assets among an “excessively large” number of descendants,

(b) Distribution and reduction of assets through divorce (for the financial implications of divorce and separation, see our separate Blog post),

(c) too high taxes,

(d) excessively high, wasteful living standards,

(e) additional costs of liquid investments that are too high, [7]

(f) too many bad business investments (“your own company”),

(g) excessive philanthropic wealth transfers/donations.

The family in question has complete control over factors (b) and (d) to (g). It can influence factor (c) (high taxes) at least to a certain extent. Only factor (a) is de facto beyond the control of the actors, because here non-economic goals (many children want) take precedence over economic goals.

In a specific rich-to-poor case, more than just one of these seven causes will usually have been at work. However, the single most important cause here is – there is little doubt in our minds – cause (f): Too many bad business investments. (Please note that the five causes [a] to [e] have already been fully or partially taken into account in our Missing Billionaires calculation described at the beginning.)

In other words: The rich become rich because in the wealth accumulation phase they typically make very profitable, concentrated investments in the form of their entrepreneurial activities over a longer period of time.

The main cause of wealth loss for the rich

Rich families then become poor again mainly because at some point, as rich people, they make bad investments - again in the form of entrepreneurial activities - or, to put it more precisely, they make too concentrated (too extensive) loss-prone entrepreneurial investments in relation to their total assets and do so again and again over a long period of time. Very often, on the financial path down, investments are made in the same companies or industries as before on the path up. Sosner explains the theoretical logic of this asset decline process in 2022 (bibliography below).

The research of the American economist Bessembinder, which caused quite a stir among academic economists, also confirms this logic. Bessembinder's empirical analyzes show that the stock market's high long-term average returns compared to other asset classes ultimately come from only around 4% of all listed companies (stocks). The remaining 96% of all listed companies only contribute returns that are below market average and in many cases even 100% losses (Bessembinder 2018). The main cause in statistical jargon: stock returns are distributed in a strongly “right-skewed” manner. These results are likely to be transferable one-to-one to unlisted companies. When it comes to new companies (startups), around 50% fail in the first five years if you define “failure” as forced or voluntary liquidation and over 90% if you define failure as “the company did not meet the founder’s original financial expectations” (see our separate Blog post).

The famous American Vanderbilt family is a concrete, well-known example of the rich-to-poor phenomenon in the United States. Cornelius Vanderbilt died in New York in 1877 at the age of 80. At his death he was the richest person in the world. He had built up this fortune on his own without the initial advantage of a significant inheritance. In 1973, almost 100 years after the patriarch's death, the 120 direct descendants met at one Family reunion in New York. At this point in time, there was not a single millionaire left among the descendants - in money from 1973. The three main reasons for this almost unbelievable implosion of family wealth over about four generations: (1) concentrated investing that went wrong (materialized cluster risk), (2) splitting of wealth among many descendants in combination with an above-average birth rate in the family, (3) lavish lifestyles among too many family members.

Reason No. 1: The Vanderbilts had left most of the family fortune in the US railroad sector, where Cornelius had become fabulously rich through cleverness and hard work until his death. Shortly after Cornelius' death, however, the US railway sector went into permanent decline due to overcapacity and economic structural change combined with political decisions (which of course was not so easily visible in real time). [8] The Vanderbilts invested a smaller portion of the family fortune in the real estate sector on the American East Coast, with overall equally disastrous results.

If the Vanderbilts had started, from the first inheritance in 1878, to invest the existing gigantic family capital little by little in US stocks and to a smaller extent in government bonds, i.e. systematically reducing the enormous, as it turned out, fatal concentration risk in the family assets and instead diversifying broadly across hundreds of companies and all industries, some Vanderbilt descendants would still be billionaires and most would be multimillionaires today.

Preventing the Vanderbilts' addiction to extravagance, which is hardly believable, from the first generation after Cornelius onwards by setting up a family foundation (in the USA, a family trust) would also have helped.

The spectacular family fortune founded by John D. Rockefeller (1839-1937) developed not quite as catastrophically, but also remarkably negatively. Rockefeller, like Vanderbilt, was the richest American and probably the richest person in the world when he died. Relative to the value of its property in 1937, the Rockefeller family has managed to “eliminate” 97% of it in about 90 years (measured by the respective share of the US gross domestic product).

The fundamental difference between the “money mindset” and investment techniques, which is huge but not really understood by many (still) rich people get rich (wealth creation) and stay rich (Asset preservation and use of assets) we have here described in more detail.

Conclusion

Entrepreneurial cluster or concentration risks - often in connection with the attempt to increase returns by using the credit leverage effect (through debt-financed investing) - are the or one of the main destroyers of large family fortunes - either while the founding generation is still alive [9] or even stronger after the founding generation has transferred its ownership to the first subsequent generation. Because this is the case, reducing these cluster risks after the wealth accumulation phase has been completed is part of the “compulsory financial program” of a wealthy family if they want to maintain the wealth they have achieved across generations. The best way to do this is to invest an increasing percentage of total assets in globally diversified stock and bond investments, possibly supplemented with an optional moderate mix of gold and crypto investments.

Anyone who is additionally worried that their descendants will not be able or unwilling to handle the existing family assets responsibly could reduce or even completely eliminate this risk or concern with the vehicle of a family foundation.

Endnotes

[1] In bad years for the family wealth, the withdrawal was reduced (a common belt-tightening policy). Any withdrawals that were not made were made up for in the good years that followed.

[2] See entry “Forbes 400” in the English language Wikipedia.

[3] The now 96-year-old American economist Thomas Sowell drew attention to this failure in his publications decades ago. Apparently without success.

[4] The Green Heinrich is one of the most important educational and developmental novels in German literature of the 19th century.

[5] The book was published in its final version in 1879.

[6] “From rags [literally “rags”] to riches in three generations and back.”

[7] “Liquid investments” are investments in stocks, bonds, precious metals, raw materials, crypto currencies, bank deposits and financial products derived from these, such as. B. investment funds.

[8] These include the political decision not to charge tolls for the use of the highway system, which was greatly expanded in the first half of the 20th century.

[9] The former Austrian billionaire René Benko is a recent example from the German-speaking world.

literature

Arnott, Robert/William Bernstein/Lillian Wu (2015): “The Rich Get Poorer: The Myth of Dynastic Wealth”; Cato Institutes; Internet reference: www.cato.org

Bessembinder, Hendrik (2018): “Do Stocks Outperform Treasury Bills?”; in: Journal of Financial Economics 129 (3); pp. 440–457

Haghani, Victor/James White (2023): "The Missing Billionaires. A Guide to Better Financial Decisions"; Wiley Publishing (book)

Sosner, Nathan (2022): “When Fortune Doesn’t Favor the Bold – Perils of Volatility for Wealth Growth and Preservation”; in: The Journal of Wealth Management; winter 2022; Volume 25; No. 3

Williamson, Samuel H. et al. (2026): “Defining Measures of Worth – Most are better than the CPI”; Internet reference: https://www.measuringworth.com

This blog post is a slightly modified version of a section from our book, which will be published in June 2026 “Protecting assets intelligently: Effective strategies for reducing risk – a practical asset protection guide”.

The post From rich to poor happens more often than you think appeared first on Gerd Kommer.

]]>The post Precious metals as an admixture – does that make sense? appeared first on Gerd Kommer.

]]>Over the last ten years, gold has had an extraordinarily high return, which significantly exceeds the historically high return of the global stock market. Silver has outperformed both stocks and gold over the past decade.

Not surprisingly, media reports about gold and silver as investments have recently increased significantly.

At the end of January 2026, there was a brief price drop of 15% for gold and silver and almost 40% for silver (measured in euros). But both break-ins were only a short “scare moment”. So far they have remained lower than the price increases in the previous three weeks.

Reason enough for us to examine the question of the attractiveness of gold and the other three most important precious metals from an investor's perspective - silver, platinum and palladium - in this blog post. The focus of our analysis is on long-term historical data, supplemented by central factual arguments.

As we will see, the parallel analysis of the four most important precious metals in terms of investment alongside each other provides interesting insights and findings that an isolated examination of just gold or just silver would not have provided. (For gold individually, we already have a similar consideration, including a literature review, in an earlier one Blog post made.)

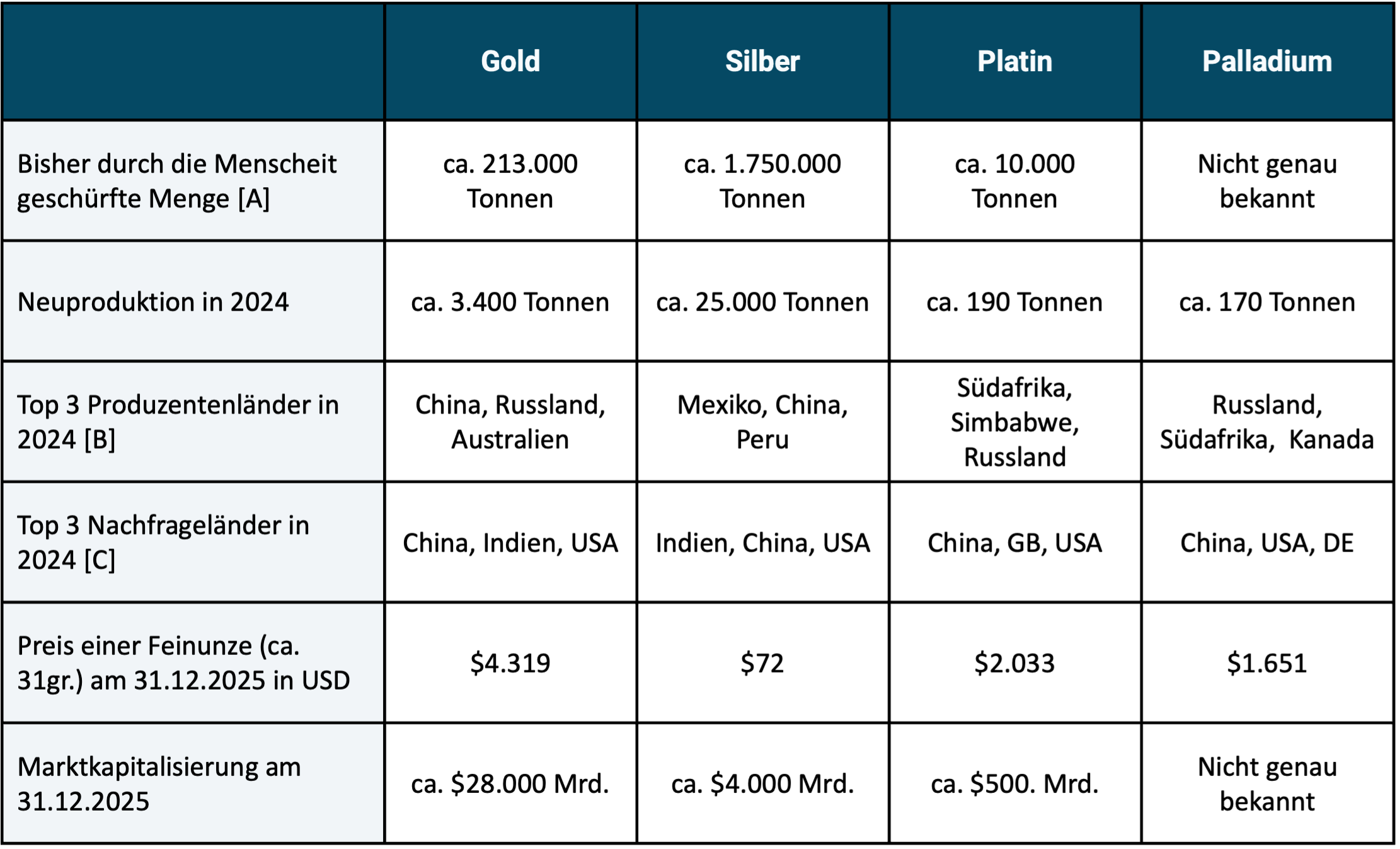

Before we start presenting the return data, here are some general real economic facts about the four precious metals that may not be known to everyone:

Table 1: Selected key real economic data for four precious metals

► All weight figures given are rough estimates from a number of different sources. ► [A] The volume that exists worldwide today and has been removed from the earth's crust by humans (“above ground stock pile”). ► [B] In order of production volume. ► [C] In order of demand volume.

There are a total of 15 precious and semi-precious metals. Curiously, according to Wikipedia, these two terms are not exactly the same in different cultures and languages, so they sometimes include different metals.

In investing practice, gold is the most important precious metal, which will surprise no one. In addition to gold, silver, platinum and palladium, the eleven other precious and semi-precious metals not discussed further in this blog post only play marginal roles in the investment market. [1]

Institutional investors and central banks essentially only invest in gold and little or no investment in silver, platinum and palladium.

The market capitalization of precious metals is small compared to that of the stock market and the bond market (see bottom row of Table 1). At the end of 2025, the global stock market had a market capitalization of approximately $130,000 billion (more than four times that of gold), the bond market had a market capitalization of $140,000 billion. At the end of 2025, Bitcoin had a market cap of approximately $1,700 billion (approximately one percent of that of the stock market).

As a private investor in Germany, you can easily invest in the four precious metals via ETFs, more precisely “ETCs” (Exchange Traded Commodities). The advantage of precious metal ETCs relative to direct investments is lower transaction costs (additional costs for buying and selling) with investment amounts (quantities) that are normal for private investors. Furthermore, with ETCs there are no costs for locker rental and insurance. They also offer greater convenience and operational security relative to direct investments. For example, the risk of loss due to theft or negligence is lower in the case of precious metal ETCs than with direct investments. Trading also takes place faster, which makes rebalancing in the overall portfolio easier. The costs (Total Expense Ratios/TERs) of the cheapest ETCs are reasonable. In the case of gold ETCs, they are particularly low.

Taxes on precious metal investments

For tax purposes, direct investments in all four precious metals in Germany are treated equally for private investors. There is tax exemption after a holding period of one year (“private sale transaction” according to Section 23 EStG); if sold before the end of 12 months, the normal income tax rate applies.

ETCs that physically hold the respective precious metal and include a so-called delivery claim (which is the case with many, but not all, precious metal ETCs sold in Germany) are treated just as favorably for private investors for income tax purposes as a direct investment.

Purchases of direct investments by private investors in silver, platinum and palladium are (unlike gold) subject to sales tax, i.e. 19% sales tax is due on the purchase. Precious metal ETCs do not have this disadvantage. (When selling direct investments, a private investor does not have to collect sales tax from the buyer.)

Silver, platinum and palladium are used industrially on a large scale, so they are real “raw materials”, not just pure investments. Apart from its use as a decorative metal, gold has virtually no commercial use. However, it is doubtful whether “jewelry” can be classified as “commercial/industrial use” at all, since in the two main demand countries for gold jewelry – India and China – it tends to play the same role in the population that gold bars and gold coins have in Western countries.

All three industrially used precious metals and gold are so valuable per unit of weight that the quantities once produced (mined) no longer disappear (e.g. in the trash), but remain permanently in circulation (stock) through recycling.

The historical returns of the four precious metals

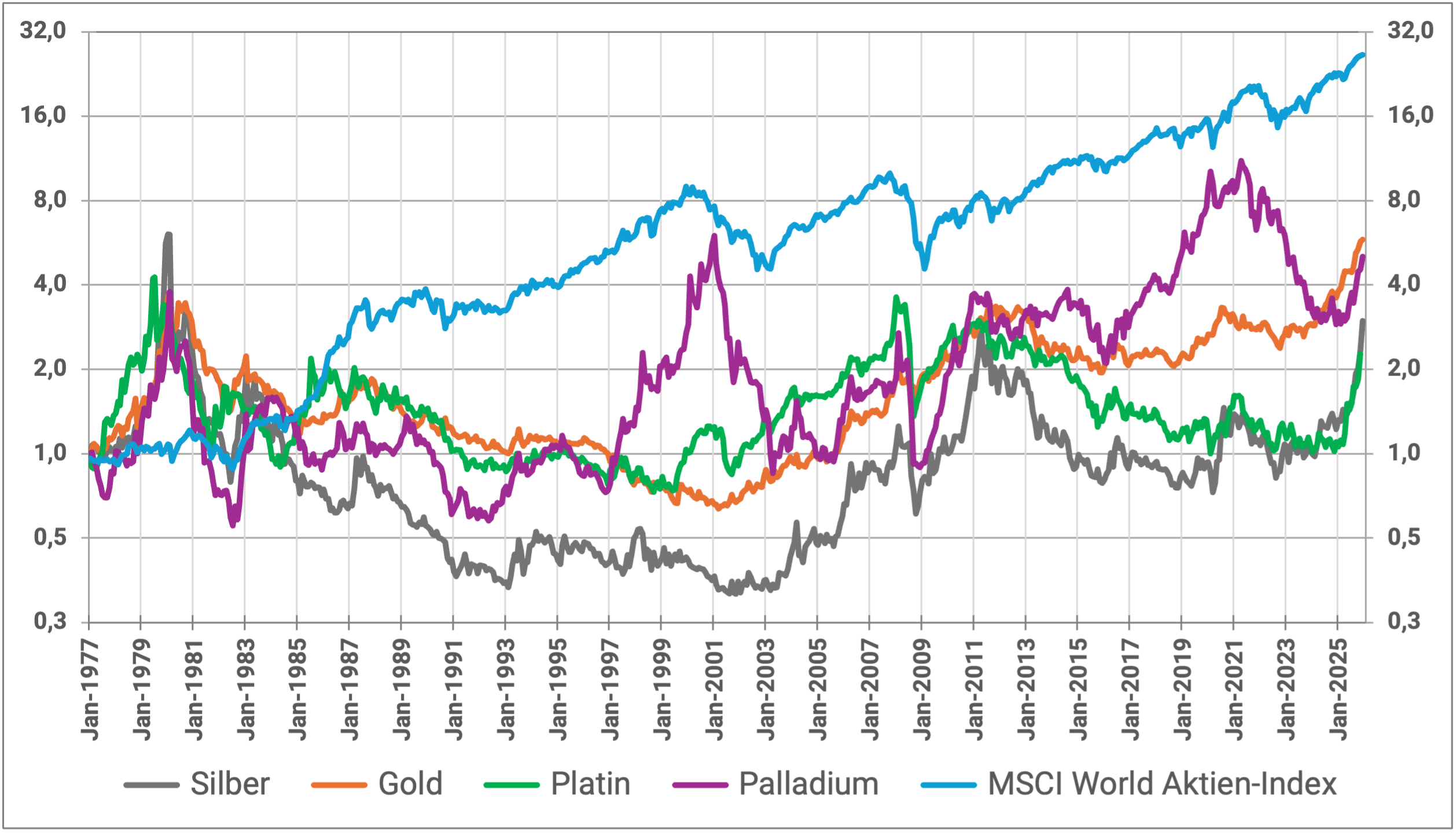

Let's move on to the investment aspect. Figure 1 shows the inflation-adjusted increases in the value of the four precious metals and the MSCI World stock index over the 49 years from the beginning of 1977 to the end of 2025. We chose the starting point in 1977 because monthly return data for palladium are only available from this point on. But even for gold, a historical investment analysis couldn't go back much further than 1977. Return data for gold before 1975 is ultimately not meaningful, as it was only at the end of 1974 that the decades-long Gold ban [2] was repealed in the USA. The corresponding gold bans in the countries China and India, which are extremely important for global gold demand, remained in place for a number of years after 1974. (Until the end of 1971, the price of gold in US dollars was set by the American government in the context of the so-called Bretton Woods monetary system, which resulted in a return in dollars of close to zero.)

Figure 1: Inflation-adjusted indexed price development of gold, silver, platinum, palladium and stocks (MSCI World Index) from 01-1977 to 12-2025 (49 years) in USD

► Data sources: Bloomberg, www.macrotrends.net, Dimensional Fund Advisors. ► Without costs and taxes.

In Figure 1 we use a logarithmic vertical scale. This ensures that a given percentage change in value from one time interval (month, year) to the next appears to the viewer to be the same size across the entire period (horizontal axis), which would not be the case with a linear vertical scale. If the goal is to analyze percentage returns and wealth gains over subperiods of a long overall period, logarithmic plots are less ambiguous.

The two main conclusions from Figure 1 are: Over the entire 49-year period, the MSCI World significantly outperformed the three precious metals. The numerical average returns are listed below in Table 2. The compound interest effect means that an average return advantage of stocks over gold of 3.3 percentage points per annum over these almost five decades results in a drastic final value advantage for stocks over precious metals (26.5 monetary units for stocks versus 6.6 monetary units for gold as the most profitable precious metal).

Risk indicators for the four precious metals in comparison with stocks

In addition, the return development of the stock portfolio was more consistent, both in the short and long term, and less volatile than that of the four precious metals. Table 2 illustrates this with three risk indicators and the risk-weighted return (Sharpe Ratio).

Table 2: Selected performance metrics for the four precious metals and stocks (inflation-adjusted returns in USD)

► Stock Global = MSCI World Index. ► [B] Simplified Sharpe Ratio = risk-weighted return (defined as arithmetic Ø return ÷ standard dev). ► [C] Maximum drawdown = maximum cumulative loss in the observation period. ► [D] Maximum drawdown date. ► [E] Maximum zero return period = longest period within these 49 years over which there was a real zero return. ► All data source: See Fig. 1. ► Excluding costs and taxes.

Table 2 provides further interesting insights:

Over the 49-year period, gold has been the best-performing of the four precious metals, but not in the last ten years. If further multi-year sub-periods were shown (which we do not do for reasons of space), the gold return would only be in first place in a minority and in second place or further down in a majority.

In the case of palladium, the relatively high long-term return within the group of four seems remarkable. It was only slightly below that of gold. What stands out about silver is its spectacular returns over the last decade.

In terms of risk, gold tends to rank first (best) among metals. However, the relative risk balance of gold does not appear to be “flawless”: First of all, gold (like the other precious metals) is noticeably riskier than the global equity investment class.

Gold's volatility of returns and maximum drawdown (MDD) are better than those of the other three metals, but at the Maximum Zero Return Period metric [3] Gold performs worse than palladium.

The periods listed in Table 2 for precious metals at the maximum zero return period may seem shockingly long to some observers. However, the numbers are correct. The reason for the high MNRP values is the inflation adjustment of returns combined with the high volatility of precious metal returns. Let's take gold as an example: Gold had an all-time high of $850 per ounce in January 1980, which in today's money (monetary value at the end of 2025), i.e. "inflated", corresponds to around $3,500. However, gold did not actually exceed this price again until August 2024 after 45 agonizingly long years. The situation was similar with the other three precious metals. Only palladium performs noticeably better here with a maximum zero return period of “only” 20 years (1980 to 2000).

Precious metals for diversification in an equity-heavy portfolio

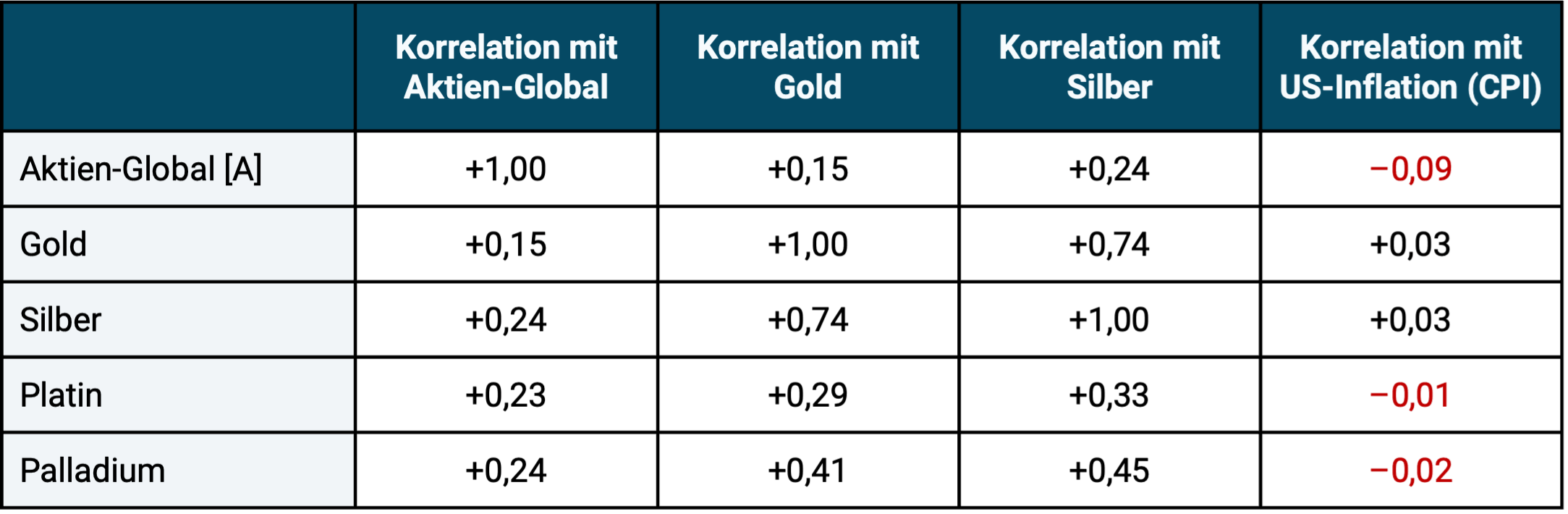

In Table 3 we take a look at the correlations. We want to use them to measure how well the four precious metals are suitable for diversification in an equity-heavy portfolio.

The quality of the inflation can be determined from the correlation with inflation (far right column). Inflation hedging-Derive characteristics of individual investments. [4]

Table 3: Correlation of precious metals with stocks, with inflation and with each other

► Global stocks = MSCI World Index. ► Data source: See footnotes to Figure 1.

What insights emerge from Table 3? All precious metals have a low correlation with the equity global asset class. From a pure diversification perspective, all four metals tend to be well suited to reducing the risk (volatility) of a pure stock portfolio. However, to be considered a “good diversifier” you need low correlation and attractive returns.

Platinum and palladium correlate relatively moderately with gold and with silver. Palladium therefore appears suitable for diversifying the risk (volatility) of gold (low correlation with almost the same long-term return). Platinum shows an even lower correlation to gold, but has a weak historical return.

In addition to pure correlation analysis, we also looked at the seven periods between 1977 and 2025 in which the MSCI World Index suffered an inflation-adjusted drawdown of 20% or more [5] and checked which of the four precious metals was the best stock hedge overall in these seven stock market declines, i.e. which fell less than the stock market or perhaps even had positive returns. Even in this diversification test, which is not shown separately using figures, gold performed best among the four metals.

One reason for gold's overall better performance in times of crisis could be that the three other precious metals each have extensive industrial commercial uses. When economies in major industrialized countries weaken (as is often the case during negative stock market returns), their industrial demand also tends to suffer.

The supposed inflation protection of precious metal investments

All four precious metals as well as Equity Global have a correlation close to zero with consumer goods inflation. Therefore, on average over the last 50 years, none of these investments was a good inflation hedge (hedge = protection). The statement that has been heard over and over again in the financial industry, by financial journalists and by finfluencers since time immemorial, that gold and stocks offer “good protection against inflation” is ultimately nonsense. We are not the first in the professional world to notice this. Many believe that an investment that produces a higher nominal return than inflation over the long term therefore offers “inflation protection”. However, this long-term “inflation beating” that every asset class provides is not what scientists understand by “inflation protection” or “inflation hedging”. Inflation hedging and inflation beating are two different things.

In Table 4 we illustrate how well each of the four precious metals performed as an admixture (diversifier) for a global equity portfolio over the period under review.

Table 4: How well do the four precious metals work as diversifiers for an equity-heavy portfolio (inflation-adjusted returns in USD)

► [A] Vola = annualized standard deviation of monthly returns. ► [B] Simplified Sharpe Ratio: See footnotes to Table 1. ► Data source: See footnotes to Figure 1.

The conclusions from Table 4 are also interesting:

A precious metal admixture of 10% with regular mechanical rebalancing has either slightly improved, left unchanged or only moderately worsened the absolute return relative to a 100% stock portfolio for all four precious metals over the period under review from 1977 to the present. In the last 10 years, the diversifier balance sheet was a little better than in the entire period.

The differences in returns for the entire period in Table 4, which may seem implausible at first glance, are correct, e.g. B. that the 90/10 palladium portfolio has a higher return than the 100% stock portfolio, even though palladium's return individually was quite significantly lower than that of gold. The respective differences between the four 90/10 portfolios are also correct. These effects result from the low correlation of the four precious metals to stocks and probably also from the specific historical return profile over these 49 years. The effect is known in the literature as “diversification return” or “rebalancing premium”. For very low correlated assets and widely varying component weights (here 90% versus 10%), the return of the mixed portfolio can be slightly higher than the return of the larger component. [6]

The additions resulted in slight improvements across the two risk indicators (volatility and maximum drawdown).

In terms of risk-weighted returns (simplified Sharpe ratio), the mixed portfolios also consistently performed slightly better than the 100% equity portfolio.

Although the differences in Table 4 seem rather small at first glance, gold still crosses the finish line as a relatively clear winner in the “Best admixture among the four precious metals” competition for the following reasons:

- When it comes to long-term returns, gold is well ahead of silver and platinum. Only palladium comes close to gold here.

- When it comes to risk, the differences between the four precious metals appear to be rather small. All four also perform similarly in terms of their diversification properties in an equity-heavy portfolio. Only the addition of gold shows slightly lower volatility and a slightly better maximum drawdown.

- Gold's market capitalization is by far the largest, which could potentially be an advantage relative to the three other metals in a truly severe global crisis.

- All four precious metals have tax advantages for private investors in Germany, both as a direct investment and as an ETC (provided the ETC is physically replicating and includes a “delivery claim”). In the case of a direct investment, however, there is only no sales tax on gold. (However, it is uncertain whether the tax exemption for gold according to Section 23 EStG will remain in place in the future.)

- Gold ETCs predominantly have lower ongoing costs (TERs) than ETCs on the three other metals.

For precious metals enthusiasts among retail investors, a palladium ETC could be a worth considering diversifier for a gold investment (replacing part of the gold investment with palladium) based on data from 1977 to today. However, this assumes that the investor is not afraid of the additional complexity that comes with it.

In our analysis, it should not be forgotten that the fundamentally high price volatility for all four metals means that the rather small differences in returns could also have been a coincidence. Given the high volatility, a statistician would complain that gold's return advantage is not “statistically significant”, i.e. not sufficiently reliable. For example, if you were to split the 49 year data into two halves, the picture would look quite different in the two half periods, which is why caution is required when interpreting.

The current valuation level of precious metals

For investment assets that do not generate current income (no current cash flows), such as precious metals, conventional raw materials, collectibles and Bitcoin, the fundamental valuation methods commonly used in economics are not applicable. An alternative valuation indicator for such non-yielding assets is the ratio of their current price to the inflation-adjusted historical average price. We show this rough evaluation indicator in Table 5.

By this standard, two of the four precious metals are expensive today, namely gold and silver. One thing is very cheap: platinum. Palladium is moving relatively marginally above its historical average real price. Looking forward, high valuations tend to lead to lower future returns.

Table 5: The current valuation level of the four precious metals – multiple of the inflation-adjusted average price since 1977 (in USD)

► “Current valuation level”: Ratio of the price for one troy ounce on January 31, 2026 relative to the average inflation-adjusted (“inflated”) price since January 1977. Reading example: On January 31, 2026, the gold price was 165% above its inflation-adjusted historical average since 1977. ► Data sources: See footnotes to Figure 1.

Naturally, such considerations (taking into account the current valuation level) are irrelevant for anyone who believes that they can predict the price development of these precious metals in the relevant future with sufficient reliability or for someone who believes that due to future economic or political developments, the already very high prices of gold and silver will continue to rise sharply. We consider such a forecast claim to be unrealistic and, if implemented in the form of market timing, ultimately detrimental to returns. We also do not believe that the high returns of gold and silver over the past 15 years will be achieved on average over the next 15 years.

Reasons for the high price increases of gold in the recent past

For gold, the very high price increases in recent years are usually justified by high and rising national debt ratios, extensive gold purchases by central banks (because they are reducing dollar bonds in their reserves and partially replacing them with gold) as well as a “new distrust” of a growing part of the population in “the elites” and the “FIAT monetary system” (this distrust is expressed with gold purchases). However, even if this is a correct identification of the main price-driving factors, the information and knowledge about these factors are probably already priced in today. From our point of view, how they will develop in the short and medium-term future and thus how the gold price will develop in the short and medium term is unknown today.

The fact that the current weakness of the dollar should be a relevant advantage for the returns of gold and other precious metals is a common misconception that we here (see “Question 9”) and here refute.

Conclusion

None of the four precious metals examined here have historically had long-term returns as high as stocks.

Of the four precious metals, gold was the most profitable in the roughly 50 years from 1977 to 2025. When it comes to long-term returns, palladium – which may come as a surprise – came in a close second.

Gold and silver currently appear to be highly valued, i.e. expensive, while platinum is cheap and palladium is close to the average price. From a statistical perspective, a high rating reduces the forward trend expected return relative to the high returns of recent years.

Overall, gold was the lowest-risk precious metal during the period under review. It also has the lowest correlation to the global stock market and was the best stock diversifier overall in the seven strong stock market down periods since 1977.

For private investors, there is a sales tax disadvantage relative to gold in the case of direct investments (not in ETCs) for silver, platinum and palladium.

Gold also performs best on balance among the four precious metals when it comes to the additional costs of investing.

So gold goes in the competition “who is the (relatively) best admixture?” clearly emerged as the winner. In our opinion, second place is not silver, as some might have expected, but palladium.

In the long term, a gold admixture is unlikely to increase the return relative to “100% stocks” and may even lower it somewhat, but it can moderately improve the risk profile of the overall portfolio.

Anyone who looks at precious metals individually, i.e. not at the aggregated effects in an overall portfolio with a precious metal admixture, must be able to cope with their high drawdowns and extremely long periods of zero returns as an investor. This is only likely to work long-term for most private investors - i.e. not result in harmful panic selling - if the percentage of (all) precious metals in their total asset portfolio is relatively low - e.g. B. a maximum of 10 percent.

Endnotes

[1] See German Wikipedia, article “Precious metals”. In addition to the four metals shown here, the following are among the 15 precious and semi-precious metals: iridium, osmium, mercury, polonium, rhodium, ruthenium, bismuth, technetium, rhenium, antimony and copper.

[2] The ban on private households owning gold existed for several decades in many capitalist and communist countries in the 20th century. A violation was usually punished with harsh and, in some states, draconian penalties. See article “Gold ban” in the German Wikipedia.

[3] Maximum NRP = Longest period within these 49 years in which there was a real zero return.

[4] A brief explanation of the “correlation” metric can be found at the end of this blog post.

[5] These include the crashes in October 1987, the dot-com crash (beginning of the noughties), the Great Financial Crisis (from 2007), the Covid crash (2020), the Ukraine war and interest rate change crash (2022).

[6] See e.g. B. Hallerbach, Winfried (2016): “Disentangling Rebalancing Return”, December 10th. 2016, Internet reference: Social Sciences Research Network/SSRN.

Infobox: Correlation – a quick explanation

Correlation is a key figure from statistics that measures the degree of parallelism in the development of two variables (series of numbers), for example the price changes of two securities or two asset classes over time. Correlation is measured in the form of the correlation coefficient, which ranges between +1.0 and -1.0, where +1 stands for complete correlation (exact parallel development), 0 for completely independent (or random) development and -1 for exactly opposite development. The lower the correlation between two financial assets, the more suitable they are for diversification in a portfolio, all other things being equal. Just like returns, correlations also fluctuate over time, but to a lesser extent.

The post Precious metals as an admixture – does that make sense? appeared first on Gerd Kommer.

]]>The post “Homeowners are wealthier than renters in old age” – lies with statistics appeared first on Gerd Kommer.

]]>In this blog post we look at a specific old wives' tale about the financial attractiveness of owner-occupied residential properties, which has been re-proclaimed "twice a year" by most media in Germany and by the real estate industry for decades with headlines such as the following:

- „Property owners have significantly more money in old age than tenants“ – Headline of an article in the news magazine Spiegel from January 13th, 2025

- „Pensioners who own their own home are particularly wealthy“ – Headline of an article on the news portal t-online.de from December 17th, 2025

- „Homeowners accumulate more wealth than renters“ –Press release from the Association of Private Building Societies in 2025.

However, the statement “own-occupied home leads to higher wealth in old age than renting” is not far from the truth. The statement is a picture-perfect case of “lying with statistics.” [1]

Lying by concealing essential information

As we know, you can lie in many ways. One of them is that person A (the liar) formulates a statement B correctly, but deliberately omits essential information in order to cause a false understanding or error on the part of addressee C. So A lures C into a comprehension trap by omitting crucial information from statement B. That is the lie. Children can already master this method. In English it has a nice compact name Context Dropping used.

Context dropping – lying by deliberately omitting, i.e. suppressing crucial additional information – happens when the statement “Pensioner with his own home [2] are statistically wealthier than pensioners who rent.”

Below we show how this deception actually works. The claim that home ownership is among older households causal for a higher net worth (as conveyed in the exemplary publications cited at the beginning through manipulative context dropping), we will henceforth call “the real estate lie”. [3]

At first glance - without the correct context - the real estate lie in question appears to be true: homeowners actually have a statistically higher net worth in old age than renter households. This is shown by the relevant data and no one doubts its formal correctness.

But the crux of the matter: the statistical wealth advantage of homeowner households (EHBs) over renter households has nothing to do with owning their own home. It is entirely due to other causes. So here correlation is confused or swapped with causation. Yes, EHB households are generally wealthier as they get older than renter households, but they Caused This asset advantage is not the home.

Here is an illustration of the manipulative swapping of cause and effect Real estate lie: The wealth of the average Ferrari-owning household in Germany (around 14,500 households) naturally exceeds that of the average non-Ferrari-owning household (around 41 million). Now the question: Was the Ferrari the cause of this wealth advantage? Of course not. The Ferrari has statistically reduced this wealth advantage - without it, the wealth advantage of the Ferrari households would be even greater. Either way, Ferrari ownership was the result of the income and wealth advantage, not its cause. It's the same with home ownership. It is the consequence, not the cause, of a number of actual causal factors.

The real causes of homeowners' wealth advantage

The “real estate propagandists” are betting that their recipients will fall for the manipulated statement and misunderstand correlation as causality.

However, as scientific research shows quite clearly, the actual causes of the wealth advantage of EHB households are as follows: [4]

1) EHB households have a higher lifetime income, i.e. h. the sum of their net income over the entire period of earning capacity is statistically higher than for renter households. The proportion of households with two incomes is higher among EHB households than among renter households.

2) EHB households have a higher percentage propensity to save. A higher percentage of their net income, which is already higher in absolute terms (see number 1), goes into wealth creation than is the case with renter households. This higher propensity to save is also expressed in the willingness to submit to a “positive compulsory savings contract” that is linked to the loan-financed purchase of a home. More on that below.

3) EHBs are more risk-averse in their investment behavior and therefore achieve statistically higher long-term returns in their wealth creation away from their own home. This increased willingness to take risks is also reflected in the higher entrepreneurial rate among EHB households than among renter households (starting a business and entrepreneurship are very risky). The higher risk affinity is probably due, among other things, to the proven higher average financial literacy of EHB households.

4) EHBs receive more frequent, larger and earlier wealth transfers from their parents and grandparents through gifts and inheritances. This often happens by “subsidizing” the equity share when the EHB household first purchases property when it is young.

5) EHB households have lower divorce rates than renter households. Divorces often cause serious financial losses for those involved. We show why and how these asset losses happen here.

6) If a home investment fails individually - for example due to a combination of unemployment and excessive debt - the affected households often lose their home through seizure or forced sale and become renter households again. Paradoxically, particularly poor home investments contribute to the “home ownership lie” analyzed here.

Note that in the list and description of the six main causes of the higher wealth of EHB households, we did not say anything about Why These households have higher incomes, higher savings rates, greater willingness to take risks, higher financial literacy or lower divorce rates. Quite obviously, a large part of these wealth-promoting factors lies in the socialization of the people concerned; a small part could also be genetically determined.

Would you compare tenant groups with EHB groups where the six causes listed above no If there were a difference, it would be shown that renters statistically achieve higher or similar levels of wealth in retirement. [5]

Why higher wealth? Quite simply because renting in conjunction with other forms of wealth creation - above all with a simple, broadly diversified stock portfolio on a buy-and-hold basis - leads to a higher net final wealth than an owner-occupied property in the majority of time frames if the financial-mathematically correct comparison is made. Furthermore: The relative final asset advantage of the “rent + capital market investment” constellation will tend to be greater, the higher the loan share (“leverage”) is in the comparison EHB. We at GKI have shown this for Germany and others for other countries - see here and here.

We probably don't need to explain in detail at this point why the real estate lie has been spread again and again by real estate agents, property developers, real estate influencers and banks for decades. These parties earn directly or indirectly from real estate purchases or their financing.

The “compulsory savings contract” for real estate

In connection with the correlation phenomenon of the higher net wealth of EHB households in old age relative to renters, it is often even said that not People with conflicts of interest, i.e. “people without a real estate agenda”, argue that the higher net assets of EHB households are based to a large extent on the phenomenon of the “positive compulsory savings contract”. This means that an EHB household that, for example, has taken out a loan for 80% of the acquisition costs is obliged to pay the corresponding expenses (loan installments, property tax, insurance, maintenance) month after month until it has been completely repaid - typically after 25 years or more. Otherwise there is a risk that the property will be seized by the bank. Above all, the repayment element in debt service contributes directly to wealth creation: with every euro of repayment, the percentage of equity in the property increases.

A tenant household is not under a comparable pressure to save, according to the theory of the positive compulsory savings contract. As a result, tenant households will often save less overall or temporarily interrupt their savings over a 25-year period for consumption purposes.

Here too, the confusion/swapping of correlation and causality probably plays a role. People with a naturally high tendency to save are represented more frequently among EHB households than among renter households. This is probably because their pre-existing strong willingness/inclination to save makes it easier for them to accept the long-term reduction in consumption that comes with the “compulsory home savings contract”. These EHB households would not have been able to purchase their own home for certain reasons [6] or if they had viewed a home as a comparatively unattractive investment, the majority of them would have been just as disciplined and saved for the long term in other asset classes. So if you look behind the façade of formalities, you can't even speak of "compulsion" for most people or households who submit to the supposed "compulsory" savings contract, because they would save even without real estate.

What does the development of the “homeownership ratio” tell us?

If you realize that in almost all countries in the world and especially in Germany, wealth creation through owner-occupied residential real estate is financially supported by the state more strongly through taxation and transfer payments (cash benefits) than any other form of private wealth creation, and if you assume for a moment - incorrectly - that owner-occupied real estate systematically produces high returns on equity, then the homeownership ratio (HOR) in most countries would have to continue to rise over time. [7]